|

市場調查報告書

商品編碼

1913421

聚異丁烯市場機會、成長要素、產業趨勢分析及預測(2026年至2035年)Polyisobutylene Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

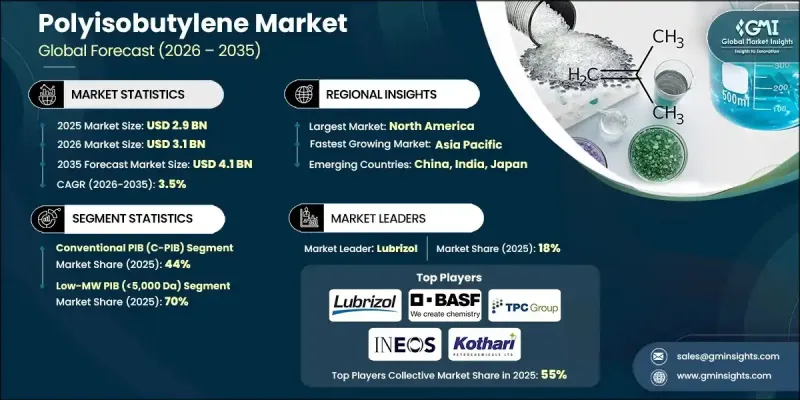

全球聚異丁烯市場預計到 2025 年將達到 29 億美元,到 2035 年將達到 41 億美元,年複合成長率為 3.5%。

食品接觸和個人護理等行業日益嚴格的安全和品質標準推動了這一成長,促進了兼容型聚異丁烯 (PIB) 的應用。包括美國食品藥物管理局(FDA) 在內的監管核准批准了 PIB 用於食品接觸黏合劑和塗料,並設定了特定的最低數均分子量標準以確保安全性。化妝品級和氫化 PIB 在潤膚劑和成膜應用中具有穩定性和皮膚相容性,從而在細分市場中佔據高階市場。新興地區基礎設施的不斷完善推動了對黏合劑、密封劑和玻璃塗層解決方案的需求,而 PIB 因其黏合性、柔軟性、耐化學性和極低的水蒸氣滲透性而備受青睞。此外,永續性趨勢和日益嚴格的法規正在推動生物基 PIB 和清潔製造流程的發展,而不斷完善的合規框架則推動了對低影響催化劑和環保原料的研發。

| 市場覆蓋範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 29億美元 |

| 預測金額 | 41億美元 |

| 複合年成長率 | 3.5% |

由於傳統聚異丁烯(C-PIB)在黏合劑、密封劑、工業油、口香糖基料、塗料等領域的廣泛應用,預計到2025年,C-PIB市場佔有率將達到44%。建築和包裝行業對C-PIB的需求密切相關,這兩個行業依賴其柔軟性、黏合性和防潮性能。 C-PIB的市場價格通常在每公斤0.8美元至1.5美元之間,具體價格取決於分子量和純度,TPC集團、BASF和英力士等主要生產商擁有強大的供應基礎。

到2025年,高分子量聚異丁烯(PIB,分子量大於100,000道爾頓)將佔據10%的市場佔有率,主要用於口香糖基料、醫療設備和特種密封劑等需要無味、無毒和高阻隔性能的特定應用領域。製造流程的進步提高了產量並增強了耐熱性,從而拓展了其在醫療和食品級應用領域的應用範圍。

預計到2025年,北美聚異丁烯市場將佔全球市場佔有率的33%,這主要得益於汽車行業的強勁發展、高反應性聚異丁烯的充足供應以及完善的添加劑生產商網路。美國憑藉其一體化的石化聯合企業和豐富的原料供應,仍然是主要的產能來源地;而加拿大的汽車和潤滑油產業則為區域供應鏈和下游應用提供了補充。

目錄

第1章調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段的附加價值

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 促進要素

- 產業潛在風險與挑戰

- 市場機遇

- 成長潛力分析

- 監管環境

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特五力分析

- PESTEL 分析

- 價格趨勢

- 按地區

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 專利狀態

- 貿易統計(HS編碼)(註:僅提供主要國家的貿易統計)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續努力

- 減少廢棄物策略

- 生產中的能源效率

- 環保舉措

- 碳足跡考量

第4章 競爭情勢

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 重大進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章 依產品類型分類的市場規模及預測(2022-2035年)

- 傳統聚異丁烯(C-PIB)

- 高反應性聚異丁烯(HR-PIB)

第6章 以分子量分類的市場規模及預測(2022-2035年)

- 低分子量聚異丁烯二酚(平均分子量<5,000道爾頓)

- 中等分子量聚異丁烯二酚(平均分子量 40,000-100,000 道爾頓)

- 高分子量聚異丁烯 (Mn>100,000 Da)

第7章 依應用領域分類的市場規模及預測(2022-2035年)

- 潤滑油添加劑

- 燃油添加劑

- 黏合劑和密封劑

- 輪胎和橡膠製品

- 電氣絕緣

- 個人護理及化妝品

- 食品接觸應用

- 拉伸膜/包裝

- 其他

第8章 依等級分類的市場規模及預測,2022-2035年

- 食品級聚異丁基 ...

- 化妝品級聚異丁基 ...

- 醫藥級PIB

- 其他

第9章 2022-2035年各地區市場規模及預測

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地區

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東和非洲地區

第10章:公司簡介

- Braskem

- RB Products

- TPC Group

- Lanxess

- Infineum International

- Kothari Petrochemicals

- Janex

- ExxonMobil Corporation

- Berkshire Hathaway

- Lubrizol

- Chevron Oronite Company

- Mayzo

The Global Polyisobutylene Market was valued at USD 2.9 billion in 2025 and is estimated to grow at a CAGR of 3.5% to reach USD 4.1 billion by 2035.

The growth is driven by increasing safety and quality standards in industries such as food contact and personal care, which encourage the adoption of compliant PIB grades. Regulatory approvals, including those by the U.S. FDA, allow PIB in food-contact adhesives and coatings, with specific minimum number-average molecular weight thresholds to ensure safety. Cosmetic and hydrogenated PIB grades provide stability and skin compatibility for emollients and film-forming applications, supporting premium pricing in niche markets. The expansion of infrastructure in emerging regions fuels demand for adhesives, sealants, and glazing solutions, where PIB's tack, flexibility, chemical resistance, and extremely low moisture vapor transmission are highly valued. Additionally, sustainability trends and regulatory tightening are encouraging the development of bio-based PIB and cleaner production processes, while evolving compliance frameworks are directing R&D toward lower-impact catalysts and environmentally friendly feedstocks.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.9 Billion |

| Forecast Value | $4.1 Billion |

| CAGR | 3.5% |

The conventional PIB (C-PIB) segment held 44% share in 2025, owing to its extensive use in adhesives, sealants, industrial oils, chewing gum bases, and coatings. Demand for C-PIB closely follows construction and packaging sectors that rely on its flexibility, tack, and moisture barrier properties. Market prices for C-PIB typically range from USD 0.8-1.5 per kilogram, depending on molecular weight and purity, with major producers such as TPC Group, BASF, and INEOS maintaining strong supply positions.

The high-molecular-weight PIB (>100,000 Da) segment accounted for 10% share in 2025, serving niche applications like chewing gum bases, medical devices, and specialized sealants that require tastelessness, non-toxicity, and high barrier strength. Advances in production processes have increased yields and expanded temperature tolerance, broadening the application spectrum for medical and food-grade uses.

North America Polyisobutylene Market held 33% share in 2025, driven by a concentration of automotive hubs, strong merchant high-reactivity PIB supply, and a robust network of additive formulators. The U.S. remains a key contributor to production capacity, supported by integrated petrochemical complexes and abundant feedstocks, while Canada's automotive and lubricant sectors complement regional supply and downstream applications.

Key players in the Global Polyisobutylene Market include TPC Group, Braskem SA, Lanxess, RB Products, Infineum International Ltd, Kothari Petrochemicals, Janex, ExxonMobil Corporation, Berkshire Hathaway, Lubrizol, Chevron Oronite Company, and Mayzo. To strengthen their presence, companies in the Polyisobutylene Market focus on several strategic approaches. They invest heavily in process optimization and R&D to enhance product quality, expand molecular weight ranges, and develop bio-based and sustainable grades. Strategic collaborations and partnerships allow for technology sharing, faster commercialization, and access to new regional markets. Firms also pursue capacity expansions in key geographies, particularly near high-demand industrial hubs, ensuring reliable supply chains. Additionally, regulatory compliance and certifications are emphasized to support entry into food, cosmetic, and medical applications.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Product type

- 2.2.2 Molecular weight

- 2.2.3 Grade

- 2.2.4 Application

- 2.3 TAM analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Size and Forecast, By Product Type, 2022-2035 (USD Billion, Kilo Tons)

- 5.1 Key trends

- 5.2 Conventional polyisobutylene (C-PIB)

- 5.3 Highly reactive polyisobutylene (HR-PIB)

Chapter 6 Market Size and Forecast, By Molecular Weight, 2022-2035 (USD Billion, Kilo Tons)

- 6.1 Key trends

- 6.2 Low molecular weight PIB (Mn < 5,000 Da)

- 6.3 Medium molecular weight PIB (Mn 40,000-100,000 Da)

- 6.4 High molecular weight PIB (Mn > 100,000 Da)

Chapter 7 Market Size and Forecast, By Application, 2022-2035 (USD Billion, Kilo Tons)

- 7.1 Key trends

- 7.2 Lubricant additives

- 7.3 Fuel additives

- 7.4 Adhesives & sealants

- 7.5 Tires & rubber products

- 7.6 Electrical insulation

- 7.7 Personal care & cosmetics

- 7.8 Food contact applications

- 7.9 Stretch films & packaging

- 7.10 Others

Chapter 8 Market Size and Forecast, By Grade, 2022-2035 (USD Billion, Kilo Tons)

- 8.1 Key trends

- 8.2 Food-grade PIB

- 8.3 Cosmetic-grade PIB

- 8.4 Pharmaceutical-grade PIB

- 8.5 Others

Chapter 9 Market Size and Forecast, By Region, 2022-2035 (USD Billion, Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East & Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

- 9.6.4 Rest of Middle East & Africa

Chapter 10 Company Profiles

- 10.1 Braskem

- 10.2 RB Products

- 10.3 TPC Group

- 10.4 Lanxess

- 10.5 Infineum International

- 10.6 Kothari Petrochemicals

- 10.7 Janex

- 10.8 ExxonMobil Corporation

- 10.9 Berkshire Hathaway

- 10.10 Lubrizol

- 10.11 Chevron Oronite Company

- 10.12 Mayzo

聚異丁烯市場:依形態、分子量、類型、應用和最終用途產業分類-2026-2032年全球市場預測

聚異丁烯市場:依形態、分子量、類型、應用和最終用途產業分類-2026-2032年全球市場預測 全球聚異丁烯市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球聚異丁烯市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 2026年全球聚異丁烯市場報告

2026年全球聚異丁烯市場報告 聚丁烯市場規模、佔有率及成長分析(按等級、應用和地區分類)-2026-2033年產業預測

聚丁烯市場規模、佔有率及成長分析(按等級、應用和地區分類)-2026-2033年產業預測 聚異丁烯(PIB):市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

聚異丁烯(PIB):市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 聚異丁烯市場規模、佔有率和成長分析(按產品類型、分子量、價格分佈範圍、應用、最終用戶、分銷管道和地區分類)—產業預測(2026-2033 年)

聚異丁烯市場規模、佔有率和成長分析(按產品類型、分子量、價格分佈範圍、應用、最終用戶、分銷管道和地區分類)—產業預測(2026-2033 年) 中等分子量聚異丁烯:全球市佔率和排名、總收入和需求預測(2025-2031年)

中等分子量聚異丁烯:全球市佔率和排名、總收入和需求預測(2025-2031年) 聚丁烯的全球市場:等級·用途·各地區 (~2035年)

聚丁烯的全球市場:等級·用途·各地區 (~2035年) 2032年聚異丁烯市場預測:按產品、分子量、應用、最終用戶和地區進行的全球分析

2032年聚異丁烯市場預測:按產品、分子量、應用、最終用戶和地區進行的全球分析 全球中分子量聚異丁烯市場

全球中分子量聚異丁烯市場