|

市場調查報告書

商品編碼

2044217

紙板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Cartonboard - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

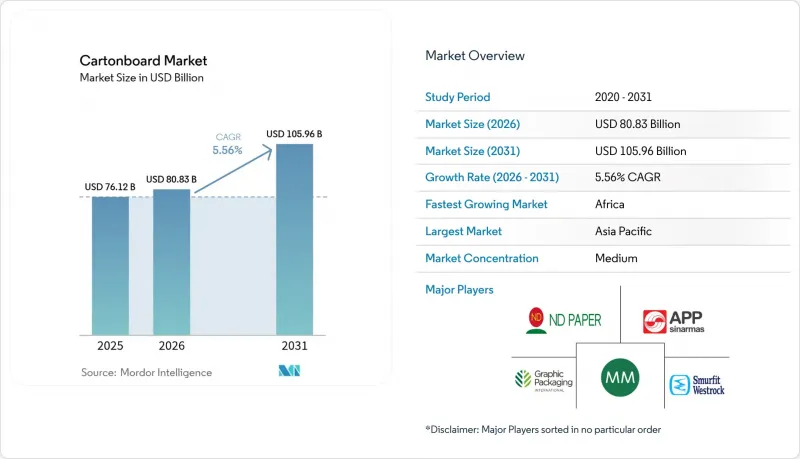

預計到 2025 年,紙板市場規模將達到 761.2 億美元,到 2026 年將達到 808.3 億美元,到 2031 年將達到 1059.6 億美元,2026 年至 2031 年的複合年成長率為 5.56%。

在強力的政策壓力(要求完全可回收)、消費者對無塑膠包裝日益成長的偏好以及電商領域輕量化包裝趨勢的推動下,品牌所有者正轉向纖維基解決方案。由阻隔塗層紙板製成的可折疊紙盒、紙套和液體包裝正在取代硬質聚對苯二甲酸乙二醇酯 (PET) 和聚丙烯 (PP) 包裝,尤其是在食品、飲料和化妝品領域。數位印刷機使面向消費者 (DTC) 品牌的小批量生產成為盈利,而高得率微纖化纖維素可將紙張重量降低 10-15%,從而降低體積重量帶來的運輸成本。在供應方面,原生紙漿廠繼續在醫藥和奢侈品領域獲得高價值訂單,而綜合回收商則專注於光學分選技術,以減少紙包品質的下降。

全球電路板市場趨勢與洞察

電子商務中用紙板取代紙箱的情況正在迅速增加。

在D2C(直接面對消費者)網路中,雙層紙箱正逐漸被單層紙板套取代,這可減輕小包裹重量20-30%,並降低承運商的體積重量費用。亞馬遜和阿里巴巴現在使用紙質緩衝材料代替塑膠空氣枕,推動緩衝材料的需求以每年3.9%的速度成長。耐吉和蘋果重新設計了服裝和電子產品的包裝,完全拋棄了紙板。這催生了對重量為200-250克/平方米且具有足夠層壓強度的可折疊紙板的需求。這種轉變為能夠向北美和歐洲大都市地區(當日送達服務盛行)供應高密度、輕質紙板的紙張製造商創造了新的收入來源。

快速消費品產業向無塑膠初級包裝轉型

全球主要消費品公司正在對其產品系列維修,採用分散塗層紙板,這種紙板無需聚乙烯層即可保持油、濕氣和氧氣阻隔性。斯特拉勒恩索公司於2026年1月推出的「Performa Lumi」紙板,採用專為化妝品品牌配製的礦物顏料,具有出色的不透明度。漢高公司於2025年10月推出了用於黏合劑的紙質墨盒,每年可減少120噸塑膠垃圾。歐洲的包裝和包裝廢棄物法規要求到2030年所有包裝都必須可回收利用,這加速了紙板的普及,儘管其成本比聚烯高出4-5倍。

能源價格波動給造紙廠的利潤率帶來了壓力。

電力和天然氣佔造紙廠支出的10%至15%。儘管2025年1月美國天然氣價格平均為每百萬英熱單位3.30美元,遠低於2022年8月9.50美元的尖峰時段,但歐洲的電價仍居高不下。擁有自有發電設施或可再生能源購電協議(PPA)的一體化造紙廠能夠維持利潤率,但受現貨價格影響的獨立回收商則面臨價差收窄的困境。

細分市場分析

預計原生紙漿將以5.93%的複合年成長率成長,這主要得益於液體包裝紙板和固態紙板需求的不斷成長,因為飲料和製藥行業的買家更加注重紙張的白度和抗張強度。 Birelude公司獲得FSC認證的「Enviro-FBB」已與化妝品行業簽訂契約,該行業優先考慮紙張的不透明度,以增強其展示吸引力。 Sappi公司計劃於2024年將其位於薩默塞特的工廠產能擴大52萬短噸,從而增加了美國符合FDA標準的基材供應。雖然再生紙漿將在2025年佔總產量的57.82%,但由於其污染程度高和纖維疲勞問題,其在高亮度應用中的適用性有限。 DS Smith公司致力於在其包裝紙板中使用100%再生纖維,這凸顯了其成本優勢,但就每噸利潤而言,原生紙漿折疊紙板市場仍優於再生紙漿市場。

在單位成本效益至關重要的折疊紙盒紙板領域,再生纖維佔據著主導地位。 Graphic Packaging Co. 80% 的原料來自回收通路,並透過先進的脫墨技術,確保紙張白度達到 ISO 80 或更高。九龍紙業在亞洲擁有 160 個生產基地,在國內和北美地區加工廢棄舊紙板。雖然再生芯紙板預計將在紙板市場保持強勁的市場佔有率,但原生材料的產能預計將在受美國食品藥物管理局 (FDA) 和歐盟食品接觸法規嚴格約束的高階細分市場中創造顯著價值。

受高階化妝品和藥品包裝(尤其注重純白美感)需求的推動,實心漂白紙板 (SBB) 預計將成為成長最快的產品,到 2031 年複合年成長率 (CAGR) 將達到 6.72%。 Sappi 公司位於薩默塞特的工廠擴建直接促進了這一成長,該工廠供應的吸塑卡和食品托盤需要高剛性並獲得 FDA 批准。折疊紙板 (FBB) 因其在穀物、糖果甜點和冷凍食品等廣泛應用領域的多功能性,預計到 2025 年將繼續佔據紙板市場 38.13% 的佔有率。斯道拉恩索 (Stora Enso) 基於 FiberLight 技術的「Performa Nova」產品幫助加工商在不影響彎曲剛度的前提下,減少了 10-15% 的材料用量。

由於Elopak的“天然白紙板”,液體包裝紙板市場蓬勃發展。與寶特瓶相比,這種紙板每單位可減少14%的溫室氣體排放。白底紙板滿足了注重成本的食品產業的需求,而食品服務用紙板則在非洲和亞洲的塑膠禁令下,被用作聚苯乙烯翻蓋式容器的替代品。儘管SBB(單層紙板)成長勢頭強勁,但FBB(纖維增強紙板)預計仍將保持銷量領先地位,因為加工商充分利用了其在剛性、印刷性和圖形表現力方面的出色平衡。

區域分析

預計到2025年,亞太地區將佔全球銷售額的43.62%,主要得益於中國產能成長8%以及印度包裝消費量增加2,400萬噸。當地造紙企業受惠於政府對節能機械的激勵措施,而區域內的回收企業則正在擴大脫墨工藝,以抵消廢舊紙板容器進口限制的影響。日本、韓國和澳洲超過70%的回收率使得FBB級紙板能夠大量使用再生紙漿,從而推動了區域紙板市場的發展。

預計到2031年,非洲將以6.57%的年均成長率實現最快成長。肯亞的塑膠禁令提振了對可折疊紙板的需求,而南非價值25億美元的造紙業也吸引了Mondi和Sappi等公司的大量投資。奈及利亞、埃及和衣索比亞的日常消費品(FMCG)出貨量均實現了兩位數成長,刺激了對能夠承受低溫運輸物流的二次包裝的需求。隨著零售連鎖店的擴張和電子商務的加速發展,包括沙烏地阿拉伯和阿拉伯聯合大公國在內的中東市場預計將以5.8%的速度成長。

在北美和歐洲,生產能力正在重組,同時資本正被投入數位印刷機和阻隔塗層生產線。國際紙業公司計劃在2024年削減100萬噸舊箱板紙產能,而美國包裝公司則斥資18億美元收購了格里夫公司的業務部門,以收緊供應。歐洲的紙張回收率已達72%,這與要求在2030年實現包裝廢棄物可回收的「包裝廢棄物法規」相輔相成。在南美洲,克雷文公司年產90萬噸的PUMA II生產線計畫於2027年運作,這將大大促進南美紙業的發展,而巴西也正成為北美買家的出口樞紐。

其他好處

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 電子商務的發展導致人們對紙板替代品的需求激增。

- 快速消費品產業向無塑膠初級包裝轉型

- 重量輕有助於降低物流成本。

- 區域性禁止使用一次性塑膠製品

- 高速數位印刷技術能夠實現SKU的快速成長。

- 奢侈品市場對豪華折疊紙盒的需求

- 市場限制因素

- 能源價格波動給造紙廠的利潤率帶來了壓力。

- 再生纖維供應長期失衡

- 遵守資本密集型阻隔塗層的相關法規

- 加工商向模塑纖維替代品的過渡

- 監理情勢

- 技術展望

- 投資分析

- 產業價值/價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間的競爭

第5章 市場規模與成長預測

- 材料

- 未使用的纖維

- 再生纖維

- 按產品等級

- 固態漂白板

- 未漂白木板

- 折疊板

- 白線塑合板

- 液體包裝板

- 食品服務委員會

- 按包裝類型

- 折疊紙箱

- 液體包裝

- 袖套和托盤

- 其他

- 按最終用戶行業分類

- 飲料

- 食物

- 醫藥保健

- 化妝品和盥洗用品

- 其他

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 歐洲

- 英國

- 德國

- 法國

- 西班牙

- 義大利

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 肯亞

- 其他非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Asia Pulp & Paper Company Ltd.

- Mayr-Melnhof Karton AG

- Nine Dragons Paper(Holdings)Limited

- Smurfit WestRock

- Graphic Packaging Holding Company

- Stora Enso Oyj

- International Paper Company

- Metsa Board Corporation

- Pankaboard Oyj

- Klabin SA

- Oji Holdings Corporation

- Mondi plc

- Rengo Co., Ltd.

- Lee & Man Paper Manufacturing Ltd.

- Georgia-Pacific LLC

- Clearwater Paper Corporation

- Sappi Limited

- Holmen AB

- DS Smith plc

- Huhtamaki Oyj

第7章 市場機會與未來展望

The cartonboard market size is projected to be USD 76.12 billion in 2025, USD 80.83 billion in 2026, and reach USD 105.96 billion by 2031, growing at a CAGR of 5.56% from 2026 to 2031.

Strong policy pressure for full recyclability, mounting consumer preference for plastic-free packs, and widespread e-commerce lightweighting are steering brand owners toward fiber-based solutions. Folding cartons, sleeves, and liquid packs made from barrier-coated board are displacing rigid polyethylene terephthalate and polypropylene formats, especially in food, beverage, and cosmetics channels. Digital printing presses are unlocking profitable micro-runs for direct-to-consumer brands, while high-yield microfibrillated cellulose enables 10%-15% basis-weight cuts that translate into lower dimensional-weight freight charges. On the supply side, virgin-fiber mills continue to win premium orders in pharmaceuticals and luxury goods, whereas integrated recyclers bank on optical sorting to offset declining bale quality.

Global Cartonboard Market Trends and Insights

E-commerce Corrugated-to-Cartonboard Substitution Surge

Direct-to-consumer networks are trading double-wall corrugated boxes for single-wall cartonboard sleeves that trim parcel mass by 20%-30%, lowering carrier dimensional-weight fees. Amazon and Alibaba now deploy paper void fill in lieu of plastic air pillows, driving 3.9% annual growth in cushioning grades. Nike and Apple redesigned apparel and electronics packs to remove corrugated altogether, opening demand pockets for 200-250 g-per-m2 folding boxboard with adequate stacking strength. The shift is creating fresh revenue for mills able to supply high-bulk, lightweight board in North American and European metro zones where same-day delivery dominates.

FMCG Pivot to Plastic-Free Primary Packaging

Global consumer-goods groups are retrofitting SKUs with dispersion-coated board that preserves grease, moisture, and oxygen barriers without polyethylene layers. Stora Enso's Performa Lumi, released January 2026, offers mineral pigment opacity tailored to beauty labels. Henkel rolled out paper cartridges for adhesives in October 2025, eliminating 120 tons of plastic per year. The European Packaging and Packaging Waste Regulation obliges all packs to be recyclable by 2030, accelerating board uptake despite a 4-5 x unit-cost premium relative to polyolefins.

Energy-Price Volatility Squeezing Mill Margins

Electricity and gas form 10%-15% of mill outlays. U.S. natural gas averaged USD 3.30 per MMBtu in January 2025, far below the USD 9.50 August 2022 peak, yet European power prices remain elevated. Integrated producers with captive generation or renewables PPAs shield margins, whereas stand-alone recyclers exposed to spot rates face compressed spreads.

Other drivers and restraints analyzed in the detailed report include:

- Lightweighting Drives Logistics Cost Savings

- Regional Single-Use-Plastic Bans

- Chronic Recycled-Fiber Supply Imbalance

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Virgin fiber captured rising demand for liquid packaging board and solid bleached board, expanding at a forecast 5.93% CAGR as beverage and pharmaceutical buyers insist on brightness and tensile integrity. Billerud's FSC-certified Enviro-FBB has secured cosmetics contracts that emphasize opacity for shelf appeal. Sappi's 520,000-short-ton Somerset mill addition in 2024 widened U.S. supply of FDA-compliant substrates. Although recycled grades hold 57.82% of 2025 volume, elevated contamination and fiber fatigue hamper their suitability for high-brightness applications. DS Smith's commitment to 100% recycled fiber in containerboard underscores its cost edge, yet the cartonboard market size attached to virgin folds still outpaces recycled in profit per ton.

Recycled fiber maintains leadership in folding boxboard where unit economics dominate, and Graphic Packaging extracts 80% of input from recovered streams while sustaining brightness above 80 ISO through advanced de-inking. Nine Dragons Paper operates 160 Asian sites processing domestic and North American post-consumer bales. The cartonboard market share of recycled medium will stay resilient, but virgin capacity is likely to win incremental value in premium niches subject to stringent FDA or EU food-contact rules.

Solid bleached board (SBB) is projected to clock the fastest 6.72% CAGR to 2031, driven by luxury cosmetics and pharma packs that prize pure-white aesthetics. Sappi's Somerset expansion directly feeds this surge, supplying blister cards and food trays that demand rigidity and FDA clearance. Folding boxboard (FBB) retained a 38.13% slice of the 2025 cartonboard market size owing to its versatility across cereal, confectionery, and frozen meals. Stora Enso's FiberLight-based Performa Nova helped converters shave 10%-15% material use without sacrificing bend stiffness.

Liquid packaging board thrives on Elopak's Natural White Board that trims greenhouse gases by 14% per unit relative to PET bottles. White-lined chipboard services cost-sensitive food sectors, while food service board steps in for polystyrene clamshells under African and Asian plastic bans. Despite SBB's growth momentum, FBB will remain the volume backbone as converters exploit its fine balance of stiffness, runnability, and graphic punch.

The Cartonboard Market Report is Segmented by Material (Virgin Fiber, and Recycled Fiber), Product Grade (Solid Bleached Board, Solid Unbleached Board, Folding Boxboard, and More), Packaging Format (Folding Cartons, Liquid Packaging, Sleeve and Tray, and More), End-User Industry (Beverage, Food, Pharmaceutical and Healthcare, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific generated 43.62% of 2025 revenue, underpinned by China's 8% capacity additions and India's 24 million-t packaging consumption. Local mills benefit from government incentives for energy-efficient machines, and regional recyclers are expanding de-inking to offset import restrictions on old corrugated containers. Japan, South Korea, and Australia post recycling rates above 70%, enabling high substitution of recycled fiber in FBB grades, thereby bolstering the regional cartonboard market.

Africa is projected to expand fastest at 6.57% through 2031. Kenya's plastics ban catalyzes folding carton demand, and South Africa's USD 2.5 billion paper sector attracts Mondi and Sappi investments. Nigeria, Egypt, and Ethiopia record double-digit FMCG volume growth, stimulating need for secondary packs that withstand hot-chain logistics. Middle East markets such as Saudi Arabia and the United Arab Emirates will grow 5.8% as retail chains proliferate and e-commerce accelerates.

North America and Europe are consolidating capacity while funneling capital into digital presses and barrier-coat lines. International Paper removed 1 million t of legacy containerboard in 2024 and Packaging Corporation of America acquired Greif's unit for USD 1.8 billion to tighten supply. Europe's 72% paper recycling rate complements its Packaging Waste Regulation, which obliges recyclability by 2030. South America is buoyed by Klabin's 900,000-t PUMA II line due in 2027, positioning Brazil as an export platform to North Atlantic buyers.

- Asia Pulp & Paper Company Ltd.

- Mayr-Melnhof Karton AG

- Nine Dragons Paper (Holdings) Limited

- Smurfit WestRock

- Graphic Packaging Holding Company

- Stora Enso Oyj

- International Paper Company

- Metsa Board Corporation

- Pankaboard Oyj

- Klabin S.A.

- Oji Holdings Corporation

- Mondi plc

- Rengo Co., Ltd.

- Lee & Man Paper Manufacturing Ltd.

- Georgia-Pacific LLC

- Clearwater Paper Corporation

- Sappi Limited

- Holmen AB

- DS Smith plc

- Huhtamaki Oyj

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 E-commerce Corrugated-to-Cartonboard Substitution Surge

- 4.2.2 FMCG Pivot to Plastic-Free Primary Packaging

- 4.2.3 Lightweighting Drives Logistics Cost Savings

- 4.2.4 Regional Single-Use-Plastic Bans

- 4.2.5 High-Speed Digital Printing Unlocks SKU Proliferation

- 4.2.6 Luxury Goods' Demand for Premium Folding Cartons

- 4.3 Market Restraints

- 4.3.1 Energy-Price Volatility Squeezing Mill Margins

- 4.3.2 Chronic Recycled-Fiber Supply Imbalance

- 4.3.3 Capital-Intensive Barrier Coatings Compliance

- 4.3.4 Converters' Shift to Molded-Fiber Alternatives

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Investment Analysis

- 4.7 Industry Value / Supply-Chain Analysis

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitute Products

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material

- 5.1.1 Virgin Fiber

- 5.1.2 Recycled Fiber

- 5.2 By Product Grade

- 5.2.1 Solid Bleached Board

- 5.2.2 Solid Unbleached Board

- 5.2.3 Folding Boxboard

- 5.2.4 White-Lined Chipboard

- 5.2.5 Liquid Packaging Board

- 5.2.6 Food Service Board

- 5.3 By Packaging Format

- 5.3.1 Folding Cartons

- 5.3.2 Liquid Packaging

- 5.3.3 Sleeve and Tray

- 5.3.4 Other Packaging Format

- 5.4 By End-User Industry

- 5.4.1 Beverage

- 5.4.2 Food

- 5.4.3 Pharmaceutical and Healthcare

- 5.4.4 Cosmetics and Toiletries

- 5.4.5 Other End-User Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Spain

- 5.5.3.5 Italy

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 Australia

- 5.5.4.5 South Korea

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Kenya

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Asia Pulp & Paper Company Ltd.

- 6.4.2 Mayr-Melnhof Karton AG

- 6.4.3 Nine Dragons Paper (Holdings) Limited

- 6.4.4 Smurfit WestRock

- 6.4.5 Graphic Packaging Holding Company

- 6.4.6 Stora Enso Oyj

- 6.4.7 International Paper Company

- 6.4.8 Metsa Board Corporation

- 6.4.9 Pankaboard Oyj

- 6.4.10 Klabin S.A.

- 6.4.11 Oji Holdings Corporation

- 6.4.12 Mondi plc

- 6.4.13 Rengo Co., Ltd.

- 6.4.14 Lee & Man Paper Manufacturing Ltd.

- 6.4.15 Georgia-Pacific LLC

- 6.4.16 Clearwater Paper Corporation

- 6.4.17 Sappi Limited

- 6.4.18 Holmen AB

- 6.4.19 DS Smith plc

- 6.4.20 Huhtamaki Oyj

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

瓦楞紙板製造機械市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、製造能力、應用、地區和競爭格局分類,2021-2031年

瓦楞紙板製造機械市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、製造能力、應用、地區和競爭格局分類,2021-2031年 瓦楞紙板:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)

瓦楞紙板:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年) 瓦楞紙板市場:2026-2032年全球市場預測(按瓦楞類型、產品類型、最終用途產業和分銷管道分類)

瓦楞紙板市場:2026-2032年全球市場預測(按瓦楞類型、產品類型、最終用途產業和分銷管道分類) 全球瓦楞紙包裝市場規模、佔有率、趨勢和成長分析報告(2026-2034年)紙板折疊市場-2026-2031年預測PP鈣塑板市場按材料類型、製造流程、厚度和應用分類-2026-2032年全球預測商用微瓦楞紙市場按產品類型、瓦楞類型、塗層類型、定量、分銷管道、應用和最終用途行業分類-全球預測,2026-2032年

全球瓦楞紙包裝市場規模、佔有率、趨勢和成長分析報告(2026-2034年)紙板折疊市場-2026-2031年預測PP鈣塑板市場按材料類型、製造流程、厚度和應用分類-2026-2032年全球預測商用微瓦楞紙市場按產品類型、瓦楞類型、塗層類型、定量、分銷管道、應用和最終用途行業分類-全球預測,2026-2032年 按類型、產品類型、最終用途產業和地區分類的箱板紙市場規模、佔有率和成長分析 - 2026-2033 年產業預測

按類型、產品類型、最終用途產業和地區分類的箱板紙市場規模、佔有率和成長分析 - 2026-2033 年產業預測 瓦楞紙包裝市場規模、佔有率和成長分析(按瓦楞類型、產品類型、包裝類型、壁結構、終端用戶產業和地區分類)—產業預測(2026-2033 年)

瓦楞紙包裝市場規模、佔有率和成長分析(按瓦楞類型、產品類型、包裝類型、壁結構、終端用戶產業和地區分類)—產業預測(2026-2033 年) 紙托盤:全球市場佔有率和排名、總收入和需求預測(2025-2031年)

紙托盤:全球市場佔有率和排名、總收入和需求預測(2025-2031年)