|

市場調查報告書

商品編碼

1939573

瀝青改質劑:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Asphalt Modifiers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

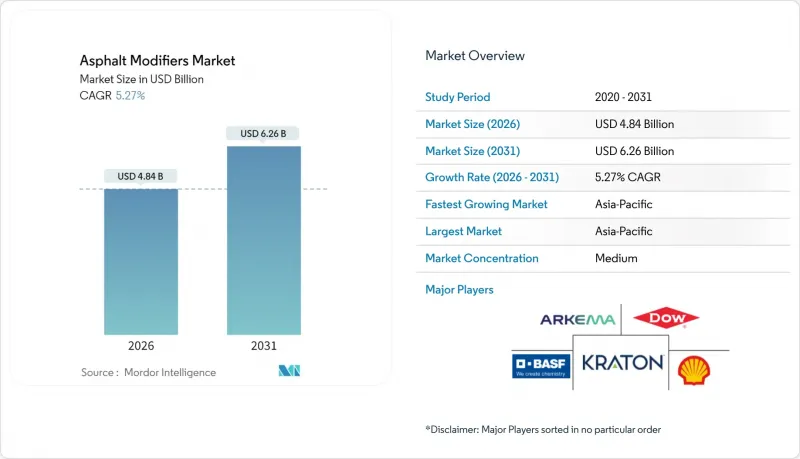

預計到 2026 年,瀝青改質劑市場規模將達到 48.4 億美元,高於 2025 年的 46 億美元。

預計到 2031 年將達到 62.6 億美元,2026 年至 2031 年的複合年成長率為 5.27%。

公共工程預算的增加、基於嚴格性能標準的道路規範以及向永續瀝青技術的逐步轉型,共同推動了這一穩步成長。亞太地區擁有最大的區域市場,雄心勃勃的高速公路擴建、不斷成長的交通流量以及快速的都市化,持續支撐著對聚合物改性黏合劑的需求。儘管北美和歐洲的滲透率已趨於穩定,但降低生命週期成本和淨零排放的要求仍在推動對高階改質劑的需求。與原油價格相關的聚合物價格波動,以及針對瀝青煙霧的日益嚴格的職場安全法規,為瀝青改質劑市場帶來了成本和合規風險。製造商正透過拓展供應鏈、擴大生物基產品組合以及深化與道路管理機構的技術合作來應對這些壓力。

全球瀝青改質劑市場趨勢及洞察

在後疫情時代的公共工程計劃中恢復基礎設施支出

新的經濟獎勵策略鼓勵公共工程機構優先考慮使用壽命長的路面,而非僅僅追求最低競標,從而維持了對優質黏合劑的需求。光是美國的《基礎設施投資與就業法案》就撥款1,100億美元用於公路和橋樑建設,中國、印度和東南亞也將很快獲得類似資金,重點是重型道路的聚合物改質瀝青。這些資金投入帶來了穩定的計劃儲備,有利於那些擁有可靠性能數據的供應商。在這種資金環境下,負責人越來越重視改質劑,以最大限度地提高納稅人的投資回報。

交通密度高,軸荷大

電子商務和工業活動的快速成長推動了貨運量的成長,使車軸應力遠遠超出傳統設計極限。現場試驗表明,與未改質瀝青相比,SBS改質瀝青的動態穩定性指標可提高10倍,並顯著降低卡車行駛造成的車轍深度。運輸部目前已將聚合物需求納入港口進場道路和物流走廊的競標,從而確保了對高模量改質劑的持續需求。

聚合物改質瀝青的初始成本

與傳統黏合劑相比,15%至25%的價格溢價持續阻礙新型黏合劑在以最低初始競標為優先的採購規則下的推廣應用。預算緊張的市政當局為了優先進行路面翻新,推遲了改質劑的採用。儘管新型黏合劑在全生命週期內具有明顯的成本節約優勢,但其短期成長前景並不樂觀。

細分市場分析

實體改質劑持續維持其收入主導地位,預計到2025年將佔瀝青改質劑市場54.10%的佔有率。 SBS(苯乙烯-丁二烯-苯乙烯共聚物)和EVA(乙烯-醋酸乙烯酯共聚物)在重載和極端溫度條件下仍廣泛應用於鋪路工程。其中,SBS憑藉其彈性恢復性和與煉廠級瀝青的相容性在該領域佔據主導地位。化學改質劑雖然目前銷量仍較小,但卻是成長最快的子類別,複合年成長率達5.36%,這主要得益於溫拌催化劑和抗剝落劑能夠滿足環保法規和耐濕性要求。受輪胎回收激勵政策的推動,橡膠顆粒改質劑在尋求提高路面耐久性並減少掩埋廢棄物的市政部門中越來越受歡迎。纖維、礦物和奈米增強材料則補充了物理性能範圍,並滿足了特定的耐久性需求。

展望未來,相關人員期望將聚合物與生物化學再生劑結合的混合系統能夠平衡剛度、抗裂性和永續性。一項重要的歐洲計劃已證實,木質素-聚合物混合在達到與SBS相似的性能等級的同時,還能降低碳足跡。能夠確保可靠的生物基原料來源並克服配方相容性挑戰的供應商,將更有利於在加速脫碳的趨勢下盈利。

瀝青改質劑報告改質劑類型(物理改質劑、化學改質劑)、瀝青混合料拌合技術(熱拌瀝青、溫拌瀝青、冷拌和半溫拌)、應用領域(路面、屋頂及其他應用)以及地區(亞太地區、北美地區、歐洲地區、南美地區以及中東和非洲地區)進行以金額為準。

區域分析

到2025年,亞太地區將佔據全球瀝青改質劑市場38.25%的佔有率,年複合成長率達5.81%,這主要得益於數兆美元的「一帶一路」高速公路計畫。中國計畫在2025年建成超過12萬公里的高品質高速公路,國內煉油廠也持續提升短鏈瀝青(SBS)生產線的產能,以滿足國內需求。印度的走廊建設規劃以及機場跑道擴建進一步推動了該地區對能夠承受季風和重型貨物運輸的高性能黏合劑的需求。東南亞國家正在投資建造模組化瀝青攪拌站,以便快速部署,並傾向於使用全球主要供應商提供的即用型聚合物顆粒。

在北美,基礎設施投資和就業法案為市場提供了支持,該法案允許長期持續進行採用高性能瀝青規格的路面翻新計劃。超過80%的美國州交通部門強制要求州際公路使用改質瀝青,維持了成熟且穩健的收入基礎。加州和華盛頓州等製定了積極的二氧化碳減排目標的州,其溫拌瀝青的採用速度尤其迅速,迫使化學添加劑供應商進行區域化分銷。

儘管歐洲的產量較低,但該地區正根據其「Fit for 55」法規,率先推廣碳最佳化型黏合劑解決方案。該地區的許多國家合約已經強制要求使用溫拌瀝青,並支持對木質素-聚合物混合技術的先進研究。例如,斯堪地那維亞的機構正在對承包商透過低溫技術減少的每一噸二氧化碳排放給予補償,從而推動了對溫拌瀝青改質劑的需求。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 在後疫情時代的公共工程計劃中恢復基礎設施支出

- 交通密度和車輛軸荷增加

- 採用基於性能的瀝青規格(例如,Superpave)

- 道路建設淨零碳排放法規

- 石墨烯增強黏合劑研究激增

- 市場限制

- 聚合物改質瀝青的初始成本高

- 對職業健康風險和煙霧暴露的擔憂

- SBS/SEBS及其他聚合物的價格波動

- 價值鏈分析

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章 市場規模與成長預測

- 按修飾符類型

- 物理修飾劑

- 塑膠(高密度聚苯乙烯、苯乙烯-丁二烯橡膠、乙烯醋酸乙烯)

- 橡膠(橡膠碎屑、脫硫橡膠)

- 纖維(纖維素、芳香聚醯胺、玻璃)

- 礦物填料和增量劑

- 化學改質劑

- 抗剝離劑

- 溫拌瀝青添加劑

- 再生劑和抗氧化劑

- 其他(奈米粘土、石墨烯)

- 物理修飾劑

- 透過瀝青混合技術

- 熱拌瀝青混合料(HMA)

- 溫拌瀝青(WMA)

- 冷拌和半熱飲

- 透過使用

- 路面

- 屋頂材料

- 其他用途

- 地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- ASEAN

- 澳洲

- 亞太其他地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 北歐國家

- 俄羅斯

- 其他歐洲地區

- 南美洲

- 巴西

- 阿根廷

- 哥倫比亞

- 其他南美洲

- 中東和非洲

- 沙烏地阿拉伯

- 卡達

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- Arkema

- BASF

- Cargill, Incorporated

- Dow

- Engineered Additives LLC

- Evonik Industries AG

- Exxon Mobil Corporation

- Genan Holding A/S

- Honeywell International Inc.

- Iterchimica SpA

- Kao Corporation

- Kraton Corporation

- McAsphalt Industries Limited

- Nouryon

- PQ Corporation

- Sasol

- Shell plc

第7章 市場機會與未來展望

Asphalt Modifiers Market size in 2026 is estimated at USD 4.84 billion, growing from 2025 value of USD 4.60 billion with 2031 projections showing USD 6.26 billion, growing at 5.27% CAGR over 2026-2031.

Expanding public-works budgets, stringent performance-based road specifications, and the gradual switch to sustainable asphalt technologies drive this steady growth. Asia-Pacific retains the largest regional foothold as ambitious highway expansions, heavier traffic loads, and rapid urbanization sustain demand for polymer-modified binders. North America and Europe show mature penetration rates but continue to favor premium modifiers thanks to lifecycle cost savings and net-zero directives. Volatile crude-linked polymer prices, coupled with tighter workplace-safety rules on asphalt fumes, introduce cost and compliance risks in the asphalt modifiers market. Producers counter these pressures by scaling supply chains, widening bio-based portfolios, and deepening technical partnerships with road agencies.

Global Asphalt Modifiers Market Trends and Insights

Infrastructure Spending Rebound in Post-COVID Public Works Programs

Fresh stimulus packages sustain demand for premium binders as agencies favor longer-life pavements over least-cost bids. The U.S. Infrastructure Investment and Jobs Act alone earmarked USD 110 billion for highways and bridges, and comparable funding waves in China, India, and Southeast Asia emphasize polymer-modified asphalt for heavy-duty corridors. These allocations translate into consistent project pipelines that reward suppliers offering proven performance data. Under this funding climate, specification writers increasingly treat modifiers as critical for maximizing return on taxpayer investment.

High Traffic Density and Heavier Axle Loads

Booming e-commerce and industrial activity intensify freight movements, raising axle stresses well above legacy design limits. Field trials show SBS-modified binders boosting dynamic-stability indices by up to tenfold compared with unmodified asphalt, sharply cutting rut depth under truck traffic. Transport ministries now embed polymer requirements in tenders for port approaches and logistics corridors, ensuring recurrent volumes for high-modulus modifiers.

High Upfront Cost of Polymer-Modified Asphalt

Premiums of 15-25% over conventional binders deter adoption where procurement rules still favor lowest initial bids. Municipalities with tight budgets postpone modifier uptake in favor of basic resurfacing, muting short-run growth prospects despite clear lifecycle savings.

Other drivers and restraints analyzed in the detailed report include:

- Adoption of Performance-Based Asphalt Specifications (Superpave)

- Net-Zero Carbon Mandates for Road Construction

- Occupational and Fume-Exposure Health Concerns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Physical modifiers dominated revenue with a 54.10% asphalt modifiers market share in 2025 as SBS and EVA remained ubiquitous for heavy-load and temperature-extreme pavements. Within this segment, SBS captured the lion's portion owing to its elastic recovery and compatibility with refinery-grade asphalt. Chemical modifiers, albeit smaller in volume, are the fastest-growing subset at a 5.36% CAGR, underpinned by warm-mix catalysts and anti-stripping agents that satisfy environmental and moisture-resistance mandates. Rubber crumb modifiers, propelled by tire-recycling incentives, are gaining ground among municipalities aiming to divert waste from landfills while adding resilience to road surfaces. Fiber, mineral, and nano-reinforcement families round out the physical spectrum and answer niche durability demands.

Looking ahead, stakeholders foresee hybrid systems that blend polymers with biochemical rejuvenators to balance stiffness, crack resistance, and sustainability credentials. Flagship projects in Europe showcase lignin-polymer hybrids achieving performance grades equivalent to SBS while claiming lower embodied carbon. Suppliers that secure dependable bio-feedstock streams and master compound-compatibility issues could carve profitable positions as decarbonization accelerates.

The Asphalt Modifiers Report is Segmented by Modifier Type (Physical Modifiers, and Chemical Modifiers), Asphalt Mix Technology (Hot-Mix Asphalt, Warm-Mix Asphalt, and Cold and Half-Warm Mix), Application (Paving, Roofing, and Other Applications), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific held 38.25% asphalt modifiers market share in 2025 and is advancing at a 5.81% CAGR, propelled by multi-trillion-dollar highway and belt-corridor initiatives. China completed more than 120,000 km of high-grade expressways by 2025, and domestic refiners continue debottlenecking SBS lines to meet internal demand. India's corridor programs, coupled with airport-runway expansions, further tilt regional growth toward high-performance binders that outlast monsoon cycles and heavy freight. Southeast Asian members invest in modular asphalt plants designed for quick deployment, which favor ready-to-dose polymer pellets supplied by global majors.

North America is buoyed by the Infrastructure Investment and Jobs Act's long runway of resurfacing projects that embed performance-graded specifications. Over 80% of U.S. state DOTs now require modified asphalt for interstate highways, sustaining a mature but sturdy revenue base. Warm-mix adoption is especially fast in states with aggressive CO2-reduction targets, such as California and Washington, compelling chemical-additive suppliers to localize distribution points.

Europe, while smaller in tonnage, pioneers carbon-optimized binder solutions under Fit-for-55 regulations. The region already mandates warm-mix for many national contracts and sponsors advanced research into lignin-polymer hybrids. Scandinavian agencies, for instance, reimburse contractors for every ton of CO2 saved via low-temperature techniques, thereby amplifying demand for WMA modifiers.

- Arkema

- BASF

- Cargill, Incorporated

- Dow

- Engineered Additives LLC

- Evonik Industries AG

- Exxon Mobil Corporation

- Genan Holding A/S

- Honeywell International Inc.

- Iterchimica SpA

- Kao Corporation

- Kraton Corporation

- McAsphalt Industries Limited

- Nouryon

- PQ Corporation

- Sasol

- Shell plc

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Infrastructure Spending Rebound in Post-COVID Public Works Programs

- 4.2.2 High Traffic Density and Heavier Axle Loads

- 4.2.3 Adoption of Performance-Based Asphalt Specifications (eg., Superpave)

- 4.2.4 Net-Zero Carbon Mandates for Road Construction

- 4.2.5 Surge in Graphene-Enhanced Binder Research

- 4.3 Market Restraints

- 4.3.1 High Upfront Cost of Polymer-Modified Asphalt

- 4.3.2 Occupational and Fume-Exposure Health Concerns

- 4.3.3 Volatile Prices of SBS/SEBS and Other Polymers

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Modifier Type

- 5.1.1 Physical Modifiers

- 5.1.1.1 Plastics (HDPE, SBS, EVA)

- 5.1.1.2 Rubber (crumb-rubber, devulcanized)

- 5.1.1.3 Fibers (cellulose, aramid, glass)

- 5.1.1.4 Mineral fillers and extenders

- 5.1.2 Chemical Modifiers

- 5.1.2.1 Anti-stripping Agents

- 5.1.2.2 Warm-mix Additives

- 5.1.2.3 Rejuvenators and Antioxidants

- 5.1.2.4 Others (nano-clay, graphene)

- 5.1.1 Physical Modifiers

- 5.2 By Asphalt Mix Technology

- 5.2.1 Hot-Mix Asphalt (HMA)

- 5.2.2 Warm-Mix Asphalt (WMA)

- 5.2.3 Cold and Half-Warm Mix

- 5.3 By Application

- 5.3.1 Paving

- 5.3.2 Roofing

- 5.3.3 Other Applications

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN

- 5.4.1.6 Australia

- 5.4.1.7 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Nordic

- 5.4.3.7 Russia

- 5.4.3.8 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 Qatar

- 5.4.5.3 South Africa

- 5.4.5.4 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Arkema

- 6.4.2 BASF

- 6.4.3 Cargill, Incorporated

- 6.4.4 Dow

- 6.4.5 Engineered Additives LLC

- 6.4.6 Evonik Industries AG

- 6.4.7 Exxon Mobil Corporation

- 6.4.8 Genan Holding A/S

- 6.4.9 Honeywell International Inc.

- 6.4.10 Iterchimica SpA

- 6.4.11 Kao Corporation

- 6.4.12 Kraton Corporation

- 6.4.13 McAsphalt Industries Limited

- 6.4.14 Nouryon

- 6.4.15 PQ Corporation

- 6.4.16 Sasol

- 6.4.17 Shell plc

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Emerging Preference for Warm-Mix Asphalt

2026年全球經銷商市場報告

2026年全球經銷商市場報告 2026-2034年全球瀝青市場規模、佔有率、趨勢和成長分析報告

2026-2034年全球瀝青市場規模、佔有率、趨勢和成長分析報告 瀝青市場規模、佔有率和成長分析:按產品類型、應用和地區分類-2026-2033年產業預測

瀝青市場規模、佔有率和成長分析:按產品類型、應用和地區分類-2026-2033年產業預測 瀝青市場:依產品類型、應用、終端用戶產業及地區分類

瀝青市場:依產品類型、應用、終端用戶產業及地區分類 再生瀝青:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)2026年全球再生瀝青市場報告全球再生瀝青市場規模、佔有率、趨勢和成長分析報告(2026-2034)

再生瀝青:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)2026年全球再生瀝青市場報告全球再生瀝青市場規模、佔有率、趨勢和成長分析報告(2026-2034) 瀝青市場:依產品類型、技術、應用、最終用戶和通路分類-2026-2032年全球預測瀝青改質劑市場:按類型、技術、形態、應用和最終用戶分類-2026-2032年全球預測

瀝青市場:依產品類型、技術、應用、最終用戶和通路分類-2026-2032年全球預測瀝青改質劑市場:按類型、技術、形態、應用和最終用戶分類-2026-2032年全球預測 耐輻射潤滑劑和潤滑脂市場規模、佔有率和成長分析:按產品類型、等級、基礎油類型、添加劑類型、應用、最終用途產業和地區分類-2026-2033年產業預測

耐輻射潤滑劑和潤滑脂市場規模、佔有率和成長分析:按產品類型、等級、基礎油類型、添加劑類型、應用、最終用途產業和地區分類-2026-2033年產業預測