|

市場調查報告書

商品編碼

2062266

建築用矽酮密封膠:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)Construction Silicone Sealant - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

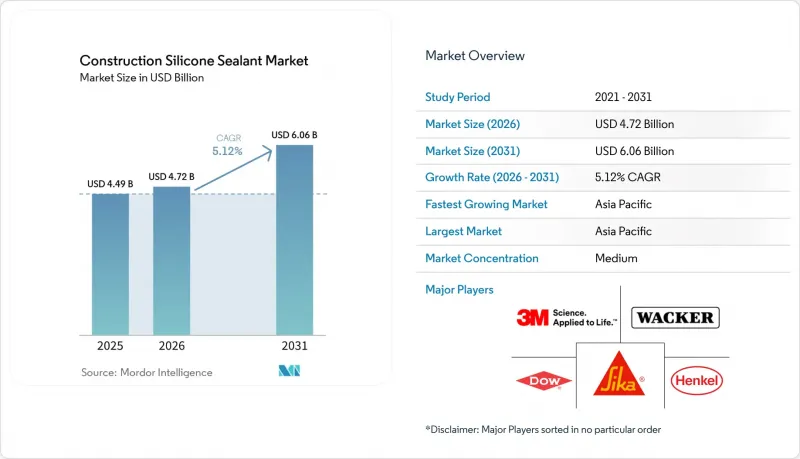

據 Mordor Intelligence 稱,建築矽酮密封膠市場預計將從 2025 年的 44.9 億美元成長到 2026 年的 47.2 億美元,到 2031 年達到 60.6 億美元,預計 2026 年至 2031 年的複合年成長率為 5.12%。

本報告按產品類型(中性固化矽酮密封膠、醋酸固化矽酮密封膠等)、應用領域(接縫填充、玻璃安裝、防水等)、最終用戶(住宅建築等)和地區(亞太地區、北美地區、歐洲地區、南美地區、中東和非洲地區)進行細分。市場預測以美元計價。

全球矽酮密封膠市場趨勢及建築業洞察。

住宅和商業建築的需求不斷成長

預計2026年,美國新建辦公大樓內裝成本將達到每平方英尺149美元,較2025年成長5.5%。這一成長促使開發商採用更耐用的密封劑以減少維護頻率。在中國,強制預製化正推動高伸縮縫的製造轉向工廠化生產,而工廠化生產主要使用中性固化矽酮。亞洲主要城市的住宅傾向於選擇低氣味產品,以防止基材變色,而低成本丙烯酸產品通常不具備此特性。由於勞動市場緊張,專案經理不僅關注材料成本,也關注總安裝成本。這些因素共同提升了矽酮在高階住宅大樓和甲級商業空間的地位。

新興國家的基礎建設熱潮

印度諾伊達國際機場和德里地鐵五期(A)工程項目,土木工程支出超過27億美元,需要經認證的密封膠,能夠承受±25%的膨脹和收縮,並具有卓越的防火性能。同樣,沙烏地阿拉伯薩勒曼國王國際機場和杜拜阿勒馬克圖姆機場的擴建計畫(總合超過640億美元)也需要耐紫外線、耐沙的矽酮接合材料,以應對嚴酷的沙漠環境。這些大型專案為能夠確保批次間一致性並提供現場技術支援的供應商提供了多年的商機。此外,較長的設計前置作業時間也有利於製造商,他們可以透過垂直整合和簽訂長期金屬矽合約來降低原料價格波動的風險。

矽酮和添加劑原料價格的波動

2026年第一季,受中國氯鹼工廠停產和矽金屬關稅上調的影響,二甲基二氯矽烷價格年增28%。此次價格上漲對依賴現貨市場採購的製劑生產商造成了衝擊。此外,2025年下半年氣相前置作業時間供不應求,導致交貨週期從四週延長至十二週。雖然這種情況有利於垂直整合型企業,但卻為小批量代工生產商帶來了挑戰。為因應這些市場狀況,瓦克公司於2026年4月宣布漲價約5%。同時,陶氏公司將矽氧烷的生產從高成本的歐洲轉移到其他地區,以保持競爭力。這些市場動態為專案預算帶來了不確定性,並可能導致在專案規格允許的情況下,轉向使用更具成本效益的化學品。

細分市場分析

到2025年,中性固化型產品將佔據建築矽酮密封膠市場44.11%的佔有率,這主要得益於其與陽極氧化鋁、鍍膜玻璃和天然石材的良好相容性。同時,受東南亞和拉丁美洲住宅的推動,醋酸固化型產品市場預計到2031年將以5.66%的複合年成長率成長,這些建築商更傾向於快速濕氣固化且單位成本降低30-40%的產品。肟基和烷氧基密封膠則佔據了更細分的市場,滿足了諸如飲用水系統和汽車彈性體黏合等特定需求。高階市場,例如計劃於2025年推出的Momentive生物基室溫硫化(RTV)產品線,正在不斷發展以滿足產品隱含碳取證要求。這種對檢驗的永續性的追求旨在遏制醋酸固化型產品在主流玻璃應用領域的成長。

產品組合的這些變化凸顯了價格分層而非直接取代。陶氏化學的DOWSIL 791是一種廣泛使用的乙醯氧基產品,在東南亞的窗框安裝中佔比超過一半,這反映了大規模住宅中注重成本的決策。同時,瓦克化學的烷氧基固化型ELASTOSIL A07符合美國食品藥物管理局(FDA)《聯邦法規彙編》(CFR)第21篇第177.2600節的衛生標準,確保了其在食品加工無塵室的需求。此外,肟基固化型產品因其對機器人擠出成型的多孔基材具有優異的黏合性,在3D列印混凝土外牆領域也備受關注。隨著建築規範根據具體應用場景而日益多樣化,預計單一的化學技術不會主導所有細分市場,因此多元化產品組合的重要性不言而喻。

區域分析

預計到2025年,亞太地區將佔全球建築矽酮密封膠銷售額的46.78%,並繼續保持主導地位,到2031年將以6.11%的複合年成長率成長。中國對預製建築的重視以及印度航空航太業的擴張正在推動穩定的需求,其中沿海省份佔國內密封膠消費量的40%以上。擁有本地混合廠的區域製造商享有前置作業時間短、在國家項目中享有優先待遇等優勢,這對依賴進口的競爭對手構成了挑戰。

在北美,將辦公空間改建為住宅的趨勢日益明顯,正在改變城市面貌。預計到2025年,空置率將有所改善,而不斷上漲的室內裝修成本也推動了對高品質、耐用材料的需求,這些材料可以減少頻繁重新密封的需要。此外,聯邦政府針對政府建築的能源性能法規也促使維修投資轉向高性能矽酮接縫密封劑,從而確保即使新房開工量保持平穩,市場需求也能保持穩定。

在歐洲,法規結構的角色比新建設更為顯著。 《企業永續發展報告指令》(CSRD) 和《建築能源效能指令》(EPBD) 正在推動採購低揮發性有機化合物 (VOC) 和碳認證產品,而擁有可追溯供應鏈的供應商則獲得了價格優勢。儘管宏觀經濟成長依然緩慢,但老舊公共住宅的維修正在增加對覆材和隔熱材料接縫材料的需求。南美洲以及中東和非洲地區正呈現快速成長,儘管市場規模較小。預計杜拜阿勒馬克圖姆機場和利雅德薩勒曼國王機場等機場將使用數百萬公尺專為乾燥氣候設計的抗紫外線密封膠。 NEOM 的鏡面帷幕牆提出了新的技術要求,例如在 45°C 的環境溫度下保持抗沙蝕性和光學清晰度。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 住宅和商業建築需求增加

- 在綠色建築和永續建築領域中得到更廣泛的應用

- 新興國家的基礎建設熱潮

- 矽酮密封膠具有優異的耐候性和耐久性

- 在3D列印建築外觀中採用高延展性密封劑

- 市場限制因素

- 矽酮和添加劑原料價格的波動

- 丙烯酸、聚硫化物和聚氨酯的替代品

- 對揮發性有機化合物和錫基催化劑配方的監管壓力

- 價值鏈分析

- 波特五力模型

第5章 市場規模與成長預測

- 依產品類型

- 中性固化矽酮密封膠

- 醋酸固化矽酮密封劑

- 肟固化矽酮密封劑

- 烷氧基固化矽酮密封膠

- 透過使用

- 接縫密封(伸縮縫和移動縫)

- 玻璃和防水

- 隔熱材料和覆材

- 廚房和衛生設施

- 防火應用

- 其他用途(隔音、電機工程等)

- 最終用戶

- 住宅

- 商業建築

- 工業建築

- 基礎建設(橋樑、道路、機場)

- 按地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 東南亞國協

- 其他亞太國家

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 其他中東和非洲國家

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- 3M

- Arkema

- Beijing Zhongtian

- CHEMENCE

- Dow

- HB Fuller Company

- Henkel AG and Co. KGaA

- Mapei

- Momentive

- Pecora Corporation

- Pidilite Industries Ltd.

- RPM International, Inc.

- Shin-Etsu Chemical Co., Ltd.

- Sika AG

- Soudal Group

- Tremco

- Wacker Chemie AG

第7章 市場機會與未來展望

According to Mordor Intelligence, the construction silicone sealant market size is expected to increase from USD 4.49 billion in 2025 to USD 4.72 billion in 2026 and reach USD 6.06 billion by 2031, growing at a CAGR of 5.12% over 2026-2031.

This report is Segmented by Product Type (Neutral-Cure Silicone Sealants, Acetoxy-Cure Silicone Sealants, and More), Application (Joint Sealing, Glazing and Weatherproofing, and More), End-User (Residential Construction and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Construction Silicone Sealant Market Trends and Insights

Rising Demand from Residential and Commercial Construction

In 2026, new office fit-out costs in the United States reached USD 149 per square foot, reflecting a 5.5% increase from 2025. This rise is driving developers to adopt longer-life sealants to reduce maintenance schedules. In China, prefabrication mandates are directing high-movement joints into factory environments, where neutral-cure silicones are predominantly used. Homeowners in tier-1 Asian cities are selecting low-odor products that resist substrate staining, a feature not commonly found in lower-cost acrylics. As labor markets tighten, project managers are focusing on total installed costs rather than just material prices. These factors collectively enhance silicone's positioning in premium residential towers and Grade-A commercial spaces.

Infrastructure Boom in Emerging Economies

India's Noida International Airport and Delhi Metro Phase V(A) represent a combined civil expenditure exceeding USD 2.7 billion, requiring sealants certified for +-25% movement and higher fire ratings. Similarly, expansions at Saudi Arabia's King Salman International and Dubai's Al Maktoum airports, with a combined value exceeding USD 64 billion, demand UV-stable, sand-resistant silicone joints to withstand extreme desert conditions. These large-scale projects provide multi-year opportunities for suppliers capable of ensuring batch consistency and offering on-site technical support. Additionally, extended design lead times benefit manufacturers that mitigate raw-material price volatility through backward integration or long-term silicon-metal contracts.

Volatility in Silicone and Additive Raw-Material Prices

In Q1 2026, prices for Dimethyldichlorosilane increased by 28% year-on-year, driven by outages at Chinese chlor-alkali units and higher tariffs on silicon metal. This price rise has impacted formulators reliant on spot market purchases. Additionally, shortages in fumed silica extended lead times from four to twelve weeks in late 2025. This situation benefited vertically integrated companies while creating challenges for small-batch contractors. In response to these market conditions, Wacker announced a mid-single-digit price increase in April 2026. Concurrently, Dow shifted its siloxane production from high-cost Europe to other regions to maintain competitiveness. These market dynamics introduce uncertainties in project budgeting and may lead to a shift toward more cost-effective chemistries when project specifications allow.

Other drivers and restraints analyzed in the detailed report include:

- Growing Use in Green Buildings and Sustainable Architecture

- Surge in Unitized Curtain-Wall Adoption (High-Movement Joints)

- Competition from Acrylic, Polyurethane, and Polysulfide Substitutes

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, neutral-cure products accounted for 44.11% of the construction silicone sealant market, supported by their compatibility with anodized aluminum, coated glass, and natural stone. Meanwhile, the market for acetoxy-cure grades is projected to grow at a 5.66% compound annual growth rate (CAGR) through 2031, driven by residential builders in Southeast Asia and Latin America who prefer the rapid moisture cure and a 30-40% lower unit cost. Oxime- and alkoxy-cure chemistries occupy smaller niches, catering to specialized needs like potable-water systems and automotive elastomer bonding. Premium tiers, exemplified by Momentive's 2025 bio-attributed room-temperature vulcanizing (RTV) range, are evolving to meet embodied-carbon disclosure demands. This competitive shift towards verified sustainability aims to address acetoxy-cure's growth in mainstream glazing applications.

The evolving product mix highlights a pricing hierarchy rather than a direct substitution. Dow's DOWSIL 791, a widely used acetoxy product, dominates over half of Southeast Asia's window-perimeter installations, reflecting cost-driven decisions in mass housing. On the other hand, Wacker's alkoxy-cure ELASTOSIL A07, compliant with Food and Drug Administration (FDA) 21 Code of Federal Regulations (CFR) 177.2600 sanitization standards, secures demand from food-processing cleanrooms. Additionally, oxime-cure products are gaining traction in 3D-printed concrete facades due to their superior adhesion on porous substrates crafted through robotic extrusion. As building codes diversify based on specific use cases, no single chemistry is expected to dominate all niches, ensuring the relevance of multigrade portfolios.

Geography Analysis

In 2025, the Asia-Pacific region accounted for 46.78% of global revenue and is projected to grow at a 6.11% compound annual growth rate (CAGR) through 2031, maintaining its leadership in the construction silicone sealant market. China's focus on prefabrication and India's expanding aviation sector indicate consistent demand, with coastal provinces consuming over 40% of the nation's sealants. Regional producers with local mixing plants benefit from shorter lead times and preferred status in state projects, creating challenges for import-dependent competitors.

North America is experiencing a shift as office spaces convert to residential use, altering urban landscapes. Vacancy rates improved in 2025, and rising fit-out costs have driven demand for premium, durable materials, reducing the need for frequent resealing. Additionally, federal energy performance mandates for government buildings are directing retrofit investments into high-performance silicone joints, ensuring stable demand even as new construction levels off.

In Europe, regulatory frameworks play a more significant role than new construction. The Corporate Sustainability Reporting Directive (CSRD) and the Energy Performance of Buildings Directive (EPBD) are driving procurement toward low-volatile organic compound (VOC), carbon-verified products, while suppliers with traceable supply chains gain pricing advantages. Although macroeconomic growth remains slow, retrofitting aging social housing is increasing demand for cladding and insulation joints. South America and the Middle East-Africa, while smaller markets, are showing rapid growth. Airports such as Dubai's Al Maktoum and Riyadh's King Salman are expected to utilize millions of linear meters of UV-stable sealants designed for arid climates. NEOM's mirrored facades are setting new technical requirements, including sand-erosion resistance and optical clarity at ambient temperatures of 45 °C.

- 3M

- Arkema

- Beijing Zhongtian

- CHEMENCE

- Dow

- H.B. Fuller Company

- Henkel AG and Co. KGaA

- Mapei

- Momentive

- Pecora Corporation

- Pidilite Industries Ltd.

- RPM International, Inc.

- Shin-Etsu Chemical Co., Ltd.

- Sika AG

- Soudal Group

- Tremco

- Wacker Chemie AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Demand From Residential and Commercial Construction

- 4.2.2 Growing Use in Green Buildings and Sustainable Architecture

- 4.2.3 Infrastructure Boom in Emerging Economies

- 4.2.4 Excellent Weatherability and Durability of Silicone Sealants

- 4.2.5 Adoption of High-movement Sealants for 3-D-printed Building Facades

- 4.3 Market Restraints

- 4.3.1 Volatility in Silicone and Additive Raw-material Prices

- 4.3.2 Availability of Acrylic, Polysulfide, and Polyurethane Substitutes

- 4.3.3 Regulatory Pressure on VOC and Tin-catalyst Formulations

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Neutral-cure silicone sealants

- 5.1.2 Acetoxy-cure silicone sealants

- 5.1.3 Oxime-cure silicone sealants

- 5.1.4 Alkoxy-cure silicone sealants

- 5.2 By Application

- 5.2.1 Joint sealing (expansion and movement joints)

- 5.2.2 Glazing and weatherproofing

- 5.2.3 Insulation and cladding

- 5.2.4 Kitchen and sanitary

- 5.2.5 Fire-resistant applications

- 5.2.6 Other Applications (sound-proofing, electrical, etc.)

- 5.3 By End-user

- 5.3.1 Residential construction

- 5.3.2 Commercial construction

- 5.3.3 Industrial construction

- 5.3.4 Infrastructure (bridges, roads, airports)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 Japan

- 5.4.1.3 India

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 South Africa

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 3M

- 6.4.2 Arkema

- 6.4.3 Beijing Zhongtian

- 6.4.4 CHEMENCE

- 6.4.5 Dow

- 6.4.6 H.B. Fuller Company

- 6.4.7 Henkel AG and Co. KGaA

- 6.4.8 Mapei

- 6.4.9 Momentive

- 6.4.10 Pecora Corporation

- 6.4.11 Pidilite Industries Ltd.

- 6.4.12 RPM International, Inc.

- 6.4.13 Shin-Etsu Chemical Co., Ltd.

- 6.4.14 Sika AG

- 6.4.15 Soudal Group

- 6.4.16 Tremco

- 6.4.17 Wacker Chemie AG

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

- 7.2 Growth Potential in Prefabricated and Modular Construction

填縫劑、水泥漿和接縫填充材料市場:按產品類型、化學類型、形態、應用和最終用戶分類-2026-2032年全球市場預測建築用矽酮密封膠市場:依最終用途、技術、包裝、應用及分銷通路分類-2026-2032年全球市場預測

填縫劑、水泥漿和接縫填充材料市場:按產品類型、化學類型、形態、應用和最終用戶分類-2026-2032年全球市場預測建築用矽酮密封膠市場:依最終用途、技術、包裝、應用及分銷通路分類-2026-2032年全球市場預測 全球矽酮密封膠市場規模、佔有率、趨勢和成長分析報告(2026-2034年)矽酮玻璃密封膠市場:依化學成分、組成數量、包裝、最終用途及銷售管道,全球預測(2026-2032年)全球流動性矽酮密封膠市場(按固化類型、產品形式、最終用途產業和分銷管道分類)預測(2026-2032年)醋酸固化矽酮密封膠市場:依產品等級、顏色、固化速度、耐熱性、應用及最終用途產業分類-2026年至2032年全球預測

全球矽酮密封膠市場規模、佔有率、趨勢和成長分析報告(2026-2034年)矽酮玻璃密封膠市場:依化學成分、組成數量、包裝、最終用途及銷售管道,全球預測(2026-2032年)全球流動性矽酮密封膠市場(按固化類型、產品形式、最終用途產業和分銷管道分類)預測(2026-2032年)醋酸固化矽酮密封膠市場:依產品等級、顏色、固化速度、耐熱性、應用及最終用途產業分類-2026年至2032年全球預測 矽酮密封膠市場規模、佔有率及成長分析(按產品、應用及地區分類)-2026-2033年產業預測

矽酮密封膠市場規模、佔有率及成長分析(按產品、應用及地區分類)-2026-2033年產業預測 美國建築用矽酮密封膠市場規模、佔有率和趨勢分析報告:按行業、應用、地區和細分市場預測(2026-2033 年)

美國建築用矽酮密封膠市場規模、佔有率和趨勢分析報告:按行業、應用、地區和細分市場預測(2026-2033 年) 矽酮密封膠市場-全球產業規模、佔有率、趨勢、機會與預測,按技術、應用、地區和競爭細分,2020-2030 年

矽酮密封膠市場-全球產業規模、佔有率、趨勢、機會與預測,按技術、應用、地區和競爭細分,2020-2030 年 全球矽膠黏合劑市場需求、預測分析(2018-2034)

全球矽膠黏合劑市場需求、預測分析(2018-2034)