|

市場調查報告書

商品編碼

2062214

工業聚氨酯彈性體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Industrial Polyurethane Elastomer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

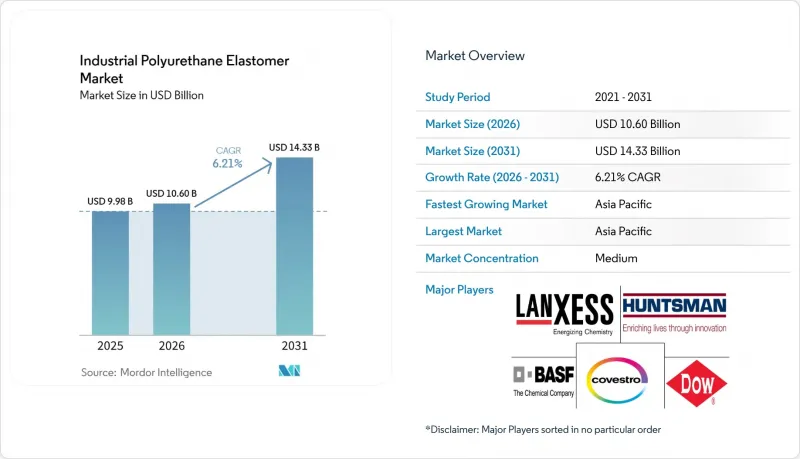

據 Mordor Intelligence 稱,2025 年工業聚氨酯彈性體市值為 99.8 億美元,預計到 2031 年將達到 143.3 億美元,而 2026 年為 106 億美元,預測期(2026-2031 年)的複合年成長率為 6.21%。

本報告按類型(熱固性聚氨酯彈性體和熱塑性聚氨酯彈性體)、加工技術(澆鑄等)、應用(輪輥、皮帶聯軸器等)、終端用戶行業(汽車和交通運輸、石油和天然氣等)以及地區(亞太地區、北美地區等)進行細分。市場預測以美元計價。

全球工業聚氨酯彈性體市場趨勢與洞察

利用聚氨酯零件擴展石油和天然氣探勘設備

聚氨酯密封件、管道清管器和電纜保護器具有卓越的耐碳氫化合物浸泡性能和低於-40 度C的耐溫性能,可取代海底工程中的丁腈橡膠和氟橡膠。邵氏A硬度為70-95的澆鑄彈性體可將磨蝕性漿液幫浦的使用壽命延長高達300%,進而減少船舶作業者的停機時間。

利用金屬-PU混合技術實現重型機械輕量化

透過將聚氨酯套管黏合到鋁或鋼芯上,可以在保持懸吊襯套和駕駛室安裝所需的剛性的同時,降低非懸吊品質。BASF的Cellasto組件在2024年的測試項目中,NVH(噪音、振動和不舒適性)性能提升了2.4%,促使巴斯夫在印度投資1億歐元新建一座Cellasto工廠,該工廠計劃於2026年投產。

歐盟REACH法規關於二異氰酸酯

根據歐盟於2023年8月生效的REACH法規,所有接觸MDI或TDI的歐洲工人必須完成認證培訓,這增加了合規成本,並促使原始設備製造商(OEM)轉向TPU。 TPU可以透過射出成型的CPU組件。

細分市場分析

至2025年,熱塑性聚氨酯(TPU)彈性體將佔據工業聚氨酯彈性體市場56.67%的佔有率,預計到2031年將以6.89%的複合年成長率成長。該細分市場在小批量重型篩網、大型輥筒以及公差要求在±5毫米或以上的客製化密封件等應用領域佔據主導地位。澆鑄過程可實現邵氏硬度從40A到75D的客製化,並便於纖維和微球填料的複合,而無需考慮剪切絕緣方面的挑戰。熱塑性TPU的成長主要得益於強制回收政策。陶氏化學於2025年推出的SPECFLEX CIR系列產品,在維持拉伸強度標準的同時,採用了高達65%的再生TPU。

熱塑性聚氨酯 (TPU) 具有射出成型效率高、符合循環經濟要求等優勢,特別適用於汽車內裝和電子設備機殼。然而,在需要極高耐磨性、超大尺寸零件以及複雜化學成分且需要現場加工柔軟性的應用領域,澆鑄聚氨酯 (CPU) 仍然佔據主導地位。 ISO 7425-1:2021 硬度和壓縮永久變形測試標準的製定,提高了供應商之間的可比性,並降低了採礦和海上平台等行業大型資產的採購風險。

射出成型憑藉其能夠以最少的後續加工即可生產出精確形狀的能力,預計到2025年將佔據39.66%的市場佔有率。 2024年的一項研究表明,將料筒溫度從190 度C提高到210 度C可將拉伸強度提高12%,這凸顯了程式參數對最佳化TPU性能的重要性。對於製造超出普通注塑機能力範圍的零件以及進行快速現場維修而言,澆鑄仍然是至關重要的工藝。其他加工技術,包括壓縮成型和吹塑成型,預計到2031年將以6.90%的複合年成長率成長,這主要得益於多成分成型技術的進步,該技術將柔軟觸感表面材料和結構型芯結合在單一工藝中。

連續擠出成型過程廣泛應用於帶材和管材的生產,其市場成長主要歸功於材料均勻性的提高和生產的連續性。此外,數位化製程控制和封閉回路型計量降低了小規模加工商採用混合平台的門檻,從而使市場佔有率重新分配給靈活的本地加工商。

區域分析

預計亞太地區將在2025年佔據全球銷售佔有率榜首,達到46.67%,並預計在2031年之前維持6.98%的複合年成長率。中國產能的擴張,包括科思創珠海一期TPU工廠(年產能3萬噸,預計2026年運作),將為鞋類、家用電子電器和汽車等產業提供在地化供應。印度多元醇消費量的成長,以及賽樂仕通預計於2026年運作的新產能,正在加強南亞的垂直整合。日本和韓國專注於供應先進的電子級TPU,而東南亞國協則正在抓住從中國沿海地區轉移過來的鞋類和家電組裝需求。

北美市場保持著強勁的市場地位,主要得益於汽車、石油天然氣和倉儲自動化產業的支撐。陶氏化學計畫於2025年在泰國擴大丙二醇產能,將確保上游原料供應,並與亨斯邁公司計畫在2026年前提升其歐洲系統產能的計畫形成協同效應。墨西哥的近岸外包趨勢也支撐了美國汽車組裝對澆鑄聚氨酯NVH零件的需求。

在歐洲,嚴格的REACH法規限制了二異氰酸酯的使用,這促使人們轉向採用TPU射出成型和低遊離單體含量的預聚物系統。德國、法國和義大利正在滿足對先進阻尼支座和鐵路零件的需求,而北歐國家則專注於生物基多元醇和無鹵阻燃劑,用於風力發電和寒冷氣候應用。在南美和中東部分地區,聚氨酯被用於採礦和石化基礎設施,但由於大宗商品週期波動,其應用成長緩慢。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 利用聚氨酯零件擴展石油和天然氣探勘設備

- 利用金屬/PU混合技術實現重型機械的輕量化

- 工業自動化需要抑制高負載振動。

- 用於快速工業原型製作的3D列印PU彈性體模具

- 現場噴塗彈性體襯裡,延長資產使用壽命

- 市場限制因素

- 歐盟REACH法規關於二異氰酸酯的規定

- 先進TPE(PEBA、TPU合金)作為替代方案

- 地下礦井中與保險相關的可燃性問題

- 價值鏈分析

- 波特五力模型

第5章 市場規模與成長預測

- 按類型

- 熱塑性聚氨酯彈性體(TPU)

- 熱固性聚氨酯彈性體(CPU)

- 透過加工技術

- 射出成型

- 鑄件

- 擠壓

- 其他加工技術(壓縮成型、吹塑成型等)

- 透過使用

- 輪子和滾輪

- 皮帶和聯軸器

- 減震和減震部件

- 密封件和墊圈

- 機械零件

- 礦用篩網和襯裡

- 其他用途

- 按最終用戶行業分類

- 汽車和運輸業

- 石油和天然氣

- 採礦和採石

- 工業機械和設備

- 物料輸送

- 建造

- 電子電器設備

- 其他終端用戶產業(紡織、造紙、食品等)

- 按地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 東南亞國協

- 其他亞太國家

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐國家

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲國家

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- Arlanxeo

- BASF

- Blickle Rader+Rollen

- COIM Group

- Covestro AG

- Dow

- Era Polymers Pty Ltd

- Herikon BV

- Huntsman International LLC

- James Walker

- LANXESS

- Lubrizol

- MCPU Polymer Engineering LLC

- Mitsui Chemicals India Pvt. Ltd.

- Parker Hannifin Corp

- Reckon Rubber Industries

- Tosoh Corporation

- Trelleborg

- Wanhua

第7章 市場機會與未來展望

According to Mordor Intelligence, the industrial polyurethane elastomer market size was valued at USD 9.98 billion in 2025 and is estimated to grow from USD 10.60 billion in 2026 to reach USD 14.33 billion by 2031, at a CAGR of 6.21% during the forecast period (2026-2031).

This report is Segmented by Type (Thermoset PU Elastomers and Thermoplastic PU Elastomers), Processing Technology (Casting, and More), Application (Wheels and Rollers, Belts and Couplings, and More), End-User Industry (Automotive and Transportation, Oil and Gas, and More), and Geography (Asia-Pacific, North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Industrial Polyurethane Elastomer Market Trends and Insights

Expansion of Oil and Gas Exploration Equipment Using Polyurethane Parts

Polyurethane seals, pipeline pigs, and cable protectors exhibit excellent resistance to hydrocarbon immersion and temperatures below -40 °C, replacing nitrile and fluoroelastomers in subsea projects. Cast elastomers with Shore A 70-95 hardness ratings extend the service life of abrasive slurry pumps by up to 300%, reducing downtime for offshore operators.

Light-Weighting via Metal-PU Hybrids in Heavy Machinery

Bonding polyurethane sleeves to aluminum or steel cores reduces unsprung mass while maintaining the required stiffness for suspension bushings and cab mounts. BASF's Cellasto components achieved a 2.4% improvement in NVH (noise, vibration, and harshness) performance during a 2024 test program, leading to a EUR 100 million investment in a new Cellasto plant in India, scheduled to begin operations in 2026.

EU REACH Restrictions on Di-Isocyanates

Under EU REACH regulations effective August 2023, all European workers handling MDI or TDI must complete certified training, increasing compliance costs and encouraging OEMs to shift toward TPU, where injection molding can replace hand-cast CPU parts.

Other drivers and restraints analyzed in the detailed report include:

- Industrial Automation Needs High-Load Vibration Damping

- 3D-Printed PU Elastomer Tooling for Rapid Industrial Prototyping

- Advanced TPEs (PEBA, TPU Alloys) as Substitutes

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Thermoplastic polyurethane (TPU) elastomers accounted for 56.67% of the industrial polyurethane elastomer market share in 2025 and are projected to grow at a 6.89% CAGR through 2031. This segment leads in applications such as low-volume, heavy-duty screens, large rollers, and bespoke seals requiring tolerances exceeding +-5 mm. Cast processing enables shore hardness customization from 40A to 75D and facilitates the integration of fiber or microsphere fillers without shear-heating challenges. The growth of thermoplastic TPU is supported by recyclability mandates; Dow's SPECFLEX CIR line, launched in 2025, incorporates up to 65% recycled TPU while maintaining tensile strength benchmarks.

Thermoplastic TPU benefits from injection molding efficiency and compliance with circular economy requirements, particularly in automotive trim and electronics housings. However, cast polyurethane (CPU) retains an advantage in applications requiring extreme abrasion resistance, oversized parts, and complex chemistries that demand on-site processing flexibility. The ISO 7425-1:2021 standardization of hardness and compression-set tests enhances cross-supplier comparability and mitigates risks in large-asset procurement for industries such as mining and offshore platforms.

Injection molding held a 39.66% market share in 2025 due to its ability to produce precise geometries with minimal finishing. A 2024 study demonstrated that increasing barrel temperatures from 190 °C to 210 °C improved tensile strength by 12%, underscoring the importance of process parameters in optimizing TPU performance. Casting remains essential for manufacturing parts exceeding typical press capacities and for rapid field repairs. Other processing technologies, including compression and blow molding, are expected to grow at a 6.90% CAGR through 2031, driven by advancements in multi-component molding that combine soft-touch skins with structural cores in a single process.

Continuous extrusion is widely used for belts and tubing, where market growth is linked to improved material homogeneity and uninterrupted production. Additionally, digital process controls and closed-loop metering are lowering barriers for small fabricators to adopt hybrid platforms, redistributing market share toward agile regional processors.

Geography Analysis

Asia-Pacific dominated with 46.67% revenue share in 2025 and is forecast to have the fastest 6.98% CAGR to 2031. Capacity expansions in China, such as Covestro's Phase 1 Zhuhai TPU plant with a 30 kt/y capacity launched in 2026, are enabling local supply for industries including footwear, consumer electronics, and automotive. India's increasing polyol consumption aligns with new Cellasto capacity expected to come online in 2026, strengthening vertical integration in South Asia. Japan and South Korea focus on supplying advanced electronics-grade TPU, while ASEAN nations capture demand for footwear and appliance assemblies relocating from coastal China.

North America maintains a strong market position, supported by automotive, oil and gas, and warehouse automation sectors. Dow's 2025 expansion of propylene glycol production in Thailand secures upstream feedstock, complementing Huntsman's planned increase in European systems capacity by 2026. Mexico's near-shoring trend supports cast polyurethane NVH components for U.S. vehicle assembly lines.

In Europe, stringent REACH regulations on di-isocyanates are driving a shift toward TPU injection molding and pre-polymer systems with lower free-monomer content. Germany, France, and Italy anchor demand for advanced damping mounts and railway components, while Nordic countries emphasize bio-based polyols and halogen-free flame retardants for wind energy and cold-climate applications. Selected South American and Middle-Eastern markets utilize polyurethane in mining and petrochemical infrastructure, though growth is moderated by commodity cycle volatility.

- Arlanxeo

- BASF

- Blickle Rader+Rollen

- COIM Group

- Covestro AG

- Dow

- Era Polymers Pty Ltd

- Herikon BV

- Huntsman International LLC

- James Walker

- LANXESS

- Lubrizol

- MCPU Polymer Engineering LLC

- Mitsui Chemicals India Pvt. Ltd.

- Parker Hannifin Corp

- Reckon Rubber Industries

- Tosoh Corporation

- Trelleborg

- Wanhua

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expansion of oil and gas exploration equipment using Polyurethane parts

- 4.2.2 Light-weighting via metal-PU hybrids in heavy machinery

- 4.2.3 Industrial automation needs high-load vibration damping

- 4.2.4 3-D printed PU elastomer tooling for rapid industrial prototyping

- 4.2.5 On-site spray-elastomer linings for asset-life extension

- 4.3 Market Restraints

- 4.3.1 EU REACH restrictions on di-isocyanates

- 4.3.2 Advanced TPEs (PEBA, TPU alloys) as substitutes

- 4.3.3 Insurance-driven flammability concerns in underground mining

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Thermoplastic PU Elastomers (TPU)

- 5.1.2 Thermoset PU Elastomers (CPU)

- 5.2 By Processing Technology

- 5.2.1 Injection Molding

- 5.2.2 Casting

- 5.2.3 Extrusion

- 5.2.4 Other Processing Technologies (Compression, Blow, etc.)

- 5.3 By Application

- 5.3.1 Wheels and Rollers

- 5.3.2 Belts and Couplings

- 5.3.3 Vibration and Shock-absorbing Components

- 5.3.4 Seals and Gaskets

- 5.3.5 Machine Components

- 5.3.6 Mining Screens and Liners

- 5.3.7 Other Applications

- 5.4 By End-user Industry

- 5.4.1 Automotive and Transportation

- 5.4.2 Oil and Gas

- 5.4.3 Mining and Quarrying

- 5.4.4 Industrial Machinery and Equipment

- 5.4.5 Material Handling

- 5.4.6 Construction

- 5.4.7 Electronics and Electrical

- 5.4.8 Other End-user Industries (Textile, Paper, Food, etc.)

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 Japan

- 5.5.1.3 India

- 5.5.1.4 South Korea

- 5.5.1.5 ASEAN Countries

- 5.5.1.6 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 NORDIC Countries

- 5.5.3.8 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Arlanxeo

- 6.4.2 BASF

- 6.4.3 Blickle Rader+Rollen

- 6.4.4 COIM Group

- 6.4.5 Covestro AG

- 6.4.6 Dow

- 6.4.7 Era Polymers Pty Ltd

- 6.4.8 Herikon BV

- 6.4.9 Huntsman International LLC

- 6.4.10 James Walker

- 6.4.11 LANXESS

- 6.4.12 Lubrizol

- 6.4.13 MCPU Polymer Engineering LLC

- 6.4.14 Mitsui Chemicals India Pvt. Ltd.

- 6.4.15 Parker Hannifin Corp

- 6.4.16 Reckon Rubber Industries

- 6.4.17 Tosoh Corporation

- 6.4.18 Trelleborg

- 6.4.19 Wanhua

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

航太彈性體市場報告:趨勢、預測與競爭分析(至2035年)

航太彈性體市場報告:趨勢、預測與競爭分析(至2035年) 工業用聚氨酯彈性體市場-2026-2032年全球市場預測3D列印彈性體市場-2026-2032年全球市場預測

工業用聚氨酯彈性體市場-2026-2032年全球市場預測3D列印彈性體市場-2026-2032年全球市場預測 彈性體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

彈性體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 聚烯彈性體市場:依應用和地區分類彈性體市場:2026-2032年全球市場預測(依彈性體類型、聚合製程、產品形式及應用分類)

聚烯彈性體市場:依應用和地區分類彈性體市場:2026-2032年全球市場預測(依彈性體類型、聚合製程、產品形式及應用分類) 2026-2034年全球3D列印彈性體市場規模、佔有率、趨勢與成長分析報告高溫彈性體市場:2026-2032年全球市場預測(依彈性體類型、產品形式、加工技術、應用與最終用途產業分類)全球聚烯彈性體市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

2026-2034年全球3D列印彈性體市場規模、佔有率、趨勢與成長分析報告高溫彈性體市場:2026-2032年全球市場預測(依彈性體類型、產品形式、加工技術、應用與最終用途產業分類)全球聚烯彈性體市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 彈性體市場分析及預測(至2035年):類型、產品、應用、技術、最終用戶、形態、材料類型、組件、製程、安裝類型

彈性體市場分析及預測(至2035年):類型、產品、應用、技術、最終用戶、形態、材料類型、組件、製程、安裝類型