|

市場調查報告書

商品編碼

2062122

尼龍6絲紗線:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)Nylon 6 Filament Yarn - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

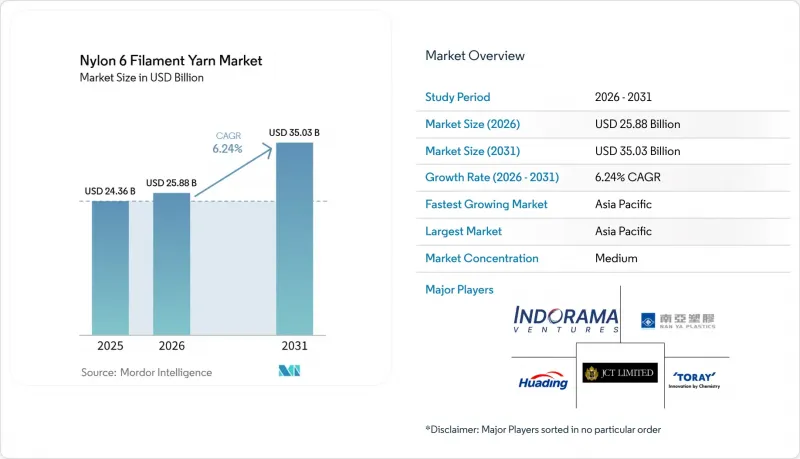

據 Mordor Intelligence 稱,2025 年尼龍 6 長絲紗線市場價值為 243.6 億美元,預計到 2031 年將達到 350.3 億美元,而 2026 年為 258.8 億美元,預測期(2026-2031 年)複合年成長率為 6.4%。

本報告按紗線類型(POY、FDY 及其他)、應用領域(布料、運動服裝及其他)、配銷通路(紡織品公司/批發商及其他)、終端用戶行業(服裝時尚、工業和技術紡織品及其他)以及地區(亞太地區、北美地區、歐洲地區、南美地區、中東和非洲地區)進行細分。市場預測以美元計價。

全球尼龍6長絲紗線市場趨勢及洞察

工業纖維的擴張

汽車製造商正在選擇尼龍6長絲,其強度高於尼龍6,6,用於某些安全氣囊織物。這項決定源自於需要在縮短聚合週期和降低材料成本的優勢與略微降低的強度之間取得平衡。在泰國,由東洋紡和Indorama營運的一家工廠每年生產11,000噸安全氣囊紗線,正在縮短東南亞各地原始設備製造商(OEM)的交貨前置作業時間。 AdvanSix的低熔體黏度樹脂可將引擎室零件的射出成型週期縮短高達40%,滿足電動車的輕量化要求。尼龍6單絲因其耐磨性而備受青睞,正被用作工業過濾,可承受反覆反沖洗循環並符合ISO 11057標準。此外,OSHA 1926的修訂版現在建議在安全網中使用紫外線穩定尼龍6。成長主要集中在美國、德國和中國的汽車工業中心。在這些地區,接近性工程中心正在推動以規範主導的應用。

亞洲城市自行車共享和電動滑板車包的快速成長

在中國、印度和整個東南亞地區,輕質210-420丹尼爾布料正日益被應用於市政微型交通工具計畫。這些布料可承受500次以上的洗滌,主要採用溶液染色尼龍6長絲。美團和Hello等公司正在推動對抗紫外線布料的需求,以確保其與用於品牌標誌的數位印刷相容。為此,中國長三角Delta的加工商已建立了專用織布機生產線。在印度,印度標準局(BIS)標準IS 15061建議使用阻燃複合材料,尤其是在電池儲存外殼方面。此外,中等丹尼爾POY布料的生產商能夠透過通常12-18個月的供貨合約來維持穩定的供貨量。

聚酯和聚丙烯的具有成本競爭力的替代品

目前,吸濕排汗性能與尼龍6相當的聚酯纖維,成本卻低15-20%。這種成本差異使得尼龍在中端運動服市場難以維持其市場佔有率。在印度,預計到2024年,尼龍單絲的進口量將年減18%,顯示來自聚丙烯的競爭日益激烈。由於密度較低,聚丙烯在地工織物和刷毛等應用中正逐漸被尼龍6取代。此外,再生聚酯纖維的價格與非再生聚酯纖維相當,而再生尼龍6的價格卻高出30-50%,這構成了一個重要的限制因素。這種價格差異限制了再生尼龍6的應用,使其主要局限於高階市場。

細分市場分析

到2025年,部分拉伸紗線將佔尼龍6長絲紗線市場的31.11%,這主要得益於其在下游加工中具有的柔軟性變形優勢。由於襪子和拉伸布料對蓬鬆度和捲曲度控制的需求,預計該細分市場將以6.31%的複合年成長率成長。全拉伸紗線(FDY)在中國運作噴射織布機的綜合紡紗廠中越來越受歡迎,與部分拉伸紗線(POY)變形製程相比,可降低12-18%的能耗。高強度等級的FDY紗線用於輪胎簾布和安全氣囊織物,這些應用需要8.5克/丹尼爾或更高的強度。

為滿足日益成長的產業用紡織品需求,中國生產商正將新增產能投入FDY和高強度生產線;同時,台灣紡紗廠則專注於為高階戶外品牌生產10旦及以下纖度的超細纖維。自動化和工業4.0控制技術能夠即時監測拉伸和縮水率,從而減少5-7%的不合格廢棄物。然而,POY(聚酯捲曲紗)尼龍6長絲紗的市場規模仍佔據主導地位,這反映出亞洲各地獨立加撚企業的強大基礎設施。

預計到2025年,織物應用將佔市場佔有率的38.89%。然而,由於聚酯纖維的替代率不斷提高,其成長受到限制。運動探險裝備領域預計將以6.45%的複合年成長率成長。這一成長歸功於尼龍的耐磨性,這使得尼龍在超輕帳篷、背包和安全帶等應用中的價格比聚酯纖維高出25%至40%。在監管嚴格的漁網細分市場,為符合歐盟和日本製定的永續發展要求,使用再生材料正逐漸成為強制性要求。

由於高階品牌提供的7-15丹尼布料符合ASTM D5034撕裂強度標準(40牛頓或更高),市場需求不斷成長。這一趨勢帶動了對全拉伸和紫外線穩定紗線的需求增加。同時,旅行配件領域正在採用溶液染色420-840丹尼長絲。這些長絲可實現大規模客製化的數位印花,從而將前置作業時間縮短30-40%。與運動和探險裝備相關的尼龍6長絲紗線市場規模仍然相對較小,但持續成長。此外,與通用布料相比,該領域的利潤率更高。

區域分析

預計到2025年,亞太地區將佔全球整體的51.12%,年複合成長率達6.36%。中國江蘇和浙江兩省的綜合性產業中心提供的加工成本比其他地區低15%至20%。此外,越南和泰國正崛起為中國企業尋求免稅進入西方輪胎市場的關鍵樞紐。在印度,蘇拉特和蒂爾普爾的紡紗產業叢集正在努力現代化,但該國仍依賴進口來滿足對特種紗線的需求。

在北美,由於BASF和Fibrant工廠的關閉,己內醯胺的供不應求面臨挑戰,並加劇了該地區對進口的依賴。受《國際武器貿易條例》(ITAR)的限制,用於安全氣囊和國防應用的高強度紗線的國內產量保持穩定。然而,受加拿大和墨西哥加工商在《美國-墨西哥-加拿大協定》(USMCA)規則下運作的影響,時尚長絲的供應正轉向亞洲。在歐洲,市場日益兩極化,一方面是像Aquafil的ECONYL這樣的高階圓形紗線,另一方面是因排放交易體系(ETS)成本而萎縮的通用產品。此外,土耳其的保障性關稅也影響出口目的地,導致亞洲以外的地區減少。

在南美,市場呈現溫和成長態勢,主要受巴西汽車產業和運動服飾需求成長的推動。然而,該地區仍依賴亞洲供應商提供特殊長絲。在中東和非洲,沙烏地阿拉伯的早期計畫正利用低成本氣態原料的供應優勢。儘管擁有這一優勢,該地區仍面臨技術純熟勞工短缺和供應鏈效率低下等挑戰,這些挑戰限制了專案的規模化發展。因此,尼龍6長絲紗線市場仍集中在亞洲,而歐洲和北美則專注於開發以永續性和可追溯性為重點的細分市場。

其他好處

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 技術紡織品(安全、過濾、安全氣囊)的拓展

- 亞洲都市區自行車共享和電動滑板車包市場快速成長

- 漁業及水產養殖網具現代化改造計劃

- 高階戶外裝備中使用低丹尼爾超細纖維

- 企業循環經濟目標正在推動再生尼龍 6 的採購。

- 市場限制因素

- 聚酯和聚丙烯的具有成本競爭力的替代品

- 高溫聚合反應中的碳定價與脫碳資本投資

- 化學回收原料的設備瓶頸

- 價值鏈分析

- 波特五力模型

第5章 市場規模與成長預測

- 依紗線類型

- POY(部分拉伸紗線)

- FDY(全拉伸紗線)

- 高強度工業紗線

- 紋理紗線

- 透過使用

- 織物

- 運動服裝

- 運動和探險裝備

- 旅行配件

- 魚網

- 透過分銷管道

- 紡織品公司和批發商

- 直接銷售(給紡紗廠)

- 電子商務平台

- 按最終用戶行業分類

- 服裝與時尚

- 工業和技術纖維

- 汽車零件

- 消費品

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 越南

- 馬來西亞

- 其他亞太國家

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 北歐國家

- 俄羅斯

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 哥倫比亞

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

- 其他中東和非洲國家

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- Aquafil SpA

- Anand Rayons Ltd.

- Changzhou Yida Chemical Fiber

- East Asia Textile Technology

- Indorama Ventures PCL

- JCT Ltd.

- NanYa Plastics Corp.

- Prutex Nylon Co., Ltd.

- Salud Industry(Dongguan)Co., Ltd.

- Singhal Industries Pvt.

- Toray Industries Inc.

- Universal Fibers, Inc.

- Yiwu Huading Nylon

- Zhejiang Century ChenXing Fiber Technology

第7章 市場機會與未來展望

According to Mordor Intelligence, the nylon 6 filament yarn market size was valued at USD 24.36 billion in 2025 and is estimated to grow from USD 25.88 billion in 2026 to reach USD 35.03 billion by 2031, at a CAGR of 6.24% during the forecast period (2026-2031).

This report is Segmented by Yarn Type (POY, FDY, and More), Application (Fabric, Sports Apparel, and More), Distribution Channel (Textile Traders/Distributors, and More), End-User Industry (Apparel & Fashion, Industrial and Technical Textiles, and More), and Geography (Asia-Pacific, North America, Europe, South America, Middle-East and Africa). Market Forecasts are Provided in Terms of Value (USD).

Global Nylon 6 Filament Yarn Market Trends and Insights

Expansion of Technical Textiles

Automakers are choosing high-tenacity Nylon 6 filaments over Nylon 6,6 in certain airbag fabrics. This decision is driven by the need to balance slightly lower strength with faster polymerization cycles and reduced material costs. In Thailand, Toyobo and Indorama's facility, producing 11,000 tons per year of airbag yarn, is reducing lead times for OEMs across Southeast Asia. AdvanSix's resins, with low melt viscosity, are reducing injection-molding cycles by up to 40% for under-hood components, aligning with the lightweighting requirements of electric vehicles. Nylon 6 monofilament, valued for its abrasion resistance, is being specified for industrial filtration media during repeated back-wash cycles, meeting ISO 11057 standards. Additionally, updates from OSHA 1926 now recommend UV-stabilized Nylon 6 for safety netting. Growth is focused around automotive hubs in the U.S., Germany, and China, where proximity to engineering centers supports specification-driven adoption.

Rapid Growth in Asian Urban Bike-Sharing and E-Scooter Bags

Across China, India, and Southeast Asia, municipal micro-mobility programs are increasingly adopting lightweight 210-420 denier fabrics. These fabrics, which can withstand over 500 wash cycles, are primarily using solution-dyed Nylon 6 filament. Operators such as Meituan and Hello are driving demand for UV-resistant grades to ensure compatibility with digital printing for branding purposes. In response, converters in China's Yangtze River Delta have set up dedicated weaving lines. In India, the Bureau of Indian Standards IS 15061 is encouraging the use of flame-retardant blends, particularly for battery enclosures. Furthermore, supply contracts, typically lasting 12-18 months, are enabling mid-denier POY producers to maintain a steady off-take.

Cost-Competitive Polyester and Polypropylene Substitutions

Polyester, which now matches Nylon 6 in moisture-wicking capabilities, achieves this at a cost that is 15 to 20 percent lower. This cost difference is creating challenges for Nylon in retaining its share within the mid-tier activewear market. In India, a year-on-year decline of 18 percent in Nylon monofilament imports in 2024 indicates increasing competition from Polypropylene. Due to its lower density, Polypropylene is gradually replacing Nylon 6 in applications such as geotextiles and brush bristles. Additionally, while recycled polyester has achieved cost parity with its non-recycled counterpart, the higher cost of recycled Nylon 6, which is 30 to 50 percent more expensive, acts as a significant restraint. This price disparity is limiting its adoption primarily to premium market segments.

Other drivers and restraints analyzed in the detailed report include:

- Fishing and Aquaculture Net Modernization Programs

- Low-Denier Micro-Filament Adoption in Premium Outdoor Gear

- Carbon-Pricing and Decarbonization CAPEX

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Partially oriented yarn accounted for 31.11% of the Nylon 6 filament yarn market in 2025, benefiting from flexibility in downstream texturing. The segment is expected to rise at a 6.31% CAGR as hosiery and stretch fabrics demand controlled bulk and crimp. Fully drawn yarn is gaining traction in integrated Chinese mills feeding air-jet looms, trimming energy use 12-18% versus POY-texturing routes. High-tenacity grades serve tire cord and airbag fabrics where greater than 8.5 g/denier strength is mandatory.

Chinese producers are allocating fresh capacity toward FDY and high-tenacity lines to capture rising technical-textile demand, while Taiwanese mills specialize in sub-10 denier micro-filament for premium outdoor brands. Automation and Industry 4.0 controls now allow real-time monitoring of draw ratio and shrinkage, reducing off-grade waste by 5-7%. However, the Nylon 6 filament yarn market size for POY still dwarfs other yarns, reflecting the entrenched infrastructure of independent texturizers across Asia.

In 2025, fabric applications accounted for 38.89% of the market share. However, their growth has been limited due to the increasing substitution of polyester. The sports and adventure equipment segment is anticipated to grow at a compound annual growth rate (CAGR) of 6.45%. This growth is attributed to the abrasion resistance of nylon, which justifies a price premium of 25-40% over polyester in applications such as ultralight tents, backpacks, and harnesses. The fishing nets segment, which operates within a regulated niche, is progressively specifying recycled content to comply with sustainability mandates established by the European Union and Japan.

The demand for 7-15 denier fabrics, commissioned by premium brands, is increasing as these fabrics meet the ASTM D5034≥40 N tear strength standard. This trend is driving the need for fully drawn and UV-stabilized yarns. In parallel, the travel accessories segment is adopting solution-dyed 420-840 denier filaments. These filaments enable mass-customized digital prints and reduce lead times by 30-40%. The market size for Nylon 6 filament yarn associated with sports and adventure gear remains relatively small but is experiencing growth. Additionally, this segment offers higher margins compared to commodity fabrics.

Geography Analysis

In 2025, Asia-Pacific accounted for 51.12% of the global volume and is projected to grow at a compound annual growth rate (CAGR) of 6.36%. China's integrated hubs in Jiangsu and Zhejiang offer conversion costs that are 15-20% lower compared to other regions. Additionally, Vietnam and Thailand are emerging as key destinations for Chinese firms seeking tariff-free access to Western tire markets. In India, efforts are underway to upgrade the Surat and Tirupur spinning clusters; however, the country continues to rely on imports to meet its demand for specialty yarns.

North America faces challenges due to a caprolactam deficit, which arose after the closures of BASF and Fibrant facilities. This has increased the region's dependence on imports. Domestic production of high-tenacity yarns, which are essential for airbags and defense applications, remains stable due to International Traffic in Arms Regulations (ITAR) restrictions. However, the sourcing of fashion-grade filaments is shifting toward Asia, facilitated by Canadian and Mexican converters operating under the United States-Mexico-Canada Agreement (USMCA) rules. In Europe, the market is divided between premium circular yarns, such as Aquafil's ECONYL, and a declining commodity production segment that is burdened by Emissions Trading System (ETS) costs. Furthermore, Turkey's safeguard duties are influencing the redirection of Asian exports.

In South America, the market is experiencing modest growth, primarily driven by Brazil's automotive sector and an increasing demand for activewear. However, the region remains dependent on Asian suppliers for specialty filaments. In the Middle East and Africa, early-stage projects in Saudi Arabia are leveraging the availability of low-cost gas feedstocks. Despite this advantage, the region faces obstacles such as a shortage of skilled labor and inefficiencies in the supply chain, which are limiting the scalability of these projects. Consequently, the Nylon 6 filament yarn market continues to be concentrated in Asia, while Europe and North America focus on developing niches that emphasize sustainability and traceability.

- Aquafil S.p.A.

- Anand Rayons Ltd.

- Changzhou Yida Chemical Fiber

- East Asia Textile Technology

- Indorama Ventures PCL

- JCT Ltd.

- NanYa Plastics Corp.

- Prutex Nylon Co., Ltd.

- Salud Industry (Dongguan) Co., Ltd.

- Singhal Industries Pvt.

- Toray Industries Inc.

- Universal Fibers, Inc.

- Yiwu Huading Nylon

- Zhejiang Century ChenXing Fiber Technology

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expansion of technical textiles (safety, filtration, airbags)

- 4.2.2 Rapid growth in Asian urban bike-sharing and e-scooter bags

- 4.2.3 Fishing and aquaculture net modernization programs

- 4.2.4 Low-denier micro-filament adoption in premium outdoor gear

- 4.2.5 Corporate circularity targets driving recycled Nylon 6 procurement

- 4.3 Market Restraints

- 4.3.1 Cost-competitive polyester and polypropylene substitutions

- 4.3.2 Carbon-pricing and decarbonisation CAPEX for high-temperature polymerisation

- 4.3.3 Equipment bottlenecks for chemical recycling feedstock

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of Substitution

- 4.5.4 Threat of New Entrants

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Yarn Type

- 5.1.1 Partially Oriented Yarn (POY)

- 5.1.2 Fully Drawn Yarn (FDY)

- 5.1.3 High-Tenacity Industrial Yarn

- 5.1.4 Textured Yarn

- 5.2 By Application

- 5.2.1 Fabric

- 5.2.2 Sports Apparel

- 5.2.3 Sports and Adventure Equipment

- 5.2.4 Travel Accessories

- 5.2.5 Fishing Nets

- 5.3 By Distribution Channel

- 5.3.1 Textile Traders / Distributors

- 5.3.2 Direct Sales (Spinners)

- 5.3.3 E-commerce Platforms

- 5.4 By End-user Industry

- 5.4.1 Apparel and Fashion

- 5.4.2 Industrial and Technical Textiles

- 5.4.3 Automotive Components

- 5.4.4 Consumer Goods

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 Vietnam

- 5.5.1.6 Malaysia

- 5.5.1.7 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Nordic Countries

- 5.5.3.7 Russia

- 5.5.3.8 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Colombia

- 5.5.4.4 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 South Africa

- 5.5.5.4 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Aquafil S.p.A.

- 6.4.2 Anand Rayons Ltd.

- 6.4.3 Changzhou Yida Chemical Fiber

- 6.4.4 East Asia Textile Technology

- 6.4.5 Indorama Ventures PCL

- 6.4.6 JCT Ltd.

- 6.4.7 NanYa Plastics Corp.

- 6.4.8 Prutex Nylon Co., Ltd.

- 6.4.9 Salud Industry (Dongguan) Co., Ltd.

- 6.4.10 Singhal Industries Pvt.

- 6.4.11 Toray Industries Inc.

- 6.4.12 Universal Fibers, Inc.

- 6.4.13 Yiwu Huading Nylon

- 6.4.14 Zhejiang Century ChenXing Fiber Technology

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

尼龍6長絲紗線市場規模、佔有率和成長分析:按類型、應用和地區分類-2026-2033年產業預測

尼龍6長絲紗線市場規模、佔有率和成長分析:按類型、應用和地區分類-2026-2033年產業預測 射出成型用聚醯胺6:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

射出成型用聚醯胺6:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031) 尼龍6市場:依產品形式、原料/供應來源、應用及地區分類

尼龍6市場:依產品形式、原料/供應來源、應用及地區分類 射出成型用聚醯胺6市場:依增強類型、等級類型、應用、最終用途零件和銷售管道分類-2026-2032年全球市場預測聚醯胺6市場:依聚合物類型、等級和最終用途產業分類-2026-2032年全球市場預測

射出成型用聚醯胺6市場:依增強類型、等級類型、應用、最終用途零件和銷售管道分類-2026-2032年全球市場預測聚醯胺6市場:依聚合物類型、等級和最終用途產業分類-2026-2032年全球市場預測 全球射出成型聚醯胺6市場報告(2026年)

全球射出成型聚醯胺6市場報告(2026年) PA 66/6 市場規模、佔有率和成長分析(按類型、應用和地區分類)—2026-2033 年產業預測

PA 66/6 市場規模、佔有率和成長分析(按類型、應用和地區分類)—2026-2033 年產業預測 尼龍6長絲的全球市場

尼龍6長絲的全球市場 全球聚醯胺 6 市場規模(按類型、等級、應用、地區、範圍和預測)

全球聚醯胺 6 市場規模(按類型、等級、應用、地區、範圍和預測) 聚□胺 6 全球市場分析:工廠產能、產量、運營效率、需求/供應、最終用戶行業、銷售渠道、區域需求、公司份額 (2015-2035)

聚□胺 6 全球市場分析:工廠產能、產量、運營效率、需求/供應、最終用戶行業、銷售渠道、區域需求、公司份額 (2015-2035)