|

市場調查報告書

商品編碼

2062462

網域名稱系統防火牆:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Domain Name System Firewall - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

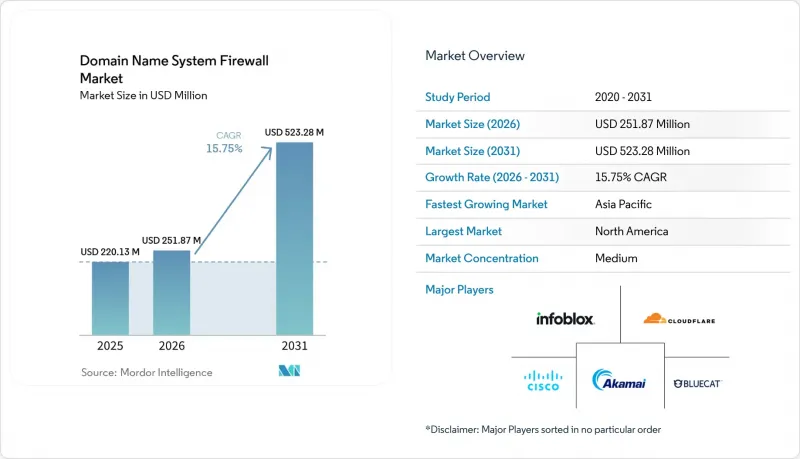

據 Mordor Intelligence 稱,2025 年域名系統 (DNS) 防火牆市場價值為 2.2013 億美元,預計到 2031 年將達到 5.2328 億美元,而 2026 年為 2.5187 億美元,預測期(2026-2031 年)的複合年成長率為 15.75%。

本報告按部署模式(本地部署、雲端部署、混合部署)、DNS 伺服器類型(遞歸解析器防火牆、權威 DNS 防火牆等)、企業規模(大型企業、中型企業、中小企業)、產業(銀行、金融服務和保險 (BFSI)、IT 和電信、政府和國防等)以及地區進行細分。市場預測以美元 (USD) 計價。

全球域名系統 (DNS) 防火牆市場趨勢與洞察

DNS 層攻擊的增加促使人們需要進行強制性的安全投資。

大規模偵察、網路釣魚和分散式阻斷服務 (DDoS) 攻擊正促使企業安全預算轉向以解析器為中心的措施。美國網路安全與基礎設施安全局 (CISA) 和國家安全局 (NSA) 於 2025 年 3 月聯合發布的一項建議指出,「快速網域輪調」技術,該技術透過將攻擊者的基礎設施隱藏在不斷變化的 IP 位址背後,從而掩蓋靜態黑名單。 2024 年初,FBI 破獲了一個控制超過一百萬台小規模辦公室路由器的俄羅斯殭屍網路,此後,這項技術變得更加緊迫。這表示無所不在的 DNS 流量可以被武器化。 Infoblox 的《2025 年 DNS 威脅報告》記錄了隧道事件增加了 37%,證實攻擊者現在將 DNS 視為一條低門檻的命令與控制路徑。董事會層級關於網路風險的討論擴大將DNS保護措施視為承保網路保險的必要條件,採購週期也從幾年縮短到每季一次。

快速過渡到多重雲端和混合IT架構

在亞馬遜雲端服務 (AWS)、微軟 Azure、谷歌雲端和託管資料中心運行工作負載的公司,難以維護一致的網域策略。 IBM 的 NS1 Connect 白皮書指出,金融公司至少維護兩個外部 DNS 供應商,以消除單點故障。 2024 年中,一次持續六小時的循環中斷影響了關鍵平台,驗證了這項做法的必要性。由於從演算法交易到即時患者遙測等對效能要求極高的應用仍然依賴本地解析器,因此企業更傾向於採用混合架構,將本地設備與雲端協作相結合。 2026 年 4 月,思科針對波灣合作理事會(GCC) 市場部署了本地化的 DNS 防火牆設備,並將其與 Umbrella 雲層整合,從而解決了延遲和主權問題,實現了統一的策略執行。隨著架構複雜性的增加,市場對能夠跨不同解析器實例近乎即時地提供威脅情報和響應式策略區域的管理主機的需求日益成長。能夠自動完成這種整合且不降低查詢效能的供應商,其市佔率正在顯著擴大。

大型成熟企業更換傳統遞迴伺服器的成本很高。

那些已經將 BIND 等開放原始碼解析器標準化的金融和電信巨頭,在遷移到商用防火牆時,將面臨超過 50 萬美元的資本支出。它們基於地理位置建構的叢集旨在確保冗餘,其中包含數百個任播節點,無法簡單地「原樣遷移」到新硬體上。 NIST 特別出版刊物800-81 修訂版 3 警告稱,在現有環境中實施 DNSSEC 和符合規範的策略區域可能需要 12 到 18 個月的時間。在過渡期間,團隊必須並行維護新舊基礎設施,這將導致人事費用增加和變更管理週期延長。對於營運利潤率低、幾乎沒有餘力承擔數百萬美元安全項目的製造業和零售業而言,預算影響將特別嚴重。

細分市場分析

混合配置將在2025年佔據相當大的支出佔有率,複合年成長率將達到16.43%,超過網域名稱系統(DNS)防火牆市場的整體表現。最初,企業傾向於選擇基於雲端的防火牆以求快速見效,預計2025年雲端防火牆的支出將占到總支出的58.91%。然而,查詢跳轉次數的增加導致延遲增加10-20毫秒,這對事務演算法和臨床成像系統來說是不可接受的延遲。因此,買家現在將輕量級的本機解析器與雲端協作相結合,以在集中策略控制的同時保持亞毫秒的反應速度。根據EfficientIP的2025年調查,員工人數超過10,000人的公司中,已有62%實施了這種雙架構,而NIS2的彈性需求推動了這一趨勢。域名系統(DNS)防火牆市場的規模也受益於買家同時採購訂閱服務和設備硬體,而不是二選一。

第二個成長要素是與主權雲相關的監管規定。沙烏地阿拉伯的「Salam Secure DNS」為其他海灣市場樹立了榜樣,它接受來自供應商雲端的威脅情報推送,同時將所有日誌保留在國內。而Cloudflare Gateway則截然相反。到2025年,將有超過15,000家沒有傳統設備的公司直接遷移到純雲端DNS。即便如此,隨著邊緣站點數量的增加,快取轉發器在頻寬有限的分支機構中仍然至關重要。無論是集中式編配或獨立運作,解析器多樣性不再是架構選擇,而是合規性要求。

到2025年,遞歸解析器引擎仍將佔據主導地位,佔網域名稱系統(DNS)防火牆市場38.45%的佔有率,因為所有終端查詢都源自於它們。然而,權威伺服器層防禦正以15.95%的複合年成長率快速成長,這主要得益於SaaS供應商和CDN為防禦Terabit級反射攻擊所做的努力。 Akamai記錄到,2025年上半年此類攻擊激增71%,迫使業者在區域頂端實施速率限制和DNSSEC檢驗。新的架構藍圖建議在共用策略網格中結合解析器過濾和權威過濾,使網域名稱系統(DNS)防火牆市場更接近整合控制平面的願景。

VeriSign 每天高達 1830 億次的查詢負載清晰地表明了權威引擎必須在不出現誤報的情況下處理容量要求。 Neustar 和 F5 正在透過部署機器學習分類器來解決這個問題,這些分類器能夠以亞秒級的時間間隔檢測異常流量峰值和地理位置異常。網際網路工程任務組 (IETF) 的「保護性 DNS」框架草案進一步加強了功能統一性的指導原則,確保供應商之間的差異化從基本的阻止/允許清單轉向更深入的分析。儘管隨著 SaaS 的持續成長,遞歸 DNS 的支出依然強勁,但權威伺服器防火牆在未來十年仍將保持其成長優勢。

區域分析

美國的「保護性DNS」舉措促使101個聯邦機構部署了基於威脅情報的解析器服務,使得北美在2025年佔據了42.56%的收入佔有率。強大的網路安全預算,加上接近性超大規模雲端和託管安全創新企業的優勢,使該地區能夠在絕對支出方面繼續保持領先地位。加拿大網路安全中心在2025年做出回應,建議各省醫療保健系統加強遞歸基礎建設;而墨西哥監管機構在2024年發生一起DNS劫持事件後,強制要求銀行進行DNS監控。

亞太地區以15.92%的複合年成長率領先成長率榜單。日本已累計49.3億日元(約3300萬美元)用於為大學和公共產業部署解析器;印度的CERT-In計劃到2025年處理294.4萬起安全事件,並已將其在人工智慧驅動的惡意域名檢測網路方面的投資增加了一倍。韓國的KISA計劃在2025年將歐盟和美國的威脅情報整合到其監控系統中,這反映了跨區域資料共用的擴展。在東協地區,ICANN的區域計畫正在加速DNSSEC研討會的舉辦和公共部門的採用。

歐洲的趨勢正受到NIS2和DORA的影響,這兩項標準將DNS置於供應鏈審計的核心。德國聯邦資訊安全局(BSI)、英國國家網路安全中心(NCSC)以及沙烏地阿拉伯和阿拉伯聯合大公國主權雲的努力都支持這樣一種觀點:解析器策略與防火牆策略同等重要。非洲和南美洲的投資仍然緩慢,但隨著付費使用制安全提供者推出按需付費的解析器保護服務,未來五年內這一差距可能會縮小。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- DNS層攻擊的增加使得安全投資變得至關重要。

- 快速過渡到多重雲端和混合IT架構

- 零信任和安全存取服務邊緣 (SASE) 框架的監管要求

- 擴大 DNS 隧道技術在邊緣物聯網設備叢集中的應用,用於命令與控制。

- 「一切皆透過 HTTPS 傳輸」的興起正在加速加密 DNS 的普及。

- 通訊業者正在利用DNS威脅情報資訊為企業創造利潤。

- 市場限制因素

- 主要現有服務供應商更換傳統遞迴伺服器的成本很高

- 熟練的DNS安全專家短缺

- 加密DNS在衛星回程傳輸鏈路上的效能權衡

- 主權雲中國家根伺服器策略的碎片化

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 市場宏觀經濟趨勢分析

第5章 市場規模與成長預測

- 按部署模式

- 現場

- 基於雲端的

- 混合

- 按DNS伺服器類型

- 循環解析器防火牆

- 權威 DNS 防火牆

- 快取類型/轉發器類型/防火牆類型

- 按公司規模

- 大型公司(員工人數1000人或以上)

- 中型企業(100-999名員工)

- 中小企業(員工人數少於100人)

- 按行業分類

- BFSI

- IT/通訊

- 政府/國防

- 醫療保健和生命科學

- 零售與電子商務

- 製造業

- 其他工業部門

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- ASEAN

- 其他亞太國家

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 其他非洲國家

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Infoblox Inc.

- Cloudflare, Inc.

- Cisco Systems, Inc.

- Akamai Technologies, Inc.

- BlueCat Networks, Inc.

- EfficientIP SAS

- Neustar Security Solutions, LLC

- F5, Inc.

- Men & Mice ehf

- VeriSign, Inc.

- DNSFilter, Inc.

- Comodo Security Solutions, Inc.

- Enea AB

- Huawei Technologies Co., Ltd.

- Palo Alto Networks, Inc.

- Quad9 Foundation

- Technitium Solutions Pvt. Ltd.

- FlashStart Srl

- Secure64 Software Corporation

- Zscaler, Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the domain name system firewall market size was valued at USD 220.13 million in 2025 and estimated to grow from USD 251.87 million in 2026 to reach USD 523.28 million by 2031, at a CAGR of 15.75% during the forecast period (2026-2031).

This report is Segmented by Deployment Model (On-Premises, Cloud-Based, and Hybrid), DNS Server Type (Recursive Resolver Firewall, Authoritative DNS Firewall, and More), Enterprise Size (Large Enterprises, Mid-Sized Enterprises, and SMEs), Industry Vertical (BFSI, IT and Telecommunications, Government and Defense, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Domain Name System Firewall Market Trends and Insights

Increasing DNS-Layer Attacks Driving Mandatory Security Investments

High-volume reconnaissance, phishing, and distributed denial-of-service assaults are shifting corporate security budgets toward resolver-centric countermeasures. A joint advisory from the U.S. Cybersecurity and Infrastructure Security Agency and the National Security Agency in March 2025 flagged "fast flux" domain rotation that hides attacker infrastructure behind constantly changing IP addresses, rendering static blocklists obsolete. The technique gained urgency after the Federal Bureau of Investigation dismantled a Russian botnet that hijacked more than one million small-office routers in early 2024, illustrating how ubiquitous DNS traffic can be weaponized. Infoblox's 2025 DNS Threat Report logged a 37% rise in tunneling events, confirming that adversaries now view DNS as a low-friction command-and-control pathway. Board-level cyber-risk discussions increasingly treat protective DNS as a prerequisite for cyber-insurance underwriting, compressing procurement cycles from years to quarters.

Rapid Migration to Multi-Cloud and Hybrid IT Architectures

Enterprises juggling workloads across Amazon Web Services, Microsoft Azure, Google Cloud, and colocation sites struggle to keep consistent domain policies. IBM's NS1 Connect white paper documented that financial firms maintain at least two external DNS providers to eliminate single points of failure, a practice vindicated when a major platform suffered a six-hour recursive outage in mid-2024. Performance-critical apps, from algorithmic trading to real-time patient telemetry, still depend on local resolvers, so organizations favor hybrid designs that blend on-premises appliances with cloud orchestration. Cisco addressed those latency and sovereignty concerns in April 2026 by rolling out localized DNS firewall appliances for Gulf Cooperation Council markets while tying them back to its Umbrella cloud layer for a unified policy push. The architectural sprawl fuels demand for management consoles that broadcast threat feeds and response-policy zones across disparate resolver instances in near real time. Vendors that can automate this federation without degrading query performance are winning disproportionate wallet share.

High Replacement Cost for Legacy Recursive Servers in Large Incumbents

Financial and telecom giants that standardized on open-source resolvers such as BIND face capital outlays topping USD 500,000 when migrating to commercial firewalls. Geographic clusters built for redundancy house hundreds of anycast nodes that cannot simply be "forklifted" into new hardware. NIST's Special Publication 800-81 Revision 3 cautions that retrofitting DNSSEC and response-policy zones can drag on for 12-18 months in brownfield environments. During the transition window, teams must dual-maintain old and new infrastructure, inflating labor costs and elongating change-control windows. The budgetary shock is especially acute in manufacturing and retail, where thin operating margins leave minimal headroom for seven-figure security projects.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory Mandates for Zero-Trust and Secure Access Service Edge Frameworks

- Growing Use of DNS Tunneling for Command-and-Control in Edge IoT Fleets

- Lack of Skilled DNS Security Professionals

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hybrid setups accounted for a material slice of 2025 spending and are growing at 16.43% CAGR, outpacing the broader Domain Name System Firewall market. Organizations first gravitated to cloud-based firewalls for quick wins, 58.91% of outlays in 2025, but discovered that added query hops inflate latency by 10-20 milliseconds, an unacceptable drag on trading algorithms and clinical imaging systems. Consequently, buyers now mesh lightweight on-premises resolvers with cloud orchestration to retain sub-millisecond response while centralizing policy control. EfficientIP's 2025 survey found that 62% of firms above 10,000 employees already run such dual architectures, and NIS2 resilience mandates reinforce the trend. The Domain Name System Firewall market size benefits because buyers procure both subscriptions and appliance hardware instead of choosing one or the other.

A second growth lever is sovereign-cloud regulation. Saudi Arabia's Salam Secure DNS keeps all logs within national borders while still accepting threat-feed pushes from vendor clouds, providing a playbook for other Gulf markets. Cloudflare Gateway illustrates the opposite end of the spectrum: more than 15,000 enterprises without legacy gear leaped straight into pure cloud DNS in 2025. Still, as edge sites proliferate, caching forwarders will remain indispensable for branch offices where bandwidth is scarce. Whether orchestrated centrally or run stand-alone, resolver diversity is now a compliance requirement rather than an architectural preference.

Recursive resolver engines remained the workhorse in 2025, controlling 38.45% of the Domain Name System Firewall market share because every endpoint query begins there. Yet authoritative-layer defenses are climbing at a 15.95% CAGR, propelled by SaaS vendors and CDNs fending off terabit-scale reflection floods. Akamai logged a 71% spike in such assaults during 1H 2025, forcing operators to deploy rate limiting and DNSSEC validation at the zone apex. New architectural blueprints now recommend pairing resolver and authoritative filters in a shared policy mesh, moving the Domain Name System Firewall market closer to a unified control-plane vision.

VeriSign's daily query load of 183 billion illustrates the throughput requirement that authoritative engines must satisfy without false positives. Neustar and F5 have responded with machine-learning classifiers that flag anomalous volume bursts or geo anomalies in sub-second intervals. The Internet Engineering Task Force's draft Protective DNS framework further cements feature parity guidelines, ensuring vendor differentiation skews toward analytics depth rather than basic block-and-allow lists. With SaaS adoption still climbing, authoritative firewalls should preserve their growth premium well into the next decade even as recursive spending stays robust.

Geography Analysis

North America generated 42.56% of 2025 receipts after the U.S. Protective DNS initiative funneled threat-fed resolver services into 101 federal agencies. Mature cyber budgets, plus proximity to hyperscale clouds and managed security innovators, keep the region ahead on absolute spend. Canada's Center for Cyber Security echoed the push in 2025 by advising provincial health systems to harden recursive infrastructure, and Mexico's regulators compelled banks to monitor DNS following 2024 hijacking incidents.

Asia-Pacific, tracking a 15.92% CAGR, tops the velocity charts. Japan earmarked JPY 4.93 billion (USD 33 million) for university and utility resolver rollouts, while India's CERT-In processed 2.944 million incidents in 2025 and doubled down on an AI-driven malicious-domain detection grid. South Korea's KISA plugged EU and U.S. threat intel into its 2025 monitoring stack, illustrating growing cross-regional data sharing. Across ASEAN, ICANN's regional plan boosted DNSSEC workshops, accelerating public-sector adoption.

Europe's trajectory is shaped by NIS2 and DORA, which pull DNS into the core of supply-chain audits. Germany's BSI, the U.K.'s National Cyber Security Center, and sovereign-cloud initiatives in Saudi Arabia and the UAE reinforce the view that resolver policy is now as strategic as firewall policy. Africa and South America still lag in spending, but managed security providers are introducing pay-as-you-go resolver protection that may compress the gap over the next five years.

- Infoblox Inc.

- Cloudflare, Inc.

- Cisco Systems, Inc.

- Akamai Technologies, Inc.

- BlueCat Networks, Inc.

- EfficientIP SAS

- Neustar Security Solutions, LLC

- F5, Inc.

- Men & Mice ehf

- VeriSign, Inc.

- DNSFilter, Inc.

- Comodo Security Solutions, Inc.

- Enea AB

- Huawei Technologies Co., Ltd.

- Palo Alto Networks, Inc.

- Quad9 Foundation

- Technitium Solutions Pvt. Ltd.

- FlashStart S.r.l.

- Secure64 Software Corporation

- Zscaler, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing DNS-Layer Attacks Driving Mandatory Security Investments

- 4.2.2 Rapid Migration to Multi-Cloud and Hybrid IT Architectures

- 4.2.3 Regulatory Mandates for Zero-Trust and Secure Access Service Edge (SASE) Frameworks

- 4.2.4 Growing Use of DNS Tunneling for Command-and-Control in Edge IoT Fleets

- 4.2.5 Rise of "Everything over HTTPS" Accelerating Encrypted DNS Adoption

- 4.2.6 Telecom Operators Monetising DNS Threat-Intel Feeds to Enterprises

- 4.3 Market Restraints

- 4.3.1 High Replacement Cost for Legacy Recursive Servers in Large Incumbents

- 4.3.2 Lack of Skilled DNS Security Professionals

- 4.3.3 Performance Trade-Offs with Encrypted DNS over Satellite Back-Haul Links

- 4.3.4 Fragmentation of National Root-Server Policies in Sovereign Clouds

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Assessment of Macroeconomic Trends on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Model

- 5.1.1 On-premises

- 5.1.2 Cloud-based

- 5.1.3 Hybrid

- 5.2 By DNS Server Type

- 5.2.1 Recursive Resolver Firewall

- 5.2.2 Authoritative DNS Firewall

- 5.2.3 Caching Forwarder Firewall

- 5.3 By Enterprise Size

- 5.3.1 Large Enterprises (>=1,000 employees)

- 5.3.2 Mid-sized Enterprises (100-999 employees)

- 5.3.3 SMEs (<100 employees)

- 5.4 By Industry Vertical

- 5.4.1 BFSI

- 5.4.2 IT and Telecommunications

- 5.4.3 Government and Defense

- 5.4.4 Healthcare and Lifesciences

- 5.4.5 Retail and e-Commerce

- 5.4.6 Manufacturing

- 5.4.7 Other Industry Vertical

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 ASEAN

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of the Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Infoblox Inc.

- 6.4.2 Cloudflare, Inc.

- 6.4.3 Cisco Systems, Inc.

- 6.4.4 Akamai Technologies, Inc.

- 6.4.5 BlueCat Networks, Inc.

- 6.4.6 EfficientIP SAS

- 6.4.7 Neustar Security Solutions, LLC

- 6.4.8 F5, Inc.

- 6.4.9 Men & Mice ehf

- 6.4.10 VeriSign, Inc.

- 6.4.11 DNSFilter, Inc.

- 6.4.12 Comodo Security Solutions, Inc.

- 6.4.13 Enea AB

- 6.4.14 Huawei Technologies Co., Ltd.

- 6.4.15 Palo Alto Networks, Inc.

- 6.4.16 Quad9 Foundation

- 6.4.17 Technitium Solutions Pvt. Ltd.

- 6.4.18 FlashStart S.r.l.

- 6.4.19 Secure64 Software Corporation

- 6.4.20 Zscaler, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

企業網路防火牆市場:2026-2032年全球市場預測(依組件、防火牆技術、吞吐量頻寬、企業規模、部署類型、用例和產業分類)

企業網路防火牆市場:2026-2032年全球市場預測(依組件、防火牆技術、吞吐量頻寬、企業規模、部署類型、用例和產業分類) 網站開發:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

網站開發:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 新一代防火牆市場規模、佔有率和成長分析:按產品、部署類型、企業規模、最終用戶產業和地區分類-2026-2033年產業預測

新一代防火牆市場規模、佔有率和成長分析:按產品、部署類型、企業規模、最終用戶產業和地區分類-2026-2033年產業預測 新一代防火牆市場報告:按類型、部署模式、安全類型、組織規模、產業和地區分類(2026-2034 年)

新一代防火牆市場報告:按類型、部署模式、安全類型、組織規模、產業和地區分類(2026-2034 年) 域名系統(DNS)防火牆全球市場規模、佔有率、趨勢和成長分析報告(2026-2034)

域名系統(DNS)防火牆全球市場規模、佔有率、趨勢和成長分析報告(2026-2034) 2026年全球網站開發市場報告

2026年全球網站開發市場報告 全球新一代防火牆市場:按組件、部署方式、企業規模、產業和地區分類新一代防火牆市場:按組件、部署模式、功能、組織規模、產業和銷售管道分類-2026-2032年全球市場預測2026年全球新一代防火牆市場報告

全球新一代防火牆市場:按組件、部署方式、企業規模、產業和地區分類新一代防火牆市場:按組件、部署模式、功能、組織規模、產業和銷售管道分類-2026-2032年全球市場預測2026年全球新一代防火牆市場報告 新一代防火牆 (NGFW) 市場分析及至 2035 年預測:按類型、產品類型、服務、技術、組件、應用、部署模式、最終用戶和功能分類

新一代防火牆 (NGFW) 市場分析及至 2035 年預測:按類型、產品類型、服務、技術、組件、應用、部署模式、最終用戶和功能分類