|

市場調查報告書

商品編碼

2062394

膜接觸器:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Membrane Contactor - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

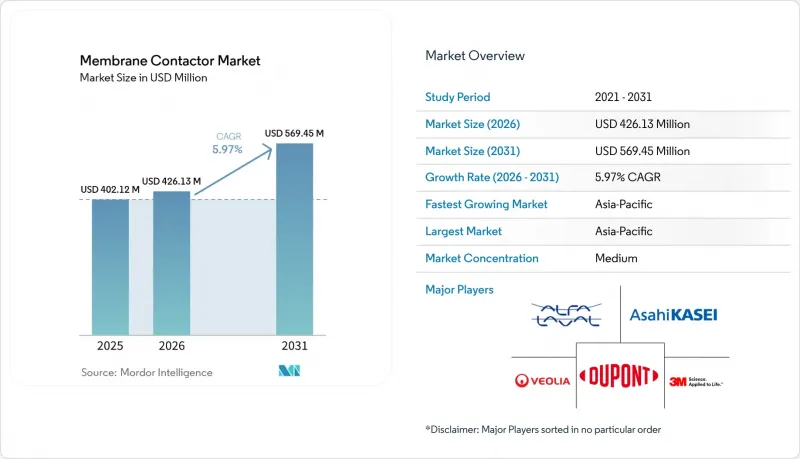

根據 Mordor Intelligence 預測,膜接觸器市場規模將從 2025 年的 4.0212 億美元成長到 2026 年的 4.2613 億美元,到 2031 年將達到 5.6945 億美元,2026 年至 2031 年的複合成長率預計為 5.97%。

本報告按膜材料(聚丙烯、聚四氟乙烯及其他)、組件結構(中空纖維及其他)、應用領域(水和廢水處理及其他)、終端用戶(工業、食品飲料及其他)以及地區(亞太、北美、歐洲、南美、中東和非洲)進行細分。市場預測以美元計價。

全球膜接觸器市場趨勢與洞察

水和飲料加工中對高效脫氣的需求

緊湊型膜組件現已成為軟性飲料、啤酒釀造和瓶裝水生產線的標準配置,能夠有效降低溶氧量至最低,同時不影響揮發性風味成分。值得一提的是,北美一家大型瓶裝水生產商已從傳統的真空脫氣系統過渡到Liqui-Cel裝置,透過提高產量和大幅降低能耗,顯著節省了成本。啤酒廠目前正在升級到佔用空間極小的模組化系統,確保製程連續運行,同時避免土木工程。在歐洲,飲料廠透過將高溫水滅菌與靈活的CIP(就地清洗)循環相結合來改進製程。這不僅顯著延長了膜的運作,而且透過抑制啤酒中的氧化劣化和防止軟性飲料中的維生素分解,延長了產品的保存期限。

製藥和生物技術領域超純水設施簡介

繼歐洲藥典核准非蒸餾注射用水後,膜分離注射劑目前已佔據相當大的裝置容量容量佔有率。在INCOG BioPharma位於印第安納州的填充和精製工廠(專為大規模生產而設計),膜接觸器可去除殘留的二氧化碳和氧氣,從而將電導率維持在嚴格的標準範圍內。基因泰克位於霍利斯普林斯的工廠和諾和諾德位於北卡羅來納州的工廠都致力於實現生物製藥中極低的氧濃度。這種高水平的控制是透過使用可承受反覆氧化劑清洗的聚聚二氟亞乙烯中空纖維來實現的。尤其值得一提的是,與多級蒸餾相比,這些方法可顯著節省能源,並與淨零排放藍圖完美契合。

高昂的資本投資和營運/維護成本

在處理流量相近的情況下,膜接觸器所需的初始投資遠高於真空塔。薄膜接觸器組件的成本也遠高於真空塔。此外,膜接觸器需要定期更換和化學清洗,從而增加了長期的營運成本。雖然節能面積帶來的經濟效益能夠轉化為實際收益,但南亞預算緊張的市政當局往往優先選擇技術含量較低的系統,並推遲升級改造。

細分市場分析

在全球膜接觸器市場,預計2025年,聚丙烯將佔據42.03%的膜材料佔有率。同時,聚偏二氟乙烯(PVDF)憑藉其優異的pH 1-10耐受性和高達175°C的耐溫性能,預計將在2026年至2031年間以6.26%的複合年成長率成長。聚二氟亞乙烯(PVDF)組件廣泛應用於需要頻繁氧化的製藥氨汽提和沼氣裝置。另一方面,聚四氟乙烯(PTFE)在半導體超純水處理領域的應用有限,這主要是由於其對品管的嚴格要求,尤其是在氦氣方面。旭化成創新的雙層聚二氟亞乙烯纖維不僅降低了洩漏風險,還具備交叉流固態截留能力,從而在單一製程中實現了純化和濃縮的雙重最佳化。

儘管利用生物基膜的商業性計畫正在進行中,但仍處於試驗階段。這主要是因為替代材料尚未達到聚偏聚二氟亞乙烯)成熟的疏水性和拉伸強度。然而,隨著對含氟聚合物監管力度的加強,合作研發活動正在顯著增加。膜生產商和化學回收商之間的這些合作旨在開發無溶劑生產方法並建立閉合迴路回收系統。

預計2025年,中空纖維膜組件在全球膜接觸器市場將佔56.33%的市場。這主要得益於其高比表面積(超過1000 m²/m³)和強大的反沖洗能力。螺旋卷式膜組件預計在2026年至2031年間將以6.38%的複合年成長率成長。由於其纖薄的外殼設計便於對機架式系統維修,溶劑脫水技術經濟研究表明,與中空纖維膜相比,螺旋捲式滲透汽化膜具有更高的傳質效率和更低的能耗。此外,濱特爾公司的Helix湍流增強器顯著維修了通量,使螺旋系統成為改造滲濾液和工業污水系統的理想選擇。同時,在實驗室篩檢和專用血氧儀等需要快速更換膜組件而非高填充密度的應用中,平板膜組件仍是首選。

區域分析

預計到2025年,亞太地區將佔杜邦總銷售額的40.28%,並在2026年至2031年間以6.56%的複合年成長率成長,這主要得益於中國「零液體排放(ZLD)」計劃的需求以及半導體行業的擴張。杜邦收購中化RO Memtech標誌著其組件在地化生產策略的推進,這將有助於降低進口關稅和物流排放。在日本,主要薄膜製造商通過完善的品質系統認證,向當地的製藥和顯示面板製造企業供應聚二氟亞乙烯纖維。

在北美,生物製藥、先進電池和半導體製造設施的擴張正推動對高純度水的需求激增。基因泰克和諾和諾德的計畫透過利用多個接觸器組,顯著提高了注射用水的產能。威立雅與美國中西部一家半導體製造廠簽訂的大規模合約凸顯了用水密集型產業回流的趨勢。同時,美國環保署 (EPA) 對硝酸鹽法規的修訂收緊了廢水標準,促使氨回收系統得到更廣泛的應用。

歐洲在碳捕獲和生物甲烷領域繼續發揮主導作用。 2024年至2025年間,運作中的捕碳封存(CCS)設施數量顯著增加。在英國,HyNet和東海岸叢集正在為膜碳轉移裝置的長期市場發展鋪平道路。在西班牙,第1085/2024號皇家法令正在加速PURON膜生物反應器的維修,將生物處理和膜脫氣結合,以滿足灌溉回用標準。

南美洲與中東和非洲一道,正崛起為新的前沿市場。膜組件正被應用於硫酸鹽和氨的治理,例如巴西石油公司(Petrobras)的浮體式生產儲裝運裝置(FPSO)專案和沙烏地阿拉伯的工業污水回用計劃。然而,價格敏感性和服務基礎設施的匱乏等挑戰阻礙了薄膜技術的快速發展。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 水和飲料加工中對高效脫氣的需求

- 製藥和生物技術領域超純水設施簡介

- 用於工業維修的緊湊型模組化氣體輸送系統

- 更嚴格的氮排放法規將加速氨的去除。

- 擴大低溫生物甲烷液化預處理規模

- 市場限制因素

- 高昂的資本成本和營運維護成本

- 高有機物含量流體中的液膜潤濕性/結垢

- 氦氣短缺導致專用模組成本上漲。

- 價值鏈分析

- 波特五力模型

第5章 市場規模與成長預測

- 透過電影材料

- 聚丙烯(PP)

- 聚四氟乙烯(PTFE)

- 聚二氟亞乙烯(PVDF)

- 其他

- 透過模組配置

- 中空纖維

- 平板

- 螺旋纏繞

- 透過使用

- 用水和污水處理

- 製藥和生物技術

- 食品/飲料加工

- 化學處理

- 發電

- 碳捕獲和氣體轉移

- 其他用途

- 按最終用戶行業分類

- 產業

- 衛生保健

- 食品/飲料

- 電力和能源

- 其他行業

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 東南亞國協

- 其他亞太國家

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐國家

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲國家

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- 3M(Liqui-Cel/Membrana)

- Alfa Laval

- Aquatech

- Asahi Kasei Corporation

- CITIC Limited

- DuPont

- EUROWATER

- Fluence Corporation Limited

- GEA Group Aktiengesellschaft

- Kovalus Separation Solutions

- LG Chem, Ltd.

- Linde PLC

- Masterfilter GmbH

- Mitsubishi Chemical Corporation

- Ovivo Water Inc.

- PARKER HANNIFIN CORP

- Pentair

- PermSelect-Silicone Gas Exchange Membranes

- SUEZ

- Synder Filtration, Inc.

- Theway Membranes

- TOYOBO CO., LTD.

- Veolia Water Technologies, Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the membrane contactor market size is expected to increase from USD 402.12 million in 2025 to USD 426.13 million in 2026 and reach USD 569.45 million by 2031, growing at a CAGR of 5.97% over 2026-2031.

This report is Segmented by Membrane Material (Polypropylene, Polytetrafluoroethylene, and Others), Module Configuration (Hollow-Fiber, and More), Application (Water and Wastewater Treatment, and More), End-User (Industrial, Food and Beverage, and More), and Geography (Asia Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Membrane Contactor Market Trends and Insights

Efficient Degassing Demand in Water and Beverage Processing

Compact membrane skids are now a staple in soft-drink, brewing, and packaged-water lines, effectively reducing dissolved oxygen levels to minimal levels without compromising volatile flavor compounds. In a notable shift, a major North American bottler transitioned from traditional vacuum deaerators to a Liqui-Cel unit, achieving significant cost savings through enhanced yield gains and a substantial reduction in energy consumption. Breweries are now retrofitting modules that occupy minimal space, sidestepping civil works and ensuring continuous process uptime. In Europe, beverage plants are enhancing their processes by integrating high-temperature water sterilization with adaptable clean-in-place cycles. This not only extends the membrane life significantly but also boosts product shelf life by curbing oxidative staling in beer and preventing vitamin degradation in soft drinks.

Adoption in Pharma and Biotech Ultrapure Utilities

Following the European Pharmacopeia's endorsement of non-distillation water for injection, membrane-based water for injection has captured a significant share of the installed capacity. At INCOG BioPharma's Indiana fill-finish site, designed for large-scale production, membrane contactors ensure residual carbon dioxide and oxygen are polished, maintaining conductivity within stringent limits. Both Genentech's facility in Holly Springs and Novo Nordisk's site in North Carolina aim for extremely low oxygen levels in their biologic formulations. This precision is achieved using polyvinylidene fluoride hollow fibers, which can endure repeated oxidant cleaning. Notably, these methods offer substantial energy savings compared to multi-effect distillation, aligning seamlessly with net-zero roadmaps.

High Capital and Operations and Maintenance Costs

Membrane contactors involve significantly higher capital expenditures compared to vacuum towers for similar flow rates. The cost of modules for membrane contactors is substantially greater than that of vacuum towers. Furthermore, membrane contactors require periodic replacement and regular chemical cleanings, leading to additional operational expenses over time. Economics improve where operators monetize energy or footprint savings, yet budget-constrained municipalities in South Asia often defer upgrades in favor of low-tech systems.

Other drivers and restraints analyzed in the detailed report include:

- Compact Modular Gas-Transfer Systems for Industrial Retrofit

- Stricter Nitrogen-Discharge Rules Spurring Ammonia Stripping

- Membrane Wetting/Fouling in High-Organic Streams

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The Global membrane contactor market size for membrane materials showed polypropylene at 42.03% in 2025, while PVDF's superior resistance under pH 1-10 and 175 °C drives a 6.26% CAGR over 2026-2031. Pharmaceutical ammonia-stripping and biogas installations, which require frequent oxidant sanitization, rely on polyvinylidene fluoride modules. While polytetrafluoroethylene finds limited application in semiconductor ultrapurification, it is primarily due to the premium quality control associated with helium. Asahi Kasei's innovative double-skin polyvinylidene fluoride fibers not only reduce leakage risks but also incorporate cross-flow solids retention, streamlining both purification and concentration in a single pass.

While commercial initiatives are exploring membranes made from biological sources, they remain in the pilot phase. This is largely because alternatives have yet to match polyvinylidene fluoride's renowned hydrophobicity and tensile strength. However, as regulatory bodies intensify scrutiny on fluorinated polymers, there is a noticeable increase in collaborative research and development. This partnership between membrane manufacturers and chemical recyclers aims to pioneer solvent-free production methods and establish closed-loop take-back systems.

The 2025 Global membrane contactor market share for hollow-fiber modules reached 56.33%, reflecting high surface area (>1,000 m2/m3) and backwash capability. Spiral-wound units are forecast for a 6.38% CAGR over 2026-2031. Thanks to slimmer housings designed for rack-mount retrofits, spiral-wound pervaporation membranes have been shown, in techno-economic studies on solvent dehydration, to significantly enhance mass transfer and reduce energy consumption compared to hollow fibers. Additionally, Pentair's Helix turbulence promoters contribute to notable increases in flux, making spiral systems ideal for leachate and industrial wastewater retrofits. Meanwhile, flat-sheet cassettes continue to be favored in laboratory screenings and specialized blood-oxygenation devices, where the speed of membrane changeouts takes precedence over packing density.

Geography Analysis

Asia-Pacific generated 40.28% of 2025 revenue and is projected to grow at 6.56% CAGR over 2026-2031 as China's push for zero-liquid-discharge and its semiconductor expansion are driving up demand. DuPont's acquisition of Sinochem RO Memtech showcases localized module manufacturing, cutting down on import duties and logistics emissions. In Japan, major membrane producers are supplying polyvinylidene fluoride fibers to local pharmaceutical and display-panel manufacturing facilities, bolstered by robust quality-system certifications.

In North America, the expansion of biopharmaceuticals, advanced batteries, and semiconductor manufacturing facilities is spurring a surge in high-purity water demand. Projects from Genentech and Novo Nordisk are significantly increasing water for injection capacity, utilizing multiple contactor banks. Veolia's substantial deal with a chip manufacturing facility in the Midwest underscores the trend of water-intensive reshoring. Meanwhile, revisions by the United States Environmental Protection Agency on nitrates are tightening effluent standards, leading to a rise in ammonia-recovery systems.

Europe continues to lead in carbon capture and biomethane initiatives. The number of operational carbon capture and storage sites has grown significantly from 2024 to 2025. In the United Kingdom, the HyNet and East Coast clusters are paving the way for long-term markets for membrane carbon dioxide transfer skids. In Spain, Royal Decree 1085/2024 has spurred PURON membrane bioreactor retrofits, combining biological treatment with membrane degassing to meet irrigation-reuse standards.

South America, along with the Middle East and Africa, is emerging as a new frontier. Petrobras's floating production storage and offloading projects and Saudi Arabia's industrial wastewater reuse initiatives are turning to membrane modules for managing sulfate and ammonia. However, challenges like price sensitivity and a lack of service infrastructure are moderating rapid expansion.

- 3M (Liqui-Cel / Membrana)

- Alfa Laval

- Aquatech

- Asahi Kasei Corporation

- CITIC Limited

- DuPont

- EUROWATER

- Fluence Corporation Limited

- GEA Group Aktiengesellschaft

- Kovalus Separation Solutions

- LG Chem, Ltd.

- Linde PLC

- Masterfilter GmbH

- Mitsubishi Chemical Corporation

- Ovivo Water Inc.

- PARKER HANNIFIN CORP

- Pentair

- PermSelect - Silicone Gas Exchange Membranes

- SUEZ

- Synder Filtration, Inc.

- Theway Membranes

- TOYOBO CO., LTD.

- Veolia Water Technologies, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Efficient degassing demand in water and beverage processing

- 4.2.2 Adoption in pharma and biotech ultrapure utilities

- 4.2.3 Compact modular gas-transfer systems for industrial retrofit

- 4.2.4 Stricter nitrogen-discharge rules spurring ammonia stripping

- 4.2.5 Scale-up for cryogenic biomethane liquefaction pre-treatment

- 4.3 Market Restraints

- 4.3.1 High capital and OandM costs

- 4.3.2 Membrane wetting / fouling in high-organic streams

- 4.3.3 Helium scarcity inflating specialty module costs

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Membrane Material

- 5.1.1 Polypropylene (PP)

- 5.1.2 Polytetrafluoroethylene (PTFE)

- 5.1.3 Polyvinylidene Fluoride (PVDF)

- 5.1.4 Others

- 5.2 By Module Configuration

- 5.2.1 Hollow-Fiber

- 5.2.2 Flat-Sheet

- 5.2.3 Spiral-Wound

- 5.3 By Application

- 5.3.1 Water and Wastewater Treatment

- 5.3.2 Pharmaceutical and Biotechnology

- 5.3.3 Food and Beverage Processing

- 5.3.4 Chemical Processing

- 5.3.5 Power Generation

- 5.3.6 Carbon Capture and Gas Transfer

- 5.3.7 Other Applications

- 5.4 By End-user Industry

- 5.4.1 Industrial

- 5.4.2 Healthcare

- 5.4.3 Food and Beverage

- 5.4.4 Power and Energy

- 5.4.5 Other Industries

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 ASEAN Countries

- 5.5.1.6 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Nordic Countries

- 5.5.3.8 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 3M (Liqui-Cel / Membrana)

- 6.4.2 Alfa Laval

- 6.4.3 Aquatech

- 6.4.4 Asahi Kasei Corporation

- 6.4.5 CITIC Limited

- 6.4.6 DuPont

- 6.4.7 EUROWATER

- 6.4.8 Fluence Corporation Limited

- 6.4.9 GEA Group Aktiengesellschaft

- 6.4.10 Kovalus Separation Solutions

- 6.4.11 LG Chem, Ltd.

- 6.4.12 Linde PLC

- 6.4.13 Masterfilter GmbH

- 6.4.14 Mitsubishi Chemical Corporation

- 6.4.15 Ovivo Water Inc.

- 6.4.16 PARKER HANNIFIN CORP

- 6.4.17 Pentair

- 6.4.18 PermSelect - Silicone Gas Exchange Membranes

- 6.4.19 SUEZ

- 6.4.20 Synder Filtration, Inc.

- 6.4.21 Theway Membranes

- 6.4.22 TOYOBO CO., LTD.

- 6.4.23 Veolia Water Technologies, Inc.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment