|

市場調查報告書

商品編碼

2062106

耐候鋼:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Weathering Steel - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

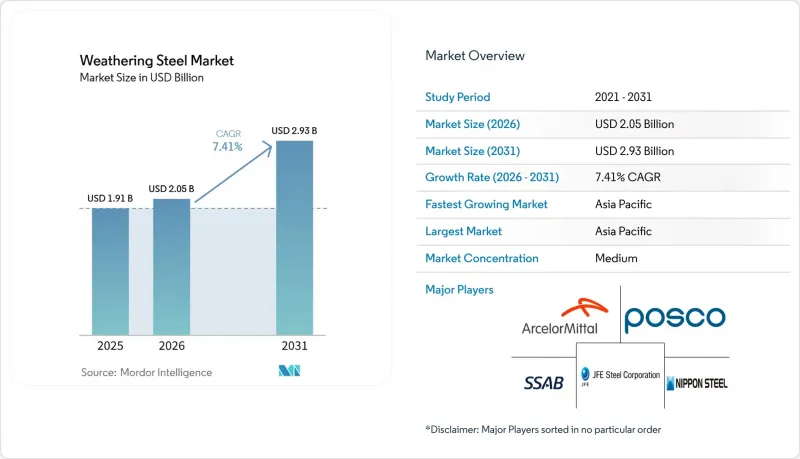

據 Mordor Intelligence 稱,耐候鋼市場在 2025 年的價值為 19.1 億美元,預計到 2031 年將從 2026 年的 20.5 億美元成長到 29.3 億美元,在預測期(2026-2031 年)內的複合年成長率為 7.41%。

本報告按類型(A588、A242、A606、ASTM A709 Gr50W 等)、形狀(板材、薄板、捲材等)、終端用戶行業(建築施工、橋樑及土木基礎設施、交通運輸、工業廠房及機械等)及地區(亞太地區、北美地區、歐洲地區、南美地區進行細分。市場預測以美元計價。

全球耐候鋼市場趨勢及洞察

脫碳措施正在促進低維護成本鋼鐵的發展。

鋼鐵製造商目前正將生命週期碳核算納入其產品線。這項轉變對耐候鋼尤為有利,因為取消塗層系統不僅可以去除揮發性有機化合物,還能減少日常維護相關的排放。安賽樂米塔爾的XCarb重型鋼板採用超過75%的廢鋼製成,並在完全運作再生能源的電弧爐(EAF)中生產,與維斯塔斯Nordlicht 1離岸風力發電項目中使用的傳統高爐鋼相比,碳強度成功降低了36%。自2026年1月起,歐盟碳邊境調節機制(CBAM)將對高碳足跡的進口產品徵收關稅。此舉鼓勵買家選擇經認證的低碳耐候鋼。作為策略性舉措,塔塔鋼鐵正投資32億美元擴建位於卡林加納加爾的工廠,並安裝一條專門用於生產高強度耐候鋼板的生產線。此舉使塔塔鋼鐵能夠同時滿足國內基礎建設熱潮及符合CBAM標準的出口市場需求。目前,需求主要由歐洲和北美主導,但隨著全球碳定價收緊,預計需求將在中期達到高峰。

城市建築中「天氣色調」的美學吸引力

2025年,設計入口網站Dezeen重點介紹了10個代表性項目,展現了建築師對不斷變化的銹褐色紋理日益成長的興趣,這種紋理因其獨特的質感和深度而備受青睞。新加坡和多倫多的市政當局修訂了相關指南,詳細規定了排水解決方案,以防止相鄰立面受到污染。此舉加快了裸露耐候鋼的核准流程。同時,2026年3月,JFE鋼鐵公司在宮雪橋推出了其「FLExB」輪胎邊緣。這項創新技術透過實現更平滑的表面並顯著減少水流,解決了行人區域的一大難題。隨著開創性建築的湧現和這種材料的不斷應用,預計這一建築趨勢將在短期內對人口密集的城市中心產生影響。

海洋/高鹽度環境中的銅綠劣化

2025年,《建築》(Buildings)雜誌的一項研究顯示,墨西哥灣沿岸的橋樑正面臨過早的截面損失。基於這些發現,路易斯安那州、奧勒岡州和華盛頓州的運輸部禁止在距離鹹水區10英里半徑範圍內使用耐候鋼。同樣,儘管離岸風力發電基礎正逐漸轉向熱鍍鋅和環氧塗層,但2025年在美國大西洋沿岸開工的五個項目(總投資超過280億美元)均未使用傳統的耐候鋼。日本製鐵住友金屬公司研發的CORSPACE混合鋼於2024年在瓦努阿圖的一座橋樑上進行了試驗應用,其特點是延長了塗層更換週期。然而,在內陸項目中,它將面臨來自傳統耐候鋼的直接競爭。由於鹽霧的限制,預計中期內沿海地區的市場佔有率成長將受到抑制。

細分市場分析

到2025年,A588的市佔率將達到41.11%,凸顯其在公路橋樑和輸電塔領域的長期領先地位。同時,ASTM A709 Gr50W的市佔率正以7.88%的複合年成長率快速成長,其優異的韌性和焊接性能使其在地震多發地區備受橋樑工程師的青睞。此外,鞍鋼的Q500qE鋼板以其減重50%的優勢而聞名,在2026年1月訂購的800米長江宜昌東灘大橋項目中發揮了關鍵作用。隨著各機構日益重視抗震性能標準,基於A709標準的橋樑應用市場預計將穩定成長。

儘管庫存合理化降低了對傳統A242的需求,但諸如SSAB公司於2025年3月推出的Strenx Weathering 700和960等新型專有高強度產品,正在為採礦和海上設備行業開拓利基市場。此外,剛在2024年10月發布的ASTM A588-24標準,收緊了化學成分和衝擊測試規程,從而促進了跨市場認證。因此,這種向更高等級產品的轉變預計將推動耐候鋼市場中優質鋼板市場佔有率的成長。

區域分析

預計到2025年,亞太地區將佔全球銷售額的46.13%,並維持8.02%的年均成長率至2031年。推動這一蓬勃發展的地區主要得益於中國雄心勃勃的橋樑建設計畫、印度卡林加納加爾年產能8萬噸的擴建以及日本在軟性焊接技術方面的創新。此外,東協的高速公路走廊和韓國的離岸風力發電建設也促進了需求的成長。

自2025年6月起,北美將依據《232條款》享有50%的關稅,進而保障美國國內鋼鐵廠的利益。為此,蓋爾道公司計劃在2025年將其結構鋼出貨量提高8.5%,達到259萬噸,並正按計畫推進在德克薩斯州新增15萬噸電弧爐(EAF)產能,目標是在2026年底前完成。同時,美國電網營運商計劃在2025年向電網投資總計1,150億美元,這將進一步增加對耐候樁和電線杆的需求。

歐洲正將重心轉向低碳鋼板。例如,安賽樂米塔爾向維斯塔斯交付的XCarb產品使其塔筒排放減少了36%。同時,蒂森克虜伯在杜伊斯堡投資8.7億美元的維修計畫以及薩爾茲吉特於2026年6月收購HKM(產能6萬噸)正在重塑歐洲的產能格局。此外,預計從2026年起實施的碳邊境調節機制(CBAM)將推高電弧爐用耐候鋼的國內溢價。

在南美洲,由於當局努力遏制補貼產品的湧入,進口激增,迫使蓋爾道公司(Geldau)將2026年的資本支出削減了20%。儘管如此,巴西、阿根廷和智利仍然優先採購用於高架橋和太陽能發電廠的耐候鋼板。同時,中東和非洲的需求主要集中在海灣國家的橋樑、海水淡化廠以及南非的採礦業,像克利夫蘭橋樑鋼鐵公司(Cleveland Bridge Steel)這樣的區域加工商正在加強產能以滿足這些需求。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 隨著脫碳進程的推進,維護需求較低的鋼鐵材料也越來越受到重視。

- 城市建築中與天氣相關的色彩所具有的美學吸引力

- 與鍍鋅鋼和塗層鋼相比,具有生命週期成本優勢。

- 擴大在貨櫃型資料中心和撬裝設備的應用

- 採用安裝在高海拔地區的太陽能追蹤器支撐桿

- 市場限制因素

- 海洋和高鹽度環境中的銅綠劣化

- 具有卓越ESG性能的新興「綠色鋼鐵」等級

- 設計師對色彩變化的抗拒情緒

- 價值鏈分析

- 波特五力模型

第5章 市場規模與成長預測

- 按類型

- A588

- A242

- A606

- ASTM A709 Gr50W

- 其他

- 按形式

- 盤子

- 片材和卷材

- 鋼筋和結構鋼

- 管道和管材

- 其他

- 按最終用戶行業分類

- 建築/施工

- 橋樑和民用基礎設施

- 交通運輸(鐵路車輛、造船)

- 工業廠房和機械

- 美術作品、雕塑、公共家具

- 可再生能源結構

- 其他

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 東南亞國協

- 其他亞太國家

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐國家

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲國家

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- ArcelorMittal

- Bluescope Steel Limited

- China Ansteel Group Corporation Limited

- Dillinger Hutte

- Gerdau S/A

- HBIS Group

- JFE Steel Corporation

- LIBERTY Steel Group

- NIPPON STEEL CORPORATION

- Oklahoma Steel & Wire, Inc.

- POSCO

- Salzgitter Flachstahl GmbH

- Severstal PJSC

- Shandong Baosteel Industry Co., Ltd

- SSAB AB

- Tata Steel

- Thyssenkrupp AG

- United States Steel Corporation

第7章 市場機會與未來展望

According to Mordor Intelligence, the weathering steel market size was valued at USD 1.91 billion in 2025 and is estimated to grow from USD 2.05 billion in 2026 to reach USD 2.93 billion by 2031, at a CAGR of 7.41% during the forecast period (2026-2031).

This report is Segmented by Type (A588, A242, A606, ASTM A709 Gr50W, Others), Form (Plates, Sheets and Coils, and More), End-User Industry (Building and Construction, Bridges and Civil Infrastructure, Transportation, Industrial Plant and Machinery, and More), and Geography (Asia-Pacific, North America, Europe, South America, Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Weathering Steel Market Trends and Insights

Decarbonization Push Favoring Low-Maintenance Steels

Steelmakers are now embedding lifecycle-carbon accounting into their product offerings. This shift is particularly advantageous for weathering grades, as the removal of paint systems not only eliminates volatile organic compounds but also reduces emissions from recurring maintenance. ArcelorMittal's XCarb heavy plates, crafted in electric arc furnaces (EAFs) using over 75% scrap and powered entirely by renewable electricity, have achieved a 36% reduction in carbon intensity for Vestas' Nordlicht 1 offshore wind project when compared to traditional blast-furnace steel. Starting January 2026, the EU's Carbon Border Adjustment Mechanism will impose tariffs on imports with high carbon footprints. This move is nudging buyers towards certified low-carbon weathering grades. In a strategic move, Tata Steel is channeling USD 3.2 billion into its Kalinganagar expansion, introducing dedicated lines for high-strength weathering plates. This positions Tata to cater to both the domestic infrastructure boom and the export markets that align with CBAM standards. Currently, Europe and North America lead in demand, but as global carbon pricing tightens, a peak is anticipated in the medium term.

Aesthetic Weather-Tone Appeal in Urban Architecture

In 2025, design portal Dezeen spotlighted 10 signature projects, showcasing architects' growing admiration for the evolving rust-brown patina, valued for its unique texture and depth. Municipalities in Singapore and Toronto have updated their guidelines, detailing drainage solutions to prevent staining on nearby facades. This move has expedited approvals for the use of exposed weathering steel. Meanwhile, JFE Steel introduced its FLExB weld bead on the Miyuki Bridge in March 2026. This innovation promises smoother surfaces, significantly reducing runoff marks and addressing a primary concern in pedestrian areas. As flagship buildings emerge, setting material precedents, this architectural trend is expected to influence dense urban centers in the short term.

Patina Breakdown in Marine/High-Chloride Climates

In 2025, a study by Buildings journal highlighted premature section loss on bridges along the Gulf Coast. This finding led the DOTs of Louisiana, Oregon, and Washington to impose a ban on weathering steel within a 10-mile radius of saltwater. Similarly, while offshore wind foundations are turning to hot-dip galvanizing or epoxy coatings, the five U.S. Atlantic projects, collectively valued at over USD 28 billion and under construction in 2025, have steered clear of conventional weathering grades. Nippon Steel's CORSPACE hybrid plate, which was trialed on a bridge in Vanuatu in 2024, boasts extended repainting intervals. However, it finds itself in direct competition with traditional weathering plates for inland projects. Due to salt-spray limitations, growth in market share near coastal areas is expected to be restrained in the medium term.

Other drivers and restraints analyzed in the detailed report include:

- Lifecycle-Cost Edge Over Galvanized and Coated Steels

- Growing Use in Containerized Data-Center Skids

- Emerging Green-Steel Grades with Superior ESG

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, A588 captured 41.11% of the market share, highlighting its long-standing leadership in highway girders and transmission towers. Meanwhile, ASTM A709 Gr50W is on the rise, with a 7.88% CAGR, due to its preferred toughness and weldability among bridge engineers in seismic zones. Additionally, Ansteel's Q500qE plate, recognized for its 50% weight reduction, was pivotal in the 800 m Yichang Dongyan Yangtze span project, awarded in January 2026. As agencies increasingly prioritize performance-based specifications that emphasize seismic resilience, the market for A709-based bridge applications is expected to grow steadily.

While demand for the legacy A242 is declining due to inventory rationalization, new proprietary high-strength products like SSAB's Strenx Weathering 700 and 960, introduced in March 2025, are creating niches in mining and offshore equipment. Furthermore, the recently published ASTM A588-24 standard in October 2024, which tightens chemistry and impact-test protocols, is facilitating cross-market certifications. As a result, the weathering steel market is anticipated to see an increase in the share of premium plates, driven by these higher-grade substitutions.

Geography Analysis

Asia-Pacific, commanding 46.13% of 2025's revenue, is projected to grow at a rate of 8.02% through 2031. The region's dynamism is supported by China's ambitious bridge program, India's 8 metric tons per annum Kalinganagar expansion, and Japan's FLExB weld innovation. Additionally, ASEAN's highway corridors and South Korea's offshore wind yards contribute to the incremental tonnage.

Since June 2025, North America has reaped the benefits of 50% Section 232 tariffs, providing a shield for domestic mills. Gerdau, in response, boosted its 2025 shapes shipments by 8.5% to reach 2.59 metric tons and is on track to introduce an additional 150 kilotons of EAF capacity in Texas by late 2026. Meanwhile, U.S. grid operators invested a total of USD 115 billion into transmission in 2025, spurring a heightened demand for weathering piles and poles.

Europe is pivoting towards a low-carbon plate. For example, ArcelorMittal's XCarb deliveries to Vestas achieved a 36% reduction in tower emissions. Concurrently, ThyssenKrupp's USD 870 million revamp in Duisburg and Salzgitter's takeover of 6 metric tons HKM in June 2026 are reshaping the continent's capacity landscape. Furthermore, the enforcement of CBAM from 2026 is set to bolster domestic premiums for certified EAF weathering grades.

In South America, Gerdau has slashed its 2026 capex by 20% due to a surge in imports, as authorities struggled to curb subsidized inflows. Nevertheless, Brazil, Argentina, and Chile continue to prioritize weathering plates for their viaducts and solar farms. Meanwhile, the Middle East & Africa's demand is concentrated around Gulf bridges, desalination plants, and South African mining, with regional fabricators like Cleveland Bridge Steel stepping up to meet these needs.

- ArcelorMittal

- Bluescope Steel Limited

- China Ansteel Group Corporation Limited

- Dillinger Hutte

- Gerdau S/A

- HBIS Group

- JFE Steel Corporation

- LIBERTY Steel Group

- NIPPON STEEL CORPORATION

- Oklahoma Steel & Wire, Inc.

- POSCO

- Salzgitter Flachstahl GmbH

- Severstal PJSC

- Shandong Baosteel Industry Co., Ltd

- SSAB AB

- Tata Steel

- Thyssenkrupp AG

- United States Steel Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Decarbonisation push favouring low-maintenance steels

- 4.2.2 Aesthetic weather-tone appeal in urban architecture

- 4.2.3 Lifecycle-cost edge over galvanised and coated steels

- 4.2.4 Growing use in containerised data-centre skids

- 4.2.5 Adoption in high-altitude solar tracker columns

- 4.3 Market Restraints

- 4.3.1 Patina breakdown in marine/high-chloride climates

- 4.3.2 Emerging "green-steel" grades with superior ESG

- 4.3.3 Designer push-back over perceived colour drift

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 A588

- 5.1.2 A242

- 5.1.3 A606

- 5.1.4 ASTM A709 Gr50W

- 5.1.5 Others

- 5.2 By Form

- 5.2.1 Plates

- 5.2.2 Sheets and Coils

- 5.2.3 Bars and Sections

- 5.2.4 Pipes and Tubes

- 5.2.5 Others

- 5.3 By End-user Industry

- 5.3.1 Building and Construction

- 5.3.2 Bridges and Civil Infrastructure

- 5.3.3 Transportation (Railcar, Shipbuilding)

- 5.3.4 Industrial Plant and Machinery

- 5.3.5 Art, Sculpture and Public Furniture

- 5.3.6 Renewable Energy Structures

- 5.3.7 Others

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 NORDIC Countries

- 5.4.3.8 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, and Recent Developments)

- 6.4.1 ArcelorMittal

- 6.4.2 Bluescope Steel Limited

- 6.4.3 China Ansteel Group Corporation Limited

- 6.4.4 Dillinger Hutte

- 6.4.5 Gerdau S/A

- 6.4.6 HBIS Group

- 6.4.7 JFE Steel Corporation

- 6.4.8 LIBERTY Steel Group

- 6.4.9 NIPPON STEEL CORPORATION

- 6.4.10 Oklahoma Steel & Wire, Inc.

- 6.4.11 POSCO

- 6.4.12 Salzgitter Flachstahl GmbH

- 6.4.13 Severstal PJSC

- 6.4.14 Shandong Baosteel Industry Co., Ltd

- 6.4.15 SSAB AB

- 6.4.16 Tata Steel

- 6.4.17 Thyssenkrupp AG

- 6.4.18 United States Steel Corporation

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

2026-2030年全球塗層鋼市場

2026-2030年全球塗層鋼市場 塗層鋼市場:2026-2032年全球市場預測(按塗層類型、塗層技術、基材等級、銷售管道、應用和最終用途行業分類)耐候鋼市場:依產品類型、技術、應用及通路分類-2026-2032年全球市場預測

塗層鋼市場:2026-2032年全球市場預測(按塗層類型、塗層技術、基材等級、銷售管道、應用和最終用途行業分類)耐候鋼市場:依產品類型、技術、應用及通路分類-2026-2032年全球市場預測 塗層鋼:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

塗層鋼:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 全球塗層鋼板市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球塗層鋼板市場規模、佔有率、趨勢和成長分析報告(2026-2034) 2026年全球耐候鋼市場報告鉻碳化物堆焊板市場按產品類型、塗層厚度、終端用戶產業、應用和銷售管道,全球預測(2026-2032年)

2026年全球耐候鋼市場報告鉻碳化物堆焊板市場按產品類型、塗層厚度、終端用戶產業、應用和銷售管道,全球預測(2026-2032年) 耐候鋼市場規模、佔有率及成長分析(按類型、形式、供應、最終用途產業及地區分類)-2026-2033年產業預測

耐候鋼市場規模、佔有率及成長分析(按類型、形式、供應、最終用途產業及地區分類)-2026-2033年產業預測 全球耐候鋼市場按類型、最終用途產業、材料類型和地區分類

全球耐候鋼市場按類型、最終用途產業、材料類型和地區分類 塗層鋼市場規模、佔有率、趨勢分析報告:按產品、最終用途、地區、細分市場預測,2025-2030 年

塗層鋼市場規模、佔有率、趨勢分析報告:按產品、最終用途、地區、細分市場預測,2025-2030 年