|

市場調查報告書

商品編碼

2062154

射出成型用聚醯胺6:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)Injection Molding Polyamide 6 - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

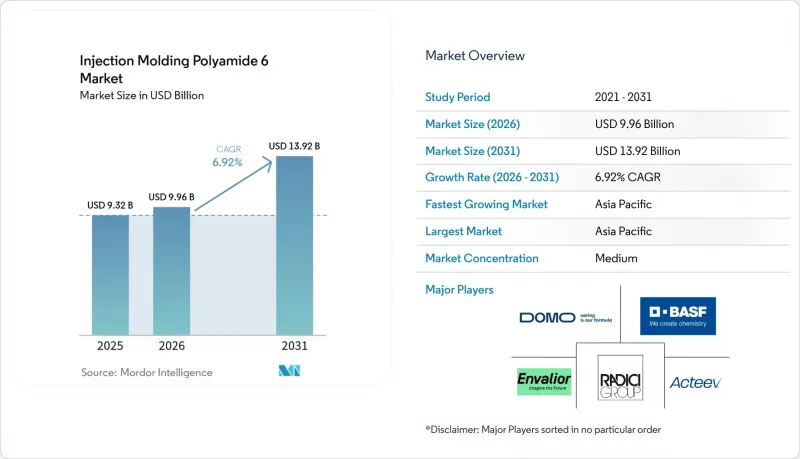

據 Mordor Intelligence 稱,射出成型聚醯胺 6 的市場規模預計將從 2025 年的 93.2 億美元成長到 2026 年的 99.6 億美元,到 2031 年達到 139.2 億美元,預計 2026 年至 2031 年的複合年成長率為 6.92%。

本報告按類型(未填充PA6、礦物填充PA6、其他)、製造方法(標準射出成型、氣體輔助射出成型、其他)、應用領域(汽車零件、電氣和電子設備、其他)以及地區(亞太地區、北美地區、歐洲地區、南美地區、中東和非洲地區)進行細分。市場預測以美元(USD)為單位。

全球射出成型聚醯胺6市場趨勢與洞察

電氣和電子領域元件小型化的發展

隨著800V高壓汽車平臺的擴展,對重量小於1克的連接器和感測器的需求日益成長。這些組件需要達到UL 94 V-0(美國保險商實驗室94垂直阻燃測試)阻燃等級和低於600V的CTI(比較追蹤指數)。玻璃纖維增強PA6級材料始終符合這些標準。BASF的特種聚醯胺「Ultramid Advanced N」於2025年與科斯塔爾汽車公司簽訂契約,將取代液晶聚合物。這顯示此特種聚醯胺能夠在滿足0.03毫米的精確公差的同時,降低約15%的樹脂成本。此外,微型射出成型機閉合迴路注射重量控制技術的進步,使得重複性達到0.5%,最大限度地減少了尺寸公差偏差,並降低了人工返工的需求。

PA6優異的機械和熱性能

未填充的聚醯胺6 (PA6) 的拉伸強度約為85 MPa。添加30%的玻璃纖維後,其強度可提高至170 MPa,使其成為非承重支架中鋁壓鑄件的潛在的輕量化替代方案。東麗株式會社的NANOALLOY改質牌號在維持薄壁成型所需熔體流動性的同時,進一步將拉伸模量提高了25%。此外,與玻璃纖維增強聚丙烯相比,PA6的減振性能可將車內噪音降低高達5分貝(dB)。這項特性被應用於儀錶面板的橫樑。

對化石基聚合物的監管壓力

歐盟將於2025年11月生效的顆粒損耗法規將強制要求設備升級以實現零排放,旨在最大限度地減少對環境的影響。預計這些法規將使中小規模混煉企業的息稅折舊攤提前利潤率(折舊免稅額利潤率)下降至多150個基點。此外,法國和德國的「生產者延伸責任制」(EPR)附加稅加劇了生物基聚醯胺6(PA6)和化學回收聚醯胺6之間的成本競爭,從而促進了後者的應用。

細分市場分析

到2025年,玻璃纖維增強PA6將主導射出成型成型聚醯胺6市場,佔48.11%的市場佔有率。這一成長主要得益於玻璃纖維增強系統在引擎蓋、座椅框架和電池組支架等應用中的廣泛應用,這些應用對彈性模量的要求為8000 MPa或更低,佔比高達30%至50%。同時,礦物填充和抗衝擊增強型聚醯胺6佔據了整體市場的四分之一,在那些優先考慮低翹曲和低溫韌性而非剛性的應用領域中,這類聚醯胺6更受歡迎。射出成型成型聚醯胺6市場的「其他」細分市場(包括碳纖維、生物基和化學回收樹脂)預計將以7.88%的複合年成長率穩步成長,這主要得益於原始設備製造商(OEM)積極推進範圍3排放減排。

正如BASF的Loopamide、Radici集團的BIONSIDE PA610以及UBE的ISCC PLUS認證生物己內醯胺所展現的那樣,原料創新正在重塑先前依賴化石衍生苯的供應鏈。同時,Envario的Durethan FLX-RTM正在旋轉成型壓力容器領域開拓利基市場。這一趨勢凸顯了市場區隔,顯示價值重心正從通用型未填充等級產品朝向滿足耐久性和永續性標準的專用工程解決方案發生明顯轉變。所有這一切都無需經歷傳統認證流程帶來的延誤。

區域分析

預計到2025年,亞太地區將佔全球市場規模的50.11%,並在2031年之前以7.78%的複合年成長率成長。 2025年下半年,中國預計運作一座年產能為92.2萬噸的新工廠,主要出口玻璃纖維增強複合材料,預計出口量將佔總產量的30%至50%。同時,在印度,混合動力汽車和塔內赫的產能擴張正在支持該國的電動車發展計劃,這得益於混合動力和電動車快速部署和製造(FAME)計劃的獎勵。日本和韓國都在將高階奈米改質和生物循環產品商業化,這些產品雖然價格高出20%至30%,但也有助於原始設備製造商(OEM)滿足日益嚴格的碳足跡要求。

在北美,受《通貨膨脹削減法案》(IRA)的推動,電池組件成型業務正呈現出明顯的回流趨勢,例如Ascend公司在阿拉巴馬州擴建了ReDefyne公司的機械回收產能。由於美國生產線的開工率超過85%,塞拉尼斯公司已宣布自2026年2月起對美國市場徵收每公斤0.25美元的額外運轉率。同時,根據《美墨加協定》(USMCA),加拿大汽車零件貿易正透過確保向美國穩定供應聚醯胺6(PA6)進氣歧管和冷卻液儲罐,加強雙邊供應鏈。

在歐洲,各公司在材料開發方面保持主導,同時有效控制了與顆粒損耗和生產者延伸責任制 (EPR)課稅相關的成本。BASF全面收購 Alsachimie 合資企業就是一個典型的例子,此舉確保了己二酸和六亞甲基二胺 (HMD) 前體在歐洲的穩定供應。德國原始設備製造商 (OEM) 在採用再生材料方面處於主導,目標是在 2028 年前達到永續產品生態設計法規 (ESPR) 規定的 25% 標準。相較之下,英國採用不同的標準,導致合規評估週期更長。在拉丁美洲,重點是引擎罩,並利用來自巴西的耐乙醇配方。同時,中東和非洲的需求雖然仍處於起步階段,但由於沙烏地阿拉伯的電動車組裝和南非的採礦機械需求,這些地區的需求正在成長。

其他好處

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 電子電氣領域小型化元件的成長

- PA6優異的機械和熱性能

- 亞洲擴大玻璃纖維增強材料產能

- 採用電動車電池機殼和電力驅動橋殼體

- 快速加熱和薄壁成型技術正在推動PA6的普及應用。

- 市場限制因素

- 對化石基聚合物的監管壓力

- 微射出成型廢品率的敏感度

- PA66 在引擎室內零件中熱裕度低,溫度超過 150 度C。

- 價值鏈分析

- 波特五力模型

第5章 市場規模與成長預測

- 按類型

- 未填充的PA6

- 玻璃纖維增強PA6

- 礦物填充PA6

- 抗衝擊性 PA6

- 其他類型(碳纖維、生物基、再生纖維)

- 透過加工方法

- 標準射出成型

- 氣體輔助射出成型

- 微型射出成型

- 其他加工方法(液壓輔助、金屬嵌件)

- 透過使用

- 汽車零件

- 電氣和電子設備

- 工業機械和設備

- 消費品(電動工具、家用電器)

- 其他用途(包裝等)

- 按地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- ASEAN

- 其他亞太國家

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐國家

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲國家

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- Arkema

- Asahi Kasei Corporation

- Ascend Performance Materials

- BASF

- Celanese Corporation

- Domo Chemicals

- EMS-CHEMIE HOLDING AG

- Ensinger

- Envalior

- Evonik Industries AG

- Kingfa Sci.& Tech. Co.,Ltd.

- LG Chem

- Mitsui Chemicals, Inc.

- Radici Partecipazioni SpA

- RTP Company

- SABIC

- Solvay

- Toray Industries, Inc.

- UBE Corp.

第7章 市場機會與未來展望

According to Mordor Intelligence, the injection molding polyamide 6 market size is expected to increase from USD 9.32 billion in 2025 to USD 9.96 billion in 2026 and reach USD 13.92 billion by 2031, growing at a CAGR of 6.92% over 2026-2031.

This report is Segmented by Type (Unfilled PA6, Mineral-Filled PA6, and More), Processing Method (Standard Injection Molding, Gas-Assisted Injection Molding, and More), Application (Automotive Components, Electrical and Electronics, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Injection Molding Polyamide 6 Market Trends and Insights

Growth in E&E Miniaturized Components

As high-voltage 800-V vehicle platforms expand, the demand for sub-gram connectors and sensors is increasing. These components require a UL 94 V-0 (Underwriters Laboratories 94 Vertical Burning Test) flame rating and a CTI (Comparative Tracking Index) of less than or equal to 600 V. Glass-fiber-reinforced PA6 grades consistently meet these standards. BASF's Ultramid Advanced N, a specialty polyamide, secured contracts in 2025 with KOSTAL Automotive, replacing liquid-crystal polymer. This demonstrates the ability of specialty polyamides to meet precise 0.03 mm tolerance windows while reducing resin costs by approximately 15%. Additionally, advancements in closed-loop shot-weight control within micro-injection presses now achieve 0.5% repeatability, minimizing dimensional drift and reducing the need for manual rework.

Excellent Mechanical and Thermal Profile of PA6

Unfilled Polyamide 6 (PA6) has a tensile strength of approximately 85 MPa. With a 30% glass loading, this strength increases to 170 MPa, making it a potential lightweight alternative to aluminum die-castings in non-load-bearing brackets. Toray's NANOALLOY-modified grades enhance the tensile modulus by an additional 25%, while maintaining the melt flow required for thin-wall molding. Additionally, PA6's vibration-damping capability reduces interior noise by up to 5 decibels (dB) compared to glass-filled polypropylene. This feature is utilized in instrument-panel cross-car beams.

Regulatory Pressure on Fossil-Based Polymers

Effective November 2025, the European Union's (EU) pellet-loss rule requires zero-discharge upgrades, aimed at minimizing environmental impact. This regulation is projected to reduce Earnings Before Interest, Taxes, Depreciation, and Amortization (EBITDA) margins for smaller compounders by up to 150 basis points. Furthermore, Extended Producer Responsibility (EPR) fees in France and Germany are driving the adoption of bio-based and chemically recycled polyamide 6 (PA6) by making it more cost-competitive.

Other drivers and restraints analyzed in the detailed report include:

- Capacity Expansions in Asia for Glass-Filled Grades

- Adoption in EV Battery Enclosures and E-Axle Housings

- Scrap-Rate Sensitivity in Micro-Injection Molding

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, glass-fiber-reinforced PA6 dominated the injection molding polyamide 6 market, seizing a 48.11% share. This surge was driven by the adoption of 30%-50% glass systems in applications like engine covers, seat frames, and battery-pack brackets, all demanding a modulus of less than or equal to 8,000 MPa. Meanwhile, mineral-filled and impact-modified variants carved out a combined quarter of the market, favored in applications prioritizing low warpage or cold-temperature toughness over stiffness. The other types segment of the injection molding polyamide 6 market, encompassing carbon-fiber, bio-based, and chemically recycled resins, is set to grow at a robust 7.88% CAGR, as OEMs aggressively pursue Scope-3 emission reductions.

Innovations in feedstock are reshaping supply chains, previously tethered to fossil benzene, as seen with BASF's loopamid, RadiciGroup's BIONSIDE PA610, and UBE's ISCC PLUS-certified bio-caprolactam. Concurrently, Envalior's Durethan FLX-RTM is carving out niches in rotational-molded pressure vessels. This trend underscores a market fragmentation, with a clear shift in value from generic unfilled grades to specialized engineered solutions that meet durability and sustainability benchmarks, all without the typical requalification holdups.

Geography Analysis

Asia-Pacific, accounting for 50.11% of the 2025 volume, is projected to grow at a 7.78% compound annual growth rate (CAGR) through 2031. In late 2025, China will activate new plants with a capacity of 922 kilotons per year, primarily focusing on exporting 30-50% glass compounds. Meanwhile, India's capacity expansions in Panoli and Thane are supporting domestic electric vehicle (EV) initiatives, driven by incentives from the Faster Adoption and Manufacturing of Hybrid and Electric Vehicles (FAME) scheme. Both Japan and South Korea are commercializing premium nano-modified and bio-circular variants, which, while commanding a 20-30% price uplift, also address the tightening carbon footprints of original equipment manufacturers (OEMs).

In North America, the reshoring of battery-component molding, spurred by the Inflation Reduction Act (IRA), is evident with Ascend's expansion of the ReDefyne mechanical-recycling capacity in Alabama. U.S. production lines are operating at over 85% utilization, leading Celanese to impose a USD 0.25 per kilogram surcharge in February 2026. Meanwhile, Canada's auto-parts trade, aligned with the United States-Mexico-Canada Agreement (USMCA), ensures a steady flow of polyamide 6 (PA6) intake manifolds and coolant reservoirs to the U.S., solidifying binational supply chains.

Europe, while managing costs from pellet-loss and extended producer responsibility (EPR) levies, maintains its leadership in material development. This is exemplified by BASF's complete acquisition of the Alsachimie joint venture, securing adipic acid and hexamethylenediamine (HMD) precursors within the bloc. German OEMs are leading the adoption of recycled content, aiming to meet the Ecodesign for Sustainable Products Regulation (ESPR)'s 25% threshold by 2028. In contrast, the UK's differing standards are extending qualification cycles. Latin America, with a focus on engine covers, is leveraging Brazil's ethanol-resistant formulations. Meanwhile, demand in the Middle East and Africa, though still in its early stages, is increasing with Saudi Arabia's EV assembly and South Africa's mining equipment.

- Arkema

- Asahi Kasei Corporation

- Ascend Performance Materials

- BASF

- Celanese Corporation

- Domo Chemicals

- EMS-CHEMIE HOLDING AG

- Ensinger

- Envalior

- Evonik Industries AG

- Kingfa Sci.&Tech. Co.,Ltd.

- LG Chem

- Mitsui Chemicals, Inc.

- Radici Partecipazioni SpA

- RTP Company

- SABIC

- Solvay

- Toray Industries, Inc.

- UBE Corp.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growth in E&E miniaturised components

- 4.2.2 Excellent mechanical and thermal profile of PA6

- 4.2.3 Capacity expansions in Asia for glass-filled grades

- 4.2.4 Adoption in EV battery enclosures and e-axle housings

- 4.2.5 Rapid-heating thin-wall molding technologies boosting PA6 penetration

- 4.3 Market Restraints

- 4.3.1 Regulatory pressure on fossil-based polymers

- 4.3.2 Scrap-rate sensitivity in micro-injection molding

- 4.3.3 Low thermal margin vs PA66 for >150 °C under-hood parts

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Unfilled PA6

- 5.1.2 Glass-fiber-reinforced PA6

- 5.1.3 Mineral-filled PA6

- 5.1.4 Impact-modified PA6

- 5.1.5 Other Types (carbon-fiber, bio-based, recycled)

- 5.2 By Processing Method

- 5.2.1 Standard injection molding

- 5.2.2 Gas-assisted injection molding

- 5.2.3 Micro-injection molding

- 5.2.4 Other Processing Methods (water-assist, metal-insert)

- 5.3 By Application

- 5.3.1 Automotive Components

- 5.3.2 Electrical and Electronics

- 5.3.3 Industrial Machinery and Equipment

- 5.3.4 Consumer Goods (power tools, appliances)

- 5.3.5 Other Applications (Packaging, etc.)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 Japan

- 5.4.1.3 India

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 NORDIC Countries

- 5.4.3.8 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Arkema

- 6.4.2 Asahi Kasei Corporation

- 6.4.3 Ascend Performance Materials

- 6.4.4 BASF

- 6.4.5 Celanese Corporation

- 6.4.6 Domo Chemicals

- 6.4.7 EMS-CHEMIE HOLDING AG

- 6.4.8 Ensinger

- 6.4.9 Envalior

- 6.4.10 Evonik Industries AG

- 6.4.11 Kingfa Sci.&Tech. Co.,Ltd.

- 6.4.12 LG Chem

- 6.4.13 Mitsui Chemicals, Inc.

- 6.4.14 Radici Partecipazioni SpA

- 6.4.15 RTP Company

- 6.4.16 SABIC

- 6.4.17 Solvay

- 6.4.18 Toray Industries, Inc.

- 6.4.19 UBE Corp.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

尼龍6長絲紗線市場規模、佔有率和成長分析:按類型、應用和地區分類-2026-2033年產業預測

尼龍6長絲紗線市場規模、佔有率和成長分析:按類型、應用和地區分類-2026-2033年產業預測 尼龍6絲紗線:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)

尼龍6絲紗線:市佔率分析、產業趨勢與統計、成長預測(2026-2031年) 尼龍6市場:依產品形式、原料/供應來源、應用及地區分類

尼龍6市場:依產品形式、原料/供應來源、應用及地區分類 射出成型用聚醯胺6市場:依增強類型、等級類型、應用、最終用途零件和銷售管道分類-2026-2032年全球市場預測聚醯胺6市場:依聚合物類型、等級和最終用途產業分類-2026-2032年全球市場預測

射出成型用聚醯胺6市場:依增強類型、等級類型、應用、最終用途零件和銷售管道分類-2026-2032年全球市場預測聚醯胺6市場:依聚合物類型、等級和最終用途產業分類-2026-2032年全球市場預測 全球射出成型聚醯胺6市場報告(2026年)

全球射出成型聚醯胺6市場報告(2026年) PA 66/6 市場規模、佔有率和成長分析(按類型、應用和地區分類)—2026-2033 年產業預測

PA 66/6 市場規模、佔有率和成長分析(按類型、應用和地區分類)—2026-2033 年產業預測 尼龍6長絲的全球市場

尼龍6長絲的全球市場 全球聚醯胺 6 市場規模(按類型、等級、應用、地區、範圍和預測)

全球聚醯胺 6 市場規模(按類型、等級、應用、地區、範圍和預測) 聚□胺 6 全球市場分析:工廠產能、產量、運營效率、需求/供應、最終用戶行業、銷售渠道、區域需求、公司份額 (2015-2035)

聚□胺 6 全球市場分析:工廠產能、產量、運營效率、需求/供應、最終用戶行業、銷售渠道、區域需求、公司份額 (2015-2035)