|

市場調查報告書

商品編碼

2062174

往復式壓縮機:市佔率分析、產業趨勢及統計、成長預測(2026-2031)Reciprocating Compressors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

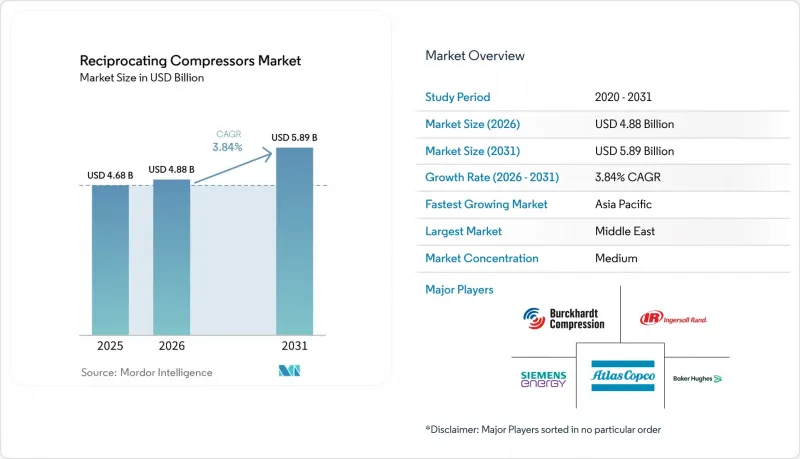

根據 Mordor Intelligence 預測,往復式壓縮機的市場規模預計將從 2025 年的 46.8 億美元和 2026 年的 48.8 億美元成長到 2031 年的 58.9 億美元,2026 年至 2031 年的複合年成長率為 3.84%。

本報告按壓縮機設計(水平對置式、垂直直列式、V型、隔膜式、雙作用式)、潤滑方式(油潤滑、無油潤滑)、級數(單級、兩級、多級)、終端用戶行業(石油天然氣、化工及石化、其他)和地區進行細分。市場預測以美元計價。

全球往復式壓縮機市場趨勢及洞察

液化天然氣液化廠重組

隨著2025年後的最終投資決策陸續訂定,新建液化天然氣工廠的建設也隨之推進,大型往復式壓縮機組因其在蒸發氣再液化和製冷劑應用領域的潛力而再次備受關注。沙烏地阿美公司於2025年2月訂購了六套用於傑夫拉三期計畫的天然氣壓縮裝置,凸顯了中東地區對無油高壓機械的重視。隨後,伯克哈特壓縮公司也訂單,顯示低溫應用領域對無油解決方案的需求日益成長。預計未來幾年,卡達北部油田東部和美國墨西哥灣沿岸地區的擴建計畫訂單。為了實現溫室氣體減排目標,業主擴大指定使用電動馬達驅動,從而減少燃氣引擎主壓縮機固有的甲烷洩漏。隨著供應鏈日益緊張,儲備曲軸和高壓閥門等關鍵零件的供應商獲得了定價權。

氫氣加註基礎設施的建設

歐洲、加州、日本和韓國強制推行的零排放卡車路線,推動了對隔膜式和多級往復式技術的需求成長,這些技術能夠將氫氣從200-500巴的儲存壓力提升至350-700巴的供應壓力。西門子能源公司於2026年1月簽訂的漢堡「綠色氫能中心」合約就是一個典型的例子,該計畫需要無洩漏、無油的壓縮系統。 Hobiger公司的HCP 500隔膜式壓縮機透過消除彈性體失效,將維護間隔延長至8000小時。 Ariel公司已交付超過150台氫氣裝置,最高壓力可達6000 psig,用於加氫和管道注入。由於離心式和螺桿式壓縮機在高揚程下效率降低,往復式壓縮機在這一細分市場中佔據主導地位。因此,預計到2031年,往復式累積訂單將超過整個往復式壓縮機市場的平均值。

原油價格跌破每桶65美元時,深海工程的資本投資將延後。

如果布蘭特原油價格跌破每桶65美元,營運商將凍結深海專案的最終投資決策,並推遲用於氣舉、出口和蒸氣回收服務的壓縮裝置的部署。國際能源總署(IEA)的記錄顯示,在過去的景氣衰退期間,深海項目的核准數量已降至歷史低位,凸顯了原始設備製造商(OEM)累積訂單積壓面臨的宏觀經濟風險。由於浮體式生產儲卸油船(FPSO)需要2-4年的設計前置作業時間,2026年的價格下跌將對2020年代末期的訂單儲備產生連鎖反應。在陸上、石化和氫能相關業務領域中企業發展的供應商可以透過分散風險來降低風險。

細分市場分析

預計到2025年,水平對置式壓縮機將佔市場佔有率的44.19%,並適用於每日總上市數量。由於管道運營商看重此類壓縮機的低振動和簡化的基礎結構,往復式壓縮機的市場佔有率不太可能快速下降。相較之下,隔膜式壓縮機在2025年僅佔市場總規模的一小部分,但隨著氫氣零售站的普及,預計其年複合成長率將達到4.58%。 Hobiger公司生產的額定壓力為500巴的金屬隔膜技術消除了彈性體膜片相關的滲透風險,並正在燃料電池汽車的關鍵應用領域中廣泛應用。 V型和直列式設計適用於機械加工車間和小規模製程裝置的緊湊佈局。對於壓力超過 3,000 psig 的氨和甲醇迴路,雙作用氣壓缸仍然是首選,這表明為什麼沒有單一技術能夠主導往復式壓縮機市場的所有應用。

製藥和半導體產業對空氣純度的嚴格要求(強制要求達到 ISO 8573-1 0 級空氣標準)推動了隔膜壓縮機的應用。在計劃於 2027 年完成流片的亞太地區晶圓廠中,由於螺桿式和渦卷式壓縮機在超過 150 psig 的壓力下性能會下降,因此無油金屬隔膜撬裝式壓縮機更受青睞。為了應對這項挑戰,平衡框架往復式壓縮機的原始設備製造商 (OEM) 正在改進脈動阻尼器並採用數位雙胞胎技術,從而將試運行時間縮短 30%。因此,即使一些成長更快的細分市場也日益受到關注,平衡框架往復式壓縮機的市場規模仍在穩步擴大。

2025年,油潤滑壓縮機將佔總出貨量的63.63%,主要應用於工業空氣供應、中游天然氣集輸和液化天然氣製冷等領域,這些領域對微量碳氫化合物的含量要求不高。然而,食品、飲料和電子產品製造商為了符合0級標準,正日益增加預算,導致無油往復式壓縮機的複合年成長率達到4.23%。布克哈特(Burckhardt)的迷宮活塞「Laby」系列可防止氨再液化過程中的交叉污染。同時,ELGi和CompAir正在推廣聚四氟乙烯(PTFE)密封圈套件,該套件可將油污染控制在測量儀器的檢測極限以下。消費品牌因產品召回而面臨罰款,也解釋了為何這項資本投資成本如此之高。

製造商也在考慮整個生命週期的電力成本。由於無油級排氣溫度較高,許多系統採用中間冷卻器進行熱回收,以降低裝置的淨能耗強度。歐洲和加州碳定價機制的引入,以及現有煉油廠的維修,正在推動往復式壓縮機市場效率的提升。雖然在預測期內,油潤滑裝置仍將是上游和中游設備的主流,但產品藍圖顯然正在朝向乾式密封技術邁進。

區域分析

預計到2025年,亞太地區將佔全球銷售額的42.59%,這主要得益於印度LNG接收站的建設以及中國沿海煉油廠的維修。該地區各國政府正在加強能源效率要求,例如印度能源效率委員會將於2026年收緊壓縮機標準,並推動不合格設備的更換。越南和印尼的工業成長帶動了車間空調的銷售,從而提振了基礎需求。由於國內原始設備製造商(OEM)為規避進口關稅而實現在地化生產,亞太地區往復式壓縮機市場規模依然強勁。

北美市場維持了約28%的市場佔有率,這主要得益於頁岩氣再分餾和聯產氣開採。曲軸和閥門供應鏈的瓶頸推高了設備租賃價格,使持有庫存的現有公司佔優勢。在美國,一條從德克薩斯州到加州的氫氣走廊試點計畫正在進行中,目前已收到700巴隔膜撬裝設備的早期訂單。加拿大的「LNG Canada二期」和「Woodfiber LNG」計畫為未來的成長提供了空間。

預計到2025年,歐洲將佔全球銷售額的約18%,但歐盟指令2000/14/EC對歐洲的噪音法規提出了嚴格要求,限制了聲音功率並強制要求低速設計。雖然對現有設備維修,加裝隔音罩和變速驅動裝置可以使其符合規定,但這會增加單位成本。同時,中東地區預計將以4.44%的複合年成長率成長,卡達的Jaffra、Tajz和North Field East等項目正在加速推進,將無油往復式壓縮機應用於藍氨和氫氣聯合裝置中。在南美洲,巴西鹽層下的開發以及阿根廷Vaca Muerta頁岩氣相關的壓縮裝置正在支撐不斷成長的需求,而非洲的成長則依賴奈米比亞和莫三比克沿海深海油田的發現。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 市場分析與定義的前提條件

- 分析範圍

第2章 分析方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 擴大新建液化天然氣工廠的建設規模(最終投資決定將在2025年後做出)

- 氫氣加註基礎設施的建設

- 頁岩氣再壓裂週期增加(北美洲)

- 現有煉油廠必須進行能源效率改進

- 人工智慧驅動的預測性維護可將運轉率提高 3-5 個百分點。

- OEM廠商向海上FPSO模組化撬裝式組件轉型

- 市場限制因素

- 當原油價格跌破每桶65美元時,對深海計畫的資本投資將會延後。

- 成熟油田從氣舉式採油過渡到電動潛水泵

- 食品和製藥業採用無油螺桿裝置的趨勢

- 嚴格的城市噪音法規(超過 75 分貝 A)限制了這些設備在城市地區的安裝。

- 產業供應鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 宏觀經濟因素對市場的影響

第5章:預測市場規模與成長率

- 壓縮機設計

- 水平對開式

- 垂直序列型

- V型

- 隔膜式

- 雙重角色

- 透過潤滑法

- 油型

- 無油

- 按層數

- 單級

- 兩階段

- 多階段

- 按最終用戶行業分類

- 石油和天然氣

- 化工/石油化工

- 發電

- 製造業和工業

- 暖通空調和製冷

- 其他終端用戶產業(醫療保健、食品和飲料)

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 法國

- 英國

- 義大利

- 西班牙

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太國家

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東國家

- 非洲

- 南非

- 其他非洲國家

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Atlas Copco AB

- Ingersoll Rand Inc.

- Burckhardt Compression AG

- Baker Hughes Company

- Siemens Energy AG

- Elliott Group(Ebara Corporation)

- Howden Group Ltd.(Chart Industries)

- Ariel Corporation

- Hitachi Ltd.

- Kobe Steel Ltd.

- Shenyang Blower Works Group Co. Ltd.

- Kirloskar Pneumatic Company Ltd.

- Mitsui E&S Machinery Co. Ltd.

- Sundyne LLC

- Mayekawa Mfg. Co., Ltd.

- Kaeser Kompressoren SE

- Hanwha Power Systems Co. Ltd.

- Shanghai Screw Compressor Co. Ltd.

- Enerflex Ltd.

- MAN Energy Solutions SE

第7章 市場機會與未來展望

According to Mordor Intelligence, the reciprocating compressors market size is projected to expand from USD 4.68 billion in 2025 and USD 4.88 billion in 2026 to USD 5.89 billion by 2031, registering a 3.84% CAGR between 2026 to 2031.

This report is Segmented by Compressor Design (Horizontal Balanced-Opposed, Vertical In-Line, V-Type, Diaphragm, and Double-Acting), Lubrication (Oil-Lubricated, Oil-Free), Number of Stages (Single-Stage, Two-Stage, and Multi-Stage), End-User Industry (Oil and Gas, Chemicals and Petrochemicals, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Reciprocating Compressors Market Trends and Insights

Renewed LNG Liquefaction Train Build-Out

Large-frame reciprocating packages are returning to favour for boil-off-gas reliquefaction and refrigerant duty as post-2025 final-investment decisions push new LNG trains forward. The February 2025 Saudi Aramco Jafurah Phase 3 award for six gas-compression trains underscores the commitment to oil-free, high-pressure machines in the Middle East. Burckhardt Compression soon followed with Laby 4K165-3 orders for Abu Dhabi's TA'ZIZ terminal, highlighting oil-free demand in cryogenic service. North Field East in Qatar and Gulf Coast expansions in the United States add a multiyear pipeline of orders exceeding 1,000 horsepower per unit. Owners increasingly specify electric-motor drives to meet greenhouse-gas targets, cutting methane slip inherent in gas-engine primaries. As supply chains strain, vendors that stock critical crankshafts and high-pressure valves secure pricing power.

Hydrogen Refuelling Infrastructure Build-Out

Mandated zero-emission truck corridors in Europe, California, Japan, and South Korea are scaling diaphragm and multi-stage reciprocating technology that can raise hydrogen from 200-500 bar storage to 350-700 bar dispensing. Siemens Energy's January 2026 contract for Hamburg's Green Hydrogen Hub typifies projects that need leak-tight, oil-free compression. Hoerbiger's HCP 500 diaphragm model extends service intervals to 8,000 hours by eliminating elastomer failure. Ariel has already shipped more than 150 hydrogen units up to 6,000 psig for refuelling and pipeline injection. Because centrifugal and screw machines lose efficiency at very high heads, reciprocating frames dominate this niche. The resulting order book is on course to outpace the broader reciprocating compressors market through 2031.

Capex Deferments in Deep-Water Projects Below USD 65 per Barrel

When Brent crude slips under USD 65 per barrel, operators freeze deepwater final-investment decisions, postponing compression packages for gas-lift, export, and vapor-recovery service. The International Energy Agency records a historic low in deepwater sanctions during prior downturns, highlighting macro exposure for OEM backlogs. Because floating production, storage, and offloading vessels need two to four years of engineering lead time, price weakness in 2026 would cascade into the late-2020s order funnel. Suppliers with onshore, petrochemical, and hydrogen exposure diversify risk.

Other drivers and restraints analyzed in the detailed report include:

- AI-Enabled Predictive Maintenance Unlocking 3-5 Point Uptime Gains

- Rise in Shale Gas Re-Fracturing Cycles

- Shift from Gas Lift to Electric Submersible Pumps in Mature Fields

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Horizontal balanced-opposed machines commanded 44.19% 2025 revenue, evidencing their suitability for gas gathering volumes above 283,000 m3 per day. The reciprocating compressors market share is unlikely to erode quickly because pipeline operators prize the low vibration and simplified foundation these frames deliver. In contrast, diaphragm units, though just a sliver of 2025 totals, are slated for a 4.58% CAGR as hydrogen retail stations proliferate. Hoerbiger's metal-diaphragm technology, rated 500 bars, removes permeation risks that plague elastomer membranes, expanding acceptance among fuel-cell vehicle corridors. V-type and in-line designs fill compact layouts in machine shops and small process units. Double-acting cylinders, still chosen for ammonia and methanol loops above 3,000 psig, illustrate why no single technology dominates every duty inside the reciprocating compressors market.

Diaphragm expansion is reinforced by stringent purity codes in pharmaceuticals and semiconductors, where ISO 8573-1 Class 0 air is mandatory. Asia-Pacific fabs scheduled for 2027 tape-out favour oil-free metal-diaphragm skids because screw or scroll machines struggle beyond 150 psig. Balanced-opposed OEMs counter with improved pulsation dampers and digital twins that cut commissioning time by 30%. As a result, the reciprocating compressors market size for balanced-opposed frames continues to inch forward even while faster niches steal headlines.

Oil-lubricated variants retained 63.63% volume in 2025, underpinning workshop air, midstream gas gathering, and LNG refrigeration where trace hydrocarbons are tolerated. Yet food, beverage, and electronics plants now budget premium pricing for Class 0 compliance, driving a 4.23% CAGR in oil-free reciprocating compressors. Burckhardt's labyrinth-piston Laby line avoids cross-contamination during ammonia reliquefication, while ELGi and CompAir promote PTFE ring kits that drop oil carryover below instrument-detectable limits. Because consumer-facing brands face product-recall penalties, the capital premium is justified.

Manufacturers also weigh life-cycle electricity costs. Oil-free stages deliver higher discharge temperatures, so many installations integrate intercooler heat recovery that trims net plant energy intensity. The reciprocating compressors market tracks these efficiency gains as brownfield refinery retrofits coincide with carbon-pricing schemes in Europe and California. Although oil-lubricated units will remain the backbone of upstream and midstream fleets for the forecast window, product roadmaps clearly arc toward dry-sealed technologies.

Geography Analysis

Asia-Pacific commanded 42.59% 2025 revenue on LNG terminal builds in India and Chinese coastal refinery upgrades. The region's governments add efficiency mandates India's Bureau of Energy Efficiency tightens compressor standards in 2026 that spur replacement of sub-standard units. Vietnam and Indonesia industrial growth drives workshop air sales, reinforcing baseline demand. The reciprocating compressors market size in Asia-Pacific remains buoyant as domestic OEMs localize production to skirt import duties.

North America held roughly 28% share, underpinned by shale gas re-fracturing and associated gas gathering. Supply-chain pinch points in crankshafts and valves elevate equipment lease rates, advantaging incumbents that carry inventory. The United States also pilot's hydrogen corridors from Texas to California, placing early orders for 700 bar diaphragm skids. Canada's LNG Canada Phase 2 and Woodfibre LNG add future upside.

Europe generated about 18% revenue in 2025 but contends with stringent noise rules under EU Directive 2000/14/EC that cap sound power and force low-speed designs. Retrofitting acoustic wraps and variable-speed drives helps legacy units stay compliant but raises unit cost. Meanwhile, the Middle East, forecast at a 4.44% CAGR, accelerates with Jafurah, TA'ZIZ, and Qatar's North Field East projects that bundle oil-free reciprocating compressors into blue-ammonia and hydrogen complexes. South America's pre-salt developments in Brazil and compression plants linked to Argentina's Vaca Muerta shale underpin incremental demand, while African growth hinges on deepwater discoveries off Namibia and Mozambique.

- Atlas Copco AB

- Ingersoll Rand Inc.

- Burckhardt Compression AG

- Baker Hughes Company

- Siemens Energy AG

- Elliott Group (Ebara Corporation)

- Howden Group Ltd. (Chart Industries)

- Ariel Corporation

- Hitachi Ltd.

- Kobe Steel Ltd.

- Shenyang Blower Works Group Co. Ltd.

- Kirloskar Pneumatic Company Ltd.

- Mitsui E&S Machinery Co. Ltd.

- Sundyne LLC

- Mayekawa Mfg. Co., Ltd.

- Kaeser Kompressoren SE

- Hanwha Power Systems Co. Ltd.

- Shanghai Screw Compressor Co. Ltd.

- Enerflex Ltd.

- MAN Energy Solutions SE

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Renewed LNG Liquefaction Train Build-Out (Post-2025 FIDs)

- 4.2.2 Hydrogen Refuelling Infrastructure Build-Out

- 4.2.3 Rise in Shale Gas Re-Fracturing Cycles (North America)

- 4.2.4 Mandatory Energy-Efficiency Retrofits in Brown-Field Refineries

- 4.2.5 AI-Enabled Predictive Maintenance Unlocking 3-5 pp Uptime Gains

- 4.2.6 OEM Shift to Modular Skid-Mounted Packages for Offshore FPSOs

- 4.3 Market Restraints

- 4.3.1 Capex Deferments in Deep-Water Projects Below USD 65 bbl

- 4.3.2 Shift from Gas Lift to Electric Submersible Pumps in Mature Fields

- 4.3.3 Industrial Move Toward Oil-Free Screw Units in Food and Pharma

- 4.3.4 Stringent Urban Noise Codes Greater Than 75 dB-A Curbing Inner-City Installations

- 4.4 Industry Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Compressor Design

- 5.1.1 Horizontal Balanced-Opposed

- 5.1.2 Vertical In-Line

- 5.1.3 V-Type

- 5.1.4 Diaphragm

- 5.1.5 Double-Acting

- 5.2 By Lubrication

- 5.2.1 Oil-Lubricated

- 5.2.2 Oil-Free

- 5.3 By Number of Stages

- 5.3.1 Single-Stage

- 5.3.2 Two-Stage

- 5.3.3 Multi-Stage

- 5.4 By End-User Industry

- 5.4.1 Oil and Gas

- 5.4.2 Chemicals and Petrochemicals

- 5.4.3 Power Generation

- 5.4.4 Manufacturing and Industrial

- 5.4.5 HVAC and Refrigeration

- 5.4.6 Others End-User Industry (Healthcare, Food and Beverage)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 France

- 5.5.3.3 United Kingdom

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Atlas Copco AB

- 6.4.2 Ingersoll Rand Inc.

- 6.4.3 Burckhardt Compression AG

- 6.4.4 Baker Hughes Company

- 6.4.5 Siemens Energy AG

- 6.4.6 Elliott Group (Ebara Corporation)

- 6.4.7 Howden Group Ltd. (Chart Industries)

- 6.4.8 Ariel Corporation

- 6.4.9 Hitachi Ltd.

- 6.4.10 Kobe Steel Ltd.

- 6.4.11 Shenyang Blower Works Group Co. Ltd.

- 6.4.12 Kirloskar Pneumatic Company Ltd.

- 6.4.13 Mitsui E&S Machinery Co. Ltd.

- 6.4.14 Sundyne LLC

- 6.4.15 Mayekawa Mfg. Co., Ltd.

- 6.4.16 Kaeser Kompressoren SE

- 6.4.17 Hanwha Power Systems Co. Ltd.

- 6.4.18 Shanghai Screw Compressor Co. Ltd.

- 6.4.19 Enerflex Ltd.

- 6.4.20 MAN Energy Solutions SE

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

壓縮機市場:2026-2032年全球市場預測(按類型、驅動系統、潤滑方式、壓力範圍、冷卻方式、級數、移動性、應用和分銷管道分類)

壓縮機市場:2026-2032年全球市場預測(按類型、驅動系統、潤滑方式、壓力範圍、冷卻方式、級數、移動性、應用和分銷管道分類) 汽車空調壓縮機市場規模、佔有率和成長分析:按類型、車輛類型、銷售管道和地區分類-2026-2033年產業預測

汽車空調壓縮機市場規模、佔有率和成長分析:按類型、車輛類型、銷售管道和地區分類-2026-2033年產業預測 2026-2030年全球壓縮機市場

2026-2030年全球壓縮機市場 2026-2030年全球往復式壓縮機市場

2026-2030年全球往復式壓縮機市場 MVR壓縮機:2026-2032年全球市佔率及排名、總營收及需求預測

MVR壓縮機:2026-2032年全球市佔率及排名、總營收及需求預測 全球壓縮機服務市場,2023-2030年

全球壓縮機服務市場,2023-2030年 縱向壓縮變形測量儀器市場預測-全球按類型、測試類型、服務、應用、最終用戶和地區分類的分析——2034年線性斯特林冷卻器市場預測至2034年—按類型、應用、最終用戶和地區分類的全球分析2026-2034年全球液封壓縮機市場規模、佔有率、趨勢及成長分析報告

縱向壓縮變形測量儀器市場預測-全球按類型、測試類型、服務、應用、最終用戶和地區分類的分析——2034年線性斯特林冷卻器市場預測至2034年—按類型、應用、最終用戶和地區分類的全球分析2026-2034年全球液封壓縮機市場規模、佔有率、趨勢及成長分析報告 壓縮機市場:依最終用戶、產品類型和地區分類

壓縮機市場:依最終用戶、產品類型和地區分類