|

市場調查報告書

商品編碼

2062113

再生瀝青:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Recycled Asphalt - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

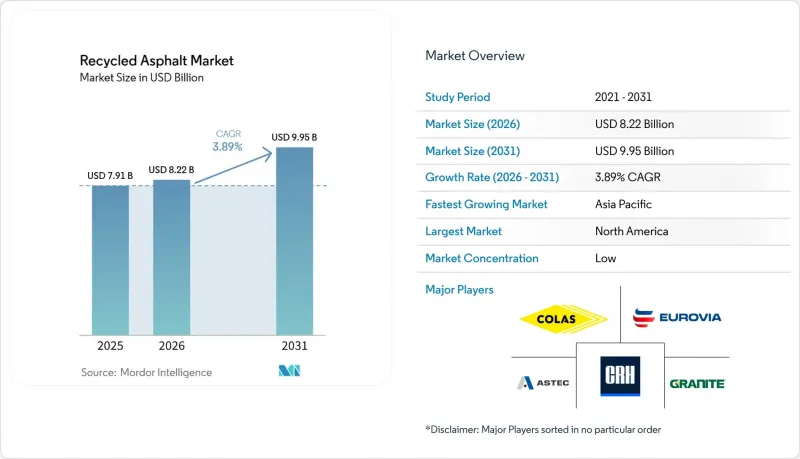

根據 Mordor Intelligence 預測,再生瀝青市場規模將從 2025 年的 79.1 億美元和 2026 年的 82.2 億美元成長到 2031 年的 99.5 億美元,2026 年至 2031 年的複合年成長率為 3.89%。

本報告依再生瀝青含量(低含量(20%或以下)、中含量(21-50%)及以上)、再生瀝青用途(修補材料、熱拌瀝青混合料及其他)、終端用戶產業(商業、工業、市政)以及地區(亞太、北美、歐洲、南美、中東和非洲)進行細分。市場預測以美元計價。

全球再生瀝青市場趨勢及洞察

RAP和原生混合料的成本競爭力

根據美國國家瀝青路面協會 (NAPA) 的報告,2023 年,美國生產商透過使用 9,610 萬噸再生瀝青路面材料 (RAP),平均摻混比例為 21.9%,實現了 34 億美元的成本節約。這充分體現了 RAP 在控制原料成本方面的重要作用。佛羅裡達州交通部的現場數據顯示,在亞熱帶氣候條件下,使用高比例 RAP 的路面能夠以更低的交付成本達到與新瀝青相當的性能。隨著原油價格上漲,這種成本優勢將更加顯著。例如,如果布蘭特原油價格超過每桶 85 美元,新瀝青和再生瀝青之間的價格差異可能會翻倍。這使得印度的建築商在高速公路項目上實現了 25% 至 30% 的成本節約。此外,市政預算的限制也推動了 RAP 的應用,使其不易受到新瀝青需求波動的影響。

交通部和地方當局有嚴格的永續性採購義務。

加州議會第2953號法案、新澤西州2023年第134號公共法案、科羅拉多的「清潔採購法案」以及明尼蘇達州2025年環境產品聲明(EPD)法規均要求競標提供碳排放強度證明,並要求所有合格的項目必須使用再生瀝青。違規處罰包括扣留合約款項和取消投標資格,這些法規旨在建立合規標準,以確保需求穩定,不受原油價格波動的影響。這些法規支援那些已投資生命週期評估(LCA)工具的供應商。

RAP中分散的物流和庫存管理

吸濕性、污染和粒徑分佈差異會影響再生瀝青路面材料(RAP)的性能裕度,並增加混合成本。由於許多公共倉儲設施缺乏分級設備和防護罩,運輸部(DOT)將RAP含量限制在20-30%,除非進行額外的實驗室檢測。為了使再生瀝青市場充分發揮RAP的巨大利用潛力,投資建造有頂棚的倉儲設施、現場分揀和連續取樣至關重要。

細分市場分析

到2025年,低RAP含量(20%或以下)的再生瀝青混合料將佔據最大的市場佔有率。這是因為大多數交通運輸部(DOT)標準都依賴傳統的性能數據。這類混合料具有穩定的壓實性能,並且與未經改造的拌合站相容,從而降低了施工風險。中等RAP含量(21%至50%)的配方由於雙料倉供料系統的改進和再生劑化學成分的提升,其應用日益廣泛,能夠在保持成本競爭力的同時,提供均衡的抗疲勞性能。

預計到2031年,高RAP含量(超過50%)的混合料將以3.98%的複合年成長率推動再生瀝青市場成長。 Eurovia的100% RAP高速公路試點計畫和Astec的ReMix CCPR工廠等措施已證明了其現場可行性。此外,2026年推出的三元複合再生技術解決了先前人們對低溫脆性的擔憂。目前,美國多個州為RAP含量達到40%或以上的項目競標提供額外加分,促使投資者重新評估成本風險平衡。投資於分級和自動化混合控制的建築公司將能夠更好地掌握這一細分市場,將其發展成為盈利的市場機會。

區域分析

預計到2031年,亞太地區的複合年成長率將達到4.41%。中國每年生產約2億噸再生瀝青路面材料(RAP),但其再利用率僅30%,這意味著仍有很大的提升空間,因為GB/T25033標準支持熱再生、溫再生和冷再生等方法。在印度,2023-2024年度,超過6300萬噸廢棄物被用於6634公里高速公路的鋪設,多個邦正在測試含有40% RAP的路面。日本的路面再生率高達99%,並已建立了完善的收集和物流系統,同時,新的路面再生研究計劃(PWRI)測試方法旨在檢驗含有高達70%再生黏合劑的混合料的有效性。澳洲和韓國目前對再生率設定了上限,但提高閾值面臨經濟方面的考量。

北美:政策和成本降低正在推動市場佔有率的成長。到2025年,北美將佔再生瀝青市場41.89%的佔有率。 2023年,美國建築商透過使用9,610萬噸再生瀝青(RAP)節省了34億美元的材料成本。加州AB 2953法案和科羅拉多「清潔法案」等州級法規強制要求提交環境產品聲明(EPD),而平衡混合料設計的試點計畫正在將RAP的允許使用比例提高到45-50%。維特根公司與各州交通部(DOT)的培訓夥伴關係正在提升操作人員在現場冷再生製程的技能。

在歐洲,受掩埋禁令和碳排放稅的推動,預計到2024年,歐洲將生產1億噸再生瀝青混合料(RAP),其中95%將被回收。法國的A10專案證明了在高速公路路面層中使用100% RAP的可行性。同時,科拉斯公司透過收購弗勞恩拉特公司,擴大了在歐洲最大的道路市場——德國的回收能力。這些進展體現了歐洲對永續道路建設實踐的重視。

南美洲、中東和非洲雖然規模較小,但市場成長迅速。在巴西,聖保羅已實施冷回收系統用於城市基礎設施維修。沙烏地阿拉伯已批准在其國家高速公路上使用25%的再生瀝青混合料(RAP)。這些地區的基礎設施獎勵策略預算和循環經濟政策表明,回收的普及率正在逐步提高。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- RAP和原生混合油的成本競爭力

- 交通部 (DOT) 和地方當局對永續性採購提出了嚴格的要求。

- 100% RAP 和溫拌瀝青攪拌站技術的廣泛應用。

- 企業實現淨零排放目標正在推動碳負排放路面信用額度的成長。

- 一個二次材料交易平台,能夠供應高品質的 RAP(再生人造珍珠)。

- 市場限制因素

- RAP中物流與庫存管理脫節

- 人們開始關注再生路面徑流中微塑膠的含量

- 瀝青再生劑的價格波動

- 價值鏈分析

- 波特五力模型

第5章 市場規模與成長預測

- 按等級分類的 RAP 內容

- 低RAP含量(20%或以下)

- 中等RAP含量(21-50%)

- 高 RAP 含量(>50%)

- 瀝青的施用

- 維修材料

- 熱拌瀝青

- 臨時道路和公路

- 道路骨材

- 互鎖磚

- 新瀝青瓦

- 能源回收

- 按最終用戶行業分類

- 商業的

- 產業

- 地方政府

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 其他亞太國家

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲國家

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- Allan Myers, Inc.

- Apollo Asphalt Reclaimers LLC

- Astec Industries

- Colas

- CRH

- Eurovia(VINCI)

- Granite Construction Inc.

- MARINI FAYAT GROUP

- Martin Marietta

- MR Roads

- necoTECH

- Superpave Engineering Inc.

- WIRTGEN INDIA Pvt. Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the recycled asphalt market size is projected to expand from USD 7.91 billion in 2025 and USD 8.22 billion in 2026 to USD 9.95 billion by 2031, registering a CAGR of 3.89% between 2026 to 2031.

This report is Segmented by RAP Content Level (Low RAP Content (Less Than or Equal To 20%), Medium RAP Content 21-50%, and More), Recycled Asphalt Application (Patch Material, Hot Mix Asphalt, and More), End-User Industry (Commercial, Industrial, Municipal), and Geography (Asia-Pacific, North America, Europe, South America, Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Recycled Asphalt Market Trends and Insights

Cost Competitiveness of RAP Versus Virgin Mixes

The National Asphalt Pavement Association reported USD 3.4 billion in U.S. producer savings in 2023 through the use of 96.1 million tons of Reclaimed Asphalt Pavement (RAP) at an average inclusion rate of 21.9%. This demonstrates the role of RAP in managing raw material costs. Field data from the Florida Department of Transportation indicated that RAP-rich pavements provide comparable performance at a lower delivered cost in subtropical climates. Cost advantages increase during crude oil price rises; for example, when Brent crude exceeds USD 85 per barrel, the price difference between virgin and reclaimed binder can double. This has enabled contractors in India to achieve cost reductions of 25-30% on highway projects. Furthermore, municipal budget limitations support RAP adoption, making its usage less influenced by fluctuations in virgin asphalt demand.

Stringent Sustainability Procurement Mandates By DOTs And Municipalities

California's Assembly Bill 2953, New Jersey's Public Law 2023 c.134, Colorado's Buy Clean Act, and Minnesota's 2025 EPD rule require bidders to document carbon intensity, integrating reclaimed asphalt content into all qualifying projects. Non-compliance penalties include measures such as contract holdbacks and disqualification, establishing a compliance baseline that ensures consistent demand regardless of crude oil price fluctuations. These regulations support suppliers that have invested in life-cycle assessment tools.

Fragmented Logistics and Stockpile Management For RAP

Moisture absorption, contamination, and variability in gradation impact the performance margins of Reclaimed Asphalt Pavement (RAP) and increase blending costs. Many public storage facilities lack fractionation and protective covering, leading Departments of Transportation (DOTs) to limit RAP content to 20-30% unless additional laboratory testing is conducted. Investments in covered storage, on-site screening, and continuous sampling are essential for the recycled asphalt market to achieve its high-RAP potential.

Other drivers and restraints analyzed in the detailed report include:

- Expansion Of 100%-RAP And Warm-Mix Plant Technologies

- Corporate Net-Zero Targets Spurring Carbon-Negative Pavement Credits

- Emergent Microplastics Scrutiny on Recycled Pavement Runoff

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, low RAP content (less than or equal to 20%) held the largest share of the recycled asphalt market. This is due to most DOT standards relying on legacy performance data. These mixes provide consistent compaction and are compatible with unmodified batch plants, reducing adoption risks. Medium RAP blends (21-50%) have seen increased usage due to dual-bin feed retrofits and advancements in rejuvenator chemistries, offering balanced fatigue resistance at a competitive cost.

High RAP content (greater than 50%) is expected to lead the recycled asphalt market with a 3.98% CAGR through 2031. Initiatives such as Eurovia's 100% RAP motorway trial and Astec's ReMix CCPR plant have demonstrated field feasibility. Furthermore, the introduction of ternary composite rejuvenation in 2026 addressed earlier concerns regarding low-temperature brittleness. Project bids incorporating at least 40% RAP now qualify for additional scoring credits in several U.S. states, prompting specifiers to reassess the cost-risk balance. Contractors investing in fractionation and automated dosage controls are positioned to expand this segment into a profitable market opportunity.

Geography Analysis

Asia-Pacific is projected to grow at a CAGR of 4.41% through 2031. China produces approximately 200 million tons of Reclaimed Asphalt Pavement (RAP) annually, but reuses only 30%, indicating potential for increased recycling as GB/T25033 supports hot, warm, and cold recycling methods. In India, over 63 million tons of waste were reused in FY 2023-24 across 6,634 kilometers of highways, with several states testing 40% RAP surface courses. Japan, with a 99% pavement recycling rate, has advanced collection logistics, while new PWRI test methods aim to validate mixes containing up to 70% reclaimed binder. Australia and South Korea currently maintain capped reuse levels but face fiscal considerations to increase thresholds.

North America: Market Share Driven by Policy and Cost Savings. North America accounted for 41.89% of the recycled asphalt market in 2025. In 2023, U.S. contractors saved USD 3.4 billion in material costs by utilizing 96.1 million tons of RAP. State regulations, such as California AB 2953 and Colorado's Buy Clean Act, mandate Environmental Product Declarations, while balanced mix design pilots are increasing allowable RAP percentages to 45-50%. Training partnerships between Wirtgen and state Departments of Transportation (DOTs) are enhancing operator skills for on-site cold recycling processes.

Europe recycled 95% of its 100 million-ton RAP output in 2024, driven by landfill bans and carbon taxes. France's A10 trial validated the use of 100% RAP in highway layers, while Colas expanded its recycling capabilities in Germany, Europe's largest road market, through the acquisition of Frauenrath. These developments reflect Europe's focus on sustainable road construction practices.

South America and the Middle East & Africa are smaller but growing markets. In Brazil, cold recycling systems were incorporated into Sao Paulo's urban infrastructure upgrades. Saudi Arabia approved the use of 25% RAP for national highways. Infrastructure stimulus budgets and circular-economy policies in these regions indicate a gradual increase in recycling adoption.

- Allan Myers, Inc.

- Apollo Asphalt Reclaimers LLC

- Astec Industries

- Colas

- CRH

- Eurovia (VINCI)

- Granite Construction Inc.

- MARINI FAYAT GROUP

- Martin Marietta

- MR Roads

- necoTECH

- Superpave Engineering Inc.

- WIRTGEN INDIA Pvt. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cost competitiveness of RAP versus virgin mixes

- 4.2.2 Stringent sustainability procurement mandates by DOTs and municipalities

- 4.2.3 Expansion of 100 %-RAP and warm-mix plant technologies

- 4.2.4 Corporate net-zero targets spurring carbon-negative pavement credits

- 4.2.5 Secondary materials trading platforms unlocking high-quality RAP supply

- 4.3 Market Restraints

- 4.3.1 Fragmented logistics and stockpile management for RAP

- 4.3.2 Emergent microplastics scrutiny on recycled pavement runoff

- 4.3.3 Volatility of bitumen-rejuvenator additive pricing

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By RAP Content Level

- 5.1.1 Low RAP Content (Less than or Equal to 20 %)

- 5.1.2 Medium RAP Content (21-50 %)

- 5.1.3 High RAP Content (Greater than 50 %)

- 5.2 By Recycled Asphalt Application

- 5.2.1 Patch Material

- 5.2.2 Hot Mix Asphalt

- 5.2.3 Temporary Driveways and Roads

- 5.2.4 Road Aggregate

- 5.2.5 Interlocking Bricks

- 5.2.6 New Asphalt Shingles

- 5.2.7 Energy Recovery

- 5.3 By End-User Industry

- 5.3.1 Commercial

- 5.3.2 Industrial

- 5.3.3 Municipal

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 Australia

- 5.4.1.5 South Korea

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Allan Myers, Inc.

- 6.4.2 Apollo Asphalt Reclaimers LLC

- 6.4.3 Astec Industries

- 6.4.4 Colas

- 6.4.5 CRH

- 6.4.6 Eurovia (VINCI)

- 6.4.7 Granite Construction Inc.

- 6.4.8 MARINI FAYAT GROUP

- 6.4.9 Martin Marietta

- 6.4.10 MR Roads

- 6.4.11 necoTECH

- 6.4.12 Superpave Engineering Inc.

- 6.4.13 WIRTGEN INDIA Pvt. Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

2026-2034年全球瀝青市場規模、佔有率、趨勢和成長分析報告

2026-2034年全球瀝青市場規模、佔有率、趨勢和成長分析報告 瀝青市場規模、佔有率和成長分析:按產品類型、應用和地區分類-2026-2033年產業預測

瀝青市場規模、佔有率和成長分析:按產品類型、應用和地區分類-2026-2033年產業預測 2026年全球再生瀝青市場報告全球再生瀝青市場規模、佔有率、趨勢和成長分析報告(2026-2034)

2026年全球再生瀝青市場報告全球再生瀝青市場規模、佔有率、趨勢和成長分析報告(2026-2034) 瀝青市場:依產品類型、技術、應用、最終用戶和通路分類-2026-2032年全球預測瀝青改質劑市場:按類型、技術、形態、應用和最終用戶分類-2026-2032年全球預測

瀝青市場:依產品類型、技術、應用、最終用戶和通路分類-2026-2032年全球預測瀝青改質劑市場:按類型、技術、形態、應用和最終用戶分類-2026-2032年全球預測 耐輻射潤滑劑和潤滑脂市場規模、佔有率和成長分析:按產品類型、等級、基礎油類型、添加劑類型、應用、最終用途產業和地區分類-2026-2033年產業預測

耐輻射潤滑劑和潤滑脂市場規模、佔有率和成長分析:按產品類型、等級、基礎油類型、添加劑類型、應用、最終用途產業和地區分類-2026-2033年產業預測 瀝青改質劑:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

瀝青改質劑:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 瀝青市場報告:按產品、瀝青類型、應用、最終用途產業和地區分類,2026-2034年2026年全球瀝青、潤滑油和潤滑脂市場報告

瀝青市場報告:按產品、瀝青類型、應用、最終用途產業和地區分類,2026-2034年2026年全球瀝青、潤滑油和潤滑脂市場報告