|

市場調查報告書

商品編碼

2062217

水合物抑制劑:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Hydrate Inhibitors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

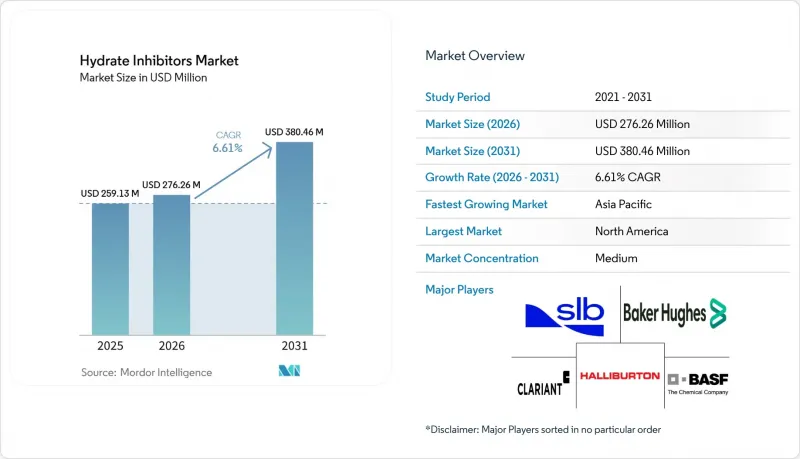

據 Mordor Intelligence 稱,水合物抑制劑市場預計將從 2025 年的 2.5913 億美元成長到 2026 年的 2.7626 億美元,到 2031 年達到 3.8046 億美元,預計 2026 年至 2031 年的複合成長率 6.61%。

本報告按類型(動態水合物抑制劑等)、形態(液體/固體)、應用(海底管線/運輸等)、終端用戶產業(油氣上游工程、中游製程/運輸等)和地區(亞太地區、北美地區、歐洲地區、南美地區、中東和非洲地區)進行分類。市場預測以美元計價。

全球水合物抑制劑市場趨勢及洞察

擴大長距離海底繫泊工程

隨著沿海油田的枯竭,超過50公里的超長距離海底回接管道正逐漸成為標準配備。科萊恩公司在墨西哥灣計劃於2026年運作的謝南多厄計畫(Shenandoah project)中採用的化學技術,凸顯了持續施用抗凝劑以維持流量(即使在超過20,000 psi的壓力下)這一不斷變化的操作要求。低劑量抑制劑(以重量計1-3%)與散裝乙二醇(MEG)相比,可將海上蘊藏量減少高達50%,並降低直升機補給成本。在全電動海底佈局中,化學品儲存槽安裝在海底,可透過即時遙測技術調節注入速率。這項理念已在埃尼集團的佐爾(Zol)氣田成功應用,該氣田的自動回饋迴路將MEG的年消耗量降低了8-12%。對於超過約40公里的回接管道,化學藥劑比管中管保溫更具成本效益,這推動了對先進水合物控制解決方案的需求。

液化天然氣幹線和天然氣管道擴建工程

在中國、印度和東南亞,新的液化天然氣進口終端正在投入運作,預計在2024年至2026年間將總合十億立方公尺的再氣化能力。這些終端與遍布陸上的管道相連,這些管道穿越潮濕的季風地區,由於季節性氣溫下降,這些地區極易形成水合物。因此,全年註入抑制劑已成為一項標準操作要求,例如印度於2026年3月建成的3000公里東西向管道網路。像印尼雲頂FLNG這樣的浮體式液化天然氣運輸船,年輸送量達16億立方米,由於海上缺乏熱能,因此完全依賴動能抑制劑。卡達的液化天然氣擴建計畫包括一個專用的MEG(乙二醇)供應迴路,用於陸上乙二醇再生,這將使整個天然氣田運作內每噸液化天然氣的化學品成本降低約20%。

上游產業資本投資的週期性與布蘭特原油價格相關。

當布蘭特原油價格跌破每桶60美元時,營運商通常會在預算週期內推遲新的海底回接項目,導致化學品採購量立即下降。相反,價格回升通常需要18到24個月的延遲才能促成專案核准,因為重啟設計和採購流程需要時間。例如,雪佛龍公司表示,根據價格預測,其2026年深海計畫預算可能會波動10%到15%,這直接影響了水合物抑制劑的競標。北美頁岩油氣作業的反應更為迅速。油井數量的減少導致天然氣收集管道的利用率降低,使得生產商能夠在短短一個季度內將抑制劑用量減少兩位數。

細分市場分析

由於動態抑制劑在陸上天然氣處理迴路中展現出卓越的有效性,其在2025年佔據了水合物抑制劑市場43.13%的佔有率。在這些迴路中,回收的乙二醇(MEG)的循環利用率高達95%。預計到2031年,綠色/可生物分解抑制劑市場將以7.44%的複合年成長率成長。這主要得益於以油酸二鈉為基礎的界面活性劑,它們在維持抗聚集功能的同時,也展現出符合OECD 301B標準的68.9%的生物分解性。 Innospec等供應商提供符合API 17TR6認證的低劑量化學品,適用於超高壓油井,每桶油可降低約500美元的物流成本。

在現有再生設施運作的區域,傳統的甲醇和乙二醇(MEG)仍然是經濟有效的選擇。然而,北海和美國墨西哥灣日益嚴格的排放法規正在逐步加速轉向更環保的替代方案。參與延壽計畫的營運商正在採用雙抑制劑策略,即在推出階段使用乙二醇,並在穩定運行階段過渡到可生物分解的抗絮凝劑,以平衡成本和合規要求。雖然預計這兩種試劑將繼續共存,但在環保意識較強的地區,環保產品的高價意味著特種化學品供應商將有更大的利潤空間。

2025年,液態抑制劑佔總銷售額的77.89%。這是因為液態抑制劑簡化了井口結構,允許使用單根注射供應連系管同時計量和注射水合物抑制劑、結垢抑制劑和腐蝕抑制劑。預計到2031年,固體抑制劑的年複合成長率將達到7.32%,這主要得益於北美遠程井口先導作業業務的發展,該業務已使季度直升機飛行次數減少了40%。

包覆在聚合物基質中的固體顆粒會在30至90天內溶解,從而在原位維持500至1000 ppm的抑制劑濃度。這種方法對於不便安裝液體儲槽的無人衛星油田尤其適用。然而,溶解速率的波動以及地質損害的風險限制了其廣泛應用。一種混合方法正在逐漸被接受,該方法在試運行使用液體抑制劑,在穩定運行階段過渡到使用顆粒抑制劑。

區域分析

預計到2025年,北美將佔據33.45%的市場佔有率,這主要得益於墨西哥灣的深海生產和頁岩氣開採系統。儘管該地區資產密集,但由於數位化加藥平台的引入,化學品消耗量減少了近10%,絕對成長速度有所放緩。

亞太地區是成長最快的地區,預計到2031年複合年成長率將達到7.25%。這項成長主要得益於中國新建的LNG接收站和印度一條長達3,000公里的天然氣管道。這兩項工程均採用24運作運行的乙二醇(MEG)或動態抑制劑循環系統,以應對高濕度和溫度波動。此外,印尼和馬來西亞正在建造的浮體式液化天然氣運輸船的船體也對此類產品產生了需求,因為這些地區目前尚無其他熱處理方案。

由於北海營運商擴大在短距離回接管道(連接管道)中採用隔熱材料,歐洲市場佔有率保持穩定。然而,該地區新興的二氧化碳捕集與儲存(CCS)管道正在催生對專用二氧化碳抑制劑的新需求。中東和非洲地區受益於卡達500公里長的專用乙二醇(MEG)系統和沙烏地阿拉伯的管道擴建。南美洲的進展較為緩慢,該地區的鹽層下油田依賴化學品物流作為最具成本效益的流量管理解決方案。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 市場分析與定義的前提條件

- 分析範圍

第2章 分析方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 擴建遠距離海底連接線

- 液化天然氣主幹管道及天然氣管道擴建工程

- 高濃度二氧化碳碳捕集與封存/碳捕集利用製程管線的出現

- 向全電動海底架構過渡

- 氫氣輸送管路(NH3、LOHC)中對水合物抑制劑的需求

- 市場限制因素

- 上游資本投資的周期性與布蘭特原油價格密切相關。

- 由於對持久性季銨鹽界面活性劑的監管,逐步淘汰

- 與化學抑制劑競爭的潛水艇隔熱材料

- 價值鏈分析

- 波特五力分析

第5章:預測市場規模與成長率

- 按類型

- 動態水合物抑制劑(THIs)

- 低劑量水合物抑制劑(LDHI)

- 環保/可生物分解抑制劑

- 按形狀

- 液體

- 固體的

- 透過使用

- 海底管線和運輸

- 石油和天然氣生產井

- 天然氣處理和分離廠

- 液化天然氣(LNG)和浮體式液化天然氣(FLNG)設施

- 二氧化碳捕集與儲存(CCS)/二氧化碳捕集、儲存與利用(CCUS),二氧化碳管

- 按最終用戶行業分類

- 石油和天然氣上游工程

- 中游工藝/運輸

- 液化天然氣(LNG)營運商

- 石油化學/GTL(氣轉液)

- 其他終端用戶產業(航運、電力、工業冷凍)

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 東南亞國協

- 其他亞太國家

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐國家

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲國家

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- Arkema

- Ashland

- Baker Hughes Company

- BASF

- Clariant

- Ecolab

- Evonik Industries AG

- Halliburton

- Innospec

- Kemira Oyj

- Kuraray

- SLB

- Thermax Limited

第7章 市場機會與未來展望

According to Mordor Intelligence, the hydrate inhibitors market size is expected to increase from USD 259.13 million in 2025 to USD 276.26 million in 2026 and reach USD 380.46 million by 2031, growing at a CAGR of 6.61% over 2026-2031.

This report is Segmented by Type (Thermodynamic Hydrate Inhibitors, and More), Form (Liquid and Solid), Application (Subsea Pipelines and Transportation, and More), End-User Industry (Upstream Oil and Gas, Midstream and Transmission, and More), and Geography (Asia-Pacific, North America, Europe, South America and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Hydrate Inhibitors Market Trends and Insights

Expansion of Long-Distance Subsea Tie-Backs

Ultra-long tie-backs exceeding 50 kilometers have become standard as near-field reservoirs are depleted. Clariant's chemistry for the 2026 Shenandoah start-up in the Gulf of Mexico highlights the evolving operational requirements, where continuous anti-agglomerant dosing ensures flow at pressures above 20,000 psi. Low-dosage inhibitors, functioning at 1-3% by weight, reduce offshore storage volumes by up to 50% compared to bulk MEG, lowering helicopter resupply costs. All-electric subsea layouts incorporate chemical tanks on the seabed, enabling real-time telemetry to adjust dosing rates. This concept has been successfully implemented at Eni's Zohr gas field, where automated feedback loops reduced annual MEG consumption by 8-12%. For tie-backs extending beyond approximately 40 kilometers, chemicals are more cost-effective than pipe-in-pipe insulation, driving demand for advanced hydrate-control solutions.

Growing LNG Trunk-line and Gas-pipeline Construction

China, India, and Southeast Asia are commissioning new LNG import terminals, collectively adding double-digit billions of cubic meters of regasification capacity between 2024 and 2026. These terminals connect to extensive onshore pipelines traversing humid, monsoon-prone regions where seasonal cooling induces hydrate formation. Consequently, year-round inhibitor injection is a standard operational requirement, as seen in India's 3,000-kilometer east-to-west grid completed in March 2026. Floating LNG vessels, such as Indonesia's 1.6 bcm-per-year Genting FLNG, rely exclusively on kinetic inhibitors due to the absence of thermal mass in offshore locations. Qatar's LNG expansion includes dedicated MEG delivery loops with onshore glycol regeneration, reducing chemical costs per ton of LNG by approximately 20% over the field's lifespan.

Upstream CAPEX Cyclicality Tied to Brent Crude Prices

When Brent crude prices fall below USD 60 per barrel, operators often defer new subsea tie-back projects within a single budgeting cycle, leading to immediate reductions in chemical procurement. Conversely, price recoveries typically stimulate project approvals only after an 18-24-month delay due to the time required for engineering and procurement processes to resume. For example, Chevron has indicated a 10-15% fluctuation in its 2026 deepwater budget based on price forecasts, directly impacting hydrate-inhibitor tenders. North American shale operations respond even more rapidly; declining well counts reduce gathering-line utilization, enabling producers to cut inhibitor dosages by double digits within a single quarter.

Other drivers and restraints analyzed in the detailed report include:

- Emergence of CO2-Rich CCS/CCUS Flowlines

- Shift Toward All-Electric Subsea Architecture

- Regulatory Phase-Out of Persistent Quaternary Surfactants

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Thermodynamic inhibitors retained 43.13% of the hydrate inhibitors market share in 2025 due to their established effectiveness in onshore gas-processing loops, where recovered MEG achieves up to 95% recycling efficiency. The market size for green/biodegradable inhibitors is anticipated to grow at a 7.44% CAGR through 2031, supported by a disodium oleate surfactant that demonstrated 68.9% biodegradation under OECD 301B standards while maintaining anti-agglomerant functionality. Vendors such as Innospec are offering API 17TR6-validated low-dose chemistries for ultra-high-pressure wells, reducing logistics costs by approximately USD 500 per delivered barrel.

Legacy methanol and MEG will remain cost-effective in regions with existing regeneration units; however, stricter discharge regulations in the North Sea and U.S. Gulf indicate a gradual shift toward greener alternatives. Operators involved in life-extension projects are adopting dual-inhibitor strategies, utilizing MEG during ramp-up phases and transitioning to biodegradable anti-agglomerants for steady-state operations to balance costs with compliance requirements. The coexistence of both chemistries is expected to continue, but the premium pricing of green products in environmentally sensitive regions suggests increasing margin opportunities for specialty suppliers.

Liquid inhibitors accounted for 77.89% of 2025 revenue, as their use simplifies topside architecture by enabling a single injection umbilical to meter hydrate, scale, and corrosion inhibitors simultaneously. Solid inhibitors are projected to grow at a 7.32% CAGR through 2031, driven by remote wellhead pilots in North America that reduced quarterly helicopter runs by 40%.

Solid pellets embedded in polymer matrices dissolve over 30-90 days, maintaining 500-1,000 ppm inhibitor in-situ. This approach is particularly appealing for unmanned satellite fields where liquid tanks are impractical. However, variability in dissolution rates and risks of formation damage limit broader adoption. Hybrid schedules, where operators begin with liquid inhibitors during commissioning and transition to pellets for steady-state operations, are gaining acceptance.

Geography Analysis

North America held a 33.45% market share in 2025, supported by deepwater volumes in the Gulf of Mexico and shale-gas gathering systems. The adoption of digital dosing platforms, which reduced chemical consumption by nearly 10%, moderated absolute growth despite the region's dense asset base.

Asia-Pacific is the fastest-growing region, with a 7.25% CAGR projected through 2031. Growth is driven by China's new LNG terminals and India's 3,000-kilometer gas pipeline, both designed with 24-hour MEG or kinetic-inhibitor loops to handle high water cuts and temperature variations. Additional demand comes from floating LNG hulls under construction in Indonesia and Malaysia, where thermal substitutes are unavailable.

Europe's market share remains stable as North Sea operators increasingly use thermal insulation for short tie-backs. However, the region's emerging CCS pipelines are creating new demand for CO2-specific inhibitors. The Middle-East and Africa benefit from Qatar's 500-kilometer dedicated MEG system and Saudi Arabia's pipeline expansions. South America is progressing slowly, with pre-salt fields relying on chemical logistics as the most cost-effective flow-assurance solution.

- Arkema

- Ashland

- Baker Hughes Company

- BASF

- Clariant

- Ecolab

- Evonik Industries AG

- Halliburton

- Innospec

- Kemira Oyj

- Kuraray

- SLB

- Thermax Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expansion of long-distance subsea tie-backs

- 4.2.2 Growing LNG trunk-line and gas-pipeline construction

- 4.2.3 Emergence of CO2-rich CCS/CCUS flowlines

- 4.2.4 Shift toward all-electric subsea architecture

- 4.2.5 Demand for hydrate inhibitors in hydrogen carrier pipelines (NH3, LOHC)

- 4.3 Market Restraints

- 4.3.1 Upstream CAPEX cyclicality tied to Brent crude prices

- 4.3.2 Regulatory phase-out of persistent quaternary surfactants

- 4.3.3 Thermal subsea insulation competing with chemical inhibitors

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Thermodynamic Hydrate Inhibitors (THIs)

- 5.1.2 Low-Dosage Hydrate Inhibitors (LDHIs)

- 5.1.3 Green/Biodegradable Inhibitors

- 5.2 By Form

- 5.2.1 Liquid

- 5.2.2 Solid

- 5.3 By Application

- 5.3.1 Subsea Pipelines and Transportation

- 5.3.2 Oil and Gas Production Wells

- 5.3.3 Gas Processing and Separation Plants

- 5.3.4 Liquified Natural Gas (LNG) and Floating Liquefied Natural Gas (FLNG) Facilities

- 5.3.5 Carbon Capture Storage (CCS)/Carbon Capture, Storage, and Utilization (CCUS) and Carbon Dioxide Pipelines

- 5.4 By End-user Industry

- 5.4.1 Upstream Oil and Gas

- 5.4.2 Midstream and Transmission

- 5.4.3 Liquified Natural Gas (LNG) Operators

- 5.4.4 Petrochemical and Gas-to-Liquids

- 5.4.5 Other End-user Industries (Marine, Power, Industrial Refrigeration)

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 ASEAN Countries

- 5.5.1.6 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 NORDIC Countries

- 5.5.3.8 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Arkema

- 6.4.2 Ashland

- 6.4.3 Baker Hughes Company

- 6.4.4 BASF

- 6.4.5 Clariant

- 6.4.6 Ecolab

- 6.4.7 Evonik Industries AG

- 6.4.8 Halliburton

- 6.4.9 Innospec

- 6.4.10 Kemira Oyj

- 6.4.11 Kuraray

- 6.4.12 SLB

- 6.4.13 Thermax Limited

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

原油流動性改進劑:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)

原油流動性改進劑:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年) 原油流動性改進劑市場:依產品類型、應用和地區分類

原油流動性改進劑市場:依產品類型、應用和地區分類 原油流動改進劑市場:按類型、劑型和應用分類-2026年至2032年全球預測

原油流動改進劑市場:按類型、劑型和應用分類-2026年至2032年全球預測 原油流動性改進劑市場規模、佔有率、趨勢和預測:按產品、應用和地區分類,2026-2034年

原油流動性改進劑市場規模、佔有率、趨勢和預測:按產品、應用和地區分類,2026-2034年 油氣市場流動保障:市場分析及至2035年預測:依類型、產品、服務、技術、組件、應用、材料類型、製程、最終用戶及設備分類水合物抑制劑市場:依抑制劑類型和地區分類

油氣市場流動保障:市場分析及至2035年預測:依類型、產品、服務、技術、組件、應用、材料類型、製程、最終用戶及設備分類水合物抑制劑市場:依抑制劑類型和地區分類 2026年全球原油流動改進劑市場報告

2026年全球原油流動改進劑市場報告 原油流動改進劑市場-全球產業規模、佔有率、趨勢、機會與預測:依改進劑類型、應用、地區和競爭格局分類,2021-2031年

原油流動改進劑市場-全球產業規模、佔有率、趨勢、機會與預測:依改進劑類型、應用、地區和競爭格局分類,2021-2031年 水合物抑制劑市場規模、佔有率和成長分析(按產品類型、應用、終端用戶產業、配方類型、分銷管道和地區分類)-2026-2033年產業預測

水合物抑制劑市場規模、佔有率和成長分析(按產品類型、應用、終端用戶產業、配方類型、分銷管道和地區分類)-2026-2033年產業預測 原油流動改進劑市場規模、佔有率和成長分析(按類型、供應類型、應用和地區分類)-2026-2033年產業預測

原油流動改進劑市場規模、佔有率和成長分析(按類型、供應類型、應用和地區分類)-2026-2033年產業預測