|

市場調查報告書

商品編碼

1936493

汽車神經自我調整觸覺回饋組件市場機會、成長要素、產業趨勢分析及預測(2026-2035年)In-Vehicle Neuroadaptive Haptic Feedback Component Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

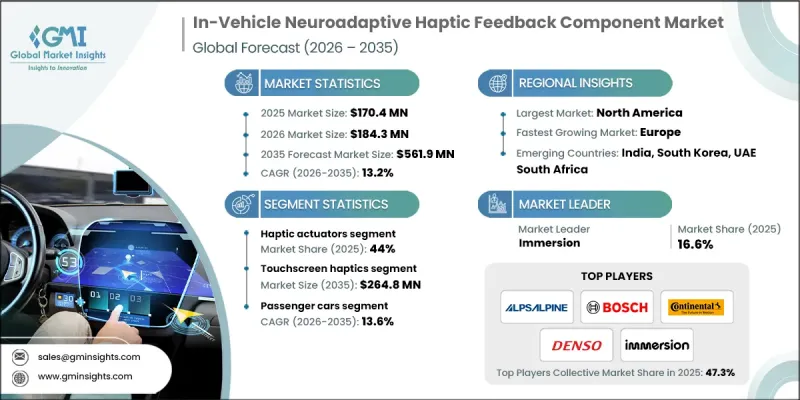

全球汽車自我調整觸覺回饋組件市場預計到 2025 年將達到 1.704 億美元,到 2035 年將達到 5.619 億美元,年複合成長率為 13.2%。

市場成長的驅動力在於人們越來越關注駕駛者的警覺性、即時反應能力以及減少車內認知和視覺干擾。汽車製造商正優先開發能夠幫助駕駛員根據不斷變化的心理和環境狀況快速感知並即時做出反應的系統。神經自適應觸覺回饋組件能夠根據即時生物識別數據和情境輸入調整觸覺回饋,幫助駕駛者保持警覺和專注,避免分心。這項轉變與智慧駕駛輔助技術和軟體主導內裝的普及相吻合,實體按鈕正逐漸被數位介面所取代。隨著內裝設計日益簡約和螢幕化,觸覺回饋在增強安全提示和提升易用性方面發揮關鍵作用。在高階車型領域,這種需求尤其突出,因為先進的人機互動是實現差異化的關鍵。隨著汽車設計不斷向直覺和自適應介面發展,神經自適應觸覺回饋組件在平衡系統複雜性、易用性和駕駛安全性方面變得至關重要。

| 市場覆蓋範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 1.704億美元 |

| 預測金額 | 5.619億美元 |

| 複合年成長率 | 13.2% |

觸覺致動器市場佔據44%的市場佔有率,預計到2025年將創造7,500萬美元的收入。致動器仍然是神經適應性觸覺系統的重要組成部分,因為它們可以將電子訊號轉化為駕駛者可以即時感知的物理感覺。儘管感測和軟體層面取得了進步,但其與車輛多個控制和介面點的廣泛整合將維持穩定的需求。

預計到 2025 年,觸控螢幕觸覺回饋市場佔有率將達到 48.4%,到 2035 年將達到 2.648 億美元。隨著數位顯示器成為車內主要控制介面,將觸覺回饋整合到觸控式介面中的需求日益成長,以支援直覺操作並最大限度地減少駕駛員分心。

美國汽車神經自適應觸覺回饋組件市場預計到2025年將達到4,710萬美元。美國高度重視道路安全,並大力推廣駕駛輔助技術,使其成為先進車載感測解決方案的領先採用者。由於大量車輛已配備智慧安全系統,美國將繼續為神經自適應觸覺技術提供強勁的成長基礎。

目錄

第1章調查方法

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 成本結構

- 每個階段的附加價值

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 促進要素

- 日益重視駕駛狀態感知與認知安全

- 自動駕駛和半自動駕駛能力的成長

- 原始設備製造商 (OEM) 推動差異化車載用戶體驗

- 對即時自適應人機互動的需求

- 產業潛在風險與挑戰

- 神經適應性回饋整合的系統複雜性很高

- 將觸覺回饋校準以適應個體認知差異所面臨的挑戰

- 市場機遇

- 與駕駛員監控系統整合

- 開發軟體定義且可升級的觸覺演算法

- 在高階電動車和軟體優先型汽車平臺的應用

- 未來認知型和響應型汽車人機互動的標準化

- 促進要素

- 成長潛力分析

- 監管環境

- 北美洲

- 美國國家公路交通安全管理局(NHTSA)

- 聯邦機動車輛安全標準(FMVSS)

- 美國汽車工程師協會(SAE International)

- 加拿大運輸部

- 歐洲

- 歐盟委員會(EC)

- 歐盟車輛類型認證機構(EU VTA)

- 德國聯邦汽車運輸管理局(KBA)

- 亞太地區

- 公路運輸和公路部(MoRTH)

- 中國汽車技術研究中心(CATARC)

- 南韓交通安全管理局(TS)

- 拉丁美洲

- 國家運輸管理局

- 巴西汽車製造商協會(ANFAVEA)

- 中東和非洲

- 海灣合作理事會標準組織(GSO)

- 南非標準局 (SABS)

- 沙烏地阿拉伯標準、計量和品質組織(SASO)

- 北美洲

- 波特五力分析

- PESTEL 分析

- 技術與創新展望

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 依產品

- 成本細分分析

- 永續性和環境影響

- 環境影響評估

- 社會影響力和社區參與

- 公司管治與企業社會責任

- 永續金融與投資趨勢

- 系統結構和技術棧分析

- 自我調整觸覺系統的架構

- 硬體層(感測器、致動器、控制器)

- 中介軟體層(訊號處理、驅動軟體)

- 應用層(人機介面整合、使用者應用)

- 系統延遲和性能要求

- 與ADAS和自動駕駛系統的整合

- ADAS與觸覺回饋之間的協同作用

- 與自動駕駛水平的整合

- 感測器與ADAS系統的融合

- 安全關鍵型觸覺回饋延遲要求

- 網路安全、資料隱私和功能安全的考慮

- 案例研究

- 未來前景與機遇

第4章 競爭情勢

- 介紹

- 公司市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 戰略展望矩陣

- 重大進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 企業擴張計畫和資金籌措

第5章 按組件分類的市場估算與預測,2022-2035年

- 觸覺致致動器

- 電磁致動器

- 壓電致動器

- 超音波相位陣列

- 神經適應性感測器

- 腦電圖(EEG)感測器

- 心電圖(ECG)感測器

- 眼動追蹤感應器

- 壓力和握力感測器

- 控制電子設備

- 軟體和演算法

第6章 2022-2035年按產品分類的市場估算與預測

- 觸控螢幕觸覺回饋

- 方向盤回饋系統

- 基於片材的觸覺模組

- 其他

第7章 依車輛類型分類的市場估計與預測,2022-2035年

- 搭乘用車

- 掀背車

- SUV

- 轎車

- 商用車輛

- 輕型商用車(LCV)

- MCV

- 重型商用車(HCV)

第8章 按車輛類型分類的市場估算與預測,2022-2035年

- 經濟型/入門級

- 中型車

- 豪華/高級汽車

9. 按自動駕駛等級分類的市場估算與預測,2022-2035 年

- 半自動駕駛汽車

- 全自動駕駛汽車

第10章 依應用領域分類的市場估計與預測,2022-2035年

- 駕駛輔助系統(ADAS)

- 資訊娛樂系統

- 安全和警報系統

- 舒適性和個性化系統

- 導航系統

第11章 依銷售管道分類的市場估計與預測,2022-2035年

- OEM

- 售後市場

第12章 2022-2035年各地區市場估算與預測

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 捷克共和國

- 比利時

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 新加坡

- 馬來西亞

- 印尼

- 越南

- 泰國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 哥倫比亞

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第13章:公司簡介

- 世界公司

- Cirrus Logic

- Continental

- DENSO

- Panasonic

- Robert Bosch

- TDK

- Texas Instruments

- Valeo

- Visteon

- ZF Friedrichshafen

- 當地公司

- Alps Alpine

- Autoliv

- Clarion

- Harman

- Hyundai Mobis

- Johnson Electric

- Yazaki

- 新興企業

- AAC Technologies

- HaptX

- Immersion

- Microchip

- ON Semiconductor

- Precision

- Synaptics

- Ultraleap

The Global In-Vehicle Neuroadaptive Haptic Feedback Component Market was valued at USD 170.4 million in 2025 and is estimated to grow at a CAGR of 13.2% to reach USD 561.9 million by 2035.

Market growth is driven by the rising focus on driver attention, real-time responsiveness, and the reduction of cognitive and visual distractions inside vehicles. Automakers are prioritizing systems that support rapid driver awareness and immediate physical response based on changing mental and environmental conditions. Neuroadaptive haptic feedback components rely on real-time biometric and contextual inputs to adjust tactile responses, helping drivers remain alert and engaged without diverting their focus. This shift aligns with the broader adoption of intelligent driver-support technologies and software-driven vehicle interiors, where physical buttons are increasingly replaced by digital interfaces. As vehicle cabins become more minimalistic and screen-oriented, tactile feedback plays a critical role in reinforcing safety cues and usability. Demand is especially strong in premium vehicle categories, where advanced human-machine interaction is a key differentiator. As automotive design continues to evolve toward intuitive and adaptive interfaces, neuroadaptive haptic feedback components are becoming essential for balancing system complexity with ease of use and driving safety.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $170.4 Million |

| Forecast Value | $561.9 Million |

| CAGR | 13.2% |

The haptic actuators segment held 44% share, generating USD 75 million in 2025. Actuators remain fundamental to neuroadaptive haptic systems because they transform electronic signals into physical sensations that drivers can perceive instantly. Their widespread integration across multiple vehicle control and interface points sustains consistent demand, regardless of progress in sensing or software layers.

The touchscreen haptics segment held 48.4% share in 2025 and is forecast to reach USD 264.8 million by 2035. As digital displays become the primary control surface within vehicles, tactile feedback integrated into touch-based interfaces is increasingly necessary to support intuitive operation and minimize driver distraction.

U.S In-Vehicle Neuroadaptive Haptic Feedback Component Market reached USD 47.1 million in 2025. Strong emphasis on road safety and high penetration of driver-assistance technologies have positioned the country as a leading adopter of advanced in-vehicle sensing solutions. With a large share of vehicles already equipped with intelligent safety systems, the U.S. continues to provide a strong growth platform for neuroadaptive haptic technologies.

Key companies operating in the In-Vehicle Neuroadaptive Haptic Feedback Component Market include Bosch, Continental, Valeo, Alps Alpine, ZF, Denso, Immersion, Hyundai Mobis, TDK, Ultraleap, and Cirrus Logic. Companies active in the in-vehicle neuroadaptive haptic feedback component market are strengthening their market position through continuous innovation in hardware-software integration and adaptive interface design. Many players are investing in advanced signal processing, real-time analytics, and AI-enabled feedback algorithms to improve responsiveness and personalization. Strategic collaborations with automotive manufacturers and platform developers are helping accelerate system integration into next-generation vehicles. Firms are also focusing on scalable component designs that support multiple vehicle categories while maintaining performance consistency. Expanding intellectual property portfolios, enhancing compatibility with digital cockpit architectures, and aligning solutions with evolving safety standards remain core priorities.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.8 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Product

- 2.2.4 Vehicle

- 2.2.5 Vehicle class

- 2.2.6 Autonomy level

- 2.2.7 Application

- 2.2.8 Sales channel

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing focus on driver state awareness and cognitive safety

- 3.2.1.2 Growth of autonomous and semi-autonomous driving features

- 3.2.1.3 OEM push for differentiated in-cabin user experience

- 3.2.1.4 Demand for real-time adaptive human-machine interaction

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High system complexity of neuro-adaptive feedback integration

- 3.2.2.2 Challenges in calibrating haptics to individual cognitive variability

- 3.2.3 Market opportunities

- 3.2.3.1 Integration with driver monitoring systems

- 3.2.3.2 Development of software-defined and upgradable haptic algorithms

- 3.2.3.3 Adoption in premium EV and software-first vehicle platforms

- 3.2.3.4 Future standardization of cognitive-responsive automotive HMIs

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 National Highway Traffic Safety Administration (NHTSA)

- 3.4.1.2 Federal Motor Vehicle Safety Standards (FMVSS)

- 3.4.1.3 Society of Automotive Engineers (SAE International)

- 3.4.1.4 Transport Canada

- 3.4.2 Europe

- 3.4.2.1 European Commission (EC)

- 3.4.2.2 European Union Vehicle Type-Approval Authorities (EU VTA)

- 3.4.2.3 German Federal Motor Transport Authority (KBA)

- 3.4.3 Asia Pacific

- 3.4.3.1 Ministry of Road Transport and Highways (MoRTH)

- 3.4.3.2 China Automotive Technology & Research Center (CATARC)

- 3.4.3.3 Korea Transportation Safety Authority (TS)

- 3.4.4 Latin America

- 3.4.4.1 National Traffic Department

- 3.4.4.2 Brazilian Association of Automotive Vehicle Manufacturers (ANFAVEA)

- 3.4.5 Middle East & Africa

- 3.4.5.1 GCC Standardization Organization (GSO)

- 3.4.5.2 South African Bureau of Standards (SABS)

- 3.4.5.3 Saudi Standards, Metrology and Quality Organization (SASO)

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Cost breakdown analysis

- 3.10 Sustainability and environmental impact

- 3.10.1 Environmental impact assessment

- 3.10.2 Social impact & community benefits

- 3.10.3 Governance & corporate responsibility

- 3.10.4 Sustainable finance & investment trends

- 3.11 System Architecture & Technology Stack Analysis

- 3.11.1 Neuroadaptive haptic system architecture

- 3.11.2 Hardware layer (sensors, actuators, controllers)

- 3.11.3 Middleware layer (signal processing, driver software)

- 3.11.4 Application layer (HMI integration, user applications)

- 3.11.5 System latency & performance requirements

- 3.12 Integration with ADAS & autonomous driving systems

- 3.12.1 ADAS-haptic feedback synergy

- 3.12.2 Autonomous driving level integration

- 3.12.3 Sensor fusion with ADAS systems

- 3.12.4 Latency requirements for safety-critical haptics

- 3.13 Cybersecurity, data privacy & functional safety considerations

- 3.14 Case studies

- 3.15 Future outlook & opportunities

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2022 - 2035 ($Mn)

- 5.1 Key trends

- 5.2 Haptic actuators

- 5.2.1 Electromagnetic actuators

- 5.2.2 Piezoelectric actuators

- 5.2.3 Ultrasonic phased arrays

- 5.3 Neuroadaptive sensors

- 5.3.1 EEG (Electroencephalography) sensors

- 5.3.2 ECG (Electrocardiography) sensors

- 5.3.3 Eye-tracking sensors

- 5.3.4 Pressure & grip sensors

- 5.4 Control electronics

- 5.5 Software & algorithms

Chapter 6 Market Estimates & Forecast, By Product, 2022 - 2035 ($Mn)

- 6.1 Key trends

- 6.2 Touchscreen haptics

- 6.3 Steering wheel feedback systems

- 6.4 Seat-based haptic modules

- 6.5 Others

Chapter 7 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Mn)

- 7.1 Key trends

- 7.2 Passenger cars

- 7.2.1 Hatchback

- 7.2.2 SUV

- 7.2.3 Sedan

- 7.3 Commercial vehicles

- 7.3.1 LCV

- 7.3.2 MCV

- 7.3.3 HCV

Chapter 8 Market Estimates & Forecast, By Vehicle Class, 2022 - 2035 ($Mn)

- 8.1 Key trends

- 8.2 Economy/entry-level

- 8.3 Mid-range

- 8.4 Luxury/premium

Chapter 9 Market Estimates & Forecast, By Autonomy Level, 2022 - 2035 ($Mn)

- 9.1 Key trends

- 9.2 Semi-autonomous vehicles

- 9.3 Fully autonomous vehicles

Chapter 10 Market Estimates & Forecast, By Application, 2022 - 2035 ($Mn)

- 10.1 Key trends

- 10.2 Driver assistance systems (ADAS)

- 10.3 Infotainment systems

- 10.4 Safety & warning systems

- 10.5 Comfort & personalization systems

- 10.6 Navigation systems

Chapter 11 Market Estimates & Forecast, By Sales Channel, 2022 - 2035 ($Mn)

- 11.1 Key trends

- 11.2 OEM

- 11.3 Aftermarket

Chapter 12 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn)

- 12.1 Key trends

- 12.2 North America

- 12.2.1 US

- 12.2.2 Canada

- 12.3 Europe

- 12.3.1 Germany

- 12.3.2 UK

- 12.3.3 France

- 12.3.4 Italy

- 12.3.5 Spain

- 12.3.6 Russia

- 12.3.7 Czech Republic

- 12.3.8 Belgium

- 12.3.9 Netherlands

- 12.4 Asia Pacific

- 12.4.1 China

- 12.4.2 India

- 12.4.3 Japan

- 12.4.4 South Korea

- 12.4.5 Australia

- 12.4.6 Singapore

- 12.4.7 Malaysia

- 12.4.8 Indonesia

- 12.4.9 Vietnam

- 12.4.10 Thailand

- 12.5 Latin America

- 12.5.1 Brazil

- 12.5.2 Mexico

- 12.5.3 Argentina

- 12.5.4 Colombia

- 12.6 MEA

- 12.6.1 South Africa

- 12.6.2 Saudi Arabia

- 12.6.3 UAE

Chapter 13 Company Profiles

- 13.1 Global players

- 13.1.1 Cirrus Logic

- 13.1.2 Continental

- 13.1.3 DENSO

- 13.1.4 Panasonic

- 13.1.5 Robert Bosch

- 13.1.6 TDK

- 13.1.7 Texas Instruments

- 13.1.8 Valeo

- 13.1.9 Visteon

- 13.1.10 ZF Friedrichshafen

- 13.2 Regional players

- 13.2.1 Alps Alpine

- 13.2.2 Autoliv

- 13.2.3 Clarion

- 13.2.4 Harman

- 13.2.5 Hyundai Mobis

- 13.2.6 Johnson Electric

- 13.2.7 Yazaki

- 13.3 Emerging players

- 13.3.1 AAC Technologies

- 13.3.2 HaptX

- 13.3.3 Immersion

- 13.3.4 Microchip

- 13.3.5 ON Semiconductor

- 13.3.6 Precision

- 13.3.7 Synaptics

- 13.3.8 Ultraleap

觸覺技術市場-2026-2032年全球市場預測

觸覺技術市場-2026-2032年全球市場預測 觸覺技術:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

觸覺技術:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 觸覺技術全球市場規模、佔有率、趨勢和成長分析報告(2026-2034)觸覺回饋手術環境市場:按設備類型、組件、回饋方式、應用和最終用戶分類-2026-2032年全球市場預測

觸覺技術全球市場規模、佔有率、趨勢和成長分析報告(2026-2034)觸覺回饋手術環境市場:按設備類型、組件、回饋方式、應用和最終用戶分類-2026-2032年全球市場預測 2026年全球觸覺技術市場報告

2026年全球觸覺技術市場報告 觸覺技術市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、設備、最終用戶、功能及安裝類型分類

觸覺技術市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、設備、最終用戶、功能及安裝類型分類 觸覺技術市場報告:按組件、回饋、技術、應用和地區分類,2026-2034 年2026年全球表面觸覺技術市場報告2026年全球觸覺設備市場報告全球觸覺技術市場:市場規模、佔有率、成長率、產業分析、依類型、應用和地區劃分的分析及預測(2026-2034)

觸覺技術市場報告:按組件、回饋、技術、應用和地區分類,2026-2034 年2026年全球表面觸覺技術市場報告2026年全球觸覺設備市場報告全球觸覺技術市場:市場規模、佔有率、成長率、產業分析、依類型、應用和地區劃分的分析及預測(2026-2034)