|

市場調查報告書

商品編碼

2062310

南美洲BOPP薄膜:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)South America BOPP Films - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

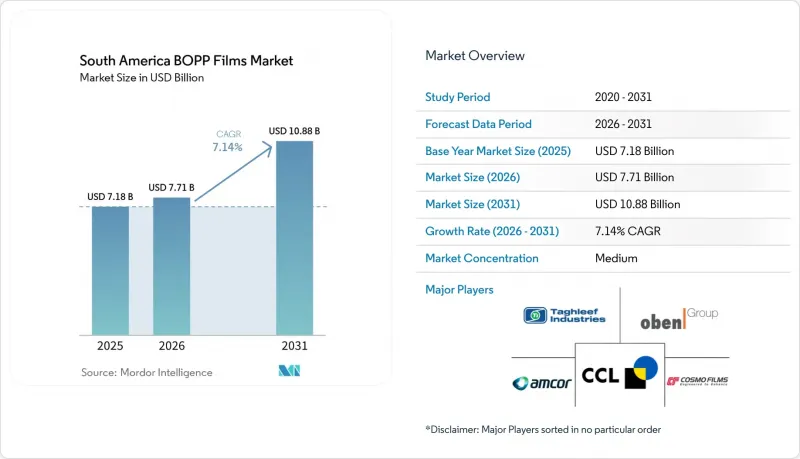

據 Mordor Intelligence 稱,2025 年南美 BOPP 薄膜市值為 71.8 億美元,預計到 2031 年將從 2026 年的 77.1 億美元成長至 108.8 億美元,預測期(2026-2031 年)的複合年成長率為 7.14%。

本報告按薄膜類型(透明、金屬化、白色/不透明/啞光等)、厚度(小於20微米、20-30微米、31-45微米等)、應用領域(食品包裝、煙草包裝、標籤和感壓膠帶等)、終端用戶行業(食品飲料、個人護理和化妝品、煙草等)以及地區進行細分。市場預測以美元計價。

南美洲雙向拉伸聚丙烯薄膜市場趨勢與洞察

食品零售業的快速成長推動了對高透明度軟質包裝的需求。

現代超級市場和便利商店連鎖店持續擴張,進駐巴西大都會圈以及阿根廷和哥倫比亞的區域性城市,為預包裝零食產品創造了更多貨架空間,而這些產品正是利用雙向拉伸聚丙烯(BOPP)的透明度和光澤度優勢而生的。購買已烹調烘焙食品和糖果甜點的消費者希望包裝盒能夠透過透明窗口展現產品新鮮度,同時又能有效阻隔水分,而拉伸聚丙烯(BOPP)恰好能夠輕鬆實現這一平衡。加工商正積極響應這一需求,對老舊生產線進行改造,升級出更先進的定位和厚度控制模組,從而在不影響剛性的前提下生產出更薄的薄膜。巴西一家名為Votorantim的大型生產線於2024年底完成升級,目前生產的高光澤度薄膜正逐漸成為高階餅乾包裝的熱門選擇。在秘魯和哥倫比亞內陸地區,由於都市區低溫運輸網路尚未完善,包裝的完整性仍然至關重要,這進一步推動了這些市場對高透明度薄膜的需求。

BOPP 是 PVC 和賽珞玢的經濟實惠的替代品。

由於巴西和智利監管機構對含氯聚合物的監管更加嚴格,加工商已將香菸包裝和糖果扭結包裝的材料從PVC轉向雙向拉伸聚丙烯(BOPP)。本地金屬化能力的提升、成本差異的縮小以及供應穩定性的增強,也促使BOPP在高階糖果甜點領域取代進口賽珞玢。由於金屬化BOPP是一種單一材料,因此使用後易於分離,這是聖保羅頒布的《生產者延伸責任法》的關鍵要求。 2026年3月雙向拉伸薄膜樹脂的現貨價格在每噸1453美元至1641美元之間,凸顯了BOPP相對於特種纖維素材料的成本優勢。隨著品牌所有者公佈其可回收性目標,預計所有形式的二次包裝都將進一步淘汰PVC。

聚丙烯樹脂價格波動劇烈

2025年第二季度,巴西聚丙烯(PP)現貨價格較上一季下降4%。這是由於亞洲供應過剩蔓延至當地經銷商,導致加工商現有薄膜訂單的利潤率承壓。價格波動使得與尋求穩定原料成本的食品品牌進行季度成本轉嫁談判變得更加複雜。據一位秘魯進口商稱,2025年5月PP交付價格下降了16.6%,但額外的運費和關稅抵消了部分節省。阿根廷貨幣走弱加劇了不不確定性,迫使一些製造商以美元對沖樹脂價格並提高庫存水準。由於金融機構在發放資金前尋求可預測的現金流,這些波動正在減緩產能擴張。

細分市場分析

透明級雙向拉伸聚丙烯薄膜(BOPP)預計將在2025年佔據南美BOPP薄膜市場43.63%的佔有率,是常溫零食和烘焙產品的主要包裝材料,這些產品需要良好的視覺透明度和較高的生產線速度。鍍金屬級BOPP薄膜作為一種可回收的鋁箔複合替代品,在提供與鋁箔複合薄膜相當的阻隔性能的同時,也獲得了品牌商的青睞,這得益於2024年下半年國內產能的提升。防霧級BOPP薄膜預計將以7.79%的複合年成長率成長,目前正擴大應用於從秘魯和智利沿海地區運往北美和亞洲的農產品包裝袋,因為這些地區濕度波動較大,更容易出現冷凝現象。

製造商正投資等離子和真空鍍膜設備,以打造耐油遷移的高價值表面。這對於巴西米納斯吉拉斯叢集出口的奶粉包裝袋至關重要。雖然白色和霧面薄膜屬於小眾市場,但在需要遮光性能的應用中,例如菸草包裝和高檔糖果甜點,它們卻能獲得溢價。這種差異化的產品組合使該綜合集團能夠規避通用透明薄膜需求的周期性下降,阿根廷和哥倫比亞的中型加工商也擴大效仿這一策略。

由於其在主流模塑-填充-封口 (FFS) 生產線中兼具剛性和良率,標準厚度為 20–30 微米的薄膜產品預計在 2025 年將佔據南美雙向拉伸聚丙烯 (BOPP) 薄膜市場 39.39% 的佔有率。厚度超過 45 微米的較厚基材預計將以 8.01% 的複合年成長率成長,用於生產酪梨、葡萄和水產品的真空包裝袋內襯,以應對冷藏運輸過程中可能發生的穿孔風險。厚度為 31–45微米的薄膜則用於中等重量的應用,例如零食包裝、飲料標籤和香菸包裝的重疊部分。

奧本集團最近在蒙特雷安裝了一條12米寬的生產線,運作為每分鐘700米,高效生產50微米厚的捲材,主要供應秘魯和智利的包裝廠出口。厚度小於20微米的薄膜則用於電商膠帶和環繞標籤,材料用量的減少直接轉化為運輸重量的降低。加工商正在權衡擴大生產線以生產更厚、速度更低的薄膜所需的資本投資成本,以及生鮮食品出口商對高阻隔阻隔性日益成長的需求所帶來的銷售成長。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 蓬勃發展的食品零售市場正在推動對高透明度軟質包裝的需求。

- 經濟實惠的BOPP替代品,可取代PVC和賽珞玢

- 電子商務的擴張正在推動對標籤和膠帶的需求。

- 品牌所有者向單一材料回收過渡

- 區域糖稅政策正在提振對金屬沉澱零食包裝的需求。

- 使用厚BOPP的農產品出口真空袋襯裡需求激增。

- 市場限制因素

- 聚丙烯樹脂的價格波動很大。

- 在阻隔性細分市場中與BOPET的競爭

- 巴西南部拉幅機架生產能力短缺

- 駕駛人長期罷工導致物流出現瓶頸。

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 按膠片類型

- 透明薄膜

- 金屬化薄膜

- 白色/不透明/霧面膜

- 防霧膜和其他功能膜

- 按厚度

- 小於20微米

- 20~30µm

- 31~45µm

- 45微米或更大

- 透過使用

- 食品包裝

- 糖果糕餅

- 小吃

- 麵包店

- 生鮮食品

- 飲料包裝

- 煙草包裝

- 標籤和感壓膠帶

- 工業及其他應用

- 食品包裝

- 按最終用戶行業分類

- 食品/飲料

- 個人護理化妝品

- 菸草

- 工業與物流

- 其他消費品

- 國家

- 巴西

- 阿根廷

- 哥倫比亞

- 智利

- 秘魯

- 其他南美國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Vitopel Group

- Oben Holding Group

- Amcor plc

- Taghleef Industries

- Polo Films

- Papion Flexible Films

- Polyplex Corporation Limited

- Braskem SA

- Mondi plc

- CCL Industries Inc.

- Jindal Poly Films Limited

- Cosmo Films Limited

第7章 市場機會與未來展望

According to Mordor Intelligence, the south america bOPP films market size was valued at USD 7.18 billion in 2025 and estimated to grow from USD 7.71 billion in 2026 to reach USD 10.88 billion by 2031, at a CAGR of 7.14% during the forecast period (2026-2031).

This report is Segmented by Film Type (Transparent, Metallized, White/Opaque/Matt, and More), Thickness (Below 20 Mm, 20-30 Mm, 31-45 Mm, and More), Application (Food Packaging, Tobacco Packaging, Labels and Pressure-Sensitive Tapes, and More), End-User Industry (Food and Beverage, Personal Care and Cosmetics, Tobacco, and More) and Geography. The Market Forecasts are Provided in Terms of Value (USD).

South America BOPP Films Market Trends and Insights

Food Retail Boom Pushing Demand for High-Clarity Flexible Packs

Modern supermarkets and convenience chains continue to spread across metropolitan Brazil and secondary cities in Argentina and Colombia, widening shelf space for portion-controlled snacks that benefit from BOPP's clarity and gloss. Consumers buying ready-to-eat bakery and confectionery products expect transparent windows that signal freshness while blocking moisture, a performance balance readily delivered by oriented polypropylene. Converters have responded by retrofitting older lines with enhanced pinning and thickness-control modules that allow down-gauging without sacrificing stiffness. Brazil's largest line upgrade at Votorantim, completed in late 2024, produced higher-gloss films that are now making inroads into premium cookie wraps. With urban cold-chain networks still nascent in Peru and interior Colombia, pack integrity remains critical, further lifting demand for high-clarity films in those markets.

Substitution of PVC and Cellophane with Cost-Efficient BOPP

Regulators in Brazil and Chile tightened rules on chlorine-containing polymers, spurring converters to transition tobacco overwraps and candy twists from PVC to BOPP. BOPP also displaced imported cellophane in premium confectionery as local metallization capacity rose, narrowing cost gaps and improving supply security. The mono-material nature of metalized BOPP aids post-consumer sorting, a key requirement under extended producer responsibility laws taking effect in Sao Paulo state. Recent spot resin quotes for bioriented film grades ranged between USD 1,453 and USD 1,641 per metric ton in March 2026, reinforcing BOPP's cost advantage over specialty cellulosics. As brand owners publicize recyclability targets, further PVC withdrawal is expected across secondary packaging formats.

Volatile Polypropylene Resin Pricing

Spot PP prices in Brazil fell 4% quarter over quarter in Q2 2025 as Asian oversupply reached local distributors, eroding converters' margins on previously contracted film orders. Fluctuations complicate quarterly pass-through negotiations with food brands that demand stable input costs. Importers in Peru reported a 16.6% decline in delivered PP values during May 2025, but additional freight and tariff surcharges offset part of the savings. Currency depreciation in Argentina adds another layer of unpredictability, forcing some makers to hedge resin prices in U.S. dollars and hold higher stock levels. These swings delay capacity expansions because financing institutions seek predictable cash flows before releasing capital.

Other drivers and restraints analyzed in the detailed report include:

- Rising E-Commerce Driving Demand for Label and Tape Films

- Brand Owners' Shift Toward Mono-Material Recyclability

- Competition from BOPET in High-Barrier Niches

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Transparent grades, accounting for 43.63% of the South America BOPP films market share in 2025, dominate shelf-stable snack and bakery wraps that demand aesthetic visibility and rapid line speeds. Metalized variants gained traction after domestic capacity rose in H2 2024, offering brand owners a recyclable alternative to foil laminates at comparable barrier levels. Anti-fog grades, projected to grow at a 7.79% CAGR, are gaining adoption in produce pouches shipped from Peru and Chile's coastal valleys to North America and Asia, where humidity swings can trigger condensation.

Producers invest in plasma and vacuum metallizers that unlock value-added surfaces resistant to grease migration, a priority for dairy powder sachets exported from Brazil's Minas Gerais cluster. White and matt films, although niche, command price premiums in tobacco overwraps and gourmet confectionery that rely on light protection. This differentiated mix allows integrated groups to hedge against cyclical declines in commodity clear films, a strategy increasingly copied by mid-tier converters across Argentina and Colombia.

Standard 20-30 µm products captured 39.39% of the South America BOPP films market size in 2025 because they balance stiffness and yield on mainstream form-fill-seal lines. Thicker substrates above 45 µm, forecast to rise at an 8.01% CAGR, underpin vacuum bag liners for avocados, grapes, and seafood that endure puncture risks during refrigerated transit. Films in the 31-45 micrometer band address mid-range applications, including snack packaging, beverage labels, and tobacco overwraps.

Oben Group's recent 12-meter-wide line in Monterrey runs at 700 m/min, enabling efficient production of 50 µm rolls targeted at export pack houses in Peru and Chile. Below-20 µm gauges are used in e-commerce tapes and wrap-around labels, where material reduction directly translates into lower shipping weight. Converters weigh the capital economics of stretching lines to run thicker films at slower speeds against the volume upside offered by fresh-produce exporters seeking robust barriers.

List of Companies Covered in this Report:

- Vitopel Group

- Oben Holding Group

- Amcor plc

- Taghleef Industries

- Polo Films

- Papion Flexible Films

- Polyplex Corporation Limited

- Braskem S.A.

- Mondi plc

- CCL Industries Inc.

- Jindal Poly Films Limited

- Cosmo Films Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Food Retail Boom Pushing Demand for High-Clarity Flexible Packs

- 4.2.2 Substitution of PVC and Cellophane with Cost-Efficient BOPP

- 4.2.3 Rising E-Commerce Driving Demand for Label and Tape Films

- 4.2.4 Brand Owners' Shift Toward Mono-Material Recyclability

- 4.2.5 Regional Sugar-Tax Policies Spurring Metallized Snack Packs

- 4.2.6 Surge in Agro-Export Vacuum-Bag Liners Using Thick BOPP

- 4.3 Market Restraints

- 4.3.1 Volatile Polypropylene Resin Pricing

- 4.3.2 Competition from BOPET in High-Barrier Niches

- 4.3.3 Limited Tenter-Frame Capacity South of Brazil

- 4.3.4 Extended Truck Strikes Causing Logistics Bottlenecks

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Industry Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Film Type

- 5.1.1 Transparent Films

- 5.1.2 Metallized Films

- 5.1.3 White / Opaque / Matt Films

- 5.1.4 Anti-Fog and Other Functional Films

- 5.2 By Thickness

- 5.2.1 Below 20 µm

- 5.2.2 20-30 µm

- 5.2.3 31-45 µm

- 5.2.4 Above 45 µm

- 5.3 By Application

- 5.3.1 Food Packaging

- 5.3.1.1 Confectionery

- 5.3.1.2 Snacks

- 5.3.1.3 Bakery

- 5.3.1.4 Fresh Produce

- 5.3.2 Beverage Packaging

- 5.3.3 Tobacco Packaging

- 5.3.4 Labels and Pressure-Sensitive Tapes

- 5.3.5 Industrial and Other Applications

- 5.3.1 Food Packaging

- 5.4 By End-User Industry

- 5.4.1 Food and Beverage

- 5.4.2 Personal Care and Cosmetics

- 5.4.3 Tobacco

- 5.4.4 Industrial and Logistics

- 5.4.5 Other Consumer Goods

- 5.5 By Country

- 5.5.1 Brazil

- 5.5.2 Argentina

- 5.5.3 Colombia

- 5.5.4 Chile

- 5.5.5 Peru

- 5.5.6 Rest of South America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Vitopel Group

- 6.4.2 Oben Holding Group

- 6.4.3 Amcor plc

- 6.4.4 Taghleef Industries

- 6.4.5 Polo Films

- 6.4.6 Papion Flexible Films

- 6.4.7 Polyplex Corporation Limited

- 6.4.8 Braskem S.A.

- 6.4.9 Mondi plc

- 6.4.10 CCL Industries Inc.

- 6.4.11 Jindal Poly Films Limited

- 6.4.12 Cosmo Films Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

BOPP薄膜市場規模、佔有率和趨勢分析報告:按類型、厚度、製造流程、應用、地區和細分市場預測(2026-2033年)

BOPP薄膜市場規模、佔有率和趨勢分析報告:按類型、厚度、製造流程、應用、地區和細分市場預測(2026-2033年) 雙向拉伸聚丙烯薄膜市場規模、佔有率、成長及全球產業分析:按類型、應用和地區的洞察,2026-2034年預測

雙向拉伸聚丙烯薄膜市場規模、佔有率、成長及全球產業分析:按類型、應用和地區的洞察,2026-2034年預測 2026-2034年BOPP薄膜市場規模、佔有率、趨勢及預測(按類型、厚度、製造流程、應用和地區分類)

2026-2034年BOPP薄膜市場規模、佔有率、趨勢及預測(按類型、厚度、製造流程、應用和地區分類) 雙向拉伸聚丙烯薄膜市場:市場規模-按地區、應用和至2034年的預測日本雙向拉伸聚丙烯薄膜市場規模、佔有率、趨勢及預測(按類型、厚度、製造流程、應用和地區分類),2026-2034年

雙向拉伸聚丙烯薄膜市場:市場規模-按地區、應用和至2034年的預測日本雙向拉伸聚丙烯薄膜市場規模、佔有率、趨勢及預測(按類型、厚度、製造流程、應用和地區分類),2026-2034年 BOPP 薄膜市場-全球產業規模、佔有率、趨勢、機會和預測,按類型、厚度、生產流程、應用、地區和競爭細分,2020-2030 年

BOPP 薄膜市場-全球產業規模、佔有率、趨勢、機會和預測,按類型、厚度、生產流程、應用、地區和競爭細分,2020-2030 年 雙向拉伸聚丙烯薄膜:市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030 年)

雙向拉伸聚丙烯薄膜:市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030 年) BOPP 薄膜市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測印度 BOPP 薄膜:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)

BOPP 薄膜市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測印度 BOPP 薄膜:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)