|

市場調查報告書

商品編碼

2062184

瓦楞紙板:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)Corrugated Board - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

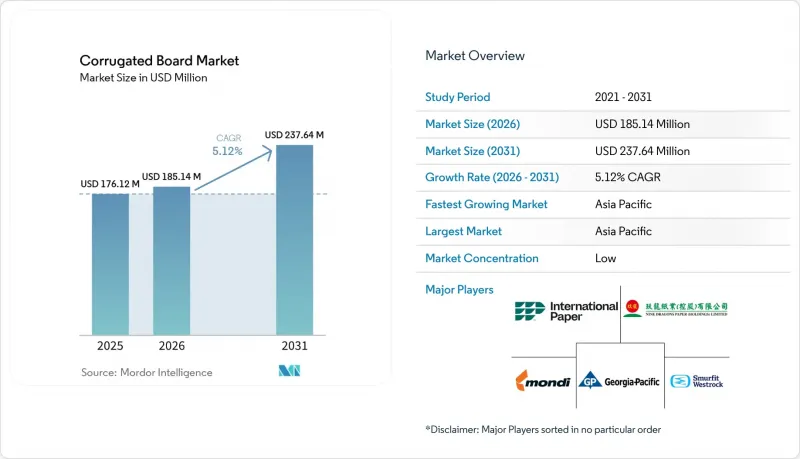

根據 Mordor Intelligence 預測,瓦楞紙板市場規模預計在 2025 年達到 1.7612 億美元,2026 年達到 1.8514 億美元,到 2031 年達到 2.3764 億美元,2026 年至 2031 年的複合年成長率為 5.12%。

本報告按瓦楞紙板類型(單層、雙層、三層)、材料類型(面紙板、紙芯、再生纖維、原生纖維)、終端用戶行業(食品飲料、電子商務零售、家用電子電器等)和地區(亞太、北美、歐洲、南美、中東和非洲)進行細分。市場預測以美元計價。

全球瓦楞紙板市場趨勢及洞察

電子商務出貨量爆炸性成長

Packsize 和 Panotec 的整合尺寸系統可將瓦楞紙板切割至與 SKU 尺寸相差 5 毫米以內,減少高達 40% 的空隙,從而降低全球宅配業者收取的體積重量附加費。預計到 2025 年,中國紙包裝出口量將達到 1,274,503 個貨櫃,遠超過印度的 272,348 個貨櫃,凸顯了該地區強大的基礎設施。Canon和 Domino 的QR碼單一途徑位印刷機現在可以以每分鐘 200 公尺的速度在 B 型和 E 型瓦楞紙箱上進行個性化印刷,將運輸紙箱轉化為行銷資產。這些進步共同滿足了跨洲小包裹量不斷成長的需求。

鼓勵紙張回收的永續性法規

歐盟的《包裝和包裝廢棄物法規》(2025/40)規定,到2030年紙張回收率必須達到85%,並禁止使用不可回收的包裝形式,這將推動對再生箱板紙的需求。美國加州、緬因州和奧勒岡州州等州正在透過生產者延伸責任制(EPR)計劃,將回收成本轉移給品牌所有者,並引導採購轉向回收率更高的原料。該計劃將於2024年至2026年實施。自2017年以來,新增的360萬噸再生纖維產能已使箱板紙的碳排放強度降低了高達20%。 2026年1月生效的食品接觸包裝禁用PFAS的規定,將進一步增加對用於披薩和外帶的水性塗層瓦楞紙箱的需求。永續性正成為一項競爭優勢,ISO 14001認證和森林供應鏈可追溯性現已成為幾乎所有跨國公司採購競標的必要條件。

與柔軟性塑膠郵寄袋的競爭

到2025年,聚乙烯郵袋將佔北美輕型小包裹市場8%至12%的佔有率,與2公斤以下重量的單層瓦楞紙箱相比,可節省30%至40%的成本。以尺寸計費的運費結構有利於貼合衣物形狀的軟性包裝袋,從而為住宅配送節省0.50至1美元。然而,目前緬因州、奧勒岡州和科羅拉多對每個塑膠郵袋徵收0.02至0.05美元的回收費,導致其經濟效益下降,促使亞馬遜試點使用可作為生活垃圾回收的纖維增強型郵袋。歐盟的一次性塑膠指令也引入了類似的生產者責任延伸(EPR)課稅,迫使品牌商轉向使用厚度僅為1.5毫米的超薄瓦楞紙板,以滿足自動化分類的嚴格要求。能夠生產厚度相當的瓦楞紙板郵袋的製造商正在重新奪回原本會被塑膠佔據的市場需求。

細分市場分析

到2025年,單層紙箱將佔總銷量的49.11%,但雙層紙箱預計到2031年將以5.43%的複合年成長率成長,因為家電運輸商將兩個瓦楞紙箱合併成一個加固單元,同時仍能滿足亞馬遜「無挫2.0」標準。層級構造目前仍主要應用於化工桶和汽車零件等需要超過1000千帕抗爆強度的市場區隔。在電子產品領域,BC型瓦楞紙板(旨在取代AC型瓦楞紙板)正被廣泛採用,以減少高達40%的衝擊損傷並改善螢幕顯示效果。

E型和F型微型瓦楞紙板因其能夠實現高清膠印和生產堅固的微型紙盒,在化妝品和製藥行業越來越受歡迎。 2024年,斯莫菲特韋斯特羅克公司關閉了年產60萬噸的傳統C型瓦楞紙板生產線,同時投資升級其B型瓦楞紙板生產線,以服務高階D2C(直接面對消費者)通路。雙層瓦楞紙層級構造的需求仍然強勁,因為它透過減少紙板層數和提高強度來降低運輸體積,從而符合永續性目標。

區域分析

預計到2025年,亞太地區將佔全球銷售額的50.24%,並在2031年之前以5.88%的複合年成長率成長,這主要得益於中國龐大的出口基礎和印度生產連結獎勵計畫(PLI)主導的電子產業叢集。日本Rengo公司正加大海外投資,旨在服務歐洲汽車製造商客戶,並計劃於2025年在德國開設一家重型瓦楞紙板廠。韓國的貨櫃出口進一步鞏固了其作為電子包裝中心的地位。

北美地區面臨箱板紙價格上漲的困境,但受益於亞馬遜不斷擴張的履約中心和在墨西哥的近岸生產。國際紙業斥資99億美元收購DS Smith,將擴大其跨大西洋業務,並帶來5.14億美元的收入。由於總計400萬噸產能的關閉,供應仍緊張,價格競爭也日益加劇。

在歐洲,企業正努力應對塑膠包裝回收強制令 (PPWR) 和碳邊境調節機制 (CBAM) 的課稅。 Mondi 對 Steti 和 Duino 的 12 億歐元投資符合脫碳趨勢,而其對 Schumacher 的 6.34 億歐元收購則加速了其進入高階加工市場的步伐。北歐的造紙廠,例如 Stora Enso 位於奧盧的年產 75 萬噸紙板生產線,正利用一體化紙漿生產帶來的能源效率提升。南美洲受益於 Cravin 的 Puma II 項目的出口,而中東則根據其「2030 願景」基礎設施規劃,擴大工業瓦楞紙板的產能。這些區域趨勢共同影響瓦楞紙板市場。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 市場分析與定義的前提條件

- 分析範圍

第2章 分析方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 電子商務出貨量爆炸性成長

- 鼓勵紙張回收的永續發展法規

- 新興市場食品飲料分銷的擴張

- 朝向輕量化、低成本包裝轉型

- 按需數位印刷客自訂套裝

- 市場限制因素

- 牛皮箱紙板的價格波動

- 與軟質塑膠郵袋的競爭

- 紙製品出口碳關稅

- 價值鏈分析

- 波特五力分析

第5章:預測市場規模與成長率

- 按紙板類型

- 單層

- 雙層

- 三層

- 依材料類型

- 襯板

- 中心核心

- 再生纖維

- 原生光纖

- 按最終用戶行業分類

- 食品/飲料

- 電子商務與零售

- 家用電子電器

- 個人護理和家居用品

- 工業和重型貨物

- 藥品和醫療保健

- 其他(家具、農業等)

- 按地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 東南亞國協

- 其他亞太國家

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐國家

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲國家

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- Georgia-Pacific LLC

- International Paper

- Klabin SA

- Mondi

- Nine Dragons Worldwide(China)Investment Group Co., Ltd.

- NIPPON PAPER INDUSTRIES CO., LTD.

- Oji Holdings Corporation

- Ondupack

- Packaging Corporation of America

- Pratt Industries, Inc.

- Rengo Co., Ltd.

- Saica

- Smurfit Westrock

- Stora Enso

- Thai Containers Group Co., Ltd.

- Visy

第7章 市場機會與未來展望

According to Mordor Intelligence, the corrugated board market size is projected to be USD 176.12 million in 2025, USD 185.14 million in 2026, and reach USD 237.64 million by 2031, growing at a CAGR of 5.12% from 2026 to 2031.

This report is Segmented by Board Type (Single-Wall, Double-Wall, and Triple-Wall), Material Type (Linerboard, Medium, Recycled Fiber, and Virgin Fiber), End-User Industry (Food and Beverage, E-Commerce and Retail, Consumer Electronics, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Corrugated Board Market Trends and Insights

Explosive Growth of E-Commerce Shipments

Integrated right-sizing systems from Packsize and Panotec cut board blanks within 5 millimeters of SKU dimensions, lowering void fill by up to 40% and reducing dimensional-weight surcharges levied by global couriers. China's export of 1,274,503 containers of paper packaging in 2025 dwarfed India's 272,348 tally, underscoring the region's infrastructure depth. QR-coded single-pass digital presses from Canon and Domino now personalize B-flute and E-flute cartons at 200 meters per minute, turning shipping boxes into marketing assets. These advances collectively keep the corrugated board market aligned with parcel-volume expansion across continents.

Sustainability Regulations Favouring Paper Recycling

The EU's Packaging and Packaging Waste Regulation 2025/40 mandates 85% collection for paper by 2030 and bans non-recyclable formats by 2030, escalating demand for recycled linerboard. U.S. states such as California, Maine, and Oregon shifted recycling costs to brand owners via extended producer responsibility schemes effective 2024-2026, steering procurement toward high-recovery substrate. Recycled-fiber capacity additions totaling 3.6 million tons since 2017 have already lowered containerboard carbon intensity by up to 20. PFAS bans in food-contact packaging, effective January 2026, further boost aqueous-coated corrugated pizza and take-out boxes. ISO 14001 certification and forest-chain traceability now appear in nearly every multinational procurement tender, embedding sustainability as a competitive necessity.

Competition from Flexible Plastic Mailers

Polyethylene mailers captured 8-12% of North American lightweight parcels in 2025, delivering 30-40% cost savings against single-wall corrugated in sub-2 kg bands. Dimensional shipping charges favor flexible pouches that hug apparel contours, saving USD 0.50-1.00 on residential deliveries. Yet Maine, Oregon, and Colorado now assess USD 0.02-0.05 recycling fees per plastic mailer, narrowing economics and prompting Amazon to test fiber-padded mailers eligible for curbside recycling. The EU Single-Use Plastics Directive layers similar EPR levies, nudging brands toward micro-flute cartons as thin as 1.5 millimeters that meet automated sortation rigors. Corrugated converters that match mailer thickness reclaim volumes otherwise lost to plastic.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Food and Beverage Distribution in Emerging Markets

- Shift Toward Lightweight, Cost-Efficient Packaging

- Carbon Border Taxes on Paper Exports

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Single-wall held 49.11% revenue in 2025, yet double-wall is growing at a 5.43% CAGR to 2031 as appliance shippers consolidate two cartons into one reinforced unit that still meets Amazon's Frustration-Free 2.0 metrics. Triple-wall remains niche for chemical drums and auto parts requiring burst strength above 1,000 kPa. Engineered BC-flute replaces AC-flute in electronics, trimming impact damage by up to 40% and enhancing shelf presentation.

Micro-flute E- and F-profiles are penetrating cosmetics and pharma because they permit high-definition litho and rigid micro-cartons. Smurfit Westrock shuttered 600,000 tons of legacy C-flute capacity in 2024 while funding B-flute upgrades that serve premium direct-to-consumer channels. Fewer, stronger cartons reduce freight cube and align with sustainability goals, giving double-wall formats durable tailwinds inside the corrugated board market.

Geography Analysis

Asia-Pacific commanded 50.24% of revenue in 2025 and is projected to grow at a 5.88% CAGR through 2031, lifted by China's vast export base and India's PLI-driven electronics clusters. Japan's Rengo opened a heavy-duty plant in Germany in 2025, underscoring outbound investments aimed at serving European auto clients. South Korea's container exports back its role as electronics-packaging hub.

North America faces linerboard price hikes yet benefits from Amazon's fulfillment build-out and nearshored Mexican manufacturing. International Paper's USD 9.9 billion DS Smith deal adds transatlantic scale and USD 514 million. Capacity closures totaling 4 million tons keep supply tight, reinforcing disciplined pricing.

Europe grapples with PPWR recyclability mandates and CBAM levies. Mondi's EUR 1.2 billion capex at Steti and Duino aligns with low-carbon trends, while its EUR 634 million acquisition of Schumacher accelerates access to premium converters. Nordic mills like Stora Enso's Oulu 750,000 tpa board line capitalize on integrated pulp energy efficiencies. South America benefits from Klabin's Puma II export flows, whereas the Middle-East builds industrial carton capacity for Vision 2030 infrastructure. These regional dynamics jointly influence the corrugated board market trajectory.

- Georgia-Pacific LLC

- International Paper

- Klabin S.A.

- Mondi

- Nine Dragons Worldwide (China) Investment Group Co., Ltd.

- NIPPON PAPER INDUSTRIES CO., LTD.

- Oji Holdings Corporation

- Ondupack

- Packaging Corporation of America

- Pratt Industries, Inc.

- Rengo Co., Ltd.

- Saica

- Smurfit Westrock

- Stora Enso

- Thai Containers Group Co., Ltd.

- Visy

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Explosive Growth of E-Commerce Shipments

- 4.2.2 Sustainability Regulations Favouring Paper Recycling

- 4.2.3 Expansion of Food and Beverage Distribution in Emerging Markets

- 4.2.4 Shift Toward Lightweight, Cost-Efficient Packaging

- 4.2.5 On-Demand Digital Printing Custom Packs

- 4.3 Market Restraints

- 4.3.1 Kraft Linerboard Price Volatility

- 4.3.2 Competition from Flexible Plastic Mailers

- 4.3.3 Carbon Border Taxes on Paper Exports

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Board Type

- 5.1.1 Single-wall

- 5.1.2 Double-wall

- 5.1.3 Triple-wall

- 5.2 By Material Type

- 5.2.1 Linerboard

- 5.2.2 Medium

- 5.2.3 Recycled Fiber

- 5.2.4 Virgin Fiber

- 5.3 By End-user Industry

- 5.3.1 Food and Beverage

- 5.3.2 E-commerce and Retail

- 5.3.3 Consumer Electronics

- 5.3.4 Personal Care and Household

- 5.3.5 Industrial and Heavy-Duty

- 5.3.6 Pharmaceuticals and Healthcare

- 5.3.7 Other (Furniture, Agriculture, etc.)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 Japan

- 5.4.1.3 India

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 NORDIC Countries

- 5.4.3.8 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Georgia-Pacific LLC

- 6.4.2 International Paper

- 6.4.3 Klabin S.A.

- 6.4.4 Mondi

- 6.4.5 Nine Dragons Worldwide (China) Investment Group Co., Ltd.

- 6.4.6 NIPPON PAPER INDUSTRIES CO., LTD.

- 6.4.7 Oji Holdings Corporation

- 6.4.8 Ondupack

- 6.4.9 Packaging Corporation of America

- 6.4.10 Pratt Industries, Inc.

- 6.4.11 Rengo Co., Ltd.

- 6.4.12 Saica

- 6.4.13 Smurfit Westrock

- 6.4.14 Stora Enso

- 6.4.15 Thai Containers Group Co., Ltd.

- 6.4.16 Visy

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

瓦楞紙板製造機械市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、製造能力、應用、地區和競爭格局分類,2021-2031年

瓦楞紙板製造機械市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、製造能力、應用、地區和競爭格局分類,2021-2031年 瓦楞紙板市場:2026-2032年全球市場預測(按瓦楞類型、產品類型、最終用途產業和分銷管道分類)

瓦楞紙板市場:2026-2032年全球市場預測(按瓦楞類型、產品類型、最終用途產業和分銷管道分類) 紙板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

紙板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 全球瓦楞紙包裝市場規模、佔有率、趨勢和成長分析報告(2026-2034年)紙板折疊市場-2026-2031年預測PP鈣塑板市場按材料類型、製造流程、厚度和應用分類-2026-2032年全球預測商用微瓦楞紙市場按產品類型、瓦楞類型、塗層類型、定量、分銷管道、應用和最終用途行業分類-全球預測,2026-2032年

全球瓦楞紙包裝市場規模、佔有率、趨勢和成長分析報告(2026-2034年)紙板折疊市場-2026-2031年預測PP鈣塑板市場按材料類型、製造流程、厚度和應用分類-2026-2032年全球預測商用微瓦楞紙市場按產品類型、瓦楞類型、塗層類型、定量、分銷管道、應用和最終用途行業分類-全球預測,2026-2032年 按類型、產品類型、最終用途產業和地區分類的箱板紙市場規模、佔有率和成長分析 - 2026-2033 年產業預測

按類型、產品類型、最終用途產業和地區分類的箱板紙市場規模、佔有率和成長分析 - 2026-2033 年產業預測 瓦楞紙包裝市場規模、佔有率和成長分析(按瓦楞類型、產品類型、包裝類型、壁結構、終端用戶產業和地區分類)—產業預測(2026-2033 年)

瓦楞紙包裝市場規模、佔有率和成長分析(按瓦楞類型、產品類型、包裝類型、壁結構、終端用戶產業和地區分類)—產業預測(2026-2033 年) 紙托盤:全球市場佔有率和排名、總收入和需求預測(2025-2031年)

紙托盤:全球市場佔有率和排名、總收入和需求預測(2025-2031年)