|

市場調查報告書

商品編碼

2062333

高活性聚異丁烯:市佔率分析、產業趨勢與統計、成長預測(2026-2031)Highly Reactive Polyisobutylene - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

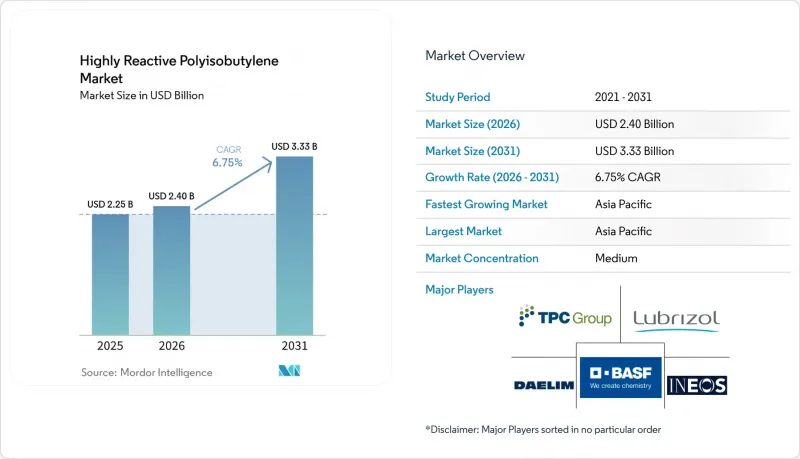

根據 Mordor Intelligence 預測,高反應性聚異丁烯的市場規模預計將在 2025 年達到 22.5 億美元,在 2026 年達到 24 億美元,在 2031 年達到 33.3 億美元,從 2026 年到 2031 年的複合年成長率為 6.75%。

本報告按分子量(小於1000 g/mol、1000–2500 g/mol和大於2500 g/mol)、應用領域(黏合劑、潤滑劑/分散劑等)、終端用戶產業(汽車/運輸等)以及地區(亞太地區、北美地區、歐洲地區、南美地區以及中東和非洲地區)進行細分。市場預測以美元計價。

全球高反應性聚異丁烯市場趨勢及洞察

對燃料和潤滑油添加劑的需求不斷成長

一項2025年發表的同行評審研究結合了密度泛函理論和引擎測試,發現含氮量為3.5%~4.0%的聚異丁烯琥珀醯亞胺(PIBSI)分散劑與金屬清潔劑相比,可將低速時的預燃抑制率提高98%,並將渦輪增壓器積碳減少90%。在Mack T-11卡車測試中,分散劑的胺基吸附在煙塵上,而疏水性的PIB鏈則阻止了煙塵聚集,從而使黏度增加不到20%。中國和印度將硫酸鹽灰含量限制在0.5%,磷含量限制在0.08%,有效地淘汰了二烷基二硫代磷酸鋅的使用,從而支持了這一趨勢。

電動車組裝中黏合劑和密封劑的消耗量激增

為防止水分滲入並控制逸散的熱氣體,電動車電池組每組使用 8 至 12 公尺長的聚異丁基橡膠密封繩和 200 至 400 克熱熔密封膠。漢高的「樂泰 RB EV 9740」密封繩和富樂公司的「EV SEAL 500」密封膠的氦氣滲透性低於 10⁻¹° cm³*cm/cm²*s*Pa,可承受高達 150 度C的溫度,並且在 1000 小時循環測試中性能優於丙烯酸類產品。預計到 2030 年,全球電動車產量將超過 2,000 萬輛,這意味著聚異丁基橡膠的需求量每年將增加高達 2 萬噸。

異丁烯價格波動劇烈

2025年第四季,中國異丁烯平均價格為每噸1,038美元,而美國則為每噸1,187美元。這一差異源自於煉油廠運轉率的不同。埃克森美孚和英力士集團透過充分利用其流體化媒裂(FCC)生產線維持了盈利能力,但依賴市場採購異丁烯的非一體化聚異丁烯(PIB)生產商由於盈利壓力而減少了對新裝置的投資。

細分市場分析

中等分子量聚異丁烯在2025年佔總銷售額的50.87%,鞏固了其在反應型聚異丁烯市場的主要地位。其在壓敏黏著劑和聚異丁烯琥珀酸酐(PIBSA)分散劑中的應用,確保了包裝和潤滑劑產業的穩定需求。高分子量聚異丁烯(分子量超過2500 g/mol)的複合年成長率達到6.63%,並且擴大應用於電池粘合劑和電纜浸漬劑等需要在100 度C下粘度超過300,000厘斯(cSt)的領域。

東南亞電纜製造商正從凡士林轉向富含聚異丁烯(PIB)的填充膏,並將介電強度超過20千伏/毫米(kV/mm)作為關鍵因素,這表明市場需求前景穩定。相較之下,由於煉油廠甲醇烷基化製程的經濟性問題,低分子量聚異丁烯(分子量小於1000克/莫耳)的成長正在放緩。這是因為辛烷值差距的擴大導致異丁烯被用於汽油混合燃料,從而限制了這種特殊聚合物的供應。

區域分析

預計到2025年,亞太地區將佔全球銷售額的47.03%,複合年成長率(CAGR)為7.32%。這一成長主要得益於中國在合成潤滑油領域實現自給自足的努力,以及韓國大林石油麗水工廠成本效益的提升。到2031年,該地區在高反應性聚異丁烯市場的佔有率預計將超過50%。這一成長是由於區域調配商提高了乘用車潤滑油中聚異丁烯磺醯亞胺(PIBSI)的比例,以滿足中國VI-B排放氣體標準。

北美在全球消費中佔據很大佔有率,這得益於其完善的價值鏈。 TPC集團、埃克森美孚和英力士等公司直接向其聚異丁烯(PIB)、聚異丁烯琥珀酸酐(PIBSA)和洗滌劑生產設施供應源自流體化媒裂(FCC)的異丁烯。 2024年,TPC集團將二異丁烯產能提高了27%,建立了一套符合《基加利修正案》的低全球暖化潛值(GWP)冷媒潤滑油供應體系。

在歐洲,主要產業參與者做出了貢獻。BASF位於路德維希港和安特衛普的工廠專注於生產中等分子量的聚異丁烯,這些聚異丁烯用於低硫酸鹽灰分、低磷低硫(低SAPS)引擎油配方,以滿足歐7排放標準測試車輛的需求。雖然對揮發性有機化合物(VOC)的嚴格監管減少了建築密封劑的產量,但對淨零排放建築中透水性薄膜的需求推動了特種聚異丁烯(PIB)的消費。南美洲和中東及非洲地區的總佔有率不到5%,但隨著沙烏地阿拉伯投資110億美元的「Amiral」石化綜合體於2027年運作,預計將實現成長。該綜合體整合了異丁烯萃取和特種聚合物生產。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 A. 標題與目錄

第2章目錄 - 高活性聚異丁烯市場

第3章:引言

- 研究假設和市場定義

- 調查範圍

第4章:調查方法

第5章執行摘要

第6章 市場狀況

- 市場概覽

- 市場促進因素

- 對燃油和潤滑油添加劑的需求增加

- 電動車組裝中黏合劑和密封劑的消耗量激增

- 加速亞太地區的產能擴張

- 推廣低SAPS和符合歐盟7排放標準的機油的相關法規

- HR-PIB作為固態電池黏合劑的新角色

- 生物基異丁烯原料的商業化

- 市場限制因素

- 異丁烯價格波動劇烈

- 嚴格的揮發性有機化合物和碳足跡法規

- 建設產業對無矽密封劑的需求日益成長

- 超低溫BF3聚合生產線需要高資本投資

- 價值鏈分析

- 波特五力模型

第7章 市場規模與成長預測

- 依分子量

- 分子量小於1000克/莫耳(低分子量)

- 1,000-2,500 g/mol(中等分子量)

- 分子量大於 2,500 g/mol(高分子量)

- 透過使用

- 黏合劑

- 潤滑劑分散劑

- 燃油清潔劑

- 密封膠帶

- 電纜化合物及其他

- 按最終用戶行業分類

- 汽車和運輸業

- 工業機械

- 石油和天然氣/煉油

- 建築和基礎設施

- 電氣和電子設備

- 按地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 東南亞國協

- 其他亞太國家

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲國家

- 亞太地區

第8章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- BASF

- Braskem

- Chemex Chemicals

- Chevron Oronite Company LLC

- China Petroleum & Chemical Corporation

- Daelim Co., Ltd.

- ExxonMobil Chemical

- INEOS AG

- Infineum International Limited

- Janex SA

- Kothari Petrochemicals Limited

- KZJ New Materials Group Co., Ltd.

- Lubrizol

- LyondellBasell Industries Holdings BV

- RB Products, Inc.

- Shandong Orient Hongye Chemical Co., Ltd.

- TPC Group

第9章 市場機會與未來展望

- 評估未開發的領域和未滿足的需求

According to Mordor Intelligence, the highly reactive polyisobutylene market size is projected to be USD 2.25 billion in 2025, USD 2.40 billion in 2026, and reach USD 3.33 billion by 2031, growing at a CAGR of 6.75% from 2026 to 2031.

This report is Segmented by Molecular Weight (Less Than 1, 000 G/Mol, 1, 000-2, 500 G/Mol, Greater Than 2, 500 G/Mol), Application (Adhesives, Lubricant Dispersants, and More), End-User Industry (Automotive and Transportation and More), Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Highly Reactive Polyisobutylene Market Trends and Insights

Rising Demand for Fuel and Lubricant Additives

According to a 2025 peer-reviewed study that combined density-functional theory with engine testing, polyisobutenyl succinimide (PIBSI) dispersants, containing 3.5-4.0% nitrogen, achieved a 98% suppression of low-speed pre-ignition and a 90% reduction in turbocharger deposits compared to metallic detergents. In Mack T-11 trials, the amine centers of the dispersants anchored to soot, while the hydrophobic PIB tails prevented agglomeration, ensuring viscosity rise remained below 20%. China and India bolstered this trend by imposing caps on sulfated ash at 0.5% and phosphorus at 0.08%, effectively sidelining the use of zinc dialkyldithiophosphate.

Surge in Adhesive and Sealant Consumption in EV Assembly

To prevent moisture ingress and contain thermal-runaway gases, electric-vehicle battery packs utilize 8-12 m of PIB-based butyl cord and 200-400 g of hot-melt sealant per unit. Henkel's LOCTITE RB EV 9740 cord and H.B. Fuller's EV SEAL 500 grade boast helium permeability below 10-1° cm3*cm/cm2*s*Pa and can withstand temperatures up to 150°C, surpassing acrylic counterparts in 1,000-hour cycling tests. With global EV assembly projected to exceed 20 million units by 2030, this translates to an additional PIB demand of up to 20,000 t/y.

Volatile Isobutylene Prices

In Q4 2025, isobutylene prices averaged USD 1,038 per ton in China, compared to USD 1,187 per ton in the United States, driven by differences in refinery run rates. Exxon Mobil Corporation and INEOS AG utilized their captive Fluid Catalytic Cracking (FCC) streams to sustain profit margins, while non-integrated Polyisobutylene (PIB) producers, dependent on merchant isobutylene purchases, reduced new plant investments due to margin pressures.

Other drivers and restraints analyzed in the detailed report include:

- Accelerated Capacity Additions in Asia-Pacific

- Emerging Role of HR-PIB as Binder in Solid-State Batteries

- Stringent VOC and Carbon-Footprint Regulations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Medium-molecular-weight grades accounted for 50.87% of the 2025 revenue, establishing them as key contributors in the reactive polyisobutylene market. Their application in pressure-sensitive adhesives and polyisobutylene succinic anhydride (PIBSA) dispersants ensures consistent demand from both packaging and lubricant sectors. High-molecular-weight grades (exceeding 2,500 g/mol) recorded a 6.63% compound annual growth rate (CAGR), gaining adoption in battery binders and cable flooding compounds that require viscosities above 300,000 centistokes (cSt) at 100 °C.

Southeast Asian cable manufacturers identify dielectric strength exceeding 20 kilovolts per millimeter (kV/mm) as a critical factor in transitioning from petroleum jelly to PIB-enriched flooding pastes, indicating a stable demand outlook. In contrast, low-molecular-weight PIB (below 1,000 g/mol) shows slower growth due to refinery alkylate economics, which diverts isobutylene into gasoline blending when octane spreads widen, limiting the availability of this specialty polymer.

Geography Analysis

Asia-Pacific, accounting for 47.03% of 2025's revenue, is growing at a 7.32% compound annual growth rate (CAGR). This growth is supported by China's efforts toward self-reliance in synthetic lubricants and the cost efficiencies achieved at Daelim's Yeosu site in South Korea. By 2031, the region's share in the highly reactive polyisobutylene market is expected to exceed 50%. This increase is driven by regional blenders raising polyisobutylene succinimide (PIBSI) inclusion rates in passenger-car oils to comply with China VI-B emission standards.

North America accounted for a significant portion of global consumption, supported by integrated value chains. Companies such as TPC Group, ExxonMobil, and INEOS direct fluid catalytic cracking (FCC)-sourced isobutylene into their proprietary polyisobutylene (PIB), polyisobutylene succinic anhydride (PIBSA), and detergent production facilities. In 2024, TPC Group expanded its diisobutylene capacity by 27%, positioning itself to supply low-global warming potential (GWP) refrigerant lubricants in compliance with the Kigali Amendment.

Europe contributed through key industry players. BASF's facilities in Ludwigshafen and Antwerp focus on medium-molecular-weight grades, which are used in low-sulfated ash, phosphorus, and sulfur (low-SAPS) engine-oil packages for Euro-7 test fleets. Although strict volatile organic compound (VOC) limits have reduced construction sealant volumes, demand for breathable membranes in net-zero buildings has supported specialty polyisobutylene (PIB) consumption. South America and the Middle East-Africa, together accounting for less than 5%, may see growth following the 2027 start-up of Saudi Arabia's USD 11 billion Amiral petrochemical complex, which integrates isobutylene extraction with specialty polymer production.

- BASF

- Braskem

- Chemex Chemicals

- Chevron Oronite Company LLC

- China Petroleum & Chemical Corporation

- Daelim Co., Ltd.

- ExxonMobil Chemical

- INEOS AG

- Infineum International Limited

- Janex S.A.

- Kothari Petrochemicals Limited

- KZJ New Materials Group Co., Ltd.

- Lubrizol

- LyondellBasell Industries Holdings B.V.

- RB Products, Inc.

- Shandong Orient Hongye Chemical Co., Ltd.

- TPC Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 A. Title and Table of Contents

2 Table of Contents - Highly Reactive Polyisobutylene Market

3 Introduction

- 3.1 Study Assumptions and Market Definition

- 3.2 Scope of the Study

4 Research Methodology

5 Executive Summary

6 Market Landscape

- 6.1 Market Overview

- 6.2 Market Drivers

- 6.2.1 Rising demand for fuel and lubricant additives

- 6.2.2 Surge in adhesive and sealant consumption in EV assembly

- 6.2.3 Accelerated capacity additions in Asia-Pacific

- 6.2.4 Regulatory push for low-SAPS and Euro-7-compliant engine oils

- 6.2.5 Emerging role of HR-PIB as binder in solid-state batteries

- 6.2.6 Commercialization of bio-based isobutylene feedstock

- 6.3 Market Restraints

- 6.3.1 Volatile isobutylene prices

- 6.3.2 Stringent VOC and carbon-footprint regulations

- 6.3.3 Growing preference for silicone-free sealants in construction

- 6.3.4 High CAPEX for ultra-low-temperature BF3 polymerization lines

- 6.4 Value Chain Analysis

- 6.5 Porter's Five Forces

- 6.5.1 Bargaining Power of Suppliers

- 6.5.2 Bargaining Power of Buyers

- 6.5.3 Threat of New Entrants

- 6.5.4 Threat of Substitutes

- 6.5.5 Competitive Rivalry

7 Market Size and Growth Forecasts (Value)

- 7.1 By Molecular Weight

- 7.1.1 Less than 1,000 g/mol (Low)

- 7.1.2 1,000-2,500 g/mol (Medium)

- 7.1.3 Greater than 2,500 g/mol (High)

- 7.2 By Application

- 7.2.1 Adhesives

- 7.2.2 Lubricant Dispersants

- 7.2.3 Fuel Detergents

- 7.2.4 Sealant Tapes

- 7.2.5 Cable Compounds and Others

- 7.3 By End-user Industry

- 7.3.1 Automotive and Transportation

- 7.3.2 Industrial Machinery

- 7.3.3 Oil and Gas/Refining

- 7.3.4 Construction and Infrastructure

- 7.3.5 Electrical and Electronics

- 7.4 By Geography

- 7.4.1 Asia-Pacific

- 7.4.1.1 China

- 7.4.1.2 Japan

- 7.4.1.3 India

- 7.4.1.4 South Korea

- 7.4.1.5 ASEAN Countries

- 7.4.1.6 Rest of Asia-Pacific

- 7.4.2 North America

- 7.4.2.1 United States

- 7.4.2.2 Canada

- 7.4.2.3 Mexico

- 7.4.3 Europe

- 7.4.3.1 Germany

- 7.4.3.2 United Kingdom

- 7.4.3.3 France

- 7.4.3.4 Italy

- 7.4.3.5 Spain

- 7.4.3.6 Russia

- 7.4.3.7 Rest of Europe

- 7.4.4 South America

- 7.4.4.1 Brazil

- 7.4.4.2 Argentina

- 7.4.4.3 Rest of South America

- 7.4.5 Middle East and Africa

- 7.4.5.1 Saudi Arabia

- 7.4.5.2 South Africa

- 7.4.5.3 Rest of Middle East and Africa

- 7.4.1 Asia-Pacific

8 Competitive Landscape

- 8.1 Market Concentration

- 8.2 Strategic Moves

- 8.3 Market Share(%)/Ranking Analysis

- 8.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, Recent Developments)

- 8.4.1 BASF

- 8.4.2 Braskem

- 8.4.3 Chemex Chemicals

- 8.4.4 Chevron Oronite Company LLC

- 8.4.5 China Petroleum & Chemical Corporation

- 8.4.6 Daelim Co., Ltd.

- 8.4.7 ExxonMobil Chemical

- 8.4.8 INEOS AG

- 8.4.9 Infineum International Limited

- 8.4.10 Janex S.A.

- 8.4.11 Kothari Petrochemicals Limited

- 8.4.12 KZJ New Materials Group Co., Ltd.

- 8.4.13 Lubrizol

- 8.4.14 LyondellBasell Industries Holdings B.V.

- 8.4.15 RB Products, Inc.

- 8.4.16 Shandong Orient Hongye Chemical Co., Ltd.

- 8.4.17 TPC Group

9 Market Opportunities and Future Outlook

- 9.1 White-space and Unmet-need Assessment

聚丁烯-1市場規模、佔有率和成長分析:按等級、應用、最終用途、通路和地區分類-2026年至2033年產業預測

聚丁烯-1市場規模、佔有率和成長分析:按等級、應用、最終用途、通路和地區分類-2026年至2033年產業預測 聚異丁烯市場:依形態、分子量、類型、應用和最終用途產業分類-2026-2032年全球市場預測

聚異丁烯市場:依形態、分子量、類型、應用和最終用途產業分類-2026-2032年全球市場預測 全球聚異丁烯市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球聚異丁烯市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 2026年全球聚異丁烯市場報告

2026年全球聚異丁烯市場報告 聚丁烯市場規模、佔有率及成長分析(按等級、應用和地區分類)-2026-2033年產業預測

聚丁烯市場規模、佔有率及成長分析(按等級、應用和地區分類)-2026-2033年產業預測 聚異丁烯(PIB):市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

聚異丁烯(PIB):市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 聚異丁烯市場規模、佔有率和成長分析(按產品類型、分子量、價格分佈範圍、應用、最終用戶、分銷管道和地區分類)—產業預測(2026-2033 年)

聚異丁烯市場規模、佔有率和成長分析(按產品類型、分子量、價格分佈範圍、應用、最終用戶、分銷管道和地區分類)—產業預測(2026-2033 年) 聚異丁烯市場機會、成長要素、產業趨勢分析及預測(2026年至2035年)

聚異丁烯市場機會、成長要素、產業趨勢分析及預測(2026年至2035年) 中等分子量聚異丁烯:全球市佔率和排名、總收入和需求預測(2025-2031年)

中等分子量聚異丁烯:全球市佔率和排名、總收入和需求預測(2025-2031年) 聚丁烯的全球市場:等級·用途·各地區 (~2035年)

聚丁烯的全球市場:等級·用途·各地區 (~2035年)