|

市場調查報告書

商品編碼

2062426

靜態應用程式安全掃瞄:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)Static Application Security Testing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

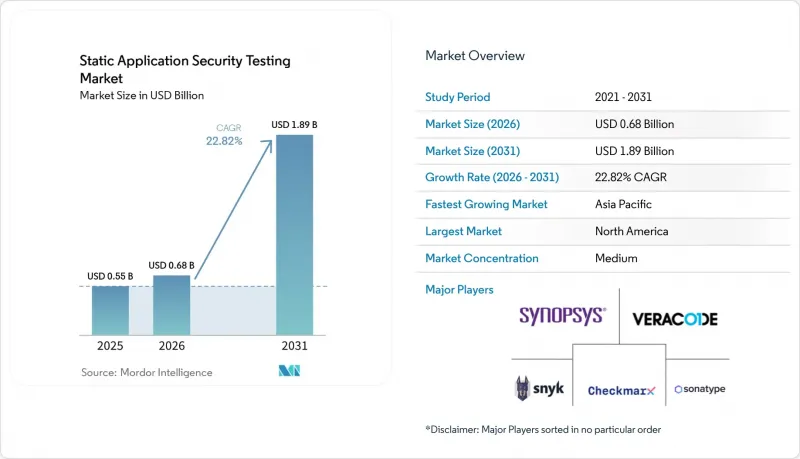

據 Mordor Intelligence 稱,2025 年靜態應用程式安全掃瞄市值為 5.5 億美元,預計到 2031 年將達到 18.9 億美元,而 2026 年為 6.8 億美元,2026 年至 2031 年的複合年成長率為 22.82%。

本報告按部署類型(本地部署、雲端部署、混合部署)、組織規模(大型企業、中小企業)、最終用戶產業(IT與電信、銀行、金融服務等)、整合階段(IDE外掛程式、CI/CD管線等)和地區進行細分。市場預測以美元計價。

全球靜態應用程式安全掃瞄市場趨勢與洞察

向 API 優先的軟體開發生命週期 (SDLC) 過渡

現代軟體依賴透過明確定義的 API 端點進行通訊的微服務。為單體程式碼建置的靜態掃描器往往會忽略這些端點處的驗證漏洞和過度資料外洩。零售商 Sally Beauty 透過在部署支援 API 的掃描器後 30 天內全面了解其 API 資產,展現了其顯著優勢。遷移到以 API 為中心的架構的組織報告稱,透過使用能夠分析 Swagger 和 OpenAPI 檔案(而不僅僅是原始程式碼)的掃描器,漏洞偵測率提高了 40%。這種高級功能正在推高平均售價,並促進整個靜態應用程式安全掃瞄市場的收入成長。這種成長要素在微服務應用最為成熟的北美和西歐地區最為顯著。

軟體SBOM的強制性要求

政府強制要求供應商提交軟體材料清單(SBOM),列出所有開放原始碼元件。 OWASP 2025 年安全建議指出,60% 的 Java 關鍵漏洞都源自於第三方函式庫,買家將 SBOM 的功能視為程式碼安全性的證明。美國聯邦機構,例如美國醫療保險和醫療補助服務中心 (CMS),已經實施了秘密掃描策略,獎勵那些能夠進行即時依賴監控的供應商。能夠自動產生 SBOM 並將掃描結果與已知 CVE 進行配對的供應商正在擴大其目標基本客群,並推動靜態應用程式安全掃瞄市場的成長。

大量假陽性導致的疲勞

安全分析師70%的調查時間都耗費在最終被證實無關緊要的警報上。這種負擔削弱了信任,並延緩了新策略的實施。小規模的團隊通常會屏蔽掃描器的輸出,這增加了漏檢漏洞的風險。供應商正在利用機器學習分類器來解決這個問題,將誤報率降低到0.1%以下,但高級模組的額外成本讓許多負責人猶豫不決。在入門級產品線的準確性得到提升之前,安全應用安全測試工具(SAST)的採購週期可能會很長。

細分市場分析

到2025年,本地部署將佔總收入的47.02%,這主要得益於歐洲銀行、國防相關企業和醫療保健機構為了滿足DORA和GDPR等監管要求,將程式碼庫置於防火牆之後。靜態應用程式安全掃瞄市場的成長則歸功於為高可靠性環境提供的專業服務捆綁式永久許可證。然而,受彈性運算的推動,雲端掃描預計到2031年將以24.4%的複合年成長率成長,彈性運算能夠加速跨微服務的平行掃描。混合模式將工件保留在本地,同時將運算任務卸載到託管的雲端節點,這種架構正在成為受監管企業的首選,兼顧了自主性和可擴展性。

控制與速度之間的平衡是採購決策的關鍵。雲端平台提供與 GitHub、GitLab 和 Azure DevOps 的原生整合,可加速價值實現,而本地部署則會產生基礎架構維護成本。超超大規模資料中心業者服務商提供的獨立雲端區域可能會削弱本地工具的合規性優勢。無論部署選項為何,都能提供相同功能集且價格不變的供應商,在 SAST 市場中最具優勢,能夠贏得那些正在滿足不斷變化的資料居住需求的企業客戶。

大型企業在2025年透過將SAST整合到其龐大的程式碼庫中並要求高度客製化,獲得了70.3%的收入。他們正在協商包含培訓、高級支援和服務等級協議(SLA)在內的全公司範圍契約,從而獲得可預測的續約收入。同時,預計到2031年,中小企業(SME)的收入將以23.3%的複合年成長率(CAGR)實現兩位數成長,因為供應商正在採用「按開發者付費」的授權模式和計量型的掃描方式來降低前期成本。

GitHub 和 SonarSource 提供的免費社群計畫正在推動其普及,而人工智慧驅動的修復功能則降低了解讀取掃描結果所需的專業知識。隨著中小企業的成熟,向 SBOM 生成和跨文件污點分析等高級功能提升銷售可以提高合約價值。擅長「先落地後擴展」策略的供應商正在將基層開發人員的採用轉變為全組織範圍的部署,從而擴大靜態應用程式安全掃瞄在中型企業的市場滲透率。

區域分析

預計到2025年,北美將佔總收入的38.2%,這主要得益於美國網路安全和基礎設施安全局 (CISA) 3.31億美元的持續診斷和緩解 (CDM) 預算,以及將靜態應用安全測試 (SAST) 作為合約交付內容納入的嵌入式(SBOM) 試點項目。美國管理和預算辦公室 (OMB) 正在轉向基於風險的驗證,評估將靜態檢查結果與運行時風險關聯起來的平台,從而改變聯邦供應商的採購趨勢。加拿大在採購要求標準化方面取得了進展,墨西哥監管機構正在對跨境銀行應用類似DORA的營運測試,從而擴大了區域成長潛力。

亞太地區正經歷最快成長,預計到2031年複合年成長率將達到25.27%。台灣的《2025年國家網路安全戰略》呼籲在整個半導體和基礎設施供應鏈中貫徹「安全設計」理念。紐西蘭的《2026-2030年網路安全藍圖》旨在為量子技術做好準備,並加強關鍵基礎設施的韌性,迫使公共產業採用程式碼掃描技術。中國、日本、印度和韓國的監管碎片化加劇了在地化難度,這有利於擁有多語言規則集和區域支援團隊的供應商。

歐洲正處於合規性十字路口。 《資料保護法》(DORA)將於2025年1月生效,該法案強制要求在四小時內報告安全事件,並實施以威脅主導的穿透測試週期,包括原始碼評估。同時,《網路與資訊系統指令》(NIS2)和《網路彈性法》也提出了更多要求。截至2025年中期,27個成員國中只有14個將NIS2完全納入其國家立法,但由於違規罰款最高可達1,000萬歐元(1,180萬美元),企業正在加速採用安全行動工作小組(SAST)認證。儘管銀行和保險公司仍然偏愛主權雲端並嚴重依賴本地部署解決方案,但混合模式因其兼顧監控和柔軟性而越來越受歡迎。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 軟體開發生命週期向 API 優先模式的轉變

- 關於軟體SBOM的法規

- 人工智慧生成程式碼的興起

- DevSecOps 工具鏈整合

- 對抗量子密碼進行審計的必要性

- 安全設計採購條款

- 市場限制因素

- 高假陽性率導致的疲勞

- 應用安全工程師短缺

- 重構遺留單體系統的成本

- 遵守資料居住要求的挑戰

- 產業價值鏈分析

- 宏觀經濟因素對市場的影響

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 部署模式

- 現場

- 基於雲端的

- 混合

- 按組織規模

- 大公司

- 小型企業

- 按最終用戶行業分類

- 資訊科技/通訊

- 銀行業、金融服務業及保險業

- 醫療保健和生命科學

- 政府/國防

- 零售與電子商務

- 製造業/汽車

- 其他終端用戶產業(能源、教育)

- 透過整合階段

- IDE插件

- CI/CD 管道

- 集中掃描

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 其他亞太國家

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 其他非洲國家

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Synopsys Inc.

- Veracode Inc.

- Checkmarx Ltd.

- IBM Corporation

- Micro Focus Software Inc.(OpenText)

- HCL Software

- GitLab Inc.

- GitHub Inc.

- SonarSource SA

- Perforce Software Inc.(Klocwork)

- CAST Software

- Parasoft Corporation

- GrammaTech Inc.

- Embold Technologies GmbH

- Kiuwan Software SL

- Contrast Security Inc.

- ShiftLeft Inc.

- DeepSource Technologies Inc.

- RIPS Technologies

- OX-Security Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the static application security testing market size was valued at USD 0.55 billion in 2025 and is expected to grow from USD 0.68 billion in 2026 to reach USD 1.89 billion by 2031, at a 22.82% CAGR over 2026-2031.

This report is Segmented by Deployment Mode (On-Premises, Cloud-Based, and Hybrid), Organization Size (Large Enterprises, and Small and Medium Enterprises), End-User Industry (IT and Telecommunications, Banking, Financial Services, and More), Integration Phase (IDE Plugins, CI/CD Pipeline, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Static Application Security Testing Market Trends and Insights

API-first SDLC shift

Modern software relies on microservices that communicate through well-defined API endpoints. Static scanners built for monolithic code often miss authentication weaknesses or excessive data exposure across these endpoints. Retailer Sally Beauty gained full API inventory visibility within 30 days by adding API-aware scanners, underscoring measurable benefits. Organisations shifting to API-centric architectures report 40% higher vulnerability detection when using scanners that parse Swagger or OpenAPI files alongside source code. This premium capability raises average selling prices, lifting revenue across the static application security testing market. The driver remains strongest in North America and Western Europe where microservices adoption is most mature.

Mandates on software SBOMs

Government orders now require suppliers to ship a software bill of materials that lists every open-source component. The OWASP 2025 advisory links 60% of critical Java bugs to third-party libraries, so buyers view SBOM functions as proof of secure code. Federal agencies such as the US Centers for Medicare & Medicaid Services have rolled out secret-scanning policies that reward vendors capable of real-time dependency monitoring. Vendors that automate SBOM generation and correlate findings with known CVEs widen their addressable base, fuelling growth for the static application security testing market.

High false-positive fatigue

Security analysts dedicate 70% of investigation time to alerts that turn out to be non-issues. This burden erodes trust and slows rollout of new policies. Smaller teams often mute scanner output, raising the risk of missed exploits. Vendors respond with machine-learning classifiers that push false-positive rates below 0.1%, but premium modules add cost that many mid-market buyers hesitate to absorb. Until accuracy improves across entry-level tiers, purchase cycles in the SAST market may elongate.

Other drivers and restraints analyzed in the detailed report include:

- Rise of AI-generated code

- DevSecOps tool-chain consolidation

- Shortage of AppSec engineers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

On-premises deployments held 47.02% of 2025 revenue as European banks, defense contractors, and healthcare providers retain code repositories behind their firewalls to meet DORA and GDPR oversight. Static application security testing market size gains here come from perpetual licenses bundled with professional services for high-assurance environments. Cloud-based scanning will nonetheless climb at a 24.4% CAGR to 2031, propelled by elastic compute that accelerates parallel scans across microservices. Hybrid models, which keep artifacts local yet offload compute to managed cloud nodes, balance sovereignty with scale and are emerging as preferred architectures for regulated entities.

Control versus velocity defines purchasing decisions. Cloud platforms integrate natively with GitHub, GitLab, and Azure DevOps, shrinking time-to-value, while on-premises installations incur infrastructure maintenance costs. Sovereign cloud regions offered by hyperscalers could erode the compliance advantage of on-premises tools. Vendors delivering identical feature sets across deployment options without price penalties position best to capture organizations navigating evolving residency mandates in the SAST market.

Large enterprises generated 70.3% of 2025 revenue by embedding SAST into sprawling codebases and demanding deep customization. They negotiate enterprise-wide contracts that fold in training, premium support, and SLAs, producing predictable renewal streams. Small and medium enterprises, however, are forecast to add double-digit revenue at a 23.3% CAGR through 2031 as vendors introduce per-developer seat models and metered scanning that drop upfront costs.

Free community tiers from GitHub and SonarSource seed adoption, while AI-guided remediation lowers the expertise needed to interpret scan results. Once SMEs mature, upselling advanced capabilities such as SBOM generation and cross-file taint analysis increases contract value. Vendors excelling at land-and-expand motions convert grassroots developer adoption into organization-wide rollouts, expanding static application security testing market penetration across the mid-market.

Geography Analysis

North America captured 38.2% of 2025 revenue, propelled by CISA's USD 331 million Continuous Diagnostics and Mitigation budget and embedded SBOM pilots that turn SAST into a contract deliverable. OMB's shift to risk-based attestations rewards platforms that correlate static findings with runtime exposure, driving refreshed procurement among federal suppliers. Canada is aligning procurement language, and Mexican regulators are applying DORA-style operational testing to cross-border banks, extending regional headroom.

Asia-Pacific is the fastest mover with a 25.27% CAGR forecast to 2031. Taiwan's 2025 National Cybersecurity Strategy requires secure-by-design attestations across semiconductor and infrastructure supply chains. New Zealand's 2026-2030 cybersecurity roadmap targets quantum readiness and critical-infrastructure resilience, prompting utilities to adopt code scanning. Fragmented regulations in China, Japan, India, and South Korea create localization complexity that favors vendors with multilingual rule sets and regional support teams.

Europe sits at a compliance crossroads. DORA took effect in January 2025, imposing four-hour incident reporting and threat-led penetration cycles that include source-code assessments, while NIS2 and the Cyber Resilience Act layer additional obligations. Only 14 of 27 member states fully transposed NIS2 by mid-2025, yet enforcement fines reach EUR 10 million (USD 11.8 million), pushing enterprises to fast-track SAST rollouts. Sovereign-cloud incentives and on-premises favoritism persist among banks and insurers, but hybrid models broaden appeal by balancing oversight with elasticity.

- Synopsys Inc.

- Veracode Inc.

- Checkmarx Ltd.

- IBM Corporation

- Micro Focus Software Inc. (OpenText)

- HCL Software

- GitLab Inc.

- GitHub Inc.

- SonarSource SA

- Perforce Software Inc. (Klocwork)

- CAST Software

- Parasoft Corporation

- GrammaTech Inc.

- Embold Technologies GmbH

- Kiuwan Software SL

- Contrast Security Inc.

- ShiftLeft Inc.

- DeepSource Technologies Inc.

- RIPS Technologies

- OX-Security Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 API-First SDLC Shift

- 4.2.2 Mandates on Software SBOMs

- 4.2.3 Rise of AI-Generated Code

- 4.2.4 DevSecOps Tool-Chain Consolidation

- 4.2.5 Quantum-Resistant Cryptography Audit Need

- 4.2.6 Secure-by-Design Procurement Clauses

- 4.3 Market Restraints

- 4.3.1 High False-Positive Fatigue

- 4.3.2 Shortage of AppSec Engineers

- 4.3.3 Legacy Monolith Refactoring Cost

- 4.3.4 Data-Residency Compliance Hurdles

- 4.4 Industry Value Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Buyer Power

- 4.8.3 Supplier Power

- 4.8.4 Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Mode

- 5.1.1 On-Premises

- 5.1.2 Cloud-Based

- 5.1.3 Hybrid

- 5.2 By Organization Size

- 5.2.1 Large Enterprises

- 5.2.2 Small and Medium Enterprises

- 5.3 By End-User Industry

- 5.3.1 IT and Telecommunications

- 5.3.2 Banking, Financial Services and Insurance

- 5.3.3 Healthcare and Life Sciences

- 5.3.4 Government and Defense

- 5.3.5 Retail and E-Commerce

- 5.3.6 Manufacturing and Automotive

- 5.3.7 Other End-User Industry (Energy, Education)

- 5.4 By Integration Phase

- 5.4.1 IDE Plugins

- 5.4.2 CI/CD Pipeline

- 5.4.3 Centralized Scanning

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Synopsys Inc.

- 6.4.2 Veracode Inc.

- 6.4.3 Checkmarx Ltd.

- 6.4.4 IBM Corporation

- 6.4.5 Micro Focus Software Inc. (OpenText)

- 6.4.6 HCL Software

- 6.4.7 GitLab Inc.

- 6.4.8 GitHub Inc.

- 6.4.9 SonarSource SA

- 6.4.10 Perforce Software Inc. (Klocwork)

- 6.4.11 CAST Software

- 6.4.12 Parasoft Corporation

- 6.4.13 GrammaTech Inc.

- 6.4.14 Embold Technologies GmbH

- 6.4.15 Kiuwan Software SL

- 6.4.16 Contrast Security Inc.

- 6.4.17 ShiftLeft Inc.

- 6.4.18 DeepSource Technologies Inc.

- 6.4.19 RIPS Technologies

- 6.4.20 OX-Security Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

2026年全球內容過濾與反垃圾郵件設備市場報告

2026年全球內容過濾與反垃圾郵件設備市場報告 行動應用安全測試市場預測-全球分析(按交付方式、企業規模、部署模式、作業系統、最終用戶和地區分類)——2034年

行動應用安全測試市場預測-全球分析(按交付方式、企業規模、部署模式、作業系統、最終用戶和地區分類)——2034年 應用安全市場:按類型、組件、產業、部署模式和組織規模分類-2026-2032年全球市場預測

應用安全市場:按類型、組件、產業、部署模式和組織規模分類-2026-2032年全球市場預測 應用安全市場規模、佔有率、趨勢和預測:按組件、類型、測試類型、部署模式、組織規模、行業和地區分類(2026-2034 年)

應用安全市場規模、佔有率、趨勢和預測:按組件、類型、測試類型、部署模式、組織規模、行業和地區分類(2026-2034 年) 應用安全市場規模、佔有率、成長率及全球產業分析:按類型、應用和地區的洞察,2026-2034年的預測2026年全球行動網路釣魚防範措施市場報告行動應用安全測試市場:依測試類型、測試方法、應用平台和部署方式分類-2026-2032年全球市場預測2026年全球應用安全市場報告

應用安全市場規模、佔有率、成長率及全球產業分析:按類型、應用和地區的洞察,2026-2034年的預測2026年全球行動網路釣魚防範措施市場報告行動應用安全測試市場:依測試類型、測試方法、應用平台和部署方式分類-2026-2032年全球市場預測2026年全球應用安全市場報告 應用安全:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)室內安防巡邏機器人市場:按組件、自主等級、移動性、最終用戶和應用分類-全球預測,2026-2032年

應用安全:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)室內安防巡邏機器人市場:按組件、自主等級、移動性、最終用戶和應用分類-全球預測,2026-2032年