|

市場調查報告書

商品編碼

2062327

超高純度碳化矽:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Ultra High Purity Silicon Carbide - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

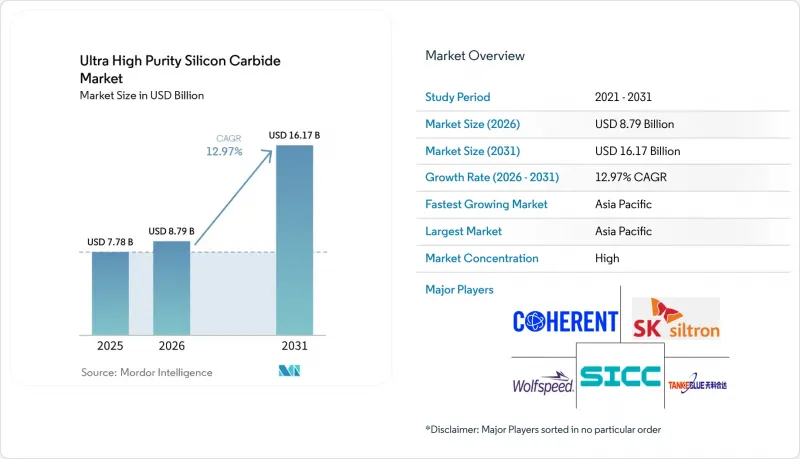

據 Mordor Intelligence 稱,2025 年超高純度碳化矽市場價值為 77.8 億美元,預計到 2031 年將達到 161.7 億美元,而 2026 年為 87.9 億美元,預測期(2026-2031 年)的複合年成長率為 12.97%。

本報告按純度等級(99.9999% 或更高 (6N)、99.999% 或更高 (5N) 等)、形態(粉末等)、應用領域(電力電子等)、終端用戶產業(汽車、可再生能源等)和地區(亞太地區、北美地區、歐洲地區、南美地區、中東和非洲地區)進行細分。市場預測以美元計價。

全球超高純度碳化矽市場趨勢及洞察

電動車牽引逆變器和車用充電器

汽車製造商正在將碳化矽(SiC)MOSFET標準化應用於驅動逆變器,與矽元件相比,效率可提高5%至10%,並在不增加電池組尺寸的情況下延長續航里程。高達200 度C的結溫可使冷卻系統品質減少50%,並使逆變器能夠整合到馬達殼體內。安森美半導體(Onsemi)與博格華納(BorgWarner)之間超過10億美元的終身收入協議凸顯了SiC技術的普及。目前,22kW三相車載充電器利用SiC的高頻開關特性,將磁性元件的體積減少了40%,這對於電池容量超過100kWh的電動車來說是一項重大成就。在中國,強勁的需求正在形成,預計到2025年,800V電動車的銷量將超過120萬輛,而SiC逆變器預計將佔其逆變器總量的80%以上。

電網級和商用太陽能逆變器

與矽的98.0%相比,碳化矽(SiC)拓樸結構的峰值效率可達99.1%。這相當於絕對值提高了1個百分點,對於每60吉瓦的裝置容量,每年可額外發電600兆瓦。弗勞恩霍夫研究所的250千瓦演示裝置將逆變器體積縮小了40%,使其能夠安裝在重量受限的屋頂結構上。效率的提升可將高太陽輻射地區的投資回收期縮短至多9個月,加速印度和中東地區的應用。歐盟資助的SiC4GRID計畫已撥款1,500萬歐元(1,696萬美元),在2027年為北海風電場安裝中壓轉換器。 Kaco的100千瓦和125千瓦SiC產品已在快速成長的分散式發電細分市場中佔據領先地位。

高純度和晶體生長成本

對於單片200毫米晶錠,在2300 度C下進行物理氣相生長需要7到10天,消耗高達20兆瓦時的電力以及昂貴的超高純氬氣。因此,基板的生產成本高達400到600美元,是矽基板(成本為50到80美元)的5到10倍。外延製程也會使每片晶圓的成本增加150到200美元。中國供應商正利用規模經濟和廉價勞動力,在2023年至2025年間將價格降低40%,迫使現有製造商加速向300毫米晶圓的轉型。

細分市場分析

純度為99.99999%或更高(7N+)的碳化矽細分市場預計在預測期(2026-2031年)內將以13.68%的複合年成長率成長,超過純度為99.9999%或更高(6N)的細分市場。後者在2025年佔了超高純度碳化矽市場48.04%的佔有率。市場需求主要來自1200V和1700V汽車逆變器以及3300V太陽能轉換器,這些應用要求雜質含量低於1ppb。英飛凌的CoolSiC Gen2僅使用7N+基板,而連貫則推出了用於10kV人工智慧資料中心電源模組的厚膜外延7N+晶圓。雖然 5N 材料在傳統 LED 和拋光應用中仍佔據一席之地,但裝置製造商正在簽署 7N+ 的供應契約,以確保其高壓藍圖的未來。

出於成本考慮,6N基板在主流的650V至1200V電動車驅動應用中仍然至關重要。 ROHM的第五代MOSFET採用6N基板,在7mm x 7mm的晶片尺寸上實現了1.0 mΩ的導通電阻,滿足高達175 度C的熱設計要求。從長遠來看,良率的提高和晶圓直徑的增加有望縮小成本差距,從而加速7N+基板在中壓級應用上的普及。

即使到了2025年,4吋外延晶圓仍佔據超高純度碳化矽市場45.06%的佔有率,但隨著資本投資轉向200毫米生產線,6吋和8吋晶圓的市場佔有率正在不斷成長。 Resonac公司的第三代HGE-3G外延晶圓於2023年開始量產,並於2025年交付了首批200毫米晶圓。粉末(主要用於磨料和陶瓷)仍然是一種成長緩慢的輔助產品。

隨著整合設備製造商 (IDM) 將基板製造業務納入企業內部,體晶圓產量預計將成長 13.92%。意法半導體 (STMicroelectronics) 投資 50 億歐元(56.5 億美元)在卡塔尼亞的園區體現了從粉末到模組的全流程生產模式,併計劃到 2033 年實現每週生產 15,000 片晶圓。電裝 (Denso) 和富士馬達 (Fuji Electric) 的合資企業計劃到 2027 年每年向豐田供應 310,000 片晶圓,這表明原始設備製造商 (OEM) 對自主晶體製造能力有著強勁的需求。

區域分析

預計到2025年,亞太地區將佔全球銷售額的52.67%,並在預測期(2026-2031年)內以14.09%的複合年成長率成長。日本已投入3,503億日圓(約24億美元)的補貼,以加強其國內碳化矽(SiC)供應鏈。此外,中國的TankeBlue和SICC透過提升價格競爭力,在全球基板生產中佔了相當大的佔有率。韓國的目標是實現20%的碳化矽自給率,並計劃在2027年將其200毫米產能擴大十倍,並利用聯邦政府和密西根州政府的獎勵支持SK Siltron CSS。印度目前仍主要集中在裝置封裝領域,但英飛凌在馬來西亞Klim工廠的200毫米晶圓廠正在擴建中。

根據《晶片和整合產品法案》(CHIPS Act),北美地區將受益於7.5億美元的津貼,用於Wolfspeed位於賽勒城(Cylar City)的工廠建設。預計到2030年,該工廠將使美國國內產能翻三倍。美國預計在2025年成為全球領先的基板)生產國,同時在300毫米PCB的研發領域也佔據主導地位。加拿大和墨西哥的組裝規模小規模。安森美半導體(ON Semiconductor)在韓國的擴張正在服務北美汽車客戶,並增強雙邊供應鏈的穩定性。

在歐洲,政府支持的大型企劃正在推動產能整合。意法半導體(STMicroelectronics)位於卡塔尼亞的園區運作,該計畫價值50億歐元(56.5億美元);英飛凌(Infineon)位於德勒斯登的智慧功率製造廠已獲得歐盟10億歐元(16.5億美元)的資金支持。安森美半導體(ON Semiconductor)正在捷克共和國建造歐洲首條完全整合的碳化矽(SiC)生產線。羅姆(ROHM)旗下的SiCrystal計畫在2027年將其在德國的產能提高三倍。英國和法國提供設計技術,但晶圓生產能力有限。

南美洲和中東/非洲地區的貢獻仍然最低,其重點在於下游可再生能源項目,而非上游基板製造。巴西的電動車計畫進口碳化矽元件,中東一個50吉瓦的太陽能發電計畫有望提振逆變器需求,但這兩個地區都沒有宣布高純度藍光晶片的產能。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 電動車牽引逆變器和車用充電器

- 用於電網級和工商業應用的可再生能源逆變器

- 800V車輛架構帶來的需求激增

- 政府獎勵措施吸引碳化矽晶圓廠落腳該國

- 300 毫米 SiC 鋼錠的技術進步提高了 7 N 的產量。

- 市場限制因素

- 高純度製程和晶體生長成本

- 超純原料供應有限。

- 基面位錯導致晶圓良率降低

- 價值鏈分析

- 波特五力模型

第5章 市場規模與成長預測

- 純度

- 99.999% 或更高 (5N)

- 99.9999% 或更高 (6N)

- 99.99999% 或更高 (7 N+)

- 按形式

- 塊狀晶體

- 外延晶片(4吋)

- 外延晶片(6吋和8吋)

- 粉末

- 透過使用

- 電力電子

- 半導體(分離式元件和積體電路)

- LED和光電子學

- 太陽能

- 高科技陶瓷和其他

- 按最終用戶行業分類

- 車

- 可再生能源

- 通訊和5G

- 家用電子產品

- 國防/航太

- 工業及其他

- 按地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 東南亞國協

- 其他亞太國家

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲國家

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- 5N Plus

- Coherent Corp.

- CoorsTek Inc.

- Entegris

- Fujimi Corporation

- Infineon Technologies AG

- Nippon Steel Corporation

- Resonac Holdings Corporation

- ROHM Co., Ltd.

- Semiconductor Components Industries, LLC

- SiCrystal GmbH

- SICC Co., Ltd.

- SK Siltron CSS

- STMicroelectronics

- TankeBlue Co., Ltd.

- Tokai Carbon Co., Ltd.

- Washington Mills

- Wolfspeed, Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the ultra high purity silicon carbide market size was valued at USD 7.78 billion in 2025 and is estimated to grow from USD 8.79 billion in 2026 to reach USD 16.17 billion by 2031, at a CAGR of 12.97% during the forecast period (2026-2031).

This report is Segmented by Purity Level (Greater Than 99. 9999% (6N), Greater Than 99. 999% (5N), and More), Form (Powder, and More), Application (Power Electronics, and More), End-User Industry (Automotive, Renewable Energy, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Ultra High Purity Silicon Carbide Market Trends and Insights

EV Traction Inverters and On-Board Chargers

Automakers have standardized SiC MOSFETs in traction inverters to unlock 5%-10% efficiency gains over silicon, extending driving range without enlarging the battery pack. Junction temperatures up to 200°C halve the cooling-system mass and allow inverters to be integrated within the e-motor housing. Lifetime revenue contracts exceeding USD 1 billion between Onsemi and BorgWarner underscore mainstream adoption. Three-phase 22 kW on-board chargers now exploit SiC's high-frequency switching to shrink magnetics by 40%, a key win as battery capacities exceed 100 kWh. China surpassed 1.2 million 800-V EVs in 2025, and SiC captured more than 80% of their inverters, creating a resilient demand floor.

Grid-Scale and Commercial Solar Inverters

SiC topologies yield 99.1% peak efficiency versus 98.0% for silicon, an absolute 1-point gain that equates to an extra 600 MW annually per 60 GW of installations. Fraunhofer's 250 kW demo cut inverter volume by 40%, enabling rooftop deployments on weight-limited structures. Higher efficiency shortens payback by up to nine months in high-irradiance regions, spurring adoption in India and the Middle East. The EU-funded SiC4GRID project earmarked EUR 15 million (USD 16.96 million) for medium-voltage converters that will debut on North Sea wind farms in 2027. Kaco's 100 kW and 125 kW SiC products already lead the fast-growing distributed-generation niche.

High Purification and Crystal-Growth Cost

Each 200 mm boule requires 7-10 days of physical-vapor transport at 2,300°C, consuming as much as 20 MWh and expensive ultra-pure argon. The resulting USD 400-USD 600 substrate contrasts with USD 50-USD 80 silicon, a 5X-10X penalty. Epitaxy adds another USD 150-USD 200 per wafer. Chinese suppliers cut prices 40% between 2023 and 2025 through scale and cheaper labor, pressuring incumbents to accelerate 300 mm transitions.

Other drivers and restraints analyzed in the detailed report include:

- Demand Spike from 800 V Vehicle Architectures

- Government On-Shoring Incentives for SiC Fabs

- Limited Ultra-Pure Feedstock Availability

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The greater than 99.99999% (7 N+) segment is poised for a 13.68% CAGR during the forecast period (2026-2031), eclipsing the greater than 99.9999% (6 N) tier that dominated 48.04% of Ultra High Purity Silicon Carbide market share in 2025. Demand comes from 1,200 V and 1,700 V automotive inverters and 3,300 V solar converters that mandate sub-1 ppb impurity levels. Infineon's CoolSiC Gen2 relies exclusively on 7N+ substrates, while Coherent rolled out thick-epitaxy 7N+ wafers aimed at 10 kV AI-datacenter power modules. Although 5N material maintains a niche in legacy LED and abrasive uses, device makers are locking in 7N+ supply contracts to future-proof high-voltage roadmaps.

Cost sensitivity keeps 6N substrates relevant for mainstream 650 V-1,200 V EV traction applications. ROHM's 5th-generation MOSFET achieves 1.0 mΩ on-resistance on a 7 mm X 7 mm die using 6N, satisfying thermal budgets up to 175°C. Long term, yield improvements and larger wafer diameters are expected to narrow the cost delta, accelerating 7N+ adoption even in mid-voltage classes.

Epitaxial 4-inch wafers still held 45.06% of the Ultra High Purity Silicon Carbide market size in 2025, but 6-inch and 8-inch formats are stealing share as capital budgets shift to 200 mm lines. Resonac's third-generation HGE-3G epi wafers entered mass production in 2023, and the firm shipped its first 200 mm volumes in 2025. Powder, primarily for abrasives and ceramics, remains a low-growth adjunct.

Bulk crystal output is forecast to grow at 13.92% as Integrated Device Manufacturers (IDMs) bring substrate fabrication in-house. STMicroelectronics' EUR 5 billion (USD 5.65 billion) Catania campus exemplifies the powder-to-module model, targeting 15,000 wafers per week by 2033. Denso's joint venture with Fuji Electric will supply 310,000 wafers annually to Toyota by 2027, underscoring OEM appetite for captive crystal capacity.

Geography Analysis

Asia-Pacific generated 52.67% of 2025 revenue and is on course for a 14.09% CAGR during the forecast period (2026-2031). Japan allocated JPY 350.3 billion (USD 2.4 billion) in subsidies to reinforce domestic SiC supply lines, and China's TankeBlue plus SICC jointly stepped up to a significant share of global substrate output by undercutting prices. South Korea aims for 20% SiC self-sufficiency, backstopping SK Siltron CSS with federal and Michigan incentives to multiply 200 mm capacity tenfold by 2027. India remains confined to device packaging, while Malaysia's Kulim hub hosts Infineon's scaling 200 mm fab.

North America benefits from the CHIPS Act's USD 750 million grant to Wolfspeed's Siler City plant, slated to triple domestic capacity by 2030. The United States held the largest share of global substrate production in 2025, but leads in 300 mm research and development. Canada and Mexico are minor assembly nodes. Onsemi's South Korea expansion services North American auto customers, reinforcing bilateral supply security.

Europe consolidates capacity via state-aided megaprojects. STMicroelectronics brought its EUR 5 billion (USD 5.65 billion) Catania campus online in 2025, and Infineon's Dresden Smart Power Fab received EUR 1 billion (USD 1.65 billion) in EU funds. Onsemi is building Europe's first fully integrated SiC line in the Czech Republic. ROHM's SiCrystal will triple its German capacity by 2027. The U.K. and France contribute design expertise but modest wafer volumes.

South America and the Middle East & Africa remain the lowest contributors, focused on downstream renewable projects rather than upstream substrate manufacturing. Brazil's EV programs import SiC devices, and the Middle East's 50 GW solar pipeline should lift inverter demand, but neither region has announced high-purity boule capacity.

- 5N Plus

- Coherent Corp.

- CoorsTek Inc.

- Entegris

- Fujimi Corporation

- Infineon Technologies AG

- Nippon Steel Corporation

- Resonac Holdings Corporation

- ROHM Co., Ltd.

- Semiconductor Components Industries, LLC

- SiCrystal GmbH

- SICC Co., Ltd.

- SK Siltron CSS

- STMicroelectronics

- TankeBlue Co., Ltd.

- Tokai Carbon Co., Ltd.

- Washington Mills

- Wolfspeed, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 EV traction inverters and on-board chargers

- 4.2.2 Grid-scale and C&I renewable inverters

- 4.2.3 Demand spike from 800 V vehicle architectures

- 4.2.4 Government on-shoring incentives for SiC wafer fabs

- 4.2.5 300 mm SiC boule breakthroughs lifting 7 N yield

- 4.3 Market Restraints

- 4.3.1 High purification and crystal-growth cost

- 4.3.2 Limited ultra-pure feed-stock availability

- 4.3.3 Wafer yield losses from basal-plane dislocations

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Purity Level

- 5.1.1 greater than 99.999% (5 N)

- 5.1.2 greater than 99.9999% (6 N)

- 5.1.3 greater than 99.99999% (7 N+)

- 5.2 By Form

- 5.2.1 Bulk Crystal

- 5.2.2 Epitaxial Wafer (4-inch)

- 5.2.3 Epitaxial Wafer (6- and 8-inch)

- 5.2.4 Powder

- 5.3 By Application

- 5.3.1 Power Electronics

- 5.3.2 Semiconductors (Discrete and IC)

- 5.3.3 LEDs and Optoelectronics

- 5.3.4 Photovoltaics

- 5.3.5 Advanced Ceramics and Others

- 5.4 By End-user Industry

- 5.4.1 Automotive

- 5.4.2 Renewable Energy

- 5.4.3 Telecommunications and 5G

- 5.4.4 Consumer Electronics

- 5.4.5 Defense and Aerospace

- 5.4.6 Industrial and Others

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 Japan

- 5.5.1.3 India

- 5.5.1.4 South Korea

- 5.5.1.5 ASEAN Countries

- 5.5.1.6 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 5N Plus

- 6.4.2 Coherent Corp.

- 6.4.3 CoorsTek Inc.

- 6.4.4 Entegris

- 6.4.5 Fujimi Corporation

- 6.4.6 Infineon Technologies AG

- 6.4.7 Nippon Steel Corporation

- 6.4.8 Resonac Holdings Corporation

- 6.4.9 ROHM Co., Ltd.

- 6.4.10 Semiconductor Components Industries, LLC

- 6.4.11 SiCrystal GmbH

- 6.4.12 SICC Co., Ltd.

- 6.4.13 SK Siltron CSS

- 6.4.14 STMicroelectronics

- 6.4.15 TankeBlue Co., Ltd.

- 6.4.16 Tokai Carbon Co., Ltd.

- 6.4.17 Washington Mills

- 6.4.18 Wolfspeed, Inc.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

碳化矽(SiC)塗層市場:依塗層類型、基材、應用、國家及地區分類-全球產業分析、市場規模、市場佔有率及2026年至2033年預測

碳化矽(SiC)塗層市場:依塗層類型、基材、應用、國家及地區分類-全球產業分析、市場規模、市場佔有率及2026年至2033年預測 碳化矽市場:2026-2032年全球市場預測(依產品類型、材料形態、裝置類型、晶圓尺寸、成型方法、應用及通路分類)

碳化矽市場:2026-2032年全球市場預測(依產品類型、材料形態、裝置類型、晶圓尺寸、成型方法、應用及通路分類) 碳化矽市場商業機會、成長要素、產業趨勢分析及2026-2035年預測碳化矽晶錠市場報告:趨勢、預測及競爭分析(至2035年)碳化矽錠市場報告:趨勢、預測及競爭分析(至2035年)

碳化矽市場商業機會、成長要素、產業趨勢分析及2026-2035年預測碳化矽晶錠市場報告:趨勢、預測及競爭分析(至2035年)碳化矽錠市場報告:趨勢、預測及競爭分析(至2035年) 2026-2030年全球碳化矽(SiC)市場

2026-2030年全球碳化矽(SiC)市場 碳化矽市場分析及預測(至2035年):依類型、產品類型、技術、零件、應用、形態、材料種類、裝置、製程及最終用戶分類

碳化矽市場分析及預測(至2035年):依類型、產品類型、技術、零件、應用、形態、材料種類、裝置、製程及最終用戶分類 碳化矽市場規模、佔有率、趨勢和預測:按產品、應用和地區分類,2026-2034年

碳化矽市場規模、佔有率、趨勢和預測:按產品、應用和地區分類,2026-2034年 碳化矽市場:依產品類型、最終用戶和地區分類LED用碳化矽載體市場:依產品類型、技術、額定功率、類型、裝置類型、應用、最終用戶分類,全球預測(2026-2032年)

碳化矽市場:依產品類型、最終用戶和地區分類LED用碳化矽載體市場:依產品類型、技術、額定功率、類型、裝置類型、應用、最終用戶分類,全球預測(2026-2032年)