|

市場調查報告書

商品編碼

2062439

觸覺技術:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Haptic Technology - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

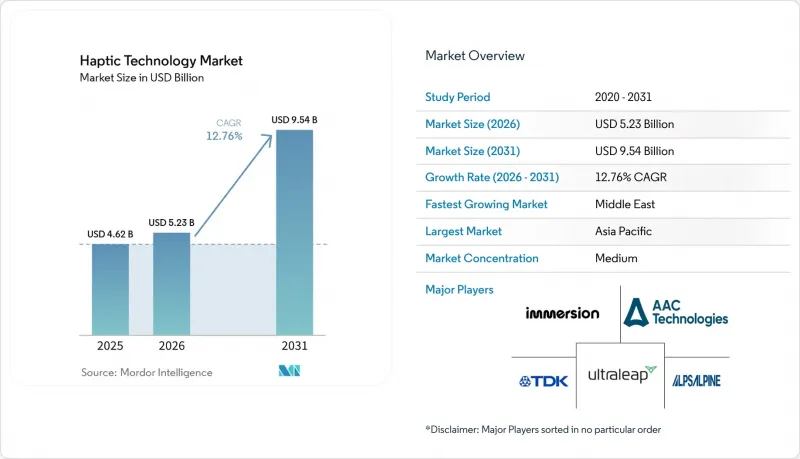

據 Mordor Intelligence 稱,觸覺技術市場預計將從 2025 年的 46.2 億美元成長到 2026 年的 52.3 億美元,到 2031 年達到 95.4 億美元,2026 年至 2031 年的複合年成長率為 12.76%。

本報告按組件(硬體和軟體)、回饋類型(觸覺(振動、皮膚拉伸、電觸覺)和力/動覺)、執行器技術(偏心旋轉質量(ERM)馬達、壓電執行器等)、應用(醫療保健和醫療設備、工業和機器人等)以及地區進行細分。市場預測以價值(美元)表示。

全球觸覺技術市場趨勢與洞察

智慧型手機的普及以及對觸覺回饋豐富的使用者體驗的需求。

行動裝置製造商目前正將多致動器陣列 (LRA) 整合到裝置中,這些陣列能夠局部定位到螢幕上的特定元素,從而提升使用者滿意度和易用性。折疊式機型配備了調諧至不同頻寬的雙 LRA,可實現更清晰的鍵盤觸覺反饋、更柔和的通知閃爍以及模擬實體按鍵的手勢確認。可折疊設備利用了軟性致動器的優勢,這些致動器在彎曲時不會損失振幅,為即將推出的捲軸式智慧型手機開闢了新的設計自由度。在成熟市場,產品更換週期不斷延長,觸覺差異化已成為客戶維繫的關鍵因素。這種轉變促使原始設備製造商 (OEM) 增加對觸覺子系統的組件成本分配,進而提升觸覺技術市場的單位價值。

用於ADAS和安全警報的汽車人機互動介面

線傳和駕駛監控功能依賴於透過方向盤、踏板和座椅結構傳遞的振動脈衝和可變阻力回饋。起亞將在其2026年車型中引入方向盤觸覺警告功能,當車道偏離或前方防撞系統偵測到即將發生的風險時,方向盤輪緣會振動。受控研究表明,這種方法比儀表板圖示識別速度快30%。將於2026年生效的歐洲新車安全評價協會(Euro NCAP)法規要求車輛必須配備實體空調控制和危險警告燈控制按鈕才能獲得五星評級,這間接增加了對觸覺響應按鈕的需求。豪華汽車製造商也嘗試使用自適應觸覺模式,在舒適模式和運動模式之間切換轉向手感,進一步拓展了聯網汽車生態系統中軟體定義商機。

高功率與散熱設計挑戰:精密執行器

壓電堆疊和靜電薄膜需要高壓驅動,這會消耗電池電量並產生熱點,迫使工程師要么增加散熱片,要么降低反饋強度。機殼厚度小於5毫米的智慧型手機面臨著最嚴峻的權衡,因為溫度升高會限制中央處理器 (CPU) 的運行,這可能會降低整體效能。穿戴式裝置也面臨類似的限制,由於優先處理藍牙和感測器的處理負載,其電池容量極小,這進一步加劇了上述問題。汽車內裝暴露在超過70°C的環境溫度下,要求工程師選擇居里點高的材料並整合冗餘熱熔斷器,這兩項措施都會增加系統成本。這些限制正在減緩設計引進週期,並減緩觸覺技術市場的短期成長速度。

細分市場分析

到2025年,硬體將主導觸覺技術市場,佔據68.19%的銷售額,因為智慧型手機、汽車和遊戲機中出貨的每個單元都需要實體致動器和驅動積體電路。雖然單元數量的成長速度會隨著時間推移而放緩,但隨著偏心旋轉質量馬達被速度更快的線性諧振器(LRA)和日益普及的壓電堆所取代,硬體銷售額仍將佔據相當大的佔有率。儘管軟體在觸覺技術市場中所佔佔有率較小,但其成長勢頭強勁,預計到2031年複合年成長率將達到13.45%。這主要歸功於TouchSense和Lofelt等跨平台中間件,它們透過抽象化特定於裝置的波形庫來縮短開發週期。

軟體收入模式仍處於不斷變化之中。許多中間件授權與執行器採購捆綁銷售,限制了經常性商機。為了克服這項限制,供應商正在試驗將觸覺流與雲端渲染技術同步,並與視聽內容結合,將觸覺效果定位為一種服務,類似於空間音訊庫。這種轉變的關鍵在於解決延遲開銷問題,並確保支援最新 ISO 和 IEEE 標準中包含的轉碼器。如果雲端觸覺技術實用化,軟體可能會改變整個觸覺技術市場的價值分配,使其向利潤更高的經常性合約傾斜。

觸覺回饋技術,例如振動、皮膚拉伸和電觸覺刺激,由於其低功耗和小巧的尺寸,易於整合到智慧型手機和穿戴式裝置中,預計到2025年將佔據61.33%的收入佔有率。然而,隨著手術機器人和協作機器人的普及,力回饋和動覺回饋預計將超越觸覺回饋,預計其年複合成長率將達到13.41%。諸如達文西5等醫療系統能夠為外科醫生提供組織阻力向量的即時回饋,從而降低穿孔風險並縮短學習曲線。同時,配備六自由度力控把手的工業協作機器人可望將首次組裝良率提高25%。

由於皮膚電阻差異導致用戶間體驗不一致,電觸覺介面目前仍停留在實驗室階段。空氣傳播的超音波陣列雖然作用力有限,但憑藉其衛生優勢,在汽車資訊娛樂系統和公共資訊亭等領域找到了市場。高階XR手套中整合的皮膚拉伸裝置能夠傳遞剪切力,從而幫助識別虛擬紋理,但其高成本限制了其在企業級應用中的使用。總體而言,儘管消費性電子產品的銷售成長趨於穩定,但專業領域對動覺硬體的轉向正在推高平均售價,並擴大觸覺技術市場。

區域分析

預計亞太地區仍將是主要的收入驅動力,到2025年將佔據38.22%的市場佔有率。這主要得益於中國深圳和東莞龐大的智慧型手機組裝叢集、日本在壓電陶瓷領域的領先地位以及韓國在顯示整合模組方面的專業技術。在該地區,受電子和醫療設備設備領域對協作機器人需求的推動,預計到2030年,日本觸覺和力感測器的出貨量將以每年18%的速度成長。預計到2025年,中國電動車產量將超過900萬輛,這將推動低阻致動器(LRA)和壓電堆在方向盤和觸控主機中的應用,使區域零件製造商保持運作運轉。韓國企業正乘著折疊式智慧型手機普及的浪潮,採用曲面致動器,即使彎曲180度也能維持觸覺強度。

預計中東地區將呈現最高成長率,到2031年複合年成長率將達到13.68%,這主要得益於沙烏地阿拉伯「2030願景」的投資,該願景為虛擬實境(VR)醫療和國防模擬器提供資金;以及阿拉伯聯合大公國採購擴展實境(XR)人才發展模組。以色列國防相關企業正在部署觸覺回饋無人機站以降低任務失敗率,其應用範圍也正從民用設備擴展到其他領域。一家卡達新創公司成功資金籌措,計劃於2026年推出VR醫療課程,這表明當地企業正在拓展業務,與進口硬體形成互補,這些因素共同推動了該地區觸覺技術市場規模的成長。

在北美和歐洲,受強制性高級駕駛輔助系統 (ADAS)、手術機器人應用以及遊戲機更換週期的推動,複合年成長率 (CAGR) 穩定在個位數中段水平,但智慧型手機市場的飽和度限制了其成長。蘋果對美國本土市場進行多年 5,000 億美元的投資(使其先進製造基金規模翻倍),凸顯了其對客製化執行器設計研發的持續重視,旨在最大限度地減少第三方專利費支出。德州儀器投資 600 億美元擴建其模擬半導體製造地,確保了驅動積體電路的本地供應鏈,並增強了其抵禦地緣政治衝擊的能力。歐洲新車安全評鑑協會 (Euro NCAP) 將於 2026 年要求空調控制和危險警告控制設備必須配備觸覺確認功能,這扭轉了以往僅限於觸控螢幕的趨勢,預計將刺激對觸覺機械按鈕的需求,尤其是來自德國豪華汽車品牌的需求。儘管南美洲和非洲由於進口關稅和購買力低下而落後,但智慧型手機普及率的不斷提高正在穩步為觸覺技術市場的未來成長奠定基礎。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 智慧型手機的普及以及對觸覺回饋豐富的使用者體驗的需求。

- 用於ADAS和安全警報的汽車人機互動介面

- XR硬體(VR/AR/MR頭戴裝置和手套)的蓬勃發展

- 遊戲周邊設備和主機回饋的標準化

- MPEG-i 和 IEEE P1918.1 標準實現了跨平台觸覺內容。

- 用於遠端控制的5G觸覺網路試點項目

- 市場限制因素

- 高功率高精度執行器的熱設計

- 零件成本和機器設計的複雜性

- 專注於智慧財產權組合,Immersion面臨特許權使用費風險

- 碎片化的跨平台互通性

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 按組件

- 硬體

- 軟體

- 按反饋類型

- 觸覺(振動、皮膚拉伸、電觸覺)

- 力量/運動感覺

- 透過執行器技術

- 偏心旋轉質量(ERM)電機

- 線性諧振致動器(LRA)

- 壓電動器

- 超音波/機載超音波

- 靜電和動態薄膜

- 透過使用

- 消費性電子產品(智慧型手機、穿戴裝置、平板電腦、個人電腦)

- 遊戲和XR設備

- 汽車與交通運輸(人機互動、進階駕駛輔助系統、資訊娛樂系統)

- 醫療保健和醫療設備

- 工業與機器人

- 其他用途

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 其他亞太國家

- 中東

- 以色列

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 埃及

- 其他非洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Immersion Corporation

- AAC Technologies Holdings Inc.

- Texas Instruments Incorporated

- Alps Alpine Co., Ltd.

- Ultraleap Holdings Ltd.

- Microchip Technology Incorporated

- Johnson Electric Holdings Limited

- TDK Corporation(InvenSense Inc.)

- Synaptics Incorporated

- Analog Devices, Inc.

- Panasonic Corporation

- Samsung Electronics Co., Ltd.(System LSI)

- Boreas Technologies Inc.

- Novasentis Inc.

- HaptX Inc.

- bHaptics Inc.

- Senseg Oy

- Force Dimension SA

- Actronika SAS

- ON Semiconductor Corporation

- Sony Group Corporation

- Apple Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the haptic technology market size is expected to increase from USD 4.62 billion in 2025 to USD 5.23 billion in 2026 and reach USD 9.54 billion by 2031, growing at a CAGR of 12.76% over 2026-2031.

This report is Segmented by Component (Hardware and Software), Feedback Type (Tactile (Vibration, Skin-Stretch, Electro-Tactile) and Force/Kinesthetic), Actuator Technology (Eccentric Rotating Mass (ERM) Motors, Piezoelectric Actuators, and More), Application (Healthcare and Medical Devices, Industrial and Robotics, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Haptic Technology Market Trends and Insights

Smartphone Proliferation and Tactile-Rich UX Demand

Mobile device makers are now embedding multi-actuator arrays that localize feedback to specific on-screen elements, raising user satisfaction scores and aiding accessibility. Flagship platforms feature dual LRAs tuned to different frequency ranges so that keyboards feel crisp, notifications pulse discreetly, and gesture confirmations mimic physical buttons. Foldable form factors benefit from flexible actuators that curve without dampening amplitude, opening new design latitude for upcoming rollable phones. Because replacement cycles continue to lengthen in mature markets, tactile differentiation is emerging as a decisive retention lever. That shift has persuaded original-equipment manufacturers to raise bill-of-materials allocations for haptic subsystems, enhancing per-unit value in the haptic technology market.

Automotive HMIs for ADAS and Safety Alerts

Steer-by-wire and driver-monitoring features rely on vibration pulses and variable-resistance cues delivered through wheels, pedals, and seat structures. Kia deployed steering-wheel haptic warnings in its 2026 model-year vehicles, pulsing the rim when lane-departure or forward-collision systems detect imminent risk, a modality that proved 30% faster than dashboard-icon recognition in controlled studies. Euro NCAP rules taking effect in 2026 require physical climate and hazard controls for a five-star rating, indirectly boosting demand for tactile-confirmed buttons. Premium automakers are also experimenting with adaptive haptic profiles that shift steering feel between comfort and sport modes, deepening software-defined revenue prospects inside connected-car ecosystems.

High Power and Thermal Budgets of Precision Actuators

Piezoelectric stacks and electrostatic films demand elevated drive voltages that drain batteries and create hot spots, pressing engineers to add heat spreaders or scale back feedback intensity. Smartphones with sub-5 millimeter chassis depth face the starkest trade-offs because higher temperatures can throttle central-processing units, degrading overall performance. Wearables share similar constraints, magnified by tiny battery capacities that prioritize Bluetooth and sensor workloads. Automotive cabins endure ambient temperatures above 70 °C, forcing engineers to select materials with high Curie points and to integrate redundant thermal fuses, both of which increase system cost. These limitations slow design-in cycles and temper the short-term growth pace of the haptic technology market.

Other drivers and restraints analyzed in the detailed report include:

- XR Hardware Boom (VR-AR-MR Headsets and Gloves)

- Gaming Peripherals and Console Haptics Standardization

- Bill-of-Materials Cost and Mechanical Design Complexity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hardware dominated revenue with a 68.19% haptic technology market share in 2025 because smartphones, automobiles, and gaming consoles require physical actuators and driver ICs in every shipped unit. Although unit growth moderates over time, hardware revenue retains heft thanks to the replacement of eccentric rotating mass motors with faster LRAs and, increasingly, piezoelectric stacks. Software, capturing a smaller slice of the haptic technology market, is on a sharper 13.45% CAGR trajectory through 2031, as cross-platform middleware such as TouchSense and Lofelt shortens development cycles by abstracting device-specific waveform libraries.

The software revenue model remains in flux. Most middleware licenses ride along with actuator procurement, limiting recurring revenue opportunities. To counter that ceiling, vendors are piloting cloud-rendered tactile streams synchronized with audiovisual content, positioning haptic effects as a service similar to spatial-audio libraries. That pivot hinges on solving latency overheads and securing codec support embedded in recent ISO and IEEE standards. If cloud haptics proves viable, software could tilt the overall value pool of the haptic technology market toward higher-margin recurring contracts.

Tactile modalities, including vibration, skin stretch, and electro-tactile stimulation, accounted for 61.33% of 2025 revenue because of their low power draw and compact footprints, which map neatly onto smartphones and wearables. Yet force and kinesthetic feedback are forecast to outpace tactile, expanding at a 13.41% CAGR as surgical-robot and collaborative-robot installations multiply. Medical systems such as the da Vinci 5 route real-time tissue-resistance vectors back to surgeons, lowering perforation risk and shortening learning curves, while industrial cobots equipped with six-degree-of-freedom force handles yield 25% higher first-pass assembly yields.

Electrotactile interfaces remain laboratory curiosities due to variable skin impedance, which hampers user-to-user consistency. Mid-air ultrasonic arrays, although force-limited, find hygienic niches in automotive infotainment and public kiosks. Skin-stretch devices in premium XR gloves convey shear forces that facilitate virtual texture recognition but still carry premium costs, limiting adoption to enterprise bundles. Overall, the shift toward kinesthetic hardware in specialized domains boosts average selling prices, expanding the haptic technology market even as consumer-electronics volume growth stabilizes.

Geography Analysis

Asia-Pacific remained the revenue anchor with a 38.22% share in 2025, sustained by China's vast smartphone-assembly clusters in Shenzhen and Dongguan, Japan's piezoelectric ceramics leadership, and South Korea's display-integrated module know-how. The region where Japanese shipments of tactile and force sensors will grow 18% annually through 2030, propelled by demand for collaborative robots in electronics and medical equipment. Chinese electric-vehicle production exceeding 9 million units in 2025 is driving the insertion of LRAs and piezo stacks into steering wheels and touch consoles, keeping regional component makers at capacity. Korean companies are riding the wave of foldable-phone adoption, embedding curved actuators that function across 180-degree bends without degrading haptic intensity.

The Middle East is forecast to post the fastest CAGR of 13.68% through 2031, catalyzed by Saudi Vision 2030 investments that fund VR medical and defense simulators and by the United Arab Emirates' procurement of XR workforce-training modules. Israel's defense contractors are fielding haptic-enabled unmanned-vehicle stations that cut mission failure rates, diversifying applications beyond consumer devices. Qatar-based startups securing 2026 funding for VR medical courses demonstrate home-grown expansion that complements imported hardware, collectively uplifting the haptic technology market size in the region.

North America and Europe maintain steady mid-single-digit CAGRs on the back of ADAS mandates, surgical-robot installations, and console refresh cycles, although smartphone saturation places a ceiling on upside. Apple's multiyear USD 500 billion domestic investment, which doubles its Advanced Manufacturing Fund, underlines continued R&D focus on custom actuator design that minimizes third-party royalties. Texas Instruments' USD 60 billion analog-fab expansion secures local supply chains for driver ICs, buffering geopolitical shocks. Euro NCAP's 2026 requirement for tactile-verified climate and hazard controls reverses earlier touchscreen-only trends, set to stimulate demand for haptic-equipped mechanical buttons, particularly among premium German marques. South America and Africa trail because of import tariffs and lower purchasing power, yet rising smartphone penetration keeps a simmering baseline for future growth in the haptic technology market.

- Immersion Corporation

- AAC Technologies Holdings Inc.

- Texas Instruments Incorporated

- Alps Alpine Co., Ltd.

- Ultraleap Holdings Ltd.

- Microchip Technology Incorporated

- Johnson Electric Holdings Limited

- TDK Corporation (InvenSense Inc.)

- Synaptics Incorporated

- Analog Devices, Inc.

- Panasonic Corporation

- Samsung Electronics Co., Ltd. (System LSI)

- Boreas Technologies Inc.

- Novasentis Inc.

- HaptX Inc.

- bHaptics Inc.

- Senseg Oy

- Force Dimension SA

- Actronika SAS

- ON Semiconductor Corporation

- Sony Group Corporation

- Apple Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Smartphone Proliferation and Tactile-Rich UX Demand

- 4.2.2 Automotive HMIs for ADAS and Safety Alerts

- 4.2.3 XR Hardware Boom (VR/AR/MR Headsets and Gloves)

- 4.2.4 Gaming Peripherals and Console Haptics Standardization

- 4.2.5 MPEG-I and IEEE P1918.1 Standards Enabling Cross-Platform Haptic Content

- 4.2.6 5G Tactile-Internet Pilots for Remote Operations

- 4.3 Market Restraints

- 4.3.1 High Power and Thermal Budgets of Precision Actuators

- 4.3.2 Bill-of-Materials Cost and Mechanical Design Complexity

- 4.3.3 Concentrated IP Portfolio, Royalty Exposure to Immersion

- 4.3.4 Fragmented Cross-Platform Interoperability

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Hardware

- 5.1.2 Software

- 5.2 By Feedback Type

- 5.2.1 Tactile (Vibration, Skin-Stretch, Electro-Tactile)

- 5.2.2 Force / Kinesthetic

- 5.3 By Actuator Technology

- 5.3.1 Eccentric Rotating Mass (ERM) Motors

- 5.3.2 Linear Resonant Actuators (LRA)

- 5.3.3 Piezoelectric Actuators

- 5.3.4 Ultrasonic / Mid-Air Ultrasound

- 5.3.5 Electrostatic and Electro-Hydrodynamic Films

- 5.4 By Application

- 5.4.1 Consumer Electronics (Smartphones, Wearables, Tablets, PCs)

- 5.4.2 Gaming and XR Devices

- 5.4.3 Automotive and Transportation (HMI, ADAS, Infotainment)

- 5.4.4 Healthcare and Medical Devices

- 5.4.5 Industrial and Robotics

- 5.4.6 Other Applications

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 Middle East

- 5.5.4.1 Israel

- 5.5.4.2 Saudi Arabia

- 5.5.4.3 United Arab Emirates

- 5.5.4.4 Turkey

- 5.5.4.5 Rest of Middle East

- 5.5.5 Africa

- 5.5.5.1 South Africa

- 5.5.5.2 Egypt

- 5.5.5.3 Rest of Africa

- 5.5.6 South America

- 5.5.6.1 Brazil

- 5.5.6.2 Argentina

- 5.5.6.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Immersion Corporation

- 6.4.2 AAC Technologies Holdings Inc.

- 6.4.3 Texas Instruments Incorporated

- 6.4.4 Alps Alpine Co., Ltd.

- 6.4.5 Ultraleap Holdings Ltd.

- 6.4.6 Microchip Technology Incorporated

- 6.4.7 Johnson Electric Holdings Limited

- 6.4.8 TDK Corporation (InvenSense Inc.)

- 6.4.9 Synaptics Incorporated

- 6.4.10 Analog Devices, Inc.

- 6.4.11 Panasonic Corporation

- 6.4.12 Samsung Electronics Co., Ltd. (System LSI)

- 6.4.13 Boreas Technologies Inc.

- 6.4.14 Novasentis Inc.

- 6.4.15 HaptX Inc.

- 6.4.16 bHaptics Inc.

- 6.4.17 Senseg Oy

- 6.4.18 Force Dimension SA

- 6.4.19 Actronika SAS

- 6.4.20 ON Semiconductor Corporation

- 6.4.21 Sony Group Corporation

- 6.4.22 Apple Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet Need Analysis

觸覺技術市場-2026-2032年全球市場預測

觸覺技術市場-2026-2032年全球市場預測 觸覺技術全球市場規模、佔有率、趨勢和成長分析報告(2026-2034)觸覺回饋手術環境市場:按設備類型、組件、回饋方式、應用和最終用戶分類-2026-2032年全球市場預測

觸覺技術全球市場規模、佔有率、趨勢和成長分析報告(2026-2034)觸覺回饋手術環境市場:按設備類型、組件、回饋方式、應用和最終用戶分類-2026-2032年全球市場預測 2026年全球觸覺技術市場報告

2026年全球觸覺技術市場報告 觸覺技術市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、設備、最終用戶、功能及安裝類型分類

觸覺技術市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、設備、最終用戶、功能及安裝類型分類 觸覺技術市場報告:按組件、回饋、技術、應用和地區分類,2026-2034 年

觸覺技術市場報告:按組件、回饋、技術、應用和地區分類,2026-2034 年 汽車神經自我調整觸覺回饋組件市場機會、成長要素、產業趨勢分析及預測(2026-2035年)2026年全球表面觸覺技術市場報告2026年全球觸覺設備市場報告全球觸覺技術市場:市場規模、佔有率、成長率、產業分析、依類型、應用和地區劃分的分析及預測(2026-2034)

汽車神經自我調整觸覺回饋組件市場機會、成長要素、產業趨勢分析及預測(2026-2035年)2026年全球表面觸覺技術市場報告2026年全球觸覺設備市場報告全球觸覺技術市場:市場規模、佔有率、成長率、產業分析、依類型、應用和地區劃分的分析及預測(2026-2034)