|

市場調查報告書

商品編碼

2062134

無刷直流風扇:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)BLDC Fan - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

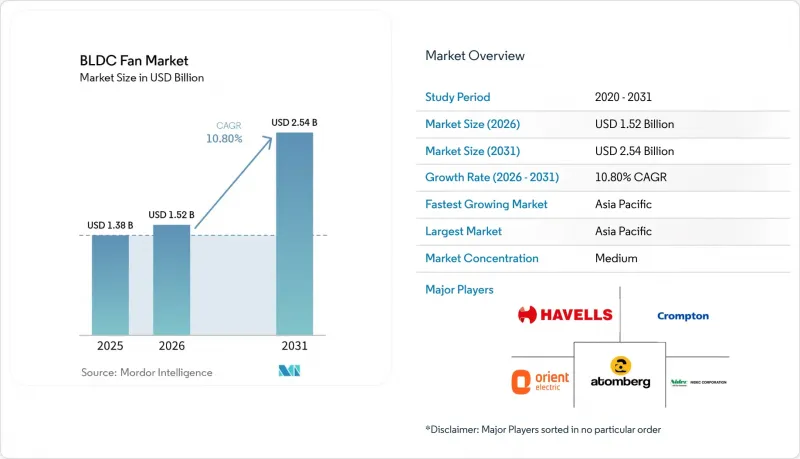

根據 Mordor Intelligence 預測,無刷直流風扇市場規模將從 2025 年的 13.8 億美元和 2026 年的 15.2 億美元成長到 2031 年的 25.4 億美元,2026 年至 2031 年的複合年成長率為 10.80%。

本報告按產品類型(吊扇、落地扇等)、馬達結構(內轉子無刷直流馬達、外轉子無刷直流馬達)、額定功率(小於30W、30-60W、其他)、應用領域(住宅、商業建築、其他)、銷售管道(實體店、線上、其他)和地區(北美、南美、其他)進行細分。市場預測以美元計價。

全球無刷直流風扇市場趨勢及洞察

更嚴格的風扇能源效率標準和星級標籤

美國、歐盟和印度的監管協調促成了「線到空氣」綜合指標和標籤系統的採用,該系統能夠揭示系統損耗,並重新定義風機性能標準。這提升了電子整流馬達在舒適性和工藝通風領域的價值。加州第20號法規要求各種商用和工業風扇的風機效率指數(FEI)達到1.00或更高,該標準得到了美國電機製造商協會(AMCA)測試程序和認證流程的支持。許多符合標準的型號已在MAEDbS註冊。歐盟委員會針對125W至500kW風機制定的2024年生態設計法規預計到2030年每年可節省31太瓦時(TWh)的電力,該法規將於2026年6月生效。這迫使製造商圍繞高效平台簡化產品線,並為設計人員提供更詳細的性能數據。 2025 年能源之星最高效通風扇標準提高了實際能源效率閾值,要求使用 EC 馬達和可靠的控制系統,而非電容啟動感應系統。隨著加州 Title 24 等建築規範將 FEI(效率指數)作為強制性要求,能源性能不再只是行銷選項,而是規範要求,這使得無刷直流風扇成為符合規範項目的預設選擇。

用無刷直流吊扇取代住宅交流感應風扇,優先考慮投資報酬率。

在印度和亞太部分地區,電費和長時間的日常運作使得無刷直流吊扇的投資回收期縮短至不到兩年,即使考慮到其通常的溢價。這使得即使沒有補貼,升級到無刷直流吊扇也極具吸引力,並增加了重複購買的可能性。根據製造商的數據,在用電高峰家庭中,一台傳統的75瓦感應吊扇的年電費可能超過2400盧比,但在典型的用電模式和收費系統下,28-35瓦的無刷直流吊扇可以將電費降低一半以上,僅從家庭經濟角度來看,升級就非常划算。印度強制要求吊扇貼星級標籤檢視,這進一步加速了這一轉變,因為它要求披露吊扇的服務價值。這使得消費者在購買時可以比較每瓦的風量,並鼓勵製造商圍繞更有效率的無刷直流平台重新設計其產品線。中國市場的產品策略正從關注能源效率轉向關注互聯互通和智慧生態系統整合,無刷直流馬達作為更廣泛的家庭自動化和室內空氣品質(IAQ)指南的一部分,能夠支援靜音和精準的調速。此外,在新興市場電網不穩定的情況下,寬電壓設計和控制器穩健性至關重要,這指導著無刷直流風扇市場的平台選擇和價值工程。

由於使用了稀土元素磁鐵和控制器,初始成本較高。

在價格敏感型市場中,資金成本仍然是一大障礙,尤其是當風扇與價格更低、卻能滿足最低風量要求的基本感應馬達產品競爭時。籌資策略和材料清單(BOM) 的選擇體現了高效率馬達、先進控制器以及在當地關稅水準下可接受的投資回收期之間持續的平衡。稀土元素加工和永久磁鐵製造領域的供應集中度增加了無刷直流風扇組件配置中的投入風險,這導致長期成本居高不下,並使大眾市場領域的定價策略更加複雜。製造商正透過平台標準化和跨產品線控制器重複使用來提高規模經濟效益並降低認證成本,從而應對這項挑戰。在整個預測期內,大型企業將更有能力應對投入成本的波動,這鞏固了整合供應商在無刷直流風扇市場的相對優勢。

細分市場分析

到2025年,吊扇將佔據52.21%的市場佔有率,成為銷售量和收入均最大的產品類型。同時,工業用HVLS和商用通風扇預計將以11.95%的複合年成長率成長至2031年,成為成長最快的市場。這種構成比反映了家庭設備的更換週期,以及物流、資料中心和工業設施等產業對無刷直流風扇日益成長的新需求。吊扇的高安裝量和高知名度使其保持了市場主導地位,而印度等國家強制性標籤制度的實施提高了透明度,也使具有高服務價值和靜音運行的無刷直流風扇更具優勢。在住宅產品創新週期中,目前重點關注的是連接性、設計和低噪音;而對於商用和工業產品,重點則在於整合控制功能、預測性維護以及符合暖通空調設計標準的高靜壓性能。此外,歐美廠商正在推出採用原生數位協定和人工智慧最佳化功能的大直徑EC軸流和離心風扇,使其在整個生命週期中都比電感式風扇更具效能優勢。這項產品陣容保持了吊扇市場的強勁成長,而無刷直流風扇市場的微小成長則轉向了高風量低轉速(HVLS)和特殊通風應用領域。

在整個產品線中,可攜式風扇、壁掛式風扇和排氣扇在調節通風和局部冷卻方面仍然發揮著重要作用,但與高風量低風速(HVLS)和先進的商用系統相比,它們的創新仍然較為緩慢。高階消費級產品,包括桌上型、塔式和無葉式風扇,在設計和靜音運行方面展開競爭,並配備了基於應用程式的整合控制和感測器回饋功能,可根據室內環境調節氣流。工業級高風量低風速(HVLS)解決方案優先考慮消除層流和確保大型設施的全年舒適度,其採用的變速EC驅動器可在低轉速下實現平穩控制,降低能耗並帶來卓越的靜音效果。在倉庫和物流設施中,無刷直流風扇與按需控制相結合,以實現尖峰時段室內空氣品質(IAQ)和舒適度目標,製造商目前正在整合振動檢測等功能,用於預測性維護並與建築管理系統(BMS)整合。無刷直流風扇市場繼續在批量生產的天花板式應用與優質化、以規格主導導向的高風量低風速(HVLS)和先進商用通風系統的成長機會之間尋求平衡。

到2025年,內轉子設計將佔據68.87%的市場佔有率,繼續成為許多吊扇、落地扇和小型風扇的主流結構。同時,外轉子EC設計預計將以9.99%的複合年成長率成長,直到2031年,因為暖通空調系統在無刷直流風扇市場中傾向於低速、高扭矩的配置。內轉子馬達在緊湊的面積內提供高扭矩密度,使其成為住宅和小規模商業場所中可逆式、擺動式和智慧吊扇的理想選擇,這些場所對快速變速和靜音運行要求很高。其限制在於高持續功率下的溫度控管,這限制了擴充性在大型暖通空調風扇中的應用,除非增加額外的導熱路徑或散熱器,但這會增加成本和重量。外轉子EC設計將質量分佈在外緣,從而在低轉速下實現高扭矩,使其適用於更大直徑和更高風量的風扇,同時還能降低噪音並延長軸承壽命。在空氣處理應用中,這些風扇可以在廣泛的調節範圍內保持效率,這對於滿足商業建築中人員流動水平波動時的通風需求至關重要。

新產品的推出進一步強化了這些趨勢,例如大直徑EC平台和緊湊型對角線模組的出現,它們以低噪音和高效率為軸流風扇提供了替代方案。歐洲供應商強調模組化框架、寬電壓容差和數位通訊協定,這些特性能夠加快試運行並實現系統級最佳化,從而長期提升效能。住宅供應商則專注於先進的連接性、應用程式控制以及低速靜音運行,因為用戶體驗是競爭激烈的零售市場中脫穎而出的關鍵。在預測期內,內轉子設計預計將在出貨量方面保持主導地位,而外轉子EC配置預計將憑藉其在靜壓和低噪音方面的優勢,在暖通空調、潔淨室和工藝通風領域獲得市場佔有率。這種架構組合將確保無刷直流風扇市場能夠繼續滿足消費者偏好和商業性性能目標。

區域分析

亞太地區預計到2025年將佔據45.75%的市場佔有率,並將在2031年之前以12.68%的複合年成長率推動區域成長。在印度,高頻家用電器的使用和強制性標識正在推動無刷直流風扇的升級換代;而在中國,隨著無刷直流風扇市場電氣化和室內空氣品質(IAQ)目標的不斷推進,其在商業和工業領域的應用也在穩步成長。在印度,功率和風量等價值提案幫助消費者權衡高價與整體擁有成本,而互聯功能和豐富的顏色選擇則有助於提升都市區的市場佔有率。在東南亞,無刷直流風扇的應用情況各不相同,新加坡商業項目中受先進綠色建築法規的影響,無刷直流風扇的滲透率很高;而對價格敏感的大型市場則處於早期轉型階段。在日本和澳大利亞,家庭和小規模商業設施對運作安靜、清潔且具備互聯功能的通風系統有著強勁的需求,這為高階EC產品線奠定了基礎。在全部區域,標準、標籤和電源穩定性正在影響無刷直流風扇市場的平台設計和行銷敘事形成。

在北美,成熟的替換需求與高價值商業設施和資料中心的部署需求之間保持平衡,這些設施和資料中心需要整合控制、可靠性和符合 FEI 規範的產品。隨著聯邦政府撤回提案的2025 年風扇能源效率規則,監管主導仍然掌握在州和地方層面,加州的消費電子和建築標準確地確立了指導國家產品組合的基本性能標準。能源之星標準繼續塑造通風風扇的性能目標,而認證建築中由建築管理系統 (BMS)主導的最佳化正在推動節能標準 (EC) 的普及。在資料中心生態系統中,先進的溫度控管解決方案和 48V 相容組件備受重視,具備遙測功能和模組化設計的無刷直流風扇被最佳化整合到下一代電源拓撲結構中。這些因素確保了北美仍然是無刷直流風扇市場的高價值部署區域。

儘管歐洲的市場佔有率絕對值低於亞太地區,但這反映了生態設計政策的大力支持、能源價格飆升以及更嚴格的建築性能標準,這些標準都建議在新建築和維修中採用節能解決方案。歐盟委員會2024年風機更新(涵蓋125瓦至500千瓦的風扇)直接提高了能源效率標準,並將於2026年6月開始實施,目標是在2030年前大幅降低能耗。這正在加速產品系列向符合FEI標準的系統的過渡。在德國和英國等市場,商用通風和潔淨環境領域的節能系統應用正在迅速普及,大型節能離心風機和軸流風機(配備數位控制)正逐漸成為標準配備。英國的案例研究表明,建築管理系統(BMS)最佳化與高效風扇的結合可以顯著降低能耗和二氧化碳排放,證明了此類投資的長期經濟效益。由於氣候和成本因素,南歐和東歐的進展較為緩慢,但透過政策、標籤制度和獎勵計劃,差距正在不斷縮小。在整個預測期內,歐洲法規的清晰度和設計師對 EC 平台的日益熟悉將有助於保持無刷直流風扇市場的穩定性。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 更嚴格的風扇能源效率標準和星級標籤

- 以無刷直流吊扇取代住宅交流電感應吊扇,優先考慮投資回收期。

- EC風扇在商用空調系統中迅速普及,實現變速控制並改善室內空氣品質(IAQ)。

- 資料中心和電子設備的熱負荷需要高度可靠的無刷直流風扇。

- 實現機架/建築物內使用 48V 直流配電直接安裝無刷直流風扇。

- 獎勵電力公司和綠色建築將智慧無刷直流風扇與電池管理系統/能源管理系統結合。

- 市場限制因素

- 稀土元素磁鐵和控制器的初始成本很高。

- 稀土元素磁鐵的價格波動與供應集中風險

- 售後服務不足,且在惡劣環境下可靠性令人擔憂。

- 電磁干擾和噪音方面的監管要求正在減緩 SKU 的全球部署速度。

- 產業價值鏈分析

- 波特五力分析

- 洞察最新市場趨勢與創新

- 洞察近期市場趨勢(新產品發布、策略性舉措、投資、合作、合資、業務擴張、併購等)

第5章 市場規模與成長預測

- 依產品類型

- 吊扇

- 落地扇和桌面扇

- 壁掛式通風扇

- 工業用高風量低流量/商用通風扇

- 運動結構

- 內轉子無刷直流電機

- 外轉子無刷直流馬達(EC)

- 額定功率

- 小於 30 瓦

- 30~60 W

- 60~120 W

- 超過120瓦

- 透過使用

- 住宅

- 商業建築

- 工業/倉儲用途

- 資料中心和電子設備的冷卻

- 汽車座艙和電池熱管理

- 透過分銷管道

- 線下零售(經銷商/MBO)

- 直接向機構和原始設備製造商銷售

- 線上(電子商務和D2C)

- 按地區

- 北美洲

- 加拿大

- 美國

- 墨西哥

- 南美洲

- 巴西

- 秘魯

- 智利

- 阿根廷

- 其他南美國家

- 亞太地區

- 印度

- 中國

- 日本

- 澳洲

- 韓國

- 東南亞(新加坡、馬來西亞、泰國、印尼、越南、菲律賓)

- 其他亞太國家

- 歐洲

- 英國

- 德國

- 法國

- 西班牙

- 義大利

- 比荷盧經濟聯盟

- 北歐的

- 其他歐洲國家

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

- 奈及利亞

- 其他中東和非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Atomberg Technologies

- Crompton Greaves Consumer

- Havells India

- Orient Electric

- Usha International

- Polycab India

- Panasonic Life Solutions

- Nidec Corporation

- Delta Electronics

- ebm-papst Group

- Johnson Electric

- Regal Rexnord(Marathon)

- ZIEHL-ABEGG

- Mitsubishi Electric

- Big Ass Fans

- Dyson

- Hunter Fan Company

- Lasko Products

- Haier Smart Home

- Midea Group

- Gree Electric

- MinebeaMitsumi Inc.

- Sanyo Denki

- Allied Motion Technologies

- Jupiter Fan

第7章 市場機會與未來展望

According to Mordor Intelligence, the bLDC fan market size is projected to expand from USD 1.38 billion in 2025 and USD 1.52 billion in 2026 to USD 2.54 billion by 2031, registering a CAGR of 10.80% between 2026 and 2031.

This report is Segmented by Product Type (Ceiling Fans, Pedestal, and More), Motor Architecture (Inner-Rotor BLDC, Outer-Rotor BLDC), Power Rating (Below30 W, 30-60 W, and More), Application (Residential, Commercial Buildings, and More), Distribution Channel (Offline Retail, Online, and More), and Geography (North America, South America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global BLDC Fan Market Trends and Insights

Tighter Energy-Efficiency Standards and Star Labeling for Fans

Converging regulations in the United States, European Union, and India reset the baseline for fan performance by using holistic wire-to-air metrics and labeling schemes that expose system losses, which elevate the value of electronically commutated machines in both comfort and process ventilation. California's Title 20 requires FEI≥ 1.00 across a wide range of commercial and industrial fan types, a standard backed by AMCA test procedures and certification pipelines that already count large numbers of compliant models in MAEDbS. The European Commission's 2024 ecodesign rules for fans from 125W to 500kW project 31 TWh of annual electricity savings by 2030 and begin applying in June 2026, which pushes manufacturers to simplify portfolios around higher-efficiency platforms and provide richer performance data for designers. ENERGY STAR Most Efficient criteria for 2025 ventilating fans raise the most practical efficacy thresholds to achieve with EC motors and robust controls rather than with capacitor-start induction systems. Building codes like California Title 24 integrate FEI into mandatory requirements, which turns energy performance into a specification gate rather than a marketing option and positions BLDC fans as default selections in compliant projects.

Payback-Led Residential Replacement of AC Induction with BLDC Ceiling Fans

In India and across parts of Asia-Pacific, electricity tariffs and long daily runtimes compress payback periods for BLDC ceiling fans to below two years at typical price premiums, which makes the switch compelling even without subsidies and lifts repeat purchase intent. Manufacturer data show a conventional 75W induction ceiling fan can cost over INR 2,400 in annual electricity for high-usage homes, while a 28-35W BLDC model can cut that cost by more than half at common usage patterns and tariffs, reinforcing the upgrade case on household economics alone. India's mandatory star labeling for ceiling fans further amplifies this shift by requiring disclosure on service value, letting consumers compare air delivery per watt at the point of purchase, and pushing manufacturers to redesign portfolios around more efficient BLDC platforms. Product strategies in China center less on energy savings and more on connectivity and integration into smart ecosystems, where BLDC motors support quiet, precise speed control as part of larger home automation and IAQ solutions. Wide-voltage designs and controller robustness are also crucial in emerging markets with grid instability, which guides platform choices and value engineering in the BLDC fan market.

Upfront Cost Premium from Rare-Earth Magnets and Controllers.

Capital cost remains a barrier in price-sensitive markets, particularly where fans compete with basic induction alternatives that meet minimum airflow requirements at lower purchase prices. Procurement strategies and bill-of-material choices reflect an ongoing balance between higher-efficiency motors, controller sophistication, and acceptable payback periods at local tariffs. Supply concentration of rare-earth processing and permanent magnet manufacturing elevates input risk for BLDC bill of materials, which sustains premiums over time and complicates pricing strategies for mass-market segments. Manufacturers respond with platform standardization and controller reuse across product lines to improve scale economics and reduce certification overhead. Over the forecast, larger players are better positioned to absorb input volatility, which supports the relative strength of integrated vendors within the BLDC fan market.

Other drivers and restraints analyzed in the detailed report include:

- Rapid EC Fan Adoption in Commercial HVAC for Variable-Speed Control and IAQ

- Data Center and Electronics Thermal Loads Favoring High-Reliability BLDC Fans

- Rare-Earth Magnet Price Volatility and Supply Concentration Risks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Ceiling fans commanded 52.21% share in 2025, making them the largest product category by volume and revenue, while industrial HVLS and commercial ventilation fans deliver the fastest expansion at 11.95% CAGR through 2031, a split that reflects replacement cycles in homes and greenfield growth in logistics, data center, and industrial settings within the BLDC fan market. The installed base and familiarity of ceiling fans sustain their lead, and mandatory labeling in countries like India increases transparency that favors BLDC models with high service value and quiet operation. Product innovation cycles in residential categories now emphasize connectivity, aesthetic options, and lower noise, while commercial and industrial products lean toward controls integration, predictive diagnostics, and high static pressure performance aligned with HVAC design standards. Vendors in Europe and North America have also brought large-diameter EC axial and centrifugal models to market with native digital protocols and AI-supported optimization that build lifetime performance advantages over induction solutions. This mix sustains a strong ceiling fan core while shifting marginal growth to HVLS and specialized ventilation use cases inside the BLDC fan market.

Across product lines, portable, wall, and exhaust fans retain solid roles in code-driven ventilation and spot cooling, but they show more incremental innovation relative to HVLS and advanced commercial systems. Premium consumer products in desk, tower, and bladeless formats compete on design and quietness, with integrated app control and sensor feedback that adapts airflow to room conditions. Industrial HVLS solutions emphasize destratification benefits and year-round comfort in large facilities, where variable-speed EC drives offer smoother control, reduced energy use, and better acoustic performance at low RPM. In warehouses and logistics, BLDC fans combine with demand-based controls to meet both IAQ and comfort targets during peak periods, and manufacturers now include features such as vibration sensing and BMS integration for predictive maintenance. The BLDC fan market continues to balance volume-driven ceiling applications with the growing premium and specification-led opportunity in HVLS and advanced commercial ventilation.

Inner-rotor designs helda 68.87% share in 2025 and remain the architecture of choice for many ceiling, pedestal, and compact fans, while outer-rotor EC designs are the fastest-growing with 9.99% CAGR through 2031 as HVAC systems favor low-speed, high-torque configurations in the BLDC fan market. Inner-rotor motors deliver high torque density in compact footprints and serve reversible, oscillating, and smart ceiling fans well, where rapid speed changes and quiet operation are emphasized in residential and light commercial settings. Their constraints lie in thermal management at higher continuous power, which curbs scalability for large HVAC fans without added conduction paths or heat sinks that raise cost and weight. Outer-rotor EC designs distribute mass around the perimeter for higher torque at low RPM, which suits larger diameters and higher airflows with lower noise and extended bearing life. In air handling applications, these fans can maintain efficiency across wide turndown ranges, which is central to meeting ventilation standards at variable occupancy levels in commercial buildings.

Product launches reinforce these themes with larger-diameter EC platforms and compact diagonal modules that substitute for axial units at lower noise and higher efficiency. European suppliers emphasize modular frames, wide voltage tolerances, and digital communication protocols for faster commissioning and system-level optimization, which improves delivered performance over time. Residential suppliers focus on refinement of connectivity, app control, and silent profiles at low speeds, where user experience drives differentiation in crowded retail categories. Over the forecast period, inner-rotor platforms should retain dominant share by unit volumes, while outer-rotor EC configurations expand share in HVAC, clean room, and process ventilation due to static pressure and low-noise advantages. This architecture mix keeps the BLDC fan market responsive to both consumer preferences and commercial performance targets.

Geography Analysis

Asia-Pacific held 45.75% share in 2025 and leads regional growth at 12.68% CAGR through 2031, with India's high-usage households and mandatory labeling catalyzing BLDC upgrades and China's commercial and industrial deployments aligning with broader electrification and IAQ goals in the BLDC fan market. In India, value communication around wattage and air delivery helps consumers weigh total ownership cost against premiums, while connected features and color choices win share in urban tiers. Southeast Asia presents varied adoption, from high BLDC penetration in Singapore's commercial projects influenced by advanced green building rules to early-stage transitions in large, price-sensitive markets. Japan and Australia show a strong preference for quiet, clean, and connected ventilation in homes and small commercial sites, which underpins premium EC product lines. Across the Asia-Pacific region, standards, labeling, and power stability shape platform designs and marketing narratives in the BLDC fan market.

North America balances mature replacement volumes with high-value commercial and data center deployments that demand integrated controls, reliability, and FEI-aligned specifications. The federal withdrawal of a proposed fan efficiency rule in 2025 kept the regulatory vector at the state and local levels, with California's appliance and building codes establishing baseline performance that guides national portfolios. ENERGY STAR criteria continue to shape ventilating fan performance goals, and BMS-led optimization in certified buildings lifts EC adoption. Data center ecosystems emphasize advanced thermal solutions and 48V-ready components, where BLDC fans with telemetry and modularity integrate best into next-generation power topologies. These factors keep North America a high-value deployment region within the BLDC fan market.

Europe's share reflects smaller absolute volumes compared with Asia-Pacific but strong policy pull from ecodesign, high energy prices, and tightening building performance standards that favor EC solutions in both new builds and retrofits. The European Commission's 2024 update on fans from 125W to 500kW directly raises the efficiency bar, with application in June 2026 and a significant electricity reduction target by 2030, which accelerates portfolio shifts to FEI-aligned systems. Markets like Germany and the UK have seen pronounced adoption in commercial ventilation and clean environments, where large EC centrifugal and axial fans with digital control are now the norm. UK case material demonstrates that BMS optimization combined with efficient fans can drive measurable energy and CO2 reductions, validating longer-run economic outcomes for these investments. Southern and Eastern Europe advance more gradually due to climate and cost factors, but policy, labeling, and incentive structures continue to close gaps. Over the forecast period, Europe's regulatory clarity and designers' familiarity with EC platforms support consistency in the BLDC fan market.

- Atomberg Technologies

- Crompton Greaves Consumer

- Havells India

- Orient Electric

- Usha International

- Polycab India

- Panasonic Life Solutions

- Nidec Corporation

- Delta Electronics

- ebm-papst Group

- Johnson Electric

- Regal Rexnord (Marathon)

- ZIEHL-ABEGG

- Mitsubishi Electric

- Big Ass Fans

- Dyson

- Hunter Fan Company

- Lasko Products

- Haier Smart Home

- Midea Group

- Gree Electric

- MinebeaMitsumi Inc.

- Sanyo Denki

- Allied Motion Technologies

- Jupiter Fan

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Tighter energy-efficiency standards and star labeling for fans

- 4.2.2 Payback-led residential replacement of AC induction with BLDC ceiling fans

- 4.2.3 Rapid EC fan adoption in commercial HVAC for variable-speed control and IAQ

- 4.2.4 Data center and electronics thermal loads favoring high-reliability BLDC fans

- 4.2.5 48V DC distribution in racks/buildings enabling direct BLDC fan deployments

- 4.2.6 Utility and green-building incentives bundling smart BLDC fans with BMS/EMS

- 4.3 Market Restraints

- 4.3.1 Upfront cost premium from rare-earth magnets and controllers

- 4.3.2 Rare-earth magnet price volatility and supply concentration risks

- 4.3.3 After-sales electronics service gaps and reliability concerns in harsh environments

- 4.3.4 EMI/acoustic compliance constraints slowing global SKU rollouts

- 4.4 Industry Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

- 4.6 Insights into the Latest Trends and Innovations in the Market

- 4.7 Insights on Recent Developments (New Product Launches, Strategic Initiatives, Investments, Partnerships, JVs, Expansion, M&As, etc.) in the Market

5 Market Size & Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Ceiling Fans

- 5.1.2 Pedestal & Table Fans

- 5.1.3 Wall & Exhaust Fans

- 5.1.4 Industrial HVLS / Commercial Ventilation Fans

- 5.2 By Motor Architecture

- 5.2.1 Inner-Rotor BLDC

- 5.2.2 Outer-Rotor BLDC (EC)

- 5.3 By Power Rating

- 5.3.1 <30 W

- 5.3.2 30 - 60 W

- 5.3.3 60 - 120 W

- 5.3.4 >120 W

- 5.4 By Application

- 5.4.1 Residential

- 5.4.2 Commercial Buildings

- 5.4.3 Industrial / Warehouse

- 5.4.4 Data-Centre & Electronics Cooling

- 5.4.5 Automotive Cabin & Battery-Thermal

- 5.5 By Distribution Channel

- 5.5.1 Offline Retail (Dealer / MBO)

- 5.5.2 Direct Institutional & OEM

- 5.5.3 Online (E-commerce & D2C)

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 Canada

- 5.6.1.2 United States

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Peru

- 5.6.2.3 Chile

- 5.6.2.4 Argentina

- 5.6.2.5 Rest of South America

- 5.6.3 Asia-Pacific

- 5.6.3.1 India

- 5.6.3.2 China

- 5.6.3.3 Japan

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 South East Asia (SG, MY, TH, ID, VN, PH)

- 5.6.3.7 Rest of Asia-Pacific

- 5.6.4 Europe

- 5.6.4.1 United Kingdom

- 5.6.4.2 Germany

- 5.6.4.3 France

- 5.6.4.4 Spain

- 5.6.4.5 Italy

- 5.6.4.6 BENELUX

- 5.6.4.7 NORDICS

- 5.6.4.8 Rest of Europe

- 5.6.5 Middle East And Africa

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 South Africa

- 5.6.5.4 Nigeria

- 5.6.5.5 Rest of Middle East And Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Atomberg Technologies

- 6.4.2 Crompton Greaves Consumer

- 6.4.3 Havells India

- 6.4.4 Orient Electric

- 6.4.5 Usha International

- 6.4.6 Polycab India

- 6.4.7 Panasonic Life Solutions

- 6.4.8 Nidec Corporation

- 6.4.9 Delta Electronics

- 6.4.10 ebm-papst Group

- 6.4.11 Johnson Electric

- 6.4.12 Regal Rexnord (Marathon)

- 6.4.13 ZIEHL-ABEGG

- 6.4.14 Mitsubishi Electric

- 6.4.15 Big Ass Fans

- 6.4.16 Dyson

- 6.4.17 Hunter Fan Company

- 6.4.18 Lasko Products

- 6.4.19 Haier Smart Home

- 6.4.20 Midea Group

- 6.4.21 Gree Electric

- 6.4.22 MinebeaMitsumi Inc.

- 6.4.23 Sanyo Denki

- 6.4.24 Allied Motion Technologies

- 6.4.25 Jupiter Fan

7 Market Opportunities & Future Outlook

- 7.1 Rapid-cook combi ovens integrating microwave & impingement for QSRs

- 7.2 AI-driven autonomous cooking algorithms for consistency & labour savings

無刷直流風扇市場-2026-2032年全球市場預測

無刷直流風扇市場-2026-2032年全球市場預測 吊扇:市佔率分析、產業趨勢與統計、成長預測(2026-2031)

吊扇:市佔率分析、產業趨勢與統計、成長預測(2026-2031) 智慧吊扇市場-全球產業規模、佔有率、趨勢、機會、預測:按連接類型、應用、分銷管道、地區和競爭格局分類,2021-2031年無刷直流風扇市場 - 全球產業規模、佔有率、趨勢、機會、預測:按類型、最終用戶、風扇轉速、地區和競爭對手分類,2021-2031年

智慧吊扇市場-全球產業規模、佔有率、趨勢、機會、預測:按連接類型、應用、分銷管道、地區和競爭格局分類,2021-2031年無刷直流風扇市場 - 全球產業規模、佔有率、趨勢、機會、預測:按類型、最終用戶、風扇轉速、地區和競爭對手分類,2021-2031年 吊扇市場規模、佔有率、趨勢和預測:按產品類型、風扇尺寸、應用、銷售管道和地區分類,2026-2034年智慧吊扇市場:2026-2032年全球預測(按馬達類型、連接技術、控制系統、產品類型、安裝類型、扇葉材質、最終用戶和分銷管道分類)天花板式集塵機市場:按集塵機類型、安裝方式、流量和最終用戶分類的全球預測,2026-2032年無刷直流軸流風扇市場:依葉片直徑、風量範圍、轉速、終端用戶產業、應用及銷售管道,全球預測,2026-2032年

吊扇市場規模、佔有率、趨勢和預測:按產品類型、風扇尺寸、應用、銷售管道和地區分類,2026-2034年智慧吊扇市場:2026-2032年全球預測(按馬達類型、連接技術、控制系統、產品類型、安裝類型、扇葉材質、最終用戶和分銷管道分類)天花板式集塵機市場:按集塵機類型、安裝方式、流量和最終用戶分類的全球預測,2026-2032年無刷直流軸流風扇市場:依葉片直徑、風量範圍、轉速、終端用戶產業、應用及銷售管道,全球預測,2026-2032年 全球吊扇市場規模、佔有率、成長率、按類型和應用分類的全球產業分析、區域趨勢以及 2026-2034 年預測。日本吊扇市場規模、佔有率、趨勢及預測(按產品類型、風扇尺寸、分銷管道、最終用途和地區分類,2026-2034年)

全球吊扇市場規模、佔有率、成長率、按類型和應用分類的全球產業分析、區域趨勢以及 2026-2034 年預測。日本吊扇市場規模、佔有率、趨勢及預測(按產品類型、風扇尺寸、分銷管道、最終用途和地區分類,2026-2034年)