|

市場調查報告書

商品編碼

2027615

奈米黏土市場商業機會、成長要素、產業趨勢分析及2026-2035年預測Nanoclays Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

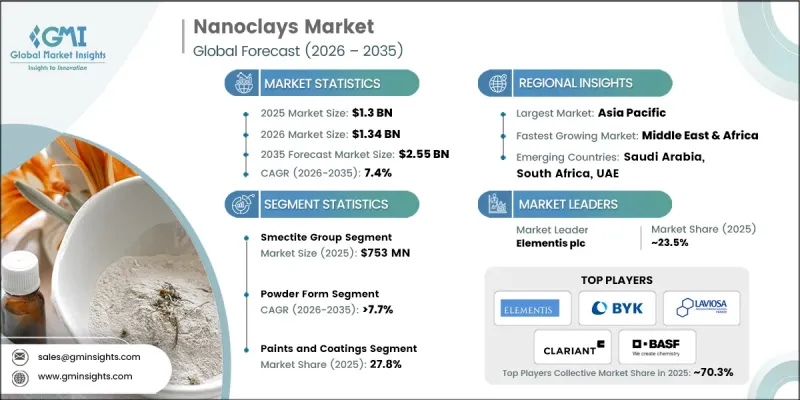

全球奈米黏土市場預計到 2025 年將價值 13 億美元,預計到 2035 年將以 7.4% 的複合年成長率成長至 25.5 億美元。

這一成長主要得益於聚合物產品、包裝解決方案、汽車零件、建築材料和工業塗料等領域對高性能材料日益成長的需求。奈米黏土因其即使在低濃度下也能提高機械強度、熱穩定性、阻燃性和阻隔性能,正被越來越多的製造商所採用。聚合物奈米複合材料和輕量材料材料配方因其成本效益和與傳統加工方法的兼容性而備受歡迎。奈米黏土能夠改善包裝材料的氣體和水分阻隔性,使汽車在不影響結構強度的前提下實現輕量化,並延長建築材料的耐久性和使用壽命。新興的高純度和改性等級奈米黏土正吸引著醫療、電子和特殊塗料領域的關注,而可擴展性、性能導向的選擇和先進的配方技術則推動著市場的穩步擴張。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 13億美元 |

| 預測金額 | 25.5億美元 |

| 複合年成長率 | 7.4% |

2025年,蒙脫石市場價值達7.53億美元,預計2026年至2035年將以7.5%的複合年成長率成長。其受歡迎的原因在於其用途廣泛、與聚合物具有良好的相容性以及優異的阻隔性和機械性能。高嶺石奈米黏土的需求穩定,尤其是在建築和塗料領域,因其成本敏感和熱穩定性要求高,而備受青睞。埃洛石因其獨特的管狀結構和功能適應性,在特種和高階應用中的使用日益增多。海泡石和坡縷石等小眾奈米黏土則用於流變改質和特殊複合材料,促進了市場的多元化發展,而非大規模生產。

預計到2025年,塗料產業市場規模將達到3.37億美元,市佔率為27.8%,並有望在2026年至2035年間以7.4%的複合年成長率成長。奈米黏土因其能夠提高耐久性、阻隔性和流變控制能力,在該行業中得到廣泛應用。在包裝和汽車行業,奈米粘土被用於提升材料性能和減輕重量;而在水處理、食品和飲料行業,奈米粘土則因其吸附和穩定特性而備受青睞。生物醫學應用正在推動創新,而其他細分應用則為市場成長和多元化發展做出了貢獻。

預計到2025年,北美奈米黏土市場規模將達到2.56億美元。這一成長主要得益於先進材料的研發、對輕量耐用產品的需求,以及聚合物奈米複合材料在汽車、包裝和塗料行業的廣泛應用。加拿大專注於長效建築材料和環保工業塗料,也為市場做出了貢獻,從而推動了區域市場的成長。

目錄

第1章:調查方法

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 產業潛在風險與挑戰

- 市場機遇

- 成長潛力分析

- 監理情勢

- 波特五力分析

- PESTEL 分析

- 價格趨勢

- 按地區

- 依產品

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 專利趨勢

- 貿易統計

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續計劃

- 減少廢棄物策略

- 生產中的能源效率

- 環保意識的舉措

- 關於碳足跡的考量

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估算與預測:依產品類型分類,2022-2035年

- 蒙脫石族

- 高嶺石族

- 埃洛石

- 其他(海泡石、坡縷石)

第6章 市場估計與預測:依類型分類,2022-2035年

- 粉狀

- 母粒/預分散體

- 凝膠/懸浮液

第7章 市場估計與預測:依應用領域分類,2022-2035年

- 水處理

- 食品/飲料包裝

- 車

- 生物醫學

- 油漆和塗料

- 其他

第8章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 其他中東和非洲地區

第9章:公司簡介

- Elementis plc

- BYK-Chemie(ALTANA)

- Laviosa Chimica Mineraria

- Tolsa Group

- BASF SE

- Evonik Industries

- Clariant AG

- Mineral Technologies

- FCC Inc.

- Nanografi

- Nanoshel

The Global Nanoclays Market was valued at USD 1.3 billion in 2025 and is estimated to grow at a CAGR of 7.4% to reach USD 2.55 billion by 2035.

The growth is fueled by rising demand for materials with superior performance in polymer products, packaging solutions, automotive components, construction materials, and industrial coatings. Manufacturers are increasingly relying on nanoclays because they enhance mechanical strength, thermal stability, flame resistance, and barrier performance even at low concentrations. Polymer nanocomposites and lightweight material formulations remain popular due to cost efficiency and compatibility with traditional processing methods. Nanoclays provide packaging with improved gas and moisture barriers, enable lightweight automotive designs without compromising structural strength, and enhance the durability and lifespan of construction materials. Emerging high-purity and modified grades are gaining traction in healthcare, electronics, and specialty coatings, while scalability, performance-oriented selection, and advanced formulations are supporting steady market expansion.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.3 Billion |

| Forecast Value | $2.55 Billion |

| CAGR | 7.4% |

The smectite group segment was valued at USD 753 million in 2025 and is expected to grow at a CAGR of 7.5% from 2026 to 2035. Its popularity stems from versatility, strong polymer compatibility, and superior barrier and mechanical enhancements. Kaolinite group nanoclays maintain steady demand for cost-sensitive and thermally stable applications, especially in construction and coatings. Halloysite is increasingly used in specialty and advanced applications due to its unique tubular structure and functional adaptability. Niche nanoclays such as sepiolite and palygorskite are used for rheology modification and specialty composites, contributing to market variety rather than bulk volume.

The paints and coatings segment was valued at USD 337 million in 2025, holding a 27.8% share, and is expected to grow at a CAGR of 7.4% during 2026-2035. Nanoclays are widely adopted in this sector for durability, barrier improvement, and rheological control. Packaging and automotive industries utilize them for material enhancement and lightweighting, while water treatment, food, and beverage sectors rely on adsorption and stabilization properties. Biomedical applications drive innovation, whereas other niche uses contribute incremental growth, promoting overall market diversification.

North America Nanoclays Market accounted for USD 256 million in 2025, driven by advanced material R&D, demand for lightweight yet durable products, and adoption of polymer nanocomposites in automotive, packaging, and coatings. Canada contributes through its focus on long-lasting construction materials and environmentally sustainable industrial coatings, strengthening regional market development.

Key players operating in the Nanoclays Market include Elementis plc, BYK-Chemie (ALTANA), Laviosa Chimica Mineraria, Tolsa Group, BASF SE, Evonik Industries, Clariant AG, Mineral Technologies, FCC Inc., Nanografi, Nanoshel, and others. Companies in the Nanoclays Market strengthen their position through multiple strategies. They focus on expanding R&D capabilities to develop high-performance and application-specific nanoclays. Strategic partnerships, mergers, and acquisitions help increase global reach and product portfolio diversity. Investment in production capacity and adoption of advanced processing technologies ensure a scalable and cost-efficient supply. Firms prioritize developing modified and high-purity grades to address niche markets such as healthcare, electronics, and specialty coatings. Market leaders also enhance their presence through sustainable manufacturing practices, regulatory compliance, and technical support services for end-users, which build long-term customer trust and loyalty.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product Type

- 2.2.3 Form

- 2.2.4 Application

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and Environmental Aspects

- 3.12.1 Sustainable Practices

- 3.12.2 Waste Reduction Strategies

- 3.12.3 Energy Efficiency in Production

- 3.12.4 Eco-friendly Initiatives

- 3.13 Carbon Footprint Considerations

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022- 2035 (USD Billion, Kilo Tons)

- 5.1 Key trends

- 5.2 Smectite Group

- 5.3 Kaolinite Group

- 5.4 Halloysite

- 5.5 Others (sepiolite, palygorskite)

Chapter 6 Market Estimates and Forecast, By Form, 2022 - 2035 (USD Billion, Kilo Tons)

- 6.1 Key trends

- 6.2 Powder Form

- 6.3 Masterbatch/Pre-dispersed

- 6.4 Gel/Suspension

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Billion, Kilo Tons)

- 7.1 Key trends

- 7.2 Water Treatment

- 7.3 Food and Beverage Packaging

- 7.4 Automotive

- 7.5 Biomedical

- 7.6 Paints and Coatings

- 7.7 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion, Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East & Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East & Africa

Chapter 9 Company Profiles

- 9.1 Elementis plc

- 9.2 BYK-Chemie (ALTANA)

- 9.3 Laviosa Chimica Mineraria

- 9.4 Tolsa Group

- 9.5 BASF SE

- 9.6 Evonik Industries

- 9.7 Clariant AG

- 9.8 Mineral Technologies

- 9.9 FCC Inc.

- 9.10 Nanografi

- 9.11 Nanoshel

石墨烯奈米複合材料市場-2026-2032年全球市場預測奈米黏土市場-2026-2032年全球市場預測奈米複合材料市場:2026-2032年全球市場預測(按類型、原料、製造技術和應用分類)奈米黏土增強材料市場:按類型、聚合物類型、形態、製程技術、粒徑範圍和應用分類-2026-2032年全球市場預測

石墨烯奈米複合材料市場-2026-2032年全球市場預測奈米黏土市場-2026-2032年全球市場預測奈米複合材料市場:2026-2032年全球市場預測(按類型、原料、製造技術和應用分類)奈米黏土增強材料市場:按類型、聚合物類型、形態、製程技術、粒徑範圍和應用分類-2026-2032年全球市場預測 奈米黏土市場規模、佔有率和成長分析:按類型、表面改質、應用、終端用戶產業、形態、分銷管道和地區分類-2026-2033年產業預測

奈米黏土市場規模、佔有率和成長分析:按類型、表面改質、應用、終端用戶產業、形態、分銷管道和地區分類-2026-2033年產業預測 聚合物基奈米複合材料市場:全球產業分析、市場規模、市佔率及2026年至2033年預測(依基體類型、應用、通路、聚合物、最終用戶、國家及地區分類)

聚合物基奈米複合材料市場:全球產業分析、市場規模、市佔率及2026年至2033年預測(依基體類型、應用、通路、聚合物、最終用戶、國家及地區分類) 工程奈米複合材料市場預測至2034年-按基體類型、奈米填料類型、應用、製造流程、最終用戶和地區分類的全球分析

工程奈米複合材料市場預測至2034年-按基體類型、奈米填料類型、應用、製造流程、最終用戶和地區分類的全球分析 奈米黏土增強材料:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)功能性奈米複合材料市場預測至2034年-按基體類型、奈米填料類型、功能、製造流程、應用和地區分類的全球分析全球先進材料市場(衝擊緩解)預測至2034年:依材料類型、機制、技術、最終用戶和地區分類

奈米黏土增強材料:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)功能性奈米複合材料市場預測至2034年-按基體類型、奈米填料類型、功能、製造流程、應用和地區分類的全球分析全球先進材料市場(衝擊緩解)預測至2034年:依材料類型、機制、技術、最終用戶和地區分類