|

市場調查報告書

商品編碼

2062397

奈米黏土增強材料:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Nanoclay Reinforcement - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

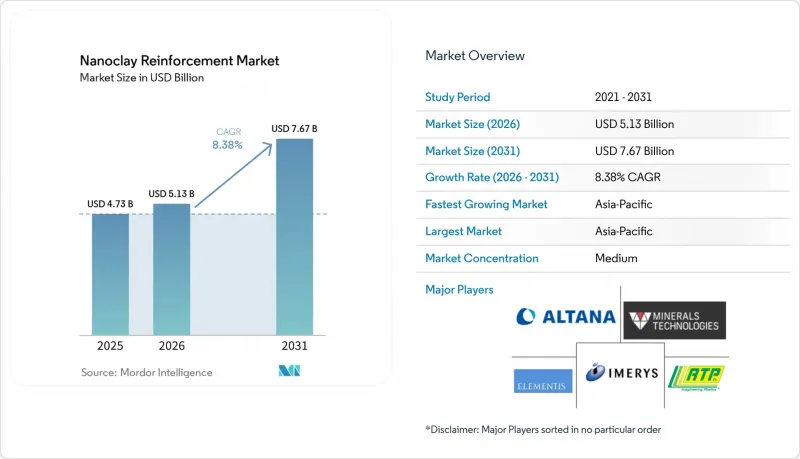

據 Mordor Intelligence 稱,2025 年奈米黏土增強材料市值為 47.3 億美元,預計到 2031 年將從 2026 年的 51.3 億美元成長至 76.7 億美元,預測期(2026-2031 年)複合年成長率為 8.38%。

本報告按類型(蒙脫石、高嶺石、蒙脫石、埃洛石、伊利石、鋰蒙脫石)、形態(粉末、母粒、分散體)、增強基體(熱塑性塑膠、熱固性塑膠、彈性體、生物聚合物、其他)、最終用戶(包裝、汽車、建築、電子、醫療保健等)和地區(亞太地區、北美等)細分。市場預測以美元計價。

全球奈米黏土增強材料市場趨勢及洞察

對高性能、輕質複合材料的快速需求

航太領域的原始設備製造商 (OEM) 目前正使用蒙脫石增強環氧樹脂預浸料作為二級結構材料。這種輕量化選擇顯著降低了每架飛機的全生命週期燃料成本。在汽車領域,一級供應商正將類似的方法應用於電池外殼。在這種應用中,奈米黏土改質聚醯胺 6 不僅能將火焰傳播速度降低到臨界閾值以下,還能減輕機殼的質量。風力發電機葉片製造商正在採用基於鋰蒙脫石的觸變劑。這可以減少廢棄物並縮短固化週期,從而縮短專案前置作業時間。然而,當客戶更換供應商時,這些進步也會帶來成本。每種應用都需要針對所用樹脂量身定做的獨特表面改質配方,這使得現有供應商免受商品價格波動的影響。因此,即使與原油價格掛鉤的聚合物價格呈下降趨勢,奈米黏土增強材料市場的新訂單仍然激增。

奈米複合材料在汽車和航太領域的應用日益廣泛

奈米黏土和磷的協同效應正日益廣泛地應用於電池組、客艙空氣管理組件和引擎室面板。這種組合能夠在極少添加劑的情況下實現高臨界氧指數值。碳纖維製造商目前供應經有機黏土預處理的絲束,這簡化了預浸料製造商的流程,並確保了批次間品質的一致性。在航太領域,人們發現片狀黏土增強的雙馬來亞醯胺基材料的吸濕性降低。這項進步使得檢測間隔得以延長。這些進展不僅維持了對複合材料生產商的高需求,也凸顯了市場的重大轉變:奈米黏土增強產品正從零星引入轉向系統性整合。

高昂的處理成本和複雜的配送流程

為了確保均勻分層,加工商通常選擇客製化的雙螺桿擠出機。然而,分散不充分會導致結塊,降低拉伸強度,並增加缺陷率,而奈米黏土產業對產品品質的要求極高。含有奈米粘土的母粒可以解決這個問題,但其成本高於標準有機粘土粉。此外,雖然專有表面活性劑包裝簡化了混合過程,但也使加工商受制於獨家契約,限制了競爭性競標。這些因素阻礙了奈米黏土增強材料市場的發展,尤其對於小規模混煉企業而言更是如此。

細分市場分析

2025年,蒙脫石佔據奈米黏土增強材料市場40.21%的主導佔有率,主要服務大眾市場汽車和包裝產業。同時,儘管埃洛石的市佔率較小,但預計在2026年至2031年的預測期內,其複合年成長率將達到8.77%,實現顯著成長。這一成長主要歸功於埃洛石10:1至30:1的理想長寬比,使其能夠承載10-15%的藥物,性能顯著優於片狀黏土。

懷俄明州的膨潤土礦和土耳其的鋰蒙脫石礦保證了蒙脫石的穩定供應,鞏固了蒙脫石在散裝市場的主導地位。相較之下,醫院則投入更高的預算用於藥用級鹵石塗層,這種塗層可在數週內釋放銀離子,從而在奈米粘土增強材料市場中佔據高階地位。

到2025年,粉狀奈米黏土增強材料將佔據47.48%的市場。同時,母粒的銷售額預計在2026年至2031年的預測期內將以8.92%的複合年成長率成長。這一成長主要歸因於加工商更傾向於使用即用型分散體,而不是投資傳統的雙螺桿擠出機。

以正確的稀釋比例使用時,RTP 的有機黏土母粒可顯著增強聚乙烯薄膜的氧氣阻隔性。這項進步不僅透過最大限度地縮短換型時間最佳化了操作流程,而且凸顯了 RTP 產品的卓越效率。分散體和溶液形式雖然面臨一些挑戰(主要是由於溶劑加工成本高昂),但它們在噴塗製程中發揮著至關重要的作用,尤其是在設備剪切力受限的情況下。

區域分析

到2025年,亞太地區以37.04%的市佔率佔據主導地位,預計在2026年至2031年的預測期內將維持強勁成長,複合年成長率(CAGR)為9.18%。中國主導,已將數百萬輛配備符合GB 38031-2020標準的奈米黏土複合電池組的電動車推向市場。在印度,受食品安全部門更嚴格的進口限制的推動,片狀黏土在軟性包裝中的應用顯著增加。在日本,鹵石加工擴大,用於生產高純度醫用級材料;而韓國電池製造商透過使用精確填充的聚醯胺外殼,實現了顯著的減重。

在北美,懷俄明州扮演著核心角色,並佔據了巨大的市場佔有率。懷俄明州每年數百萬噸的膨潤土供應為國內複合材料生產商提供了穩定的原料來源。航太產業的主要公司根據美國太空總署(NASA)的燃油效率目標,將奈米黏土預浸料應用於引擎短艙。 2025年,受惠於近岸外包的墨西哥汽車工業對引擎室零件的需求激增。

在歐洲,儘管受到歐洲食品安全局 (EFSA) 的延誤,這項技術仍獲得了顯著的市場佔有率並實現了穩步成長。 2024 年,德國原始設備製造商 (OEM) 在其所有平台上都採用了符合 UL 94 V-0 標準的奈米黏土聚醯胺機殼。在法國,利用血小板阻隔瓶的創新技術已成功顯著延長了葡萄酒的保存期限。在西班牙,奈米黏土複合材料的引入大幅減少了除草劑徑流。同時,英國一項小規模的纖維水泥覆層試點計畫在格倫費爾大廈火災後,因安全法規的訂定而備受關注。

儘管南美洲、中東和非洲的市場佔有率相對較小,但巴西的石化襯裡和沙烏地阿拉伯的密封劑銷售量保持穩定,南非的礦場泥漿管道磨損也顯著降低。儘管市場佔有率不大,但這些地區始終滿足訂單需求,並在2026年至2031年的預測期內為奈米黏土增強材料市場的整體成長做出了貢獻。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 對高性能、輕質複合材料的需求激增

- 奈米複合材料在汽車和航太領域的應用日益廣泛

- 推動制定具有增強阻隔性能的永續包裝法規

- 經濟高效的層間插入和層壓技術取得了突破性進展。

- 電動車電池機殼需要阻燃複合材料

- 市場限制因素

- 高昂的處理成本和複雜的經銷流程

- 關於奈米黏土作為食品接觸材料的環境、健康與安全 (EHS) 和相關法規不確定性。

- 與石墨烯、碳奈米管和其他奈米添加劑的競爭

- 價值鏈分析

- 技術展望

- 波特五力模型

第5章 市場規模與成長預測

- 按類型

- 蒙脫石

- 高嶺土

- 蒙脫石

- 埃洛石

- 伊利石

- 鋰蒙脫石

- 按形式

- 粉末

- 母粒

- 分散劑和溶液

- 按類型分類的增強矩陣

- 熱塑性塑膠

- 熱固性樹脂

- 彈性體

- 生物聚合物

- 其他聚合物體系

- 按最終用戶行業分類

- 包裝

- 汽車和運輸業

- 建築/施工

- 消費品/電子設備

- 醫療保健

- 航太/國防

- 能源、船舶、工業

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 東南亞國協

- 其他亞太國家

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐國家

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲國家

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- 3M

- ALTANA(BYK Additives)

- Amcol corporation

- Elementis PLC

- Globela Pharma

- HTMC Group

- Imerys

- Ionic Mineral Technologies

- KPL International Limited

- KUNIMINE INDUSTRIES CO., LTD.

- Laviosa SpA

- Minerals Technologies Inc

- Mitsubishi Chemical Corporation

- Pipelinepharma

- RT Vanderbilt Holding Company, Inc.

- Reade

- RTP Company

- Sika AG

- Techmer PM

第7章 市場機會與未來展望

According to Mordor Intelligence, the nanoclay reinforcement market size was valued at USD 4.73 billion in 2025 and is estimated to grow from USD 5.13 billion in 2026 to reach USD 7.67 billion by 2031, at a CAGR of 8.38% during the forecast period (2026-2031).

This report is Segmented by Type (Montmorillonite, Kaolinite, Smectite, Halloysite, Illite, and Hectorite), Form (Powder, Masterbatch, and Dispersion), Matrix (Thermoplastics, Thermosets, Elastomers, Biopolymers, and Others), End-User (Packaging, Automotive, Construction, Electronics, Healthcare, and More), and Geography (Asia-Pacific, North America, and More). Market Forecasts in Value (USD).

Global Nanoclay Reinforcement Market Trends and Insights

Rapid Demand for High-Performance and Lightweight Composites

Aerospace original-equipment makers are now choosing montmorillonite-reinforced epoxy prepregs for secondary structures. This weight-reduction choice leads to significant lifetime fuel savings per aircraft. In the automotive sector, tier-1 suppliers are applying the same rationale to battery housings. In this application, nanoclay-modified polyamide 6 not only reduces flame-spread rates to below a critical threshold but also decreases the enclosure's mass. Wind-turbine blade manufacturers are adopting hectorite-based thixotropes, which cut down on scrap and speed up cure cycles, thereby shortening project lead times. These advancements make it costlier for customers to switch suppliers. Each application demands unique surface-modification recipes tailored to its resin, granting established vendors protection against commodity price swings. As a result, the nanoclay reinforcement market is witnessing a surge in new orders, even as crude-oil-linked polymer prices see a downturn.

Growing Nanocomposite Use in Automotive and Aerospace

Battery packs, cabin air-management components, and nacelle panels are increasingly leveraging a synergy of nanoclay and phosphorus. This combination achieves elevated limiting-oxygen-index values with minimal loading. Carbon-fiber manufacturers are now providing tows pre-treated with organoclay, which streamlines the process for prepreggers and ensures consistent quality across batches. In the aerospace sector, bismaleimide systems, now enhanced with platelet clays, have seen a reduction in moisture absorption. This advancement extends inspection intervals. Collectively, these advancements not only maintain a high demand for compounders but also highlight a significant shift - the market is moving from sporadic to systematic integration of nanoclay reinforcement products.

High Processing Cost and Dispersion Complexity

Processors frequently opt for twin-screw extruders with tailored configurations to ensure consistent exfoliation. Yet, inadequate dispersion can create sizable agglomerates, diminishing tensile strength and elevating scrap rates in industries aiming for perfection. Although a nanoclay-infused masterbatch can remedy this challenge, it commands a higher price than the standard organoclay powder. Moreover, while proprietary surfactant packages simplify mixing, they also tether processors to exclusive contracts, limiting competitive bidding. These factors have hindered the expansion of the nanoclay reinforcement market, especially for smaller compounders.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory Push for Barrier-Enhanced Sustainable Packaging

- Cost-Effective Intercalation and Exfoliation Breakthroughs

- EHS and Regulatory Uncertainty for Food-Contact Nanoclays

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, montmorillonite dominated the nanoclay reinforcement market with a commanding 40.21% share, primarily supporting the mass-market automotive and packaging sectors. Meanwhile, halloysite, although holding a smaller share, experienced significant growth with an 8.77% CAGR during the forecast period of 2026-2031. This growth is attributed to halloysite's advantageous aspect ratio of 10:1 to 30:1, enabling a drug payload of 10 to 15 percent, which significantly outperforms platelet clays.

Wyoming's bentonite and Turkish hectorite mines ensure a steady supply of montmorillonite, reinforcing its dominance in the bulk market. In contrast, hospitals allocate significantly higher budgets for pharmaceutical-grade halloysite coatings, which provide a gradual release of silver ions over weeks, establishing a premium niche in the nanoclay reinforcement market.

In 2025, powder held a dominant 47.48% share of the nanoclay reinforcement market. Meanwhile, revenues from masterbatches have been climbing at a CAGR of 8.92% during the forecast period of 2026-2031. This growth is primarily driven by the processors' preference for ready dispersions, steering away from conventional twin-screw capital investments.

RTP's organoclay masterbatch, when applied at a precise let-down ratio, significantly bolsters oxygen barriers in polyethylene films. This advancement not only optimizes operations by minimizing changeover durations but also highlights the superior efficiency of RTP's product. Although dispersion and solution formats face challenges, mainly due to the elevated costs tied to solvent handling, they play pivotal roles in spray-applied coatings, particularly in scenarios with limited equipment shear.

Geography Analysis

In 2025, the Asia-Pacific region dominated the revenue landscape with a commanding 37.04% share and a robust growth trajectory, boasting a 9.18% CAGR during the forecast period of 2026-2031. China led the charge, rolling out millions of electric vehicles, each outfitted with GB 38031-2020 compliant nanoclay composite battery packs. In India, the food-safety agency's tightening of migration limits catalyzed growth, resulting in a significant uptick in the use of platelet clays for flexible packaging. Japan ramped up halloysite processing to produce high-purity medical grades, while South Korean battery manufacturers, leveraging polyamide housings with precise loading, achieved impressive weight reductions.

North America, with Wyoming as a pivotal player, secured a substantial market share. Wyoming's annual supply of millions of tons of bentonite ensured a steady feedstock for domestic compounders. Aerospace leaders, aligning with NASA's fuel efficiency goals, integrated nanoclay prepregs into nacelles. In 2025, Mexico's auto hubs, benefiting from nearshoring, experienced a surge in demand for under-hood parts.

Europe, despite navigating delays from EFSA, carved out a significant market share and experienced steady growth. In 2024, German OEMs rolled out UL 94 V-0 nanoclay polyamide enclosures across their platforms. French innovations, harnessing platelet-barrier bottles, achieved a remarkable extension of wine shelf life. Spain's adoption of nanoclay mulches led to a significant drop in herbicide run-off. While the United Kingdom's trials with fiber-cement cladding were modest, they gained prominence in the wake of post-Grenfell safety regulations.

South America, alongside the Middle-East and Africa, held a smaller slice of the market. Brazilian petrochemical liners and Saudi sealants ensured steady volumes, while South Africa's mining slurry lines enjoyed a marked reduction in abrasion. Despite their modest market share, these regions consistently met order demands, contributing to the overarching growth of the nanoclay reinforcement market during the forecast period of 2026-2031.

- 3M

- ALTANA (BYK Additives)

- Amcol corporation

- Elementis PLC

- Globela Pharma

- HTMC Group

- Imerys

- Ionic Mineral Technologies

- KPL International Limited

- KUNIMINE INDUSTRIES CO., LTD.

- Laviosa S.p.A.

- Minerals Technologies Inc

- Mitsubishi Chemical Corporation

- Pipelinepharma

- R.T. Vanderbilt Holding Company, Inc.

- Reade

- RTP Company

- Sika AG

- Techmer PM

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid demand for high-performance and lightweight composites

- 4.2.2 Growing nanocomposite use in automotive and aerospace

- 4.2.3 Regulatory push for barrier-enhanced sustainable packaging

- 4.2.4 Cost-effective intercalation and exfoliation breakthroughs

- 4.2.5 EV battery enclosures needing flame-resistant composites

- 4.3 Market Restraints

- 4.3.1 High processing cost and dispersion complexity

- 4.3.2 EHS/regulatory uncertainty for food-contact nanoclays

- 4.3.3 Competition from graphene, CNTs and other nano-additives

- 4.4 Value Chain Analysis

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Montmorillonite

- 5.1.2 Kaolinite

- 5.1.3 Smectite

- 5.1.4 Halloysite

- 5.1.5 Illite

- 5.1.6 Hectorite

- 5.2 By Form

- 5.2.1 Powder

- 5.2.2 Masterbatch

- 5.2.3 Dispersion/Solution

- 5.3 By Reinforcement Matrix

- 5.3.1 Thermoplastics

- 5.3.2 Thermosets

- 5.3.3 Elastomers

- 5.3.4 Biopolymers

- 5.3.5 Other Polymer Systems

- 5.4 By End-user Industry

- 5.4.1 Packaging

- 5.4.2 Automotive and Transportation

- 5.4.3 Building and Construction

- 5.4.4 Consumer Goods and Electronics

- 5.4.5 Healthcare and Medical

- 5.4.6 Aerospace and Defense

- 5.4.7 Energy, Marine and Industrial

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 ASEAN Countries

- 5.5.1.6 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Nordic Countries

- 5.5.3.8 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 3M

- 6.4.2 ALTANA (BYK Additives)

- 6.4.3 Amcol corporation

- 6.4.4 Elementis PLC

- 6.4.5 Globela Pharma

- 6.4.6 HTMC Group

- 6.4.7 Imerys

- 6.4.8 Ionic Mineral Technologies

- 6.4.9 KPL International Limited

- 6.4.10 KUNIMINE INDUSTRIES CO., LTD.

- 6.4.11 Laviosa S.p.A.

- 6.4.12 Minerals Technologies Inc

- 6.4.13 Mitsubishi Chemical Corporation

- 6.4.14 Pipelinepharma

- 6.4.15 R.T. Vanderbilt Holding Company, Inc.

- 6.4.16 Reade

- 6.4.17 RTP Company

- 6.4.18 Sika AG

- 6.4.19 Techmer PM

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

- 7.2 Opportunities in Fire-Retardant and Antimicrobial Nanocomposites

- 7.3 Rising use in Bio-polymer and Recyclable Packaging

石墨烯奈米複合材料市場-2026-2032年全球市場預測奈米黏土市場-2026-2032年全球市場預測奈米複合材料市場:2026-2032年全球市場預測(按類型、原料、製造技術和應用分類)奈米黏土增強材料市場:按類型、聚合物類型、形態、製程技術、粒徑範圍和應用分類-2026-2032年全球市場預測

石墨烯奈米複合材料市場-2026-2032年全球市場預測奈米黏土市場-2026-2032年全球市場預測奈米複合材料市場:2026-2032年全球市場預測(按類型、原料、製造技術和應用分類)奈米黏土增強材料市場:按類型、聚合物類型、形態、製程技術、粒徑範圍和應用分類-2026-2032年全球市場預測 奈米黏土市場規模、佔有率和成長分析:按類型、表面改質、應用、終端用戶產業、形態、分銷管道和地區分類-2026-2033年產業預測

奈米黏土市場規模、佔有率和成長分析:按類型、表面改質、應用、終端用戶產業、形態、分銷管道和地區分類-2026-2033年產業預測 聚合物基奈米複合材料市場:全球產業分析、市場規模、市佔率及2026年至2033年預測(依基體類型、應用、通路、聚合物、最終用戶、國家及地區分類)

聚合物基奈米複合材料市場:全球產業分析、市場規模、市佔率及2026年至2033年預測(依基體類型、應用、通路、聚合物、最終用戶、國家及地區分類) 工程奈米複合材料市場預測至2034年-按基體類型、奈米填料類型、應用、製造流程、最終用戶和地區分類的全球分析

工程奈米複合材料市場預測至2034年-按基體類型、奈米填料類型、應用、製造流程、最終用戶和地區分類的全球分析 奈米黏土市場商業機會、成長要素、產業趨勢分析及2026-2035年預測功能性奈米複合材料市場預測至2034年-按基體類型、奈米填料類型、功能、製造流程、應用和地區分類的全球分析全球先進材料市場(衝擊緩解)預測至2034年:依材料類型、機制、技術、最終用戶和地區分類

奈米黏土市場商業機會、成長要素、產業趨勢分析及2026-2035年預測功能性奈米複合材料市場預測至2034年-按基體類型、奈米填料類型、功能、製造流程、應用和地區分類的全球分析全球先進材料市場(衝擊緩解)預測至2034年:依材料類型、機制、技術、最終用戶和地區分類