|

市場調查報告書

商品編碼

2043908

亞太地區單層膜:市場佔有率分析、產業趨勢和統計數據以及成長預測(2026-2031 年)Asia-Pacific Single-Ply Membrane - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

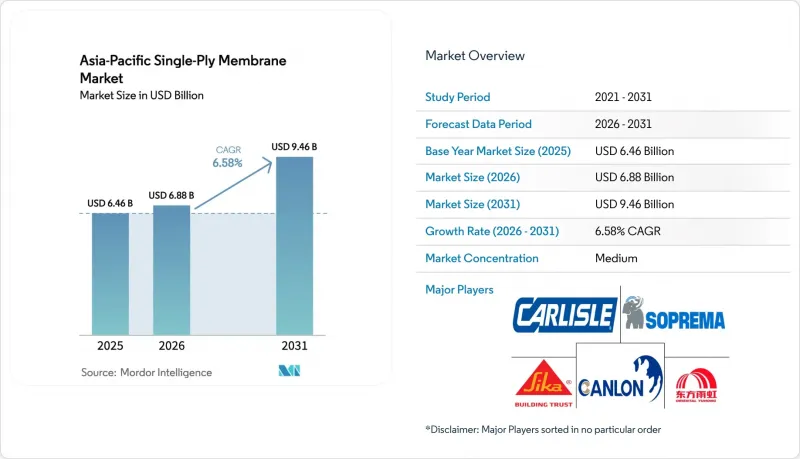

預計亞太地區單層膜市場規模將從 2025 年的 64.6 億美元和 2026 年的 68.8 億美元成長到 2031 年的 94.6 億美元,2026 年至 2031 年的年複合成長率(CAGR)為 6.58%。

中國、越南和印尼的基礎設施投資持續推動對橋樑、隧道和掩埋的需求。同時,印度和日本的淨零能耗建築標準正在加速推廣冷屋頂技術,相關支出正轉向採用白色熱塑性聚烯(TPO)和乙丙橡膠(EPDM)製成的屋頂材料。新加坡、孟買和雅加達的資料中心營運商擴大採用固化時間為四小時的薄膜結構系統,以最大限度地減少冷卻系統的停機時間。與火焰噴塗改質瀝青卷材相比,TPO熱焊接縫更能有效滿足這些要求。隨著模組化建築標準的擴展,工廠焊接產品的普及勢頭強勁。例如,香港的公共住宅模組化一體化建築(MiC)計劃和中國30%的預製構件強制令已將現場施工人員減少了30%,並將缺陷率降低到2%以下。然而,聚烯原物料價格的波動(預計2024年1月至2025年12月期間將上漲22%)正對毛利率構成壓力。儘管如此,西卡、東方裕宏和陶氏等公司的垂直整合策略正幫助這些市場領導緩解成本壓力,並保持相對於小規模擠出機的競爭優勢。

亞太地區單層膜市場趨勢及洞察

更嚴格的建築節能標準正在促進冷屋頂。

強制性冷屋頂標準已將能源效率目標轉化為強制性採購標準,從而推動了高反射率TPO和PVC膜材的普及。印度的「2024年建築能源效率標準」規定,九個氣候區的低坡度屋頂太陽反射率(SRI)必須達到78或更高,這實際上淘汰了清奈、海得拉巴和加爾各答等城市新計畫中的深色改性瀝青。日本修訂後的「建築能效法」將於2025年4月生效,該法規定了面積超過300平方公尺的非住宅建築必須採用被動式冷卻標準,這加速了東京和大阪辦公大樓採用EPDM膜材。在中國,GB 50189標準的修訂將綠色建築稅收優惠與反射性屋頂掛鉤,加速了深圳和廣州等城市採用TPO膜材。新加坡的「綠建築標誌2024」對老化後太陽反射率(SRI)達到63或以上的屋頂給予加分,這一標準與加州的「第24號法規」基準相一致。綜合來看,預計到2028年,這些法規將使亞太地區主要都會區非反射性屋頂材料的市場佔有率減少約18%至22%。

加速商業不動產屋頂更換週期

在日本、韓國和印度,隨著建築物老化,屋頂更換週期正從25-30年縮短至18-22年。這是因為業主優先考慮的是能源效率,而非延長建築物的使用壽命。預計到2025年,印度的商業維修市場規模將達到4.5兆印度盧比(約53億美元),其中45%的租賃物業將進行維修。儘管截至2024年10月,日本新屋開工量下降了7.1%,但日本開發人員仍在爭分奪秒地遵守將於2025年4月生效的能源效率法。在韓國,首爾和釜山的業主正利用2.5兆韓元(約19億美元)的低利率住宅維修貸款,並專注於反射性屋頂。在新加坡,為了維持「綠建築標誌白金級」認證,房東們正積極地提前八年更換A級物業(例如濱海灣金融中心)的屋頂。屋頂更換正從一種被動措施轉變為對環境、社會和管治(ESG) 因素的主動投資,在注重永續發展的市場中,租金上漲了 12-15%。

聚烯和塑化劑的價格波動

與原油價格相關的聚丙烯價格波動(2024年1月至2025年12月上漲22%)導致非整合TPO擠出機的毛利率下降3-5個百分點。此外,中國將四種鄰苯二甲酸酯類物質列入RoHS指令清單後,2025年第二季PVC薄膜生產用塑化劑成本上漲了18%。陶氏化學在張家港擴大其矽酮業務,旨在開發非鄰苯二甲酸酯替代品,但由於需要18-24個月的現場檢驗,其廣泛的商業性應用受到阻礙。越南和印尼的中小型製造商由於缺乏避險手段,將下游價格提高了12-15%,導致對成本敏感的基礎設施項目競標延期。這些市場動態正在加速垂直整合策略,例如西卡收購樹脂業務以及東方裕宏進軍瀝青精煉業務。這些努力有助於降低投入成本波動的風險,並鞏固我們在亞太地區單層膜市場的市場地位。

細分市場分析

截至2025年,改質瀝青在亞太單層防水卷材市場佔據32.38%的市場佔有率,而TPO預計到2031年將以8.41%的複合年成長率成長。根據中國「一帶一路」採購標準,基礎設施採購者仍然傾向於選擇火炬瀝青用於承受反覆凍融循環的橋樑。同時,資料中心客戶正在擴大熱熔焊接TPO的應用,以滿足接縫失效率低於0.5%和固化時間4小時的目標,這推動了新加坡、雅加達和孟買等地資料中心園區的部署。 EPDM的市佔率約為15%,由於其耐台風暴雨和閉孔結構,在東京的維修工程中備受青睞。 PVC的成長受到中國鄰苯二甲酸酯禁令的限制。然而,在禁止使用火焰的區域,新加坡的高層公寓開發商重視PVC的可焊接性。

預計2029年印度全面實施SRI標準時,改質瀝青在橋樑和隧道中的優勢將逐漸下降,降幅達4至6個百分點。在日本,由於節能維修措施的推廣,EPDM的市場佔有率正在不斷擴大;而PVC供應商則爭相在中國於2026年1月禁用鄰苯二甲酸酯類塑化劑之前,爭取獲得不含鄰苯二甲酸酯類塑化劑的認證。

亞太地區單層膜市場報告按類型(乙丙橡膠 (EPDM)、熱塑性聚烯(TPO)、聚氯乙烯(PVC)、改性瀝青等)、應用(住宅、商業、工業和公共以及基礎設施)和地區(印度、中國、日本、韓國、東南亞國協和其他亞太國家)對產業進行細分。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 更嚴格的建築節能法規正在推動冷屋頂的普及。

- 加速商業不動產屋頂更換週期

- 政府強制性的淨零排放政策正在提振對反光膜的需求。

- 模組化建築正在推動對工廠焊接輥的需求。

- 資料中心容量的激增對屋頂系統提出了更高的要求,即停機時間要盡可能短。

- 市場限制因素

- 聚烯和塑化劑的價格波動

- 對聚氯乙烯和鄰苯二甲酸酯的監管

- 亞太地區二線城市熟練承包商短缺

- 價值鏈分析

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章 市場規模與成長預測

- 按類型

- 改性瀝青

- 乙丙橡膠(EPDM)

- 熱塑性聚烯(TPO)

- 聚氯乙烯(PVC)

- 其他

- 透過使用

- 基礎設施(橋樑、隧道、掩埋陸)

- 住宅

- 商業的

- 工業和公共設施

- 依建築類型

- 新建工程

- 維修和整修

- 按地區

- 中國

- 印度

- 日本

- 韓國

- 印尼

- 越南

- 泰國

- 馬來西亞

- 亞太其他地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- BMI Group

- Carlisle Companies Inc.

- CKS Roofing

- Dow Inc.

- GAF Materials

- HB Fuller

- Holcim

- Hongyuan waterproof technology group co.,ltd

- Jiangsu Canlon Building Materials Co.,Ltd.

- Joaboa Technology

- Johns Manville

- Oriental Yuhong

- Polygomma

- Protan AS

- Renolit SE

- Sika AG

- Soprema Group

- Tremco Inc.

第7章 市場機會與未來展望

The Asia-Pacific Single-Ply Membrane Market size is projected to expand from USD 6.46 billion in 2025 and USD 6.88 billion in 2026 to USD 9.46 billion by 2031, registering a CAGR of 6.58% between 2026 to 2031.

Infrastructure investments in China, Vietnam, and Indonesia continue to drive demand for bridges, tunnels, and landfills. Meanwhile, net-zero building codes in India and Japan are accelerating the adoption of cool roofs, directing spending toward white thermoplastic polyolefin (TPO) and ethylene-propylene-diene monomer (EPDM) roofing materials. Data center operators in Singapore, Mumbai, and Jakarta are increasingly specifying membrane systems with four-hour cure windows to minimize cooling downtime. TPO's heat-welded seams meet these requirements more effectively than torch-applied modified bitumen sheets. The shift toward factory-welded products is gaining momentum as modular construction standards expand. For example, Hong Kong's public housing Modular Integrated Construction (MiC) program and China's 30% prefabrication mandate have reduced on-site labor by 30% and lowered defect rates to below 2%. However, a volatile polyolefin feedstock cycle, projected to increase by 22% between January 2024 and December 2025, is putting pressure on gross margins. Despite this, vertical integration strategies by companies such as Sika, Oriental Yuhong, and Dow are helping these market leaders mitigate cost pressures and maintain a competitive edge over smaller extruders.

Asia-Pacific Single-Ply Membrane Market Trends and Insights

Tightening Building-Energy Codes Driving Cool-Roof Adoption

Mandatory cool-roof thresholds are turning energy-efficiency objectives into enforceable procurement criteria, favoring high-albedo TPO and PVC membranes. India's Energy Conservation Building Code 2024 specifies an SRI >= 78 for low-slope roofs across nine climate zones, effectively excluding dark modified bitumen from new projects in cities such as Chennai, Hyderabad, and Kolkata. Japan's revised Building Energy Efficiency Act, effective April 2025, mandates non-residential buildings larger than 300 m2 to meet passive-cooling standards, driving EPDM upgrades in office buildings across Tokyo and Osaka. In China, the GB 50189 update links green-building tax incentives to reflective roofs, accelerating TPO adoption in cities like Shenzhen and Guangzhou. Singapore's Green Mark 2024 provides bonus points for roofs with an aged SRI >= 63, aligning its standards with California Title 24 benchmarks. Collectively, these regulations are projected to reduce the market share of non-reflective membranes by an estimated 18-22% in major Asia-Pacific metropolitan areas by 2028.

Accelerating Re-Roofing Cycle in Commercial Real Estate

Aging building inventories in Japan, South Korea, and India are shortening re-roofing cycles from 25-30 years to 18-22 years, as property owners prioritize energy savings over lifecycle extensions. India's commercial renovation market reached INR 45,000 crore (USD 5.3 billion) in 2025, with 45% of leases involving refurbished properties. Japanese developers have expedited retrofits to comply with the April 2025 efficiency law, despite a 7.1% decline in new construction starts as of October 2024. In South Korea, property owners in Seoul and Busan accessed KRW 2.5 trillion (USD 1.9 billion) in low-interest loans for housing upgrades, focusing on reflective roofs. In Singapore, landlords are proactively re-roofing Grade-A properties, such as the Marina Bay Financial Centre, up to eight years ahead of schedule to maintain Green Mark Platinum certifications. Re-roofing is transitioning from a reactive measure to a proactive environmental, social, and governance (ESG) investment, yielding rental increases of 12-15% in sustainability-focused markets.

Volatile Polyolefin and Plasticizer Prices

Crude oil-driven polypropylene price swings of 22% between January 2024 and December 2025 reduced the gross margins of non-integrated TPO extruders by 3-5 percentage points. Plasticizer costs for PVC membrane production increased by 18% in Q2 2025 following China's addition of four phthalates to its RoHS restricted list. Dow's silicone expansion in Zhangjiagang aims to address non-phthalate alternatives; however, the 18-24 months required for field validation delays broader commercial adoption. Smaller producers in Vietnam and Indonesia, lacking hedging mechanisms, implemented downstream price increases of 12-15%, leading to project delays in cost-sensitive infrastructure tenders. These market dynamics have accelerated vertical integration strategies, such as Sika's resin acquisition and Oriental Yuhong's entry into bitumen refining. These approaches help mitigate input cost volatility and strengthen market positions in the Asia-Pacific single-ply membrane segment.

Other drivers and restraints analyzed in the detailed report include:

- Government Net-Zero Mandates Boosting Reflective Membranes

- Modular Construction Boosting Demand for Factory-Welded Rolls

- PVC and Phthalate Regulatory Scrutiny

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Modified bitumen accounted for 32.38% of the Asia-Pacific single-ply membrane market share in 2025, while TPO is projected to grow at a CAGR of 8.41% through 2031. Infrastructure buyers continue to prefer torch-applied bitumen for freeze-thaw bridges under China's Belt and Road procurement standards. On the other hand, data-center clients increasingly adopt heat-welded TPO, which meets <= 0.5% seam-failure targets and four-hour cure windows, driving its adoption in Singapore, Jakarta, and Mumbai campuses. EPDM holds a mid-teens market share, favored by Tokyo renovators for its closed-cell resilience against typhoon-driven rain. PVC's growth is hindered by China's phthalate ban, although high-rise condo developers in Singapore value its weldability in areas where torch flames are prohibited.

Modified bitumen's dominance in bridges and tunnels is expected to decline gradually, with a 4-6 percentage point reduction by 2029 as India's SRI threshold is fully implemented. EPDM's market presence is strengthening due to Japan's stimulus for retrofit energy savings, while PVC suppliers are racing to qualify non-phthalate plasticizers ahead of China's January 2026 deadline.

The Asia-Pacific Single-Ply Membrane Market Report Segments the Industry Into by Type (Ethylene Propylene Diene Monomer (EPDM), Thermoplastic Polyolefin (TPO), Polyvinyl Chloride (PVC), Modified Bitumen, Other Types), by Application (Residential, Commercial, Industrial and Institutional, Infrastructure), and by Geography (India, China, Japan, South Korea, ASEAN Countries, Rest of Asia-Pacific).

List of Companies Covered in this Report:

- BMI Group

- Carlisle Companies Inc.

- CKS Roofing

- Dow Inc.

- GAF Materials

- H.B. Fuller

- Holcim

- Hongyuan waterproof technology group co.,ltd

- Jiangsu Canlon Building Materials Co.,Ltd.

- Joaboa Technology

- Johns Manville

- Oriental Yuhong

- Polygomma

- Protan AS

- Renolit SE

- Sika AG

- Soprema Group

- Tremco Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Tightening building-energy codes driving cool-roof adoption

- 4.2.2 Accelerating re-roofing cycle in commercial real-estate

- 4.2.3 Government net-zero mandates boosting reflective membranes

- 4.2.4 Modular construction boosting demand for factory-welded rolls

- 4.2.5 Data-centre capacity boom requiring low-downtime roof systems

- 4.3 Market Restraints

- 4.3.1 Volatile polyolefin and plasticizer prices

- 4.3.2 PVC and phthalate regulatory scrutiny

- 4.3.3 Skilled-installer shortage in Tier-2 Asia-Pacific cities

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Modified Bitumen

- 5.1.2 Ethylene Propylene Diene Monomer (EPDM)

- 5.1.3 Thermoplastic Polyolefin (TPO)

- 5.1.4 Polyvinyl Chloride (PVC)

- 5.1.5 Other Types

- 5.2 By Application

- 5.2.1 Infrastructure (Bridges, Tunnels, Landfills)

- 5.2.2 Residential

- 5.2.3 Commercial

- 5.2.4 Industrial and Institutional

- 5.3 By Construction Type

- 5.3.1 New Construction

- 5.3.2 Refurbished/Renovation

- 5.4 By Geography

- 5.4.1 China

- 5.4.2 India

- 5.4.3 Japan

- 5.4.4 South Korea

- 5.4.5 Indonesia

- 5.4.6 Vietnam

- 5.4.7 Thailand

- 5.4.8 Malaysia

- 5.4.9 Rest of Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 BMI Group

- 6.4.2 Carlisle Companies Inc.

- 6.4.3 CKS Roofing

- 6.4.4 Dow Inc.

- 6.4.5 GAF Materials

- 6.4.6 H.B. Fuller

- 6.4.7 Holcim

- 6.4.8 Hongyuan waterproof technology group co.,ltd

- 6.4.9 Jiangsu Canlon Building Materials Co.,Ltd.

- 6.4.10 Joaboa Technology

- 6.4.11 Johns Manville

- 6.4.12 Oriental Yuhong

- 6.4.13 Polygomma

- 6.4.14 Protan AS

- 6.4.15 Renolit SE

- 6.4.16 Sika AG

- 6.4.17 Soprema Group

- 6.4.18 Tremco Inc.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment