|

市場調查報告書

商品編碼

2062120

橡膠硫化:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Rubber Vulcanization - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

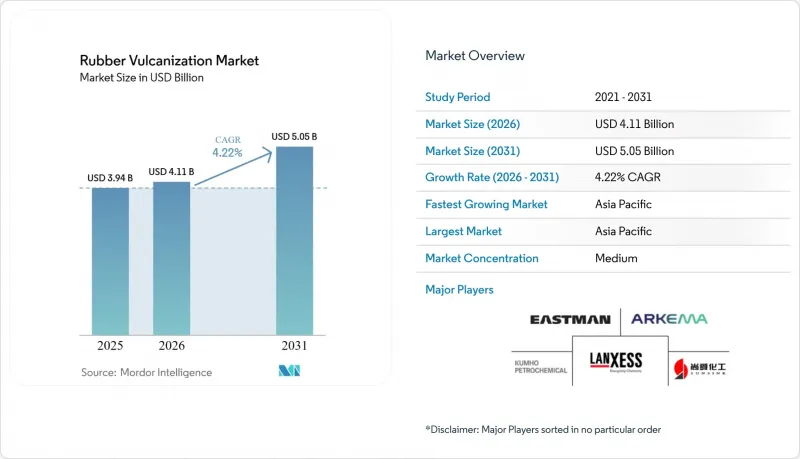

據 Mordor Intelligence 稱,2025 年橡膠硫化市場價值為 39.4 億美元,預計到 2026 年將成長至 41.1 億美元,到 2031 年將成長至 50.5 億美元,2026 年至 2031 年的複合年成長率為 4.22%。

本報告按產品類型(促進劑、硫化劑、活化劑及其他)、應用領域(汽車及交通運輸、工業、消費品、鞋類及其他)及地區(亞太地區、北美地區、歐洲地區、南美地區、中東和非洲)進行細分。市場預測以美元計價。

全球橡膠硫化市場趨勢及洞察

過渡到高性能、低滾動阻力橡膠化合物

在全球輪胎能效法規的推動下,輪胎配方商正從炭黑轉向沉澱二氧化矽。這項轉變需要使用基於Thiram和磺醯胺的硫化促進劑,以便在較低溫度下引發硫化反應。大陸集團於2025年推出了EcoContact 7輪胎,在不影響濕地抓地力的前提下降低了滾動阻力。這是透過將天然橡膠與超快速CBS硫化促進劑複合來實現的。即將訂定的歐盟法規將要求在產品上顯示標示碳足跡的QR碼。這使得低碳足跡硫化促進劑成為OEM採購的關鍵標準。為此,BASF於2026年推出了一系列低碳足跡的丁二醇和聚四氫呋喃產品,使配方設計師能夠突顯顯著的排放效果。此外,諸如科騰公司的SYLVATRAXX等生物基添加劑能夠增強這些配方的性能,在保持回彈性能的同時提高牽引力。

擴大亞太地區的製造業和基礎設施投資。

到2025年,中國將在全球輪胎生產中佔據重要佔有率,生產大量乘用車輪胎。同時,到2026年,印度的輪胎產量也將實現顯著的年成長。兩國都在擴大新的產能,並得到了國內主要品牌的巨額投資支持。在上游領域,錦湖石化和東曹正在擴大其特殊彈性體產品的生產線,這些產品需要客製化的硫化包裝。同時,朗盛大幅提高了位於青島的啟動工廠的產量,以滿足該地區的即時需求。這種策略性在地化佈局符合亞太地區出口主導輪胎產業的擴張趨勢,並凸顯了橡膠硫化化學品市場的成長。

原料價格波動-丁二烯、硫磺、氧化鋅

2025年,中國丁二烯價格上漲。 2026年初,北美合約價格也大幅上漲,導致非一體化加速劑生產商的價格差距縮小,避險變得困難。同期,由於伊朗礦山減產,硫磺價格飆升,造成嚴重的供不應求。 2026年初,由於冶煉廠因成本上升而減產,氧化鋅價格也隨之上漲。這些價格趨勢擠壓了利潤空間,導致NOCIL公司2026會計年度第三季息稅折舊免稅額提前利潤(EBITDA)下降。大型跨國公司利用其跨區域採購網路應對了這些挑戰,但中小企業仍然受制於固定契約,這給它們的營運資金帶來了壓力。

細分市場分析

預計到2025年,促進劑的銷售額將佔總銷售額的41.11%,證實了其在所有主要橡膠配方中的核心地位。磺胺類促進劑因其在混煉溫度下確保足夠的抗焦燒性能,並在壓模溫度下短時間內實現完全硫化,而鞏固了其在輪胎和工業產品中的主導地位。Thiram促進劑價格昂貴,但只需添加極少量的硫。這項特性對於低滾動阻力胎面膠料至關重要,大陸集團已將其應用於其EcoContact 7配方中。雖然氧化鋅等活化劑的成熟過程較慢,但由於微波維修技術的應用,市場對耐熱熱點的鎂基活化劑的需求日益成長。在橡膠硫化化學品市場中,硫化劑的市場規模預計將超過促進劑。這一轉變歸因於硫供體和過氧化物系統的擴展,這些系統有效地解決了與硫供應和高溫耐久性相關的挑戰,預計從 2026 年到 2031 年將以 4.63% 的複合年成長率成長。中國森信和 NOCIL 正專注於整合式硫供體包裝,旨在贏得那些偏好一站式包裝的客戶。

硫化劑包括元素硫、硫供體、過氧化物和特殊不溶性硫。價格昂貴的不溶性硫能有效防止徑向帶錶面出現霜化現象。另一方面,過氧化物硫化在乙丙橡膠(EPDM)軟管中越來越受歡迎,尤其是在電動車的冷卻迴路中,其工作溫度高於傳統動力傳動系統。中國供應商目前提供硫化促進劑和硫供體的組合母粒,簡化了物流。歐美中型企業為了維持市場佔有率,應該效法這種做法。此外,微波硫化技術的普及增加了對超快硫供體的需求,這類硫供體能夠顯著縮短交聯反應時間。這一趨勢表明,在橡膠硫化化學品市場,創新正變得比商品化更為重要。

區域分析

預計到2025年,亞太地區將佔全球銷售額的50.22%,並預計在2026年至2031年間以5.13%的複合年成長率成長。中國是乘用車輪胎的主要生產國,其次是印度。對新建子午線輪胎工廠的大量投資仍在持續。朗盛已大幅提升其青島工廠的產能。同時,中國陽光正利用其大規模硫化生產線,以具有競爭力的到岸成本提供一體化包裝解決方案。在日本,東曹正在擴大其氯丁橡膠產品線,這顯示其對依賴進口的硫化劑的需求,也凸顯了亞洲已開發市場對硫化劑的持續需求。

北美和歐洲在全球需求中佔據相當大的佔有率。儘管成長動能依然強勁,但汽車保有量日趨成熟以及監管日益嚴格(尤其是針對某些化學品的監管)等挑戰正在限制其發展速度。朗盛已在南卡羅來納州開始生產特殊化學品,為美國輪胎製造商提供在地採購貨源,並縮短運輸時間。BASF正在採用環保前驅以滿足排放氣體標籤標準,並將其位於中國的綜合生產設施轉型為100%可再生能源供電,為其歐洲客戶提供合規優勢。

南美洲、中東和非洲總合市佔率在整體市場中相對較小。巴西正在增加卡車和客車用子午線輪胎的產量,墨西哥也保持相當可觀的輪胎產量,但兩國都嚴重依賴從亞洲進口硫化促進劑。由於伊朗硫磺供應減少,該地區的原料供應日益緊張。為此,巴西的幾家工廠正在試驗能夠顯著減少硫磺用量的替代系統。沙烏地阿拉伯正在擴大輪胎產能以滿足區域需求,預計這些生產線投入運作後,特種硫化劑將迎來新的市場機會。

其他好處

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 過渡到高性能、低滾動阻力橡膠化合物

- 擴大亞太地區的製造業和基礎設施投資。

- 工業領域對輸送機、軟管和皮帶的更換需求

- 微波硫化和連續線硫化製程的改進顯著縮短了硫化時間。

- 利用人工智慧即時最佳化硬化曲線,提高植物產量。

- 市場限制因素

- 原料價格波動-丁二烯、硫磺、氧化鋅

- 6-對苯二酚醌的生態毒性評估及潛在禁用

- 2026-2027年因採礦作業減少導致硫磺供應衝擊

- 價值鏈分析

- 波特五力模型

第5章 市場規模與成長預測

- 依產品類型

- 加速器

- 硫化劑

- 活化劑

- 其他

- 透過使用

- 汽車和交通運輸

- 工業的

- 消費品

- 鞋類

- 其他

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- ASEAN

- 澳洲和紐西蘭

- 其他亞太國家

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 法國

- 英國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲國家

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- Arkema

- BASF

- Bolflex

- China Sunsine Chemical Holdings Ltd.

- Duslo as

- Eastman Chemical Company

- Finorchem

- KUMHO PETROCHEMICAL

- LANXESS

- NOCIL Ltd

- OSAKA SODA

- OUCHI SHINKO CHEMICAL INDUSTRIAL CO., LTD

- Sumitomo Chemical Co., Ltd.

- Thomas Swan

- Tianjin Kemai Chemical

- Vanderbilt Holding Company, Inc.

- Zhejiang Baina Rubber & Plastic Equipment Co., Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the rubber vulcanization market size was valued at USD 3.94 billion in 2025 and is expected to grow from USD 4.11 billion in 2026 to USD 5.05 billion by 2031, growing at a CAGR of 4.22% from 2026 to 2031.

This report is Segmented by Product Type (Accelerators, Vulcanizing Agents, Activators, and Others), Application (Automotive and Transportation, Industrial, Consumer Goods, Footwear, and Others), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Rubber Vulcanization Market Trends and Insights

Shift Toward High-Performance, Low-Rolling-Resistance Rubber Compounds

Driven by global mandates on tire energy efficiency, compounders are shifting from carbon black to precipitated silica. This transition necessitates the use of thiuram and sulfenamide accelerators, which can initiate curing at lower temperatures. Continental introduced its EcoContact 7 tire in 2025, achieving a reduction in rolling resistance without compromising wet grip. This was accomplished by blending natural rubber with ultra-fast CBS accelerators. A forthcoming European Union regulation mandates a QR code indicating a product's carbon footprint. This makes low-product-carbon-footprint accelerators a key criterion for original equipment manufacturer procurement. In response, BASF launched a 2026 line of butanediol and PolyTHF with reduced product carbon footprint, enabling formulators to tout significant emission reductions. Additionally, bio-based additives like Kraton's SYLVATRAXX are enhancing these formulations, boosting traction while preserving rebound properties.

Expansion of Asia-Pacific Manufacturing and Infrastructure Spend

In 2025, China accounted for a significant share of global production, manufacturing a substantial number of passenger-car tires. Meanwhile, in 2026, India also recorded notable growth in production compared to the previous year. Both nations are strengthening their greenfield capacities, supported by considerable investments from leading domestic brands. On the upstream front, Kumho Petrochemical and Tosoh are expanding their specialty elastomer lines, which require customized curing packages. Concurrently, LANXESS has significantly increased the output of its Qingdao promoter plant to meet the region's just-in-time demand. This strategic localization highlights the growth of the rubber vulcanization chemicals market, aligning with the expansion of Asia-Pacific's export-driven tire industry.

Raw-Material Price Volatility - Butadiene, Sulfur, Zinc Oxide

In 2025, Chinese butadiene prices experienced an increase. By early 2026, North American contracts also saw a significant rise, creating a challenging price gap for non-integrated accelerator producers, making hedging difficult. During the same period, sulfur prices witnessed a substantial surge due to reduced output from Iranian mines, which resulted in a notable supply deficit. Zinc oxide prices also increased in early 2026 as smelters reduced production because of higher costs. These price dynamics have led to tighter profit margins, with NOCIL's earnings before interest, taxes, depreciation, and amortization declining in the third quarter of the fiscal year 2026. Larger multinational companies have managed to navigate these challenges by leveraging multi-regional sourcing networks, while smaller firms remain constrained by fixed contracts, putting pressure on their working capital.

Other drivers and restraints analyzed in the detailed report include:

- Industrial Demand for Conveyor, Hose and Belt Upgrades

- Microwave and Continuous-Line Vulcanization Retrofits Slash Cure Time

- 6PPD-Quinone Eco-Toxicity Scrutiny and Potential Bans

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Accelerators contributed 41.11% of 2025 sales, confirming their central role in every major rubber recipe. Sulfenamide grades ensure sufficient scorch safety at mixing temperatures and achieve full curing in a short time at press temperatures, solidifying their status as a staple for tires and industrial products. While more expensive, Thiuram accelerators allow for minimal sulfur loadings. This capability is crucial for low-rolling-resistance tread compounds, a feature Continental integrated into its EcoContact 7. While activators like zinc oxide have a slow maturation process, there is a rising demand for magnesium-based variants, which resist thermal hotspots, thanks to microwave retrofits. The market for vulcanizing agents in rubber vulcanization chemicals is projected to surpass that of accelerators. This shift comes as sulfur donors and peroxide systems effectively tackle challenges related to sulfur supply and durability at high temperatures, expanding at a 4.63% CAGR between 2026 and 2031. China Sunsine and NOCIL are doubling down on integrated sulfur-donor packages, aiming to lock in customers that prefer a single-source bundle.

Vulcanizing agents include elemental sulfur, sulfur donors, peroxides, and specialty insoluble sulfur. Insoluble sulfur, which commands a premium, effectively eliminates surface bloom on radial belts. Meanwhile, peroxide curing is gaining traction in ethylene propylene diene monomer hoses, especially for electric-vehicle coolant circuits that operate at higher temperatures than traditional powertrains. Chinese suppliers are now providing combined accelerator-sulfur donor masterbatches, streamlining logistics. This is a service that mid-sized western firms need to match to maintain their market share. Additionally, microwave curing is driving up demand for ultra-fast donors, capable of completing cross-linking in a significantly reduced time. This trend underscores the rubber vulcanization chemicals market's preference for innovation over commoditization.

Geography Analysis

Asia-Pacific accounted for 50.22% of 2025 revenue and is expected to advance at a 5.13% CAGR through 2026 to 2031. China leads with a significant output of passenger-car tires, followed closely by India. Substantial investments continue to flow into new radial plants. LANXESS has notably increased capacity at its Qingdao facility. Meanwhile, China Sunsine is utilizing its large-scale accelerator line to deliver integrated packages at competitive landed costs. In Japan, Tosoh is expanding its offerings with chloroprene rubber, dependent on imported vulcanization chemicals, signaling a sustained demand in developed Asian markets.

North America and Europe account for a considerable portion of the global demand. Growth remains steady but is tempered by a mature vehicle parc and regulatory challenges, notably the impending limits on certain chemical compounds. LANXESS has commenced production of specialized grades in South Carolina, providing United States tire manufacturers with a local source and reducing freight times. BASF, in a bid to meet emission-labeling standards, has adopted environmentally friendly precursors and transitioned its Verbund site in China to fully renewable energy, offering a compliance edge to European clients.

South America, the Middle-East and Africa collectively account for a smaller share of the market. Brazil has increased its truck-bus-radial output, while Mexico has maintained a notable level of tire production, with both nations heavily reliant on accelerator imports from Asia. Due to reduced sulfur availability from Iran, feedstock supplies have tightened in this region. In response, several Brazilian plants are experimenting with alternative systems that significantly reduce sulfur input. Saudi Arabia is expanding its tire production capacity to cater to regional demand, presenting new opportunities for specialty curing agents once these lines become operational.

- Arkema

- BASF

- Bolflex

- China Sunsine Chemical Holdings Ltd.

- Duslo a.s.

- Eastman Chemical Company

- Finorchem

- KUMHO PETROCHEMICAL

- LANXESS

- NOCIL Ltd

- OSAKA SODA

- OUCHI SHINKO CHEMICAL INDUSTRIAL CO., LTD

- Sumitomo Chemical Co., Ltd.

- Thomas Swan

- Tianjin Kemai Chemical

- Vanderbilt Holding Company, Inc.

- Zhejiang Baina Rubber & Plastic Equipment Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Shift toward high-performance, low-rolling-resistance rubber compounds

- 4.2.2 Expansion of Asia-Pacific manufacturing and infrastructure spend

- 4.2.3 Industrial demand for conveyor, hose and belt upgrades

- 4.2.4 Microwave and continuous-line vulcanization retrofits slash cure time

- 4.2.5 AI-driven real-time cure-profile optimization boosting plant yield

- 4.3 Market Restraints

- 4.3.1 Raw-material price volatility-butadiene, sulfur, zinc oxide

- 4.3.2 6PPD-quinone eco-toxicity scrutiny and potential bans

- 4.3.3 Sulfur-supply shocks from mining curtailments in 2026-27

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Accelerators

- 5.1.2 Vulcanizing Agents

- 5.1.3 Activators

- 5.1.4 Others

- 5.2 By Application

- 5.2.1 Automotive and Transportation

- 5.2.2 Industrial

- 5.2.3 Consumer Goods

- 5.2.4 Footwear

- 5.2.5 Others

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN

- 5.3.1.6 Australia and New Zealand

- 5.3.1.7 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 France

- 5.3.3.3 United Kingdom

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Arkema

- 6.4.2 BASF

- 6.4.3 Bolflex

- 6.4.4 China Sunsine Chemical Holdings Ltd.

- 6.4.5 Duslo a.s.

- 6.4.6 Eastman Chemical Company

- 6.4.7 Finorchem

- 6.4.8 KUMHO PETROCHEMICAL

- 6.4.9 LANXESS

- 6.4.10 NOCIL Ltd

- 6.4.11 OSAKA SODA

- 6.4.12 OUCHI SHINKO CHEMICAL INDUSTRIAL CO., LTD

- 6.4.13 Sumitomo Chemical Co., Ltd.

- 6.4.14 Thomas Swan

- 6.4.15 Tianjin Kemai Chemical

- 6.4.16 Vanderbilt Holding Company, Inc.

- 6.4.17 Zhejiang Baina Rubber & Plastic Equipment Co., Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

橡膠促進劑市場預測至2034年—按類型、應用和地區分類的全球分析

橡膠促進劑市場預測至2034年—按類型、應用和地區分類的全球分析 橡膠加工化學品市場報告:按類型、應用、最終用途和地區分類(2026-2034 年)

橡膠加工化學品市場報告:按類型、應用、最終用途和地區分類(2026-2034 年) 橡膠加工化學品市場:依產品類型、原料來源、形態、應用、最終用途產業及通路分類-2026-2032年全球預測

橡膠加工化學品市場:依產品類型、原料來源、形態、應用、最終用途產業及通路分類-2026-2032年全球預測 全球橡膠加工化學品市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球橡膠加工化學品市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 2026年全球橡膠加工化學品市場報告

2026年全球橡膠加工化學品市場報告 2025-2029年全球橡膠加工化學品市場

2025-2029年全球橡膠加工化學品市場 橡膠加工化學品市場規模、佔有率及成長分析(按產品、應用、最終用途及地區分類)-2026-2033年產業預測

橡膠加工化學品市場規模、佔有率及成長分析(按產品、應用、最終用途及地區分類)-2026-2033年產業預測 橡膠加工化學品市場機會、成長要素、產業趨勢分析及2026年至2035年預測

橡膠加工化學品市場機會、成長要素、產業趨勢分析及2026年至2035年預測 全球橡膠加工助劑及防沾劑市場全球橡膠加工化學品市場規模(按產品、應用、地區和預測)

全球橡膠加工助劑及防沾劑市場全球橡膠加工化學品市場規模(按產品、應用、地區和預測)