|

市場調查報告書

商品編碼

2062481

汽油發電機:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Gasoline Genset - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

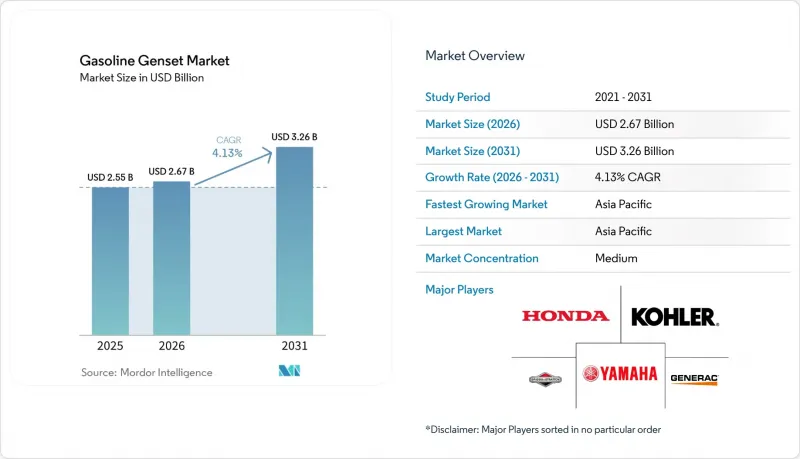

據 Mordor Intelligence 稱,汽油發電機市場預計將從 2025 年的 25.5 億美元成長到 2026 年的 26.7 億美元,到 2031 年達到 32.6 億美元,預計 2026 年至 2031 年的複合年成長率為 4.13%。

本報告按類型(可攜式、備用式、逆變器)、容量(50kVA以下、50-330kVA、330kVA以上)、應用(備用電源、尖峰用電調節、主用/連續運行)、最終用戶(住宅、商業、工業)和地區(北美、歐洲、亞太、南美、中東和非洲細分市場)進行細分。市場預測以美元計價。

全球汽油發電機市場趨勢及洞察

老化的電網基礎設施導致頻繁停電。

據美國電力公司稱,超過70%的輸電線路和變壓器已超過設計壽命,老化的基礎設施導致2024年颶風「海倫」期間出現431次自動斷電。與2023年相比,紐約用戶在2024年經歷了162%的斷電,迫使許多住宅和小型企業購買備用汽油發電機組,以確保可靠的故障容錯能力。歐洲也出現了類似的趨勢,一些國家的電網仍在使用已有50年歷史的木製電線杆,這增加了計畫維護期間對備用電源的需求。雖然電力公司正在部署重合閘、分段設備和先進的測量儀器,但電網升級需要數年時間,因此預計在可預見的未來,汽油發電機市場的需求將保持在高位。製造商正抓住這一機遇,推廣遠端監控套件,這些套件可以通知用戶斷電並自動啟動發電機,從而確保即使在電網故障期間也能無縫運作。

極端天氣導致住宅緊急用電需求增加

根據美國能源資訊署 (EIA) 的記錄,2024 年,電力公司用戶平均停電時間超過 10 小時,創下近十年來的最高紀錄。其中 80% 的停電是由大型風暴造成的。颶風海倫和米爾頓影響了 470 萬用戶。在加州,由於野火肆虐,出於公共安全考慮而計劃的停電次數急劇增加,促使許多家庭主動安裝緊急發電機。美國國家海洋暨大氣總署 (NOAA) 預測,2026 年大西洋颶風季的強度將高於平均水平,這將進一步增加住宅對可靠備用電源系統的需求。布里格斯-斯特拉頓 (Briggs & Stratton) 的 26kW PowerProtect 發電機,憑藉其 65.6kVA 的電機啟動能力和每週一次的自診斷功能(可降低油耗和噪音),深受安靜郊區居民的青睞。隨著越來越多的家庭尋求能夠確保冷藏庫、空調和重要電子設備即使在停電數天的情況下也能運作的承包解決方案,汽油發電機市場正在蓬勃發展。

加強小型火花點火引擎的排放氣體法規

美國環保署 (EPA) 第三階段法規將非攜帶式引擎的碳氫化合物 (HC) 和氮氧化物 (NOx)排放上限降低至 8 克/千瓦時。同時,歐洲第五階段法規增加了顆粒物計數測量和運作中合規性審計。製造商正透過採用燃油噴射器、催化消音器和蒸發排放罐來應對這些法規,但這導致零件成本增加,並迫使製造商在重量和機殼尺寸方面做出妥協。印度的 CPCB IV+ 法規將於 2024 年 7 月生效,該法規已涵蓋功率高達 800 千瓦的引擎,要求原始設備製造商 (OEM) 對汽油和柴油車型進行認證,並為現有車隊提供後處理系統。合規性測試和文件編制工作正在加重工程預算的負擔,延長產品上市週期,並略微減緩汽油發電機市場的成長,直到成本因學習曲線和規模經濟而再次下降。

細分市場分析

預計到2025年,可攜式汽油發電機將佔據54.2%的市場佔有率,推動市場成長。這證實了攜帶式汽油發電機因其便攜性而對屋主、建築商和戶外愛好者俱有無可否認的吸引力。然而,預計到2031年,逆變式汽油發電機的複合年成長率將達到7.0%,透過智慧燃油噴射和變速運行,顯著降低噪音和油耗。本田的iGX400和iGX430展示了電子控制、SAE J1939連接和無阻風門啟動功能如何解決客戶在季節性使用情境中遇到的挑戰。雖然緊急發電機受益於日益頻繁的停電,但它們也面臨來自太陽能和儲能系統的激烈競爭。 Briggs & Stratton的26kW「PowerProtect」發電機填補了這一市場空白,它不僅通過了非緊急運行週期的認證,還允許用戶從公用事業需量反應中獲得收益。因此,汽油發電機市場正逐漸向逆變器和先進的緊急平台轉變,這些平台將清潔輸出與數位控制相結合。

傳統開放式可攜式發電機作為輕型建築和DIY項目的備用電源,在價格方面仍然具有優勢,尤其是在新興市場。然而,各國日益嚴格的噪音法規和引擎標準正促使高階市場買家轉向更安靜、更乾淨的逆變發電機。原始設備製造商(OEM)正在其產品線中增加2-3kW的手持式並聯發電機,為5-7kW的開放式發電機提供模組化替代方案,後者可以連接以應對更高的負載。零售通路正在重點宣傳燃油成本節省模擬器和噪音水平對比,以鼓勵傳統發電機用戶改用逆變發電機,從而維持逆變發電機在汽油發電機市場的成長。

2025年,50 kVA以下的汽油發電機將佔據73.5%的市場佔有率,主要用於住宅備用電源、資訊亭和小規模建築工地。對這一功率等級發電機的需求與家庭停電趨勢和小規模企業的成長直接相關。同時,預計330 kVA以上的發電機將以6.4%的複合年成長率成長,主要得益於超大規模資料中心的建設、電力公司高峰需量反應項目以及礦區的需求。康明斯全新Centum系列,包括全新QSK50和QSK78,體現了康明斯對高功率輸出的承諾,並專注於為關鍵任務工作負載提供高密度和高可靠性解決方案。

50至330千伏安的中型發電機組一直廣泛應用於飯店、中層辦公大樓和租賃車隊等領域。然而,隨著工業設施整合為數量更少、規模更大的設施,例如人工智慧晶片製造廠和超級工廠,對330千伏安以上發電機組的需求日益成長。為此,原始設備製造商(OEM)正在引入模組化並聯控制面板和車載機載診斷功能,以簡化兆瓦級安裝。同時,在50千伏安以下的細分市場,來自屋頂太陽能發電系統和用於關鍵負載電路的電池的競爭也日益激烈。儘管如此,這些小型發電機組的便攜性和較低的初始成本仍然吸引著許多買家。因此,汽油發電機市場呈現兩極化的趨勢:高功率發電機組瞄準能源密集產業的成長目標,而小型發電機組則致力於維持其現有的廣泛應用基礎。

區域分析

亞太地區是汽油發電機市場的主要驅動力,預計2025年將佔全球銷量的46.4%,並預計在2031年之前以5.7%的複合年成長率穩步成長。在印度,儘管中央污染控制委員會(CPCB)於2024年實施了更為嚴格的小型引擎排放氣體法規IV+,康明斯印度公司仍交付了超過23,000台符合標準的發電機組,並將其GOEM經銷商網路擴展至127個地點,這表明市場需求強勁。中國的基礎設施建設和東南亞國協的電氣化項目正在推動可攜式發電機和租賃設備的強勁需求。同時,在日本和韓國,逆變式發電機更受青睞,以滿足嚴格的噪音法規和燃油效率標準。新加坡和印尼資料中心建設的快速發展也帶動了對大容量緊急發電機組的訂單。

由於野火和強風暴造成的長時間停電,北美仍是緊急發電機和逆變發電機採購趨勢的關鍵指標。科羅拉多一家建築公司自電力公司於2024年開始實施預防性停電以來,諮詢量從每年12起激增至每週7起。為了滿足不斷成長的商業和工業需求,Generac公司計劃於2025年投資3500萬美元,在威斯康辛州比弗丹新建一座35萬平方英尺的工廠,並以2000萬美元的價格收購了位於蘇塞克斯的一家工廠。除了加拿大偏遠地區的採礦和管道行業外,墨西哥的建築熱潮也推動了該地區的成長。

歐洲汽油發電機市場正面臨歐盟第五階段排放法規的挑戰,該法規推高了柴油車的合規成本,因此,輕載產業的汽油車型間接受益。在德國和北歐國家,電池-柴油混合動力發電機正在引入建築工地以減少排放氣體,但在擁有大量老舊建築的南歐國家,人們在季節性熱浪期間仍然依賴傳統的可攜式發電機。阿特拉斯·科普柯於2026年3月推出的「QHS整合混合動力」系統聲稱可將二氧化碳排放減少高達80%,這表明歐洲原始設備製造商(OEM)正在將重心轉向低碳解決方案。同時,中東的大型企劃,例如沙烏地阿拉伯的特大城市和阿拉伯聯合大公國的資料中心,正在推動對數兆瓦備用和主用發電機組的訂單,而南非的計劃性停電也提振了撒哈拉以南非洲地區住宅和工商業市場的需求。在拉丁美洲,巴西的建設產業和安第斯山脈地區的採礦業正在推動需求,儘管外匯波動可能會減緩進口。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 由於電網基礎設施老化,頻繁發生停電

- 極端天氣導致住宅緊急用電需求增加

- 房車和戶外休閒的蓬勃發展帶動了可攜式逆變器的銷售成長。

- 新興國家的快速城市建設

- 利用物聯網進行遠端監控,最佳化營運成本(OPEX)。

- 市場限制因素

- 加強小型火花點火引擎的排放氣體法規

- 太陽能發電與儲能結合的家用系統已廣泛應用。

- 銅和鋼價格的波動推高了生產成本。

- 供應鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按類型

- 可攜式汽油發電機

- 備用汽油發電機

- 逆變式汽油發電機

- 按產能

- 小於 50 千伏安

- 50~330 kVA

- 超過330千伏安

- 透過使用

- 支援

- 尖峰用電調節

- 主/連續

- 最終用戶

- 住宅

- 商業的

- 產業

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 北歐國家

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 東南亞國協

- 其他亞太國家

- 南美洲

- 巴西

- 阿根廷

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

- 埃及

- 其他中東和非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢(併購、聯盟、購電協議)

- 市場佔有率分析(主要公司的市場排名和佔有率)

- 公司簡介

- Honda Motor Co., Ltd.

- Yamaha Motor Co., Ltd.

- Generac Holdings Inc.

- Briggs & Stratton Corporation

- Rehlko

- Cummins Inc.

- Caterpillar Inc.

- Champion Power Equipment

- Atlas Copco AB

- Hyundai Corporation

- Wacker Neuson SE

- Multiquip Inc.

- Westinghouse Electric Company LLC

- Denyo Co., Ltd.

- Perkins Engines Co. Ltd.

- Himoinsa SL

- Pramac SpA

- Stanley Black & Decker, Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the gasoline genset market size is expected to increase from USD 2.55 billion in 2025 to USD 2.67 billion in 2026 and reach USD 3.26 billion by 2031, growing at a CAGR of 4.13% over 2026-2031.

This report is Segmented by Type (Portable, Standby, Inverter), Capacity (Below 50 KVA, 50 To 330 KVA, Above 330 KVA), Application (Standby, Peak Shaving, Prime/Continuous), End-User (Residential, Commercial, Industrial), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Gasoline Genset Market Trends and Insights

Aging Grid Infrastructure Causing Frequent Outages

U.S. utilities report that over 70% of transmission lines and transformers have exceeded their intended service life, and this aging fleet contributed to 431 automatic transmission outages during Hurricane Helene in 2024 . Customers in New York endured 162% more interruption hours in 2024 than in 2023, forcing many homeowners and small businesses to purchase standby gasoline sets for guaranteed resilience . Europe shows a similar pattern, with 50-year-old wooden distribution poles still in place across several national networks, pushing demand for backup power during scheduled maintenance windows. Although utilities are installing reclosers, sectionalizers, and advanced metering, grid upgrades occur over multi-year cycles, leaving a near-term window where gasoline genset market demand remains elevated. Manufacturers are capitalizing by promoting remote-monitoring packages that alert owners to outages and automate generator starts, ensuring seamless operation during grid failures.

Residential Backup-Power Demand from Extreme Weather Events

The U.S. Energy Information Administration recorded more than 10 outage hours per utility customer in 2024, the highest level in a decade, with 80% of those hours caused by major storms. Hurricanes Helene and Milton left 4.7 million customers without electricity, while wildfire-driven public-safety shutoffs in California expanded dramatically, encouraging households to install standby sets pre-emptively. NOAA forecasts an above-average Atlantic hurricane season in 2026, further intensifying homeowner appetite for robust backup systems . Briggs & Stratton's 26-kW PowerProtect generator offers 65.6 kVA of motor-starting capacity and a quick weekly self-test that reduces fuel use and noise, appealing to residents in quiet suburban areas. The gasoline genset market gains a tailwind as households seek turnkey solutions that ensure refrigeration, HVAC, and critical electronics remain operational during multiday blackouts.

Stricter Emission Norms for Small Spark-Ignition Engines

The U.S. EPA's Phase 3 rules impose HC+NOx limits as low as 8 g/kWh for non-handheld engines, while Europe's Stage V adds particulate-number counting and in-service conformity audits. Manufacturers answer with fuel injection, catalytic mufflers, and evaporative canisters, raising bill-of-materials costs and forcing design compromises on weight and enclosure size. India's CPCB IV+ regulation came into force in July 2024 and already covers engines up to 800 kW, obliging OEMs to certify both gasoline and diesel models and to offer retrofit aftertreatment for existing fleets. Compliance testing and paperwork stretch engineering budgets and lengthen product-launch cycles, marginally dampening gasoline genset market growth until learning curves and economies of scale bring costs back down.

Other drivers and restraints analyzed in the detailed report include:

- RV & Outdoor-Leisure Boom Boosting Portable Inverter Sales

- Urban Construction Surge in Emerging Economies

- Rising Uptake of Solar-Plus-Storage Home Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Portable units dominated the gasoline genset market size with a 54.2% revenue share in 2025, confirming their go-anywhere appeal for households, contractors, and outdoor enthusiasts. Inverter models, however, are forecast to climb at a 7.0% CAGR to 2031 because smart fuel injection and variable-speed operation slash noise and fuel burn. Honda's iGX400 and iGX430 demonstrate how electronic control, SAE J1939 connectivity, and choke-free starts attack customer pain points in seasonal-use scenarios. Standby sets benefit from rising grid outages, yet face silent competition from solar-plus-storage. Briggs & Stratton's 26-kW PowerProtect, certified for non-emergency cycles, bridges this gap by letting owners earn utility demand-response revenue. The gasoline genset market, therefore, tilts gradually toward inverters and advanced standby platforms that combine clean output with digital controls.

Traditional open-frame portables remain price leaders for light construction and do-it-yourself backup, especially in emerging markets. Nevertheless, country-level noise ordinances and stricter engine standards push buyers in premium segments toward quieter, cleaner inverter sets. OEMs are broadening their catalogs with parallel-ready 2-3 kW models that can be hand-carried yet linked for higher draws, providing a modular alternative to 5-7 kW open-frame designs. Retail channels highlight fuel-savings calculators and decibel comparisons to convert legacy-generator owners, supporting sustained inverter share gains inside the gasoline genset market.

Sub-50 kVA machines captured 73.5% gasoline genset market share in 2025, serving residential backup, kiosks, and light construction. Demand in this size class aligns directly with household outage trends and small-business growth. Conversely, units above 330 kVA are projected to grow at a 6.4% CAGR thanks to hyperscale data-center builds, utility peaking projects, and mining camps. Cummins' new QSK50- and QSK78-powered Centum Series sets exemplify the high-power push by emphasizing density and reliability for mission-critical workloads.

Middle-capacity gensets, ranging from 50 to 330 kVA, are consistently utilized in applications such as hotels, mid-rise office buildings, and rental fleets. However, as industrial operations consolidate into fewer, larger facilities, such as AI chip manufacturing plants and giga-factories, demand for gensets above 330 kVA is increasing. In response, original equipment manufacturers (OEMs) are introducing modular paralleling panels and on-board diagnostics to streamline multi-megawatt installations. At the same time, the sub-50 kVA segment is experiencing gradual competition from rooftop solar systems combined with batteries for essential-load circuits. Despite this, the portability and lower upfront costs of these smaller units continue to attract many buyers. Consequently, the gasoline genset market is diverging: high-horsepower units are targeting growth in energy-intensive industries, while smaller units focus on maintaining their extensive installed base.

Geography Analysis

Asia-Pacific led the gasoline genset market with 46.4% revenue in 2025 and is forecast at a brisk 5.7% CAGR to 2031. India tightened small-engine emissions with CPCB IV+ in 2024, yet Cummins India still shipped over 23,000 compliant units and expanded its GOEM dealer roster to 127 outlets, signaling strong underlying demand. China's infrastructure push and ASEAN electrification projects keep portable and rental fleets busy, while Japan and South Korea favor inverter units to meet stringent noise and fuel-efficiency criteria. Rapid data-center construction in Singapore and Indonesia also lifts orders for high-capacity standby sets.

North America remains the bellwether for standby and inverter purchases because wildfire-driven shutoffs and severe storms lengthen outage durations. One Colorado contractor saw inquiries soar from 12 per year to seven per week once utilities began preventive shutoffs in 2024. Generac opened a USD 35 million, 350,000-square-foot facility in Beaver Dam, Wisconsin, in 2025 and bought a Sussex plant for USD 20 million to meet climbing commercial-industrial demand. Canada's remote mining and pipeline sectors, plus Mexico's construction boom, round out regional growth.

Europe's gasoline genset market grapples with EU Stage V rules that inflate diesel compliance costs, indirectly benefiting gasoline models in light-duty niches. Germany and the Nordics embrace hybrid battery-diesel gensets to trim emissions on job sites, yet southern nations with older building stock still rely on conventional portables during seasonal heat waves. Atlas Copco's QHS Integrated Hybrid launch in March 2026 claims up to 80% CO2 savings, showing European OEMs' pivot to low-carbon solutions. Meanwhile, Middle East megaprojects like Saudi giga-cities and UAE data hubs drive multi-megawatt orders for standby and prime sets, while South Africa's rolling blackouts fuel residential and C&I uptake across sub-Saharan Africa. Latin America contributes via Brazilian construction and Andean mining, though currency volatility occasionally slows imports.

- Honda Motor Co., Ltd.

- Yamaha Motor Co., Ltd.

- Generac Holdings Inc.

- Briggs & Stratton Corporation

- Rehlko

- Cummins Inc.

- Caterpillar Inc.

- Champion Power Equipment

- Atlas Copco AB

- Hyundai Corporation

- Wacker Neuson SE

- Multiquip Inc.

- Westinghouse Electric Company LLC

- Denyo Co., Ltd.

- Perkins Engines Co. Ltd.

- Himoinsa S.L.

- Pramac S.p.A.

- Stanley Black & Decker, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Aging grid infrastructure causing frequent outages

- 4.2.2 Residential backup-power demand from extreme weather events

- 4.2.3 RV & outdoor-leisure boom boosting portable inverter sales

- 4.2.4 Urban construction surge in emerging economies

- 4.2.5 IoT-enabled remote monitoring improving OPEX economics

- 4.3 Market Restraints

- 4.3.1 Stricter emission norms for small spark-ignition engines

- 4.3.2 Rising uptake of solar-plus-storage home systems

- 4.3.3 Volatile copper & steel prices inflating production costs

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Type

- 5.1.1 Portable Gasoline Gensets

- 5.1.2 Standby Gasoline Gensets

- 5.1.3 Inverter Gasoline Gensets

- 5.2 By Capacity

- 5.2.1 Below 50 kVA

- 5.2.2 50 to 330 kVA

- 5.2.3 Above 330 kVA

- 5.3 By Application

- 5.3.1 Standby

- 5.3.2 Peak Shaving

- 5.3.3 Prime/Continuous

- 5.4 By End-user

- 5.4.1 Residential

- 5.4.2 Commercial

- 5.4.3 Industrial

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 NORDIC Countries

- 5.5.2.6 Russia

- 5.5.2.7 Rest of Europe

- 5.5.3 Asia Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 ASEAN Countries

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 South Africa

- 5.5.5.4 Egypt

- 5.5.5.5 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Honda Motor Co., Ltd.

- 6.4.2 Yamaha Motor Co., Ltd.

- 6.4.3 Generac Holdings Inc.

- 6.4.4 Briggs & Stratton Corporation

- 6.4.5 Rehlko

- 6.4.6 Cummins Inc.

- 6.4.7 Caterpillar Inc.

- 6.4.8 Champion Power Equipment

- 6.4.9 Atlas Copco AB

- 6.4.10 Hyundai Corporation

- 6.4.11 Wacker Neuson SE

- 6.4.12 Multiquip Inc.

- 6.4.13 Westinghouse Electric Company LLC

- 6.4.14 Denyo Co., Ltd.

- 6.4.15 Perkins Engines Co. Ltd.

- 6.4.16 Himoinsa S.L.

- 6.4.17 Pramac S.p.A.

- 6.4.18 Stanley Black & Decker, Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment