|

市場調查報告書

商品編碼

2062270

雲端財務營運:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)Cloud FinOps - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

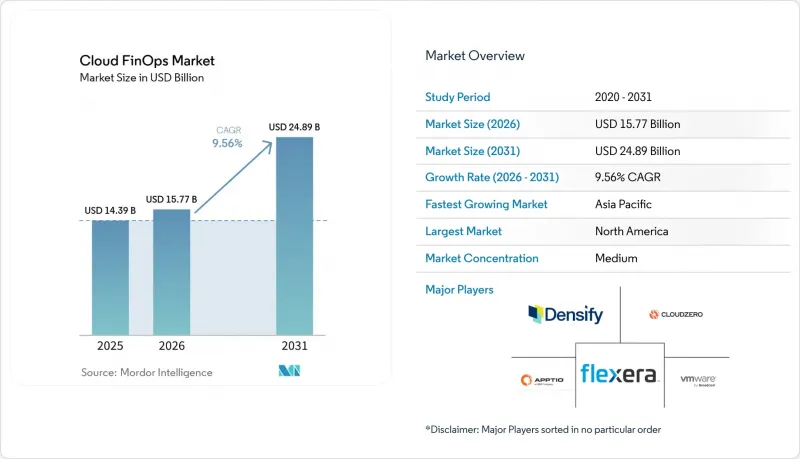

根據 Mordor Intelligence 預測,雲端 FinOps 市場規模將從 2025 年的 143.9 億美元和 2026 年的 157.7 億美元成長到 2031 年的 248.9 億美元,2026 年至 2031 年的年複合成長率(CAGR)為 9.56%。

本報告按組件(軟體、服務)、部署類型(公共雲端、私有雲端等)、組織規模(大型企業、中小企業)、最終用戶行業(IT與電信、銀行、金融服務與保險、零售與電子商務、醫療保健與生命科學等)以及地區進行細分。市場預測以價值(美元)表示。

全球雲端財務營運市場趨勢與洞察

多重雲端和混合雲端日益複雜,因此需要統一的成本管治。

在亞馬遜雲端服務 (AWS)、微軟 Azure 和谷歌雲端平台 (GCP) 上運行工作負載的組織面臨著許多挑戰,例如收費方案不相容、折扣邏輯分散以及標籤不一致。儘管 FinOps 開放成本和使用規範 (OCC) 正在推進資料標準化,超大規模資料中心業者服務商優先考慮的是自身供應商的鎖定,這促使企業採用編配平台來匯總支出、準確分配成本並執行全局策略。由於監管障礙要求準確扣回爭議帳款,金融服務和電信公司率先採用了這些平台。因此,統一管治是推動雲端 FinOps 市場成長的關鍵因素。

2024 年審計規則修訂後,財務長對雲端預算的監督義務。

隨著美國財務會計準則委員會 (FASB) 將多年期雲端合約歸類為經營租賃負債,雲端支出已成為財務長關注的關鍵問題。一項 2025 年的調查顯示,66% 的董事會將審查雲端預算,並且對符合審計標準的差異報告和情境建模的需求日益成長。在英國一家銀行的案例中,集中化財務營運 (FinOps) 節省了超過 380 萬英鎊(480 萬美元)的成本。這些監管因素正在加速雲端財務營運的普及,並增強市場信心。

認證的財務營運從業人員短缺阻礙了公司規模的擴大。

FinOps基金會頒發數千份認證,但需求遠超供應,尤其是在亞太和中東市場。企業需支付高額費用聘請外部顧問,這推高了專案成本,並延緩了從人工審核向自動化管治的過渡。中小企業受此影響最大,它們往往選擇僅限於購買預留實例等表面最佳化措施,而非進行進階的資源調整。因此,人才短缺限制了雲端FinOps市場的成長。

細分市場分析

到2025年,軟體將佔據雲端FinOps市場65.15%的主導佔有率,這反映出軟體在幫助企業有效管理雲端財務營運方面發揮著至關重要的作用。然而,服務業預計將以10.55%的複合年成長率穩定成長,這主要是由於企業內部缺乏專業知識。這一缺口為託管服務供應商帶來了商機,他們正日益將FinOps整合到更廣泛的數位轉型(DX)舉措中。同時,顧問公司也在透過組建內部團隊並實施有針對性的最佳化衝刺來滿足這項需求,從而提高營運效率。

中小企業 (SME) 通常更傾向於固定費率模式,這種模式可以消除基於支出的費用所帶來的不確定性。此類模式與成長型企業通常有限的預算非常契合,因此對這群人來說極具吸引力。在軟體方面,供應商不斷創新以增強其平台。具體而言,他們正在整合一些高級功能,例如利用人工智慧驅動的異常檢測來識別可疑活動,與 Terraform 整合以簡化基礎設施管理,以及碳排放預測以支援永續發展目標。這些增強功能不僅提升了平台的功能性,也提高了平台的採用率,並促進了客戶維繫。自動化和諮詢服務的結合創造了多層次的價值提案,吸引了眾多類型的組織。這種組合保持了雲端 FinOps 市場的強勁發展勢頭,確保其在日益雲主導的商業環境中持續成長並保持其重要性。

2025年,公共雲端支出將佔雲端總支出的46.45%。然而,混合雲和多重雲端環境正經歷顯著成長,年複合成長率高達11.34%,因為企業擴大採用這些模式來降低供應商鎖定帶來的風險。由於無法在不同供應商之間轉移預留實例折扣,導致承諾管理分散,並增加了雲端成本最佳化策略的複雜性。儘管公共雲端和混合雲端模式興起,但由於其合規性和安全性優勢,私有雲端在受監管行業仍然至關重要。

同時,FinOps 工具也在不斷發展,以實現一致的標籤和扣回爭議帳款策略,確保本地、邊緣和公共工作負載的統一性。儘管開放成本和使用規範 (OCUS) 旨在標準化跨平台的資料輸入,但其應用的不均衡性仍然推動了對第三方規範化引擎的需求,以簡化運維流程。雲端環境管理日益複雜的現狀正推動雲端 FinOps 市場走上快速且持續成長的道路。

區域分析

到2025年,北美將主導雲端FinOps市場,佔37.45%的營收佔有率。這一主導地位得益於超大規模資料中心業者的設立、FinOps基礎架構的早期應用以及豐富的人才儲備。該地區的董事會日益將雲端預算視為策略工具,加速了FinOps實踐的成熟。這些因素共同促成了北美在全球市場的重要地位,並為其他地區樹立了標竿。

歐洲緊隨其後,其中《企業永續發展報告指令》(CSRD) 在將綠色營運碳指標納入財務審查方面發揮了關鍵作用。這種整合使成本管理與ESG(環境、社會和管治)優先事項保持一致,反映出對永續發展的日益重視。同時,亞太地區成為成長最快的地區,年複合成長率高達12.21%。這一成長主要得益於中國、印度和韓國超大規模資料中心業者的擴張,以及在地化IT服務調整FinOps實踐以應對多語言計費複雜性。

在沙烏地阿拉伯和阿拉伯聯合大公國強制推行主權雲端政策的推動下,中東和非洲地區也呈現出強勁的發展勢頭,這刺激了對符合當地法規平台的需求。然而,該地區認證人員的短缺正在減緩這些措施的推進速度。在南美洲,市場仍處於起步階段,但巴西和阿根廷在金融營運(FinOps)實踐的採用方面處於領先地位,尤其是在電子商務和金融服務領域。這種地域分佈凸顯了雲端金融營運市場的全球崛起,並顯示其重要性日益增強,不受地域限制。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 市場定義與研究假設

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 多重雲端和混合雲端日益複雜,因此需要統一的成本管治。

- 2024 年審計規則修訂後,財務長對雲端預算的監督。

- GenAI 工作負載成本飆升,因此需要對單位經濟效益進行詳細追蹤。

- FinOps框架v4.0與超大規模資料中心業者的主流化

- 將碳排放意識強的綠色彙報整合到財務營運關鍵績效指標中

- 雲端原生 FinOps 即程式碼管道與 CI/CD 整合的興起

- 市場限制因素

- 認證的財務營運從業人員短缺阻礙了公司規模的擴大。

- 多樣化的收費API 和標籤標準使資料規範化變得複雜。

- 開發團隊對即時成本管理標準的抵制正在減緩自動化進程。

- 邊緣和主權雲端中的資料局部規則和可見性碎片化

- 產業價值/價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 宏觀經濟因素的影響

第5章 市場規模與成長預測

- 按組件

- 軟體

- 服務

- 依部署類型

- 公共雲端

- 私有雲端

- 混合/多重雲端

- 按組織規模

- 大公司

- 中小企業

- 按最終用戶行業分類

- IT/通訊

- 銀行業、金融服務業及保險業

- 零售與電子商務

- 醫療保健和生命科學

- 製造業

- 政府/公共部門

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲和紐西蘭

- 其他亞太國家

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 埃及

- 其他非洲國家

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Apptio, Inc.

- VMware, Inc.(Broadcom, Inc.)

- Flexera Software LLC

- CloudZero, Inc.

- Densify Inc.

- Harness Inc.

- Spot by NetApp, Inc.

- Microsoft Corporation(Azure Cost Management)

- Amazon Web Services, Inc.(AWS Cost Explorer)

- Google LLC(Cost Management Tools)

- Anodot Ltd.

- Turbonomic, Inc.(an IBM company)

- CloudBolt Software, Inc.

- Yotascale, Inc.

- Stackwatch, Inc.(Kubecost)

- ProsperOps, Inc.

- nOps, Inc.

- Granulate Cloud Solutions Ltd.(an Intel company)

- Finout Ltd.

- Zesty Tech Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the cloud FinOps market size is projected to expand from USD 15.77 billion in 2026 and USD 14.39 billion in 2025 to USD 24.89 billion by 2031, registering a CAGR of 9.56% between 2026 and 2031.

This report is Segmented by Component (Software, Services), Deployment Type (Public Cloud, Private Cloud, and More), Organization Size (Large Enterprises, Small and Medium Enterprises), End-User Industry (IT and Telecommunications, Banking Financial Services and Insurance, Retail and E-Commerce, Healthcare and Life Sciences, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Cloud FinOps Market Trends and Insights

Escalating Multi-Cloud and Hybrid-Cloud Complexity Requires Unified Cost Governance

Organizations running workloads across Amazon Web Services, Microsoft Azure, and Google Cloud Platform navigate incompatible billing schemas, fragmented discount logic, and inconsistent tagging. The FinOps Open Cost and Usage Specification is normalizing data, yet hyperscalers prioritize proprietary lock-in, so enterprises adopt orchestration platforms that aggregate spend, allocate costs accurately, and enforce global policies. Financial services and telecommunications firms are early adopters, given regulatory segmentation that mandates precise chargeback. Unified governance is therefore a pivotal growth catalyst for the cloud FinOps market.

Mandatory CFO Oversight of Cloud Budgets After 2024 Audit-Rule Updates

Financial Accounting Standards Board guidance now treats multiyear cloud commitments as operating-lease liabilities, elevating cloud spend to the CFO agenda. A 2025 survey showed 66% of boards review cloud budgets, driving demand for audit-grade variance reporting and scenario modeling. United Kingdom banking examples illustrate savings exceeding GBP 3.8 million (USD 4.8 million) after centralizing FinOps. This regulatory driver accelerates adoption, reinforcing the credibility of the cloud FinOps market.

Shortage of Certified FinOps Practitioners Limits Enterprise Scaling

The FinOps Foundation has issued thousands of certifications, yet demand outpaces supply, especially in Asia-Pacific and Middle East markets. Enterprises pay premiums for external consultants, increasing program costs and slowing the shift from manual reviews to automated governance. Small and medium enterprises feel the pinch most acutely, often accepting shallow optimization limited to reserved-instance purchases rather than advanced rightsizing. The talent gap therefore restrains the cloud FinOps market.

Other drivers and restraints analyzed in the detailed report include:

- GenAI Workload Cost Spikes Raise Urgency for Granular Unit-Economics Tracking

- Mainstream Adoption of FinOps Framework v4.0 by Hyperscalers

- Disparate Billing APIs and Tagging Standards Complicate Data Normalization

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, software held a dominant 65.15% share of the cloud FinOps market, reflecting its critical role in enabling organizations to manage cloud financial operations effectively. However, services are projected to experience significant growth, with a robust 10.55% CAGR, driven largely by the lack of in-house expertise within organizations. This gap has created opportunities for managed-service providers, who are increasingly integrating FinOps into broader digital transformation initiatives. At the same time, consultancies are stepping in to address this need by training internal teams and executing targeted optimization sprints to enhance operational efficiency.

Small and medium enterprises (SMEs) are showing a preference for flat-fee pricing models, which eliminate the unpredictability of percentage-of-spend fees. These models align well with the constrained budgets typical of growth-stage businesses, making them an attractive option for this segment. On the software side, vendors are continuously innovating to strengthen their platforms. They are incorporating advanced features such as AI-driven anomaly detection to identify irregularities, Terraform integration to streamline infrastructure management, and carbon forecasting to support sustainability goals. These enhancements not only improve functionality but also increase platform stickiness, encouraging long-term customer retention. The interplay between automation and advisory services is creating a layered value proposition that appeals to a wide range of organizations. This combination sustains the momentum of the cloud FinOps market, ensuring its continued growth and relevance in an increasingly cloud-driven business environment.

In 2025, public cloud spending accounted for 46.45% of the total cloud expenditure. However, hybrid and multi-cloud estates are witnessing significant growth, expanding at an 11.34% CAGR as companies increasingly adopt these models to mitigate the risks associated with vendor lock-in. The inability to transfer reserved-instance discounts across providers has resulted in fragmented commitment management, adding complexity to cloud cost optimization strategies. Despite the rise of public and hybrid cloud models, private cloud remains a critical component in regulated sectors due to its compliance and security advantages.

Meanwhile, FinOps tools are evolving to implement consistent tagging and chargeback policies, ensuring uniformity across on-premises, edge, and public workloads. The Open Cost and Usage Specification seeks to standardize data inputs across platforms, but inconsistent adoption has underscored the continued demand for third-party normalization engines to streamline operations. This growing complexity in managing cloud environments is driving the cloud FinOps market to experience a steep and sustained growth trajectory.

Geography Analysis

In 2025, North America dominated the cloud FinOps market, accounting for 37.45% of the revenue share. This leadership was driven by the presence of hyperscaler headquarters, early adoption of the FinOps Foundation, and a deep talent pool. Boards across the region increasingly treat cloud budgets as strategic levers, accelerating the maturity of FinOps practices. These factors collectively position North America as a key player in the global market, setting benchmarks for other regions to follow.

Europe followed closely, where the Corporate Sustainability Reporting Directive played a pivotal role by incorporating GreenOps carbon metrics into financial reviews. This integration aligns cost management with ESG (Environmental, Social, and Governance) priorities, reflecting a growing emphasis on sustainability. Meanwhile, Asia-Pacific emerged as the fastest-growing region, with a remarkable 12.21% CAGR. The region's growth is anchored by the expansion of hyperscalers in China, India, and Korea, alongside localized IT services that adapt FinOps practices to address multilingual billing complexities.

The Middle East and Africa also witnessed momentum, driven by sovereign-cloud mandates in Saudi Arabia and the UAE, which spurred demand for platforms compliant with national regulations. However, the scarcity of certified talent in the region has slowed the pace of scaling these initiatives. In South America, the market remains in its emerging phase, with Brazil and Argentina leading the adoption of FinOps practices, particularly in the e-commerce and financial services sectors. This diverse geographic spread highlights the global rise of the cloud FinOps market, showcasing its growing importance across regions.

- Apptio, Inc.

- VMware, Inc. (Broadcom, Inc.)

- Flexera Software LLC

- CloudZero, Inc.

- Densify Inc.

- Harness Inc.

- Spot by NetApp, Inc.

- Microsoft Corporation (Azure Cost Management)

- Amazon Web Services, Inc. (AWS Cost Explorer)

- Google LLC (Cost Management Tools)

- Anodot Ltd.

- Turbonomic, Inc. (an IBM company)

- CloudBolt Software, Inc.

- Yotascale, Inc.

- Stackwatch, Inc. (Kubecost)

- ProsperOps, Inc.

- nOps, Inc.

- Granulate Cloud Solutions Ltd. (an Intel company)

- Finout Ltd.

- Zesty Tech Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Market Definition and Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Escalating Multi-Cloud and Hybrid-Cloud Complexity Requires Unified Cost Governance

- 4.2.2 Mandatory CFO Oversight of Cloud Budgets After 2024 Audit-Rule Updates

- 4.2.3 GenAI Workload Cost Spikes Raise Urgency for Granular Unit-Economics Tracking

- 4.2.4 Mainstream Adoption of FinOps Framework v4.0 by Hyperscalers

- 4.2.5 Carbon-Aware-GreenOps-Reporting Embedded in FinOps KPIs

- 4.2.6 Rise of Cloud-Native FinOps-as-Code Pipelines Integrated in CI/CD

- 4.3 Market Restraints

- 4.3.1 Shortage of Certified FinOps Practitioners Limits Enterprise Scaling

- 4.3.2 Disparate Billing APIs and Tagging Standards Complicate Data Normalization

- 4.3.3 Resistance from Dev Teams to Real-Time Cost Guardrails Slows Automation

- 4.3.4 Edge and Sovereign-Cloud Data-Locality Rules Fragment Visibility

- 4.4 Industry Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment Type

- 5.2.1 Public Cloud

- 5.2.2 Private Cloud

- 5.2.3 Hybrid / Multi-Cloud

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises (SMEs)

- 5.4 By End-User Industry

- 5.4.1 IT and Telecommunications

- 5.4.2 Banking, Financial Services and Insurance

- 5.4.3 Retail and E-Commerce

- 5.4.4 Healthcare and Life Sciences

- 5.4.5 Manufacturing

- 5.4.6 Government and Public Sector

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Egypt

- 5.5.5.2.4 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Apptio, Inc.

- 6.4.2 VMware, Inc. (Broadcom, Inc.)

- 6.4.3 Flexera Software LLC

- 6.4.4 CloudZero, Inc.

- 6.4.5 Densify Inc.

- 6.4.6 Harness Inc.

- 6.4.7 Spot by NetApp, Inc.

- 6.4.8 Microsoft Corporation (Azure Cost Management)

- 6.4.9 Amazon Web Services, Inc. (AWS Cost Explorer)

- 6.4.10 Google LLC (Cost Management Tools)

- 6.4.11 Anodot Ltd.

- 6.4.12 Turbonomic, Inc. (an IBM company)

- 6.4.13 CloudBolt Software, Inc.

- 6.4.14 Yotascale, Inc.

- 6.4.15 Stackwatch, Inc. (Kubecost)

- 6.4.16 ProsperOps, Inc.

- 6.4.17 nOps, Inc.

- 6.4.18 Granulate Cloud Solutions Ltd. (an Intel company)

- 6.4.19 Finout Ltd.

- 6.4.20 Zesty Tech Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

雲端財務運維最佳化市場預測至2034年:按組件、部署類型、企業規模、最終用戶和地區分類的全球分析

雲端財務運維最佳化市場預測至2034年:按組件、部署類型、企業規模、最終用戶和地區分類的全球分析 雲端財務維運市場規模、佔有率和成長分析:按解決方案類型、部署模式、雲端類型、組織規模、最終用戶產業、銷售管道和地區分類-2026-2033年產業預測

雲端財務維運市場規模、佔有率和成長分析:按解決方案類型、部署模式、雲端類型、組織規模、最終用戶產業、銷售管道和地區分類-2026-2033年產業預測 雲端財務維運市場:2026-2032年全球市場預測(依服務產品、組織規模、服務供應商類型、部署模式及產業分類)

雲端財務維運市場:2026-2032年全球市場預測(依服務產品、組織規模、服務供應商類型、部署模式及產業分類) 2026-2030年全球雲端FinOps市場

2026-2030年全球雲端FinOps市場 全球雲端金融維運市場依產品、用途/功能、部署、服務模式、組織規模、垂直產業和地區分類-預測至2030年

全球雲端金融維運市場依產品、用途/功能、部署、服務模式、組織規模、垂直產業和地區分類-預測至2030年 全球雲端金融營運市場

全球雲端金融營運市場 雲端金融營運市場 - 全球產業規模、佔有率、趨勢、機會和預測(按產品、部署類型、垂直產業、地區和競爭情況,2020-2030 年預測)

雲端金融營運市場 - 全球產業規模、佔有率、趨勢、機會和預測(按產品、部署類型、垂直產業、地區和競爭情況,2020-2030 年預測) 雲端金融營運市場規模、佔有率、趨勢分析報告:按組件、應用、部署類型、組織模式、最終用途、地區和細分市場預測,2025 年至 2033 年

雲端金融營運市場規模、佔有率、趨勢分析報告:按組件、應用、部署類型、組織模式、最終用途、地區和細分市場預測,2025 年至 2033 年 雲端金融營運市場、規模、趨勢和行業分析報告:按產品、服務模式、部署、組織規模、應用、垂直和地區 - 市場預測,2025-2034 年

雲端金融營運市場、規模、趨勢和行業分析報告:按產品、服務模式、部署、組織規模、應用、垂直和地區 - 市場預測,2025-2034 年 2024 - 2032 年雲端 FinOps 市場機會、成長促進因素、產業趨勢分析與預測

2024 - 2032 年雲端 FinOps 市場機會、成長促進因素、產業趨勢分析與預測