|

市場調查報告書

商品編碼

2062482

石墨烯電池:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)Graphene Battery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

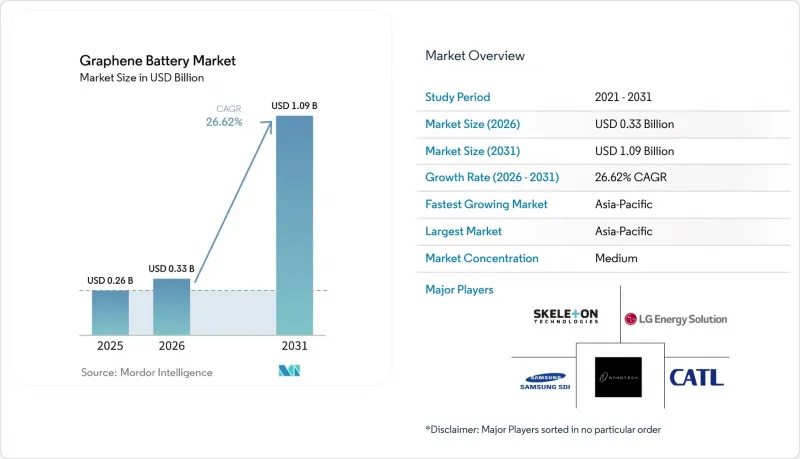

根據 Mordor Intelligence 預測,石墨烯電池市場規模預計在 2025 年達到 2.6 億美元,在 2026 年達到 3.3 億美元,在 2031 年達到 10.9 億美元。

預計從 2026 年到 2031 年,其複合年成長率將達到 26.62%。

本報告按類型(鋰離子石墨烯電池、石墨烯超級電容、鉛酸石墨烯電池等)、應用(汽車、消費性電子、儲能、工業機器人和機械等)以及地區(北美、歐洲、亞太、南美、中東和非洲)進行細分。市場預測以美元計價。

全球石墨烯電池市場趨勢及洞察

電動車主導的需求擴張

諸如中國的雙軌制政策、歐盟2035年前逐步淘汰引擎的計劃以及加州的“先進清潔汽車II”法規等零排放法規,都要求汽車製造商在20分鐘內實現80%的充電率。石墨烯能夠降低電荷轉移電阻,從而在不發生過熱的情況下實現3C或更高的充電電流。 2026年3月對塔塔Nexon電動車進行的一項模擬表明,添加石墨烯可將充電速度提高22%至27%,並將電池溫度降低高達15°C。三星的石墨烯球塗NCM正極材料即使在4.5V電壓下循環100次後仍能保持97.3%的容量,展現了其在高功率下的耐久性。對於車隊營運商而言,其優勢包括更小的電池組、更低的負載重量以及因機器充電而減少的怠速時間。這些因素共同促成了石墨烯電池市場成為短期內滿足法規要求並實現整體擁有成本(TCO)目標的關鍵推動因素。

卓越的能量密度和超快充電速度

石墨烯高達2630 m²/g的表面積和超過10000 cm²/V*s的載子遷移率,能夠同時提升活性材料的填充效率和電子傳輸效率。莫納什大學研發的多尺度還原氧化石墨烯超級電容實現了99.5 Wh/L的能量密度和69.2 kW/L的功率輸出,展現出與鉛酸電池相當的性能,同時保持了超級電容的輸出特性。 2026年1月發布的雷射預鋰化矽-石墨烯負極,在5 A/g的電流密度下,容量超過1700 mAh/g,且在2000次循環後容量衰減小於2%。 GMG公司的鋁離子軟包電池在3.2分鐘內充電至62%,目標是在6分鐘內完成充滿,這表明石墨烯有望為低成本、非鋰基化學系統鋪路。這些突破性成果證明,石墨烯不僅可以改善鋰離子電池的性能,而且還為其他化學系統打開了大門。

石墨烯材料高成本

高純度石墨烯的成本仍然會使電極添加劑的成本翻倍,從而擠壓入門級電動車和消費性電子產品的利潤空間。寧德時代(CATL)在2025年預測,採用尖端材料的硫化物基固態電池的成本將是傳統鋰離子電池的3到5倍。在氧化石墨烯的成本達到與奈米碳管相當的水平之前(可能在2028年左右),其應用將僅限於高階細分市場,這將使石墨烯電池市場的成長受到約4.5個百分點的限制。

細分市場分析

到2025年,鋰離子石墨烯電池將佔總銷售量的54.1%,現有NCM和LFP產品線中逐步引入1-5%(重量比)石墨烯添加劑的趨勢十分明顯。固態電池仍處於發展階段,預計將以37.0%的複合年成長率成長,因為石墨烯塗層能夠穩定硫化物電解並抑制枝晶形成,從而提高電池能量密度,最終達到500 Wh/kg的目標。

石墨烯超級電容雖然體積小巧,但在石墨烯電池市場中佔有重要的戰略地位。莫納什大學研發的99.5 Wh/L軟包電池已證明,其輸出功率可達69.2 kW/L,同時保持與鉛酸電池相當的體積能量密度。新興的鋁離子和鋰硫電池體系則構成「其他」類別。 GMG公司的鋁離子軟包電池可在6分鐘內完成充電,而Lyten公司的3D石墨烯鋰硫正極材料已於2024年交付汽車進行測試。隨著整合技術的成熟,這些替代化學體系中石墨烯電池的市場規模預計將會擴大,從而帶來除傳統鋰離子電池之外的多元化收入來源。

區域分析

預計到2025年,亞太地區將佔全球需求的44.9%,並將在2031年之前以27.8%的年均速度成長,這主要得益於中國和韓國石墨礦、石墨烯合成和電池組裝設施的集中。寧德時代(CATL)藍圖在2027年實現500 Wh/kg全固體原型,這正是主要企業如何利用石墨烯大幅突破性能極限的絕佳例證。

儘管北美在產量上落後於其他地區,但在公共資金投入方面卻遙遙領先。美國能源局對萊頓公司鋰硫電池先導計畫和空軍二氧化碳製石墨計畫的支持,體現了出於國家安全考量而對供應多元化的重視。加拿大NanoXplore公司獲得的用於研發高功率圓柱形電池的津貼,進一步鞏固了該地區在小眾高價值應用領域的地位。

歐洲透過GRAPHERGIA等資助聯盟確立了其在該領域的地位,旨在透過軟性超級電容和乾電極鋰離子電池,將石墨烯電池的技術成熟度從3-4級提升至5級。澳洲昆士蘭州的計畫將關鍵礦產資源與高價值鋁離子電池的先導工廠相結合,而印度的生產連結獎勵計畫計畫則吸引國內石墨烯供應商加入電池生產線。整體而言,石墨烯電池市場受益於亞洲的市場規模、北美國防相關資金以及歐洲法規和研發的推動作用。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 電動車主導的需求擴張

- 卓越的能量密度和超快充電速度

- 政府對研發的津貼措施

- 降低石墨烯的生產成本

- 與全固態電池架構的整合

- 在高功率無人機和航太領域的應用。

- 市場限制因素

- 石墨烯材料高成本

- 商業規模生產能力短缺

- 化學氣相沉積石墨烯薄片的質量差異

- 奈米顆粒釋放帶來的環境與安全問題

- 供應鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按類型

- 鋰離子石墨烯電池

- 石墨烯超級電容

- 石墨烯鉛酸電池

- 固體石墨烯電池

- 其他

- 透過使用

- 車

- 家用電子產品

- 儲能

- 工業機器人與機械

- 航太/國防

- 其他

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 北歐國家

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 東南亞國協

- 其他亞太國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

- 埃及

- 其他中東和非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢(併購、聯盟、購電協議)

- 市場佔有率分析(主要公司的市場排名和佔有率)

- 公司簡介

- Samsung SDI Co. Ltd.

- LG Energy Solution Ltd.

- Nanotech Energy Inc.

- Skeleton Technologies OU

- Contemporary Amperex Technology Ltd.(CATL)

- Panasonic Holdings Corp.

- Huawei Technologies Co., Ltd.

- Talga Group Ltd.

- NanoXplore Inc.

- Graphene Manufacturing Group Ltd.

- XG Sciences Inc.

- Lyten Inc.

- Vorbeck Materials Corp.

- Cabot Corporation

- ZEN Graphene Solutions Ltd.

- Grabat Energy SA

- Real Graphene USA

- Tesla Inc.

- EnGraphene Inc.

- Graphenano SA

第7章 市場機會與未來展望

According to Mordor Intelligence, the graphene battery market size is projected to be USD 0.26 billion in 2025, USD 0.33 billion in 2026, and reach USD 1.09 billion by 2031, growing at a CAGR of 26.62% from 2026 to 2031.

This report is Segmented by Type (Lithium-Ion Graphene Batteries, Graphene Supercapacitors, Lead-Acid Graphene Batteries, and More), Application (Automotive, Consumer Electronics, Energy Storage, Industrial Robotics & Machinery, and More), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Graphene Battery Market Trends and Insights

EV-led Demand Acceleration

Zero-emission mandates such as China's dual-credit policy, the EU's 2035 engine phase-out, and California's Advanced Clean Cars II rule are forcing automakers to meet 80% state-of-charge targets in under 20 minutes . Graphene lowers charge-transfer resistance, enabling 3C-plus currents without runaway heat. A March 2026 simulation of a Tata Nexon EV showed 22-27% faster charging and up to 15 °C lower cell temperatures when graphene was added. Samsung's graphene-ball-coated NCM cathode retained 97.3% capacity after 100 cycles at 4.5 V, confirming durability under high power . Fleet operators benefit because smaller packs or opportunity charging cut payload weight and idle time. Together, these factors position the graphene battery market as a near-term enabler for regulatory compliance and total-cost-of-ownership goals.

Superior Energy Density & Ultra-Fast Charging

Graphene's 2,630 m2/g surface area and carrier mobility above 10,000 cm2/V*s simultaneously raise active-material loading and electron transport. Monash University's multiscale reduced graphene oxide supercapacitor delivered 99.5 Wh/L and 69.2 kW/L, rivaling lead-acid while keeping supercapacitor power. A January 2026 laser-prelithiated silicon-graphene anode surpassed 1,700 mAh/g at 5 A/g with <2% fade over 2,000 cycles. GMG's aluminum-ion pouch cell hit 62% charge in 3.2 minutes and targets a full 6-minute charge, demonstrating how graphene opens non-lithium chemistries at lower cost. These milestones prove that graphene not only upgrades lithium-ion but also unlocks alternative chemistries.

High Cost of Graphene Materials

High-purity graphene still doubles electrode additive cost, squeezing margins in entry-level EVs and consumer electronics. CATL noted in 2025 that sulfide solid-state cells with advanced materials run 3-5 times the cost of conventional lithium-ion. Until reduced graphene oxide reaches parity with carbon nanotubes, likely by 2028, adoption will cluster in premium niches and curb the graphene battery market expansion by roughly 4.5 percentage points.

Other drivers and restraints analyzed in the detailed report include:

- Government R&D Funding Incentives

- Declining Graphene Production Costs

- Limited Commercial-Scale Manufacturing Capacity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Lithium-ion graphene batteries held 54.1% revenue share in 2025, underlining the preference for incremental 1-5 wt% graphene additives in established NCM and LFP lines. Solid-state variants, though nascent, are forecast to expand at a 37.0% CAGR because graphene coatings stabilize sulfide electrolytes and suppress dendrites, raising cell energy toward 500 Wh/kg targets.

Graphene supercapacitors occupy a small yet strategically important corner of the graphene battery market. Monash University's 99.5 Wh/L pouch cell proves volumetric energy can rival lead-acid while delivering 69.2 kW/L power. Emerging aluminum-ion and lithium-sulfur chemistries form the "Others" bucket; GMG's aluminum-ion pouch cell charges in six minutes, and Lyten's 3D-graphene lithium-sulfur cathodes shipped for automotive tests in 2024. As integration techniques mature, the graphene battery market size for these alternative chemistries is expected to widen, offering diversified revenue streams beyond conventional lithium-ion.

Geography Analysis

Asia-Pacific generated 44.9% of global demand in 2025 and is projected to grow at 27.8% through 2031, thanks to integrated graphite mines, graphene synthesis, and cell assembly hubs in China and South Korea. CATL's roadmap toward 500 Wh/kg solid-state prototypes by 2027 exemplifies how local champions use graphene to leapfrog performance ceilings.

North America trails in volume but leads in public funding. The U.S. DOE's backing for Lyten's lithium-sulfur pilot and the Air Force's CO2-to-graphite project indicate security-driven interest in supply diversification. Canada's NanoXplore grant for ultra-high-power cylindrical cells further cements the region's role in niche, high-value applications.

Europe positions itself through consortium funding like GRAPHERGIA, aiming to lift technology readiness from 3-4 to 5 via flexible supercapacitors and dry-electrode lithium-ion cells . Australia's Queensland program links critical mineral reserves to value-added aluminum-ion pilot plants, while India's Production-Linked Incentive schemes draw domestic graphene suppliers into battery lines. Overall, the graphene battery market benefits from Asia's scale, North America's defense capital, and Europe's regulatory and R&D pull.

- Samsung SDI Co. Ltd.

- LG Energy Solution Ltd.

- Nanotech Energy Inc.

- Skeleton Technologies OU

- Contemporary Amperex Technology Ltd. (CATL)

- Panasonic Holdings Corp.

- Huawei Technologies Co., Ltd.

- Talga Group Ltd.

- NanoXplore Inc.

- Graphene Manufacturing Group Ltd.

- XG Sciences Inc.

- Lyten Inc.

- Vorbeck Materials Corp.

- Cabot Corporation

- ZEN Graphene Solutions Ltd.

- Grabat Energy S.A.

- Real Graphene USA

- Tesla Inc.

- EnGraphene Inc.

- Graphenano S.A.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 EV-led demand acceleration

- 4.2.2 Superior energy density & ultra-fast charging

- 4.2.3 Government R&D funding incentives

- 4.2.4 Declining graphene production costs

- 4.2.5 Integration with solid-state battery architectures

- 4.2.6 High-power UAV & aerospace adoption

- 4.3 Market Restraints

- 4.3.1 High cost of graphene materials

- 4.3.2 Limited commercial-scale manufacturing capacity

- 4.3.3 Inconsistent quality in CVD graphene flakes

- 4.3.4 Environmental & safety concerns over nano-emissions

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Type

- 5.1.1 Lithium-ion Graphene Batteries

- 5.1.2 Graphene Supercapacitors

- 5.1.3 Lead-acid Graphene Batteries

- 5.1.4 Solid-state Graphene Batteries

- 5.1.5 Others

- 5.2 By Application

- 5.2.1 Automotive

- 5.2.2 Consumer Electronics

- 5.2.3 Energy Storage

- 5.2.4 Industrial Robotics and Machinery

- 5.2.5 Aerospace and Defense

- 5.2.6 Others

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 NORDIC Countries

- 5.3.2.6 Russia

- 5.3.2.7 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 ASEAN Countries

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 South Africa

- 5.3.5.4 Egypt

- 5.3.5.5 Rest of Middle East and Africa

- 5.3.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Samsung SDI Co. Ltd.

- 6.4.2 LG Energy Solution Ltd.

- 6.4.3 Nanotech Energy Inc.

- 6.4.4 Skeleton Technologies OU

- 6.4.5 Contemporary Amperex Technology Ltd. (CATL)

- 6.4.6 Panasonic Holdings Corp.

- 6.4.7 Huawei Technologies Co., Ltd.

- 6.4.8 Talga Group Ltd.

- 6.4.9 NanoXplore Inc.

- 6.4.10 Graphene Manufacturing Group Ltd.

- 6.4.11 XG Sciences Inc.

- 6.4.12 Lyten Inc.

- 6.4.13 Vorbeck Materials Corp.

- 6.4.14 Cabot Corporation

- 6.4.15 ZEN Graphene Solutions Ltd.

- 6.4.16 Grabat Energy S.A.

- 6.4.17 Real Graphene USA

- 6.4.18 Tesla Inc.

- 6.4.19 EnGraphene Inc.

- 6.4.20 Graphenano S.A.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

石墨烯電池市場報告:按電池類型、應用和地區分類(2026-2034 年)

石墨烯電池市場報告:按電池類型、應用和地區分類(2026-2034 年) 石墨烯電池市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、應用、地區和競爭格局分類,2021-2031年

石墨烯電池市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、應用、地區和競爭格局分類,2021-2031年 全球石墨烯電池市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球石墨烯電池市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 石墨烯電池市場規模、佔有率和成長分析(按類型、應用、外形規格和地區分類)—產業預測(2026-2033 年)

石墨烯電池市場規模、佔有率和成長分析(按類型、應用、外形規格和地區分類)—產業預測(2026-2033 年) 石墨烯電池市場機會、成長動力、產業趨勢分析及2025-2034年預測石墨烯市場:未來預測(2025-2030)

石墨烯電池市場機會、成長動力、產業趨勢分析及2025-2034年預測石墨烯市場:未來預測(2025-2030) 2030 年石墨烯電池市場預測:按類型、形式、銷售管道、應用、最終用戶和地區進行的全球分析

2030 年石墨烯電池市場預測:按類型、形式、銷售管道、應用、最終用戶和地區進行的全球分析