|

市場調查報告書

商品編碼

2062373

汽車空氣清新劑和除臭劑:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)Car Air Freshener - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

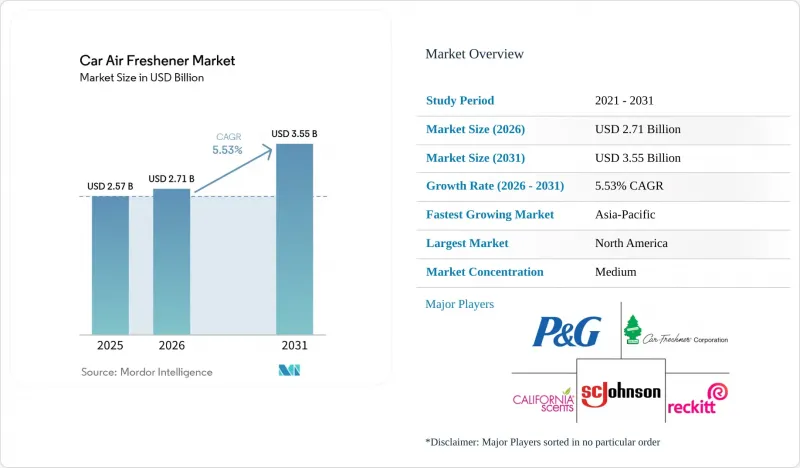

預計汽車空氣清新劑和除臭劑市場將從 2025 年的 25.7 億美元成長到 2026 年的 27.1 億美元,到 2031 年達到 35.5 億美元,2026 年至 2031 年的複合年成長率為 5.53%。

本報告按產品類型(吊掛空氣清新劑、通風口夾式空氣清新劑、噴霧/氣霧劑空氣清新劑、凝膠空氣清新劑等)、類別(大眾市場、高階市場)、銷售管道(實體店、網路商店)和地區(北美、歐洲、亞太、南美、中東和非洲)進行細分。市場預測以美元計價。

全球汽車空氣清新劑及除臭劑市場趨勢及洞察

香水領域的持續創新

可調式旋鈕式通風口夾、感應式凝膠香氛盒和緩釋噴霧氣霧劑正在重新定義消費者對吊掛空氣清新劑市場的期望。寶潔公司計畫於2024年推出的Febreze車載通風口夾,擁有長達40天的持久留香時間,並減少了20%的塑膠用量。這項創新表明,模組化設計不僅提升了產品的永續性,還能在不增加初始成本的情況下促進補充裝的銷售,從而吸引具有環保意識的消費者。揚基蠟燭公司的Sidekick香氛盒用途廣泛,適用於通風口、遮陽帽和吊墜式香氛架,使用者無需更換底座即可改變其形狀。這種適應性滿足了不同消費者的偏好,提供了便利,並減少了廢棄物。此外,跨品牌相容性,例如在Air Wick香氛盒中使用Glade補充裝,透過提供柔軟性和成本節約,降低了消費者的購買門檻。這種「刮鬍刀和刀片」策略如今也被應用於共享汽車,這些車輛需要快速更換香氛以適應乘客的更替,從而保持清新舒適的環境。將設備和耗材分開的品牌可以提高客戶終身價值,提升客戶維繫,並顯著降低對環境的影響。

偏好持久濃郁的香水

通勤者和叫車司機越來越傾向於選擇「擴散力」強、香味持續時間超過一個月的車載空氣清新劑。為了順應此一趨勢,吊掛式車載空氣清新劑市場的供應商正著力提升產品的性能標準,力求達到60天甚至365天的持久效果。 PURGGO採用竹炭吸附劑,號稱香味永續一年,並具備太陽能充電功能,使其成為無需頻繁補充的永續替代品。這款產品不僅吸引了具有環保意識的消費者,也滿足了人們對持久耐用、維護簡單的解決方案日益成長的需求。不同地區的消費者偏好也有差異。中東消費者偏好沉香濃郁的木質香氣,而北美消費者則更喜歡清新潔淨的柑橘香。一項2024年的車內空氣品質研究發現,噴灑15次後,車內揮發性有機化合物(VOC)的總濃度飆升至364.3微克/立方公尺。此外,在25°C下觀察到奈米顆粒分離率增加了25.3%,凸顯了供應商必須重視的健康問題。這些發現強調了製造商需要在香氛性能和安全標準之間取得平衡的必要性。現今的消費者越來越關注每日消費成本,他們傾向於選擇在香氛濃度和留香時間之間取得平衡的產品,以確保物有所值並滿足消費者的需求。

關於揮發性有機化合物和過敏原的健康問題

一項研究在12種不同的車載空氣清新劑中檢測到546種不同的揮發性有機化合物(VOCs),其中包括30種有害物質,例如乙醛和BETA-月桂烯,而這些物質均未在標籤上標明。這項發現加劇了消費者對吊掛式車載空氣清新劑市場的不信任,因為人們對潛在健康風險的認知正在不斷提高。美國環保署(EPA)指出,車內VOC濃度在使用產品期間可增加高達1000倍,這引發了嚴重的安全隱患,因為這種暴露與呼吸系統和神經系統疾病有關。為此,加州空氣資源委員會(CARB)和國際香料協會(IFRA)等監管機構正在收緊對可接受的香料過敏原的規定,迫使品牌商花費高昂的成本重新配製產品。聯邦標準對各種產品中的VOC含量設定了限制。單相香料的VOC含量上限為70%,雙相香料為30%,液體和噴霧劑為18%,固體和凝膠狀香料則僅為3%。雖然這些監管變化旨在降低健康風險,但也為製造商維持產品吸引力帶來了挑戰。無法在香氛性能和揮發性安全性之間取得平衡的公司,將面臨市場佔有率迅速流失的風險,因為低過敏性和無香型替代品正受到注重健康的消費者的青睞。

細分市場分析

2025年,吊掛空氣清新劑佔據市場主導地位,市佔率高達43.87%。其強勢地位源自於其成熟的品牌價值、廣泛的零售通路以及數十年來消費者對其的熟悉度。售價低於3美元的傳統紙質空氣清新劑刺激了便利商店和汽車產業的衝動消費。然而,它們也存在一些挑戰:香味的持久性和濃度不如新型產品。同時,通風口夾式和凝膠罐式空氣清新劑憑藉其便捷的設計,鞏固了其在中端價位市場的地位,因為它們符合防止駕駛分心的相關法規,並且可以被動釋放香味超過30天。儘管來自電動和可程式設計產品的競爭日益激烈,吊掛式仍保持著其優勢。

插電式和電動空氣清新劑正迅速崛起,預計到2031年將以6.24%的年複合成長率(CAGR)成長。這項快速成長得益於創新產品的湧現,例如可循環使用40-70天的電池供電式通風口夾、USB充電式香薰機和太陽能款。其中,太陽能款式尤其受到叫車司機的青睞,因為它可以調整香氛釋放間隔。隨著氣霧劑噴霧的流行度下降(預計到2024年,氣霧劑噴霧會導致車內揮發性有機化合物(VOC)濃度上升至364.3微克/立方米),人們正加速轉向這些更清潔、更持久的替代品。 Inhalio的應用程式控制LIN/CAN匯流排裝置和PURGGO的竹炭袋等高級產品在市場上脫穎而出,針對特定客戶群,其價格溢價高達3-5倍。隨著人們對永續性和健康的日益關注,這些電動空氣清新劑有望進一步擴大市場佔有率。

區域分析

到2025年,北美將佔吊掛式車載空氣清新劑市場41.52%的佔有率。在美國,消費者每年每輛車花費8至12美元。隨著監管日益複雜,例如加州將揮發性有機化合物(VOC)的含量上限設定為18%,以及九個州禁止使用後視鏡掛鉤式空氣清新劑,消費者正逐漸轉向使用通風口夾式空氣清新劑。寶潔公司(P&G)正著眼於填補1.7億個低滲透率的替換產品市場空白,並計劃於2026年推出其「Febrezé」品牌的車內空氣清新劑。這表明該公司正在策略性地將過濾與香氛功能相結合。加拿大和墨西哥透過新車附帶的原廠配件包來刺激市場需求,但其人均消費支出低於美國。

亞太地區預計將成為成長最快的地區,複合年成長率將達到6.58%,這主要得益於中國超過3億輛的龐大汽車保有量以及印度汽車保有量的快速成長。中國法規要求使用當地語言標註成分,這使得能夠對其成分進行認證的國內製造商更具優勢。文化差異影響著人們的偏好。在日本和韓國,竹炭香氛和淡雅的香氛更受歡迎,人們往往更注重除臭效果而非濃郁的香味。在印度,高階香氛在大都會圈廣受歡迎,而價格親民的紙香氛則在農村地區流行起來,凸顯了印度市場格局的多樣性。

歐洲市場雖然呈現穩定成長態勢,但也面臨許多挑戰,例如REACH法規中的過敏原警告和IFRA致敏物質法規。 BMWAtmosphere和賓士香氛系統等高階品牌已在德國和英國站穩腳跟,但在北歐國家,無香型產品更受歡迎。隨著原廠嵌入式模組的普及,富裕消費者正逐漸放棄購買售後補充裝產品,市場重點也轉向中階和低價位市場。在南美,巴西佔據主導地位,但其成長動能受到經濟波動的限制。同時,在中東,沙烏地阿拉伯和阿拉伯聯合大公國等市場的單車空氣清新劑支出依然強勁,消費者明顯偏好價格較高的沉香基香氛。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 香水產品持續創新

- 持久濃郁的香味偏好

- 過渡到天然環保原料

- 擴大高階和設計師產品線

- 人工智慧驅動的香水個性化客製化及與聯網汽車的整合

- 現已推出無需補充的固體基材(生物聚合物珠、竹子)

- 市場限制因素

- 關於揮發性有機化合物和過敏原的健康問題

- 車載空氣清淨機正在蠶食空氣清新劑的銷售量。

- 電動車內部氣味排放低

- 區域性吊掛後視鏡的限制以及防止駕駛分心的規定。

- 消費行為分析

- 監理展望

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 依產品類型

- 吊掛式

- 通風口夾式空氣清新劑

- 噴霧/氣霧劑空氣清新劑

- 凝膠型空氣清新劑

- 插電式/電動空氣清新劑

- 紙質空氣清新劑

- 其他

- 按類別

- 鱒魚

- 優質的

- 透過分銷管道

- 實體店面

- 線上零售商店

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 其他北美國家

- 歐洲

- 德國

- 英國

- 義大利

- 法國

- 西班牙

- 荷蘭

- 波蘭

- 比利時

- 瑞典

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 印尼

- 韓國

- 泰國

- 新加坡

- 其他亞太國家

- 南美洲

- 巴西

- 阿根廷

- 哥倫比亞

- 智利

- 秘魯

- 其他南美國家

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 奈及利亞

- 埃及

- 摩洛哥

- 土耳其

- 其他中東和非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Procter and Gamble(Febreze/Ambi Pur)

- Car-Freshner Corp.(Little Trees)

- Reckitt Benckiser(Air Wick)

- California Scents

- SC Johnson(Glade)

- Yankee Candle(Newell Brands)

- Church and Dwight(Arm and Hammer)

- Henkel

- Godrej Consumer Products

- Dabur

- HandStands/Energizer Brands

- Auto Expressions(Gold Eagle)

- Areon(Balev Corp.)

- Bullsone

- Sakura Group

- Aromate Industries

- Air Spencer

- Jo Malone Automotive Editions

- SmarDy

- Little Joe

- ELiX Scent(AROMATONE)

- Farcent Enterprise

- Kobayashi Pharmaceutical

- CAR MATE

- Involve Your Senses

第7章 市場機會與未來展望

According to Mordor Intelligence, the air fresheners market size is expected to increase from USD 2.57 billion in 2025 to USD 2.71 billion in 2026 and reach USD 3.55 billion by 2031, growing at a CAGR of 5.53% over 2026-2031.

This report is Segmented by Product Type (Hanging Air Fresheners, Vent Clip Air Fresheners, Spray/Aerosol Air Fresheners, Gel-Based Air Fresheners, and More), Category (Mass, Premium), Distribution Channel (Offline Retail Stores, Online Retail Stores), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Car Air Freshener Market Trends and Insights

Continuous fragrance-format innovation

Adjustable dial vent clips, motion-activated gel pods, and time-releasing spray aerosols are reshaping consumer expectations in the hanging air fresheners market. Procter & Gamble's Febreze CAR vent clip, set for a 2024 release, boasts a 40-day lifespan and a 20% reduction in plastic use. This innovation highlights how modular designs not only enhance product sustainability but also drive recurring refill sales without increasing initial costs, making it appealing to environmentally conscious consumers. Yankee Candle's Sidekick cartridge is versatile, fitting vent, visor, and pendant holders, enabling users to change forms without discarding the base. This adaptability caters to diverse consumer preferences, offering convenience and reducing waste. Additionally, cross-brand compatibility, like Glade refills in Air Wick dispensers, lowers the barriers for consumers by providing flexibility and cost savings. This "razor-and-blade" strategy is now being adopted by ride-share fleets, which need quick scent changes between passengers to maintain a fresh and pleasant environment. Brands that separate devices from their consumables can enhance their lifetime value, improve customer retention, and significantly reduce their environmental impact.

Preference for Long-Lasting, Intense Fragrances

Commuters and ride-share drivers are gravitating towards high "throw" fragrances, ones that linger for over a month. This trend has led suppliers to highlight performance benchmarks of 60 or even 365 days in the Hanging air fresheners market. PURGGO, with its bamboo-charcoal absorber, claims a year-long efficacy and boasts solar rechargeability, positioning itself as a sustainable alternative to products that require frequent refills. This product not only appeals to environmentally conscious consumers but also addresses the growing demand for low-maintenance, long-lasting solutions. Regional preferences are evident: customers in the Middle East are drawn to oud notes, which are rich and woody, while those in North America favor a zesty citrus touch, offering a fresh and clean aroma. A 2024 study on cabin air quality found total VOC levels spiking to 364.3 µg/m3 after 15 sprays. Additionally, it observed a 25.3% rise in nanoparticle fractions at 25 °C, highlighting the health considerations suppliers must address. These findings emphasize the need for manufacturers to balance fragrance performance with safety standards. Today's consumers are increasingly evaluating the cost per day, showing a preference for products that balance intensity with lasting power, ensuring both value and satisfaction.

Health concerns over VOCs and Allergens

A study identified 546 volatile organic compounds (VOCs) in a dozen car air fresheners, including 30 hazardous ones like acetaldehyde and beta-myrcene, all without any label disclosures. This revelation has sown seeds of distrust among consumers in the Hanging air fresheners market, as they become increasingly aware of potential health risks. The U.S. EPA has highlighted that during product use, cabin VOC levels can spike by as much as 1,000 times, and such exposure is linked to respiratory and neurological problems, raising significant safety concerns. In response, regulatory bodies like CARB and IFRA are tightening the reins on permissible fragrance allergens, leading to expensive reformulations for brands. Federal standards set VOC content limits for a range of products: single-phase air fresheners are allowed up to 70% VOCs, double-phase can have up to 30%, liquids and pump sprays are restricted to 18%, while solids and gels are limited to a mere 3%.These regulatory changes aim to mitigate health risks but pose challenges for manufacturers in maintaining product appeal. Those unable to strike a balance between scent performance and emission safety may swiftly lose market share to hypoallergenic or fragrance-free alternatives, which are gaining traction among health-conscious consumers.

Other drivers and restraints analyzed in the detailed report include:

- Shift toward natural and eco-friendly ingredients

- Growth in premium and designer offerings

- Cabin-air purifiers cannibalizing fragrance sales

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, hanging air fresheners dominated the market, capturing 43.87% share. This stronghold is attributed to their established brand equity, widespread retail presence, and decades of consumer familiarity. Traditional paper-based air fresheners, priced under USD 3, spurred impulse buys in convenience and automotive sectors. Yet, these face challenges: their scent longevity and intensity lag behind newer alternatives. Meanwhile, vent-mounted clips and gel pots, with their practical designs, cater to distracted-driver regulations and offer a passive scent release over 30 days, solidifying their place in the mid-price category. Despite rising competition from electric and programmable options, hanging air fresheners maintain their dominance.

Plug-in and electric air fresheners are on a rapid ascent, with projections indicating a 6.24% CAGR through 2031. This surge is driven by innovations like battery-powered vent clips boasting 40-70 day scent cycles, USB-charged diffusers, and solar-assisted models. The latter are particularly favored by ride-share drivers for their adjustable intervals. As aerosol sprays, which raised cabin VOCs to 364.3 µg/m3 in 2024, see a decline in preference, the shift towards these cleaner, longer-lasting alternatives accelerates. Premium products, such as Inhalio's app-controlled LIN/CAN-bus units and PURGGO's bamboo-charcoal bags, stand out in the market, commanding 3-5X price multiples among niche customers. With a growing emphasis on sustainability and health, these electric air fresheners are poised for an expanded market presence.

Geography Analysis

In 2025, North America accounted for 41.52% of the revenue in the hanging air fresheners market. In the U.S., consumers spent between USD 8-12 annually per vehicle. As regulatory complexities mount, with California imposing an 18% VOC cap and nine states banning rear-view-mirror hangers, consumers are increasingly gravitating towards vent clips. Procter & Gamble, eyeing the under-penetrated 170 million replacement gap, is set to launch Febreze-branded cabin filters in 2026, hinting at a strategic blend of filtration and fragrance. While Canada and Mexico contribute to demand through OEM accessory packs in new vehicles, their per-capita spending lags behind that of the U.S.

Asia-Pacific is poised for the swiftest growth at a 6.58% CAGR, driven by China's expansive vehicle base of over 300 million and India's brisk motorization. Chinese regulations mandate ingredient disclosures in the local language, giving an edge to domestic players who can certify their formulations. Cultural nuances shape preferences: Japan and South Korea favor bamboo-charcoal absorbers and subtle scents, prioritizing odor neutralization over pronounced fragrances. In India, metropolitan areas are leaning towards premium diffusers, while rural locales stick to budget-friendly paper trees, highlighting the market's diverse landscape.

Europe experiences steady growth, navigating challenges like REACH allergen warnings and IFRA sensitizer restrictions. Premium brands like BMW Atmosphere and Mercedes scent systems find a foothold in Germany and the UK, while Nordic nations show a preference for fragrance-free alternatives. As OEM-embedded modules gain traction, they're drawing affluent consumers away from aftermarket refills, shifting the market's focus towards mid-tier and value offerings. Brazil leads in South America, but its momentum is tempered by economic fluctuations. Meanwhile, in the Middle East, markets like Saudi Arabia and the UAE maintain robust per-vehicle fragrance expenditures, with a distinct preference for premium-priced oud-based notes.

- Procter and Gamble (Febreze / Ambi Pur)

- Car-Freshner Corp. (Little Trees)

- Reckitt Benckiser (Air Wick)

- California Scents

- SC Johnson (Glade)

- Yankee Candle (Newell Brands)

- Church and Dwight (Arm and Hammer)

- Henkel

- Godrej Consumer Products

- Dabur

- HandStands / Energizer Brands

- Auto Expressions (Gold Eagle)

- Areon (Balev Corp.)

- Bullsone

- Sakura Group

- Aromate Industries

- Air Spencer

- Jo Malone Automotive Editions

- SmarDy

- Little Joe

- ELiX Scent (AROMATONE)

- Farcent Enterprise

- Kobayashi Pharmaceutical

- CAR MATE

- Involve Your Senses

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Continuous fragrance-format innovation

- 4.2.2 Preference for long-lasting, intense fragrances

- 4.2.3 Shift toward natural and eco-friendly ingredients

- 4.2.4 Growth in premium and designer offerings

- 4.2.5 AI-driven scent personalization and connected-car integration

- 4.2.6 Emergence of solid-state, refill-free substrates (bio-polymer beads, bamboo)

- 4.3 Market Restraints

- 4.3.1 Health concerns over VOCs and allergens

- 4.3.2 Cabin-air purifiers cannibalising fragrance sales

- 4.3.3 Lower odour emissions in EV interiors

- 4.3.4 Regional rear-view-mirror hanging bans and distracted-driver regulations

- 4.4 Consumer Behavior Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Hanging Air Freshners

- 5.1.2 Vent Clip Air Freshners

- 5.1.3 Spray/Aerosol Air Freshners

- 5.1.4 Gel-based Air Freshners

- 5.1.5 Plug-in/Electric Air Freshners

- 5.1.6 Paper Air Fresheners

- 5.1.7 Others

- 5.2 By Category

- 5.2.1 Mass

- 5.2.2 Premium

- 5.3 By Distribution Channel

- 5.3.1 Offline Retail Stores

- 5.3.2 Online Retail Stores

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.1.4 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 Italy

- 5.4.2.4 France

- 5.4.2.5 Spain

- 5.4.2.6 Netherlands

- 5.4.2.7 Poland

- 5.4.2.8 Belgium

- 5.4.2.9 Sweden

- 5.4.2.10 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 Australia

- 5.4.3.5 Indonesia

- 5.4.3.6 South Korea

- 5.4.3.7 Thailand

- 5.4.3.8 Singapore

- 5.4.3.9 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Chile

- 5.4.4.5 Peru

- 5.4.4.6 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 South Africa

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 United Arab Emirates

- 5.4.5.4 Nigeria

- 5.4.5.5 Egypt

- 5.4.5.6 Morocco

- 5.4.5.7 Turkey

- 5.4.5.8 Rest of Middle East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Procter and Gamble (Febreze / Ambi Pur)

- 6.4.2 Car-Freshner Corp. (Little Trees)

- 6.4.3 Reckitt Benckiser (Air Wick)

- 6.4.4 California Scents

- 6.4.5 SC Johnson (Glade)

- 6.4.6 Yankee Candle (Newell Brands)

- 6.4.7 Church and Dwight (Arm and Hammer)

- 6.4.8 Henkel

- 6.4.9 Godrej Consumer Products

- 6.4.10 Dabur

- 6.4.11 HandStands / Energizer Brands

- 6.4.12 Auto Expressions (Gold Eagle)

- 6.4.13 Areon (Balev Corp.)

- 6.4.14 Bullsone

- 6.4.15 Sakura Group

- 6.4.16 Aromate Industries

- 6.4.17 Air Spencer

- 6.4.18 Jo Malone Automotive Editions

- 6.4.19 SmarDy

- 6.4.20 Little Joe

- 6.4.21 ELiX Scent (AROMATONE)

- 6.4.22 Farcent Enterprise

- 6.4.23 Kobayashi Pharmaceutical

- 6.4.24 CAR MATE

- 6.4.25 Involve Your Senses

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

全球汽車空氣清新劑市場規模、佔有率、趨勢和成長分析報告:2026-2034年

全球汽車空氣清新劑市場規模、佔有率、趨勢和成長分析報告:2026-2034年 2026年全球汽車空氣清新劑市場報告汽車空氣清新劑市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類,並預測至2026-2034年

2026年全球汽車空氣清新劑市場報告汽車空氣清新劑市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類,並預測至2026-2034年 汽車空氣清新劑市場機會、成長要素、產業趨勢分析及2026年至2035年預測

汽車空氣清新劑市場機會、成長要素、產業趨勢分析及2026年至2035年預測 汽車空氣清新劑市場規模、佔有率和成長分析(按產品類型、香型、材質、通路、最終用戶和地區分類)-2026-2033年產業預測

汽車空氣清新劑市場規模、佔有率和成長分析(按產品類型、香型、材質、通路、最終用戶和地區分類)-2026-2033年產業預測 汽車空氣清新劑市場-全球產業規模、佔有率、趨勢、機會和預測,按類型、產品形式、銷售通路、地區和競爭格局分類,2020-2030年預測

汽車空氣清新劑市場-全球產業規模、佔有率、趨勢、機會和預測,按類型、產品形式、銷售通路、地區和競爭格局分類,2020-2030年預測