|

市場調查報告書

商品編碼

1940634

塗層鋼:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Coated Steel - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

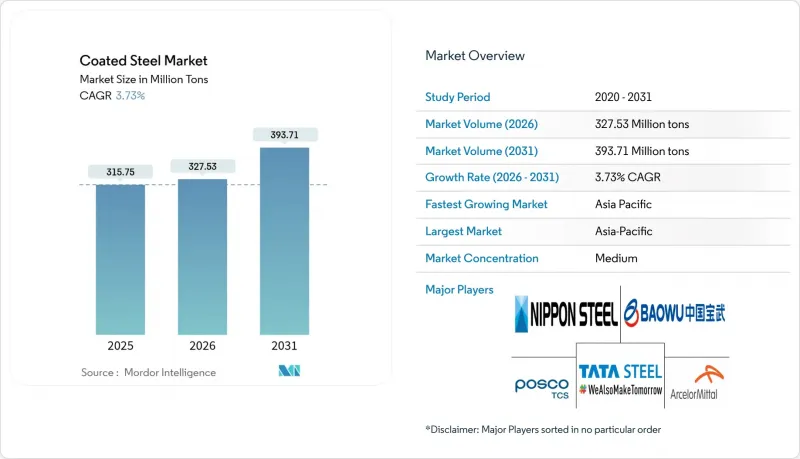

2025年塗層鋼市場價值為3.1575億噸,預計到2031年將達到3.9371億噸,而2026年為3.2753億噸。

預計在預測期(2026-2031 年)內,複合年成長率將達到 3.73%。

這一成長反映了汽車輕量化項目的強勁需求、節能建築圍護結構的推廣以及主要生產基地產能的持續擴張。鋅鋁鎂合金塗層的加速商業化(與傳統鍍鋅產品相比,其使用壽命更長)進一步推動了這種成長動能。生產商也積極推動垂直整合和可再生能源業務,以避免原料價格波動風險並遵守日益嚴格的碳排放法規。貿易救濟措施,特別是美國對耐腐蝕進口產品徵收的反傾銷稅,正在重塑區域供應鏈格局,同時鼓勵國內投資。同時,歐盟的碳邊境調節機制(CBAM)正在加快產品排放的揭露,使得經認證的低碳塗層鋼能夠獲得溢價。

全球塗層鋼市場趨勢及展望

輕型電動車對高強度鋼基塗層鋼的需求激增

電動車製造商目前正指定使用高抗張強度鋼結合塗層來保護電池機殼和碰撞結構,同時還要承受複雜的成型過程。安賽樂米塔爾投資12億美元的阿拉巴馬州電鋼計劃正是順應這股趨勢的策略性資本配置。鋅鋁鎂合金的化學成分賦予了塗層高強度鋼(AHSS)雷射焊接電池組所需的邊緣耐腐蝕性,使其成為傳統汽車用鋼與下一代汽車技術之間的橋樑。

預塗漆卷材在節能建築外牆的應用

冷凍負載法規正在推動採用太陽反射率不低於0.7、熱輻射率不低於0.8的塗層盤管屋頂。亞洲開發銀行的實地研究表明,在熱帶地區,冷屋頂可減少15%至20%的冷凍能耗。基於聚偏氟乙烯(PVDF)的塗層,例如Kynar 500,可提供30年質保,從而提高生命週期經濟效益,並幫助建築商達到LEED和歐盟生態設計標準。

鋅鋁價格波動

2024年底,現貨鋅價收於每噸人民幣25,900元(年增19.8%),但由於礦場作業中斷與需求波動,2025年第一季跌至每噸人民幣23,370元。鋁價也出現類似波動,導致鋅鋁鎂合金和鋁電鍍生產線的採購更加複雜。成本轉嫁和合約滯後交織的領域,利潤壓力最為嚴峻。

細分市場分析

截至2025年,熱鍍鋅鋼板將佔鍍鋅鋼板市場佔有率的63.10%,相當於約1.99億噸。到2031年,熱浸鍍鋅鋼板市場將以3.89%的複合年成長率成長,這將成為傳統建築、家電和倉儲應用領域鍍鋅鋼板市場規模的基礎。電鍍鋅和鍍鋁產品在高精度、高溫應用等細分市場成長更為迅速,但從資本投資效率的角度來看,產能擴張的重點仍是熱鍍鋅線。

塗層鋼產業正轉向「其他」類別中的鋅鋁鎂合金,其中AM/NS印度公司的Magnelis產品提供的耐腐蝕壽命是熱鍍鋅的三到五倍。製造商正在將雷射焊接塗層應用於汽車車體,這表明熱鍍鋅的產量不會徹底下降,而是逐漸被新一代塗層所取代。

本《塗層鋼市場報告》依產品類型(熱鍍鋅、鍍鋅退火、電鍍鋅、鍍鋁及其他)、應用領域(建築結構構件、汽車零件、家用電器、管道及其他)和地區(亞太地區、北美地區、歐洲地區、南美地區、中東和非洲)進行細分。市場預測以噸為單位。

區域分析

預計到2025年,亞太地區將佔據全球鍍鋅鋼市場61.10%的佔有率(超過1.93億噸),並預計到2031年將以4.47%的複合年成長率成長。中國憑藉其綜合性鋼鐵廠升級下游生產線,主導;而印度、韓國和日本則在出口特種產品。東南亞國協正在擴大其產能,以滿足太陽能、物流和住宅計劃的需求,這進一步增強了區域鍍鋅鋼市場的韌性。

北美位居第二。美國對來自10個國家的耐腐蝕鋼材徵收反傾銷稅,縮小了進口選擇範圍,促使相關企業進行投資,例如紐柯公司在南卡羅來納州投資4.25億美元建設鍍鋅生產線,以及現代鋼鐵公司在路易斯安那州投資58億美元建設綜合工廠。墨西哥在2025年至2026年間新增800萬噸產能,正在加強近岸外包,並平衡該地區的塗層鋼市場。

歐洲正面臨能源成本飆升和碳邊境調節機制(CBAM)帶來的挑戰。生產商正在提交環境產品聲明(EPD),以確保在建築業獲得溢價並降低碳課稅。德國、法國、義大利和英國仍然是主要的消費國,而北歐鋼鐵廠則專注於可再生能源和海洋領域。有關循環經濟和廢鋼利用的監管確定性將影響歐洲塗層鋼市場的競爭力。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 輕型電動車對基於高抗張強度鋼(AHSS)的塗層鋼的需求激增

- 在節能建築圍護結構中使用預塗漆卷材。

- 亞洲鋅鋁鎂合金塗層生產線的快速引進

- 稅收優惠的家電置換計畫(歐盟和美國)

- 經認證的低碳(EPD/CBAM相容)塗層鋼

- 市場限制

- 鋅鋁價格波動

- 鋁複合材料建築幕牆的替代方案

- 針對塗層鋼的反傾銷/反補貼稅貿易措施

- 價值鏈分析

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章 市場規模與成長預測

- 依產品類型

- 熱浸電鍍

- 鍍鋅

- 電鍍

- 鋁化

- 其他產品類型

- 透過使用

- 建築構件

- 汽車零件

- 家用電器

- 管道和管材

- 其他用途

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 東南亞國協

- 亞太其他地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 俄羅斯

- 北歐國家

- 其他歐洲地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- AM/NS INDIA

- ArcelorMittal

- China Baowu Steel Group Corp., Ltd

- CUMIC STEEL LIMITED

- JFE Steel Corporation

- Jindal Steel

- JSW

- KOBE STEEL, LTD.

- MMK(PJSC)

- Nippon Steel Coated Sheet Corporation

- NLMK

- NS BlueScope

- Nucor Corporation

- POSCO Coated Steel(Thailand)Co.,Ltd.

- Salzgitter Flachstahl GmbH

- SSAB AB

- Tata Steel

- thyssenkrupp Steel

- United States Steel Corporation

- voestalpine Stahl GmbH

第7章 市場機會與未來展望

The Coated Steel Market was valued at 315.75 Million tons in 2025 and estimated to grow from 327.53 Million tons in 2026 to reach 393.71 Million tons by 2031, at a CAGR of 3.73% during the forecast period (2026-2031).

This growth reflects resilient demand from automotive lightweighting programs, expanding energy-efficient building envelopes, and sustained capacity additions in key production hubs. Momentum is reinforced by quicker commercialization of Zn-Al-Mg alloy coatings that extend service life versus conventional galvanized products. Producers are also pursuing vertical integration and renewable-powered operations to hedge raw-material volatility and meet tightening carbon rules. Trade remedies-most notably the United States' anti-dumping duties on corrosion-resistant imports-reshape regional supply flows while favoring domestic investments. At the same time, EU carbon-border pricing accelerates disclosure of embedded emissions, allowing certified low-carbon coated steel to command premiums.

Global Coated Steel Market Trends and Insights

Surging Demand for AHSS-Based Coated Steels in EV Lightweighting

Electric-vehicle producers now specify advanced high-strength steel grades paired with coatings that survive complex forming while protecting battery enclosures and crash structures. ArcelorMittal's USD 1.2 billion Alabama electrical-steel project illustrates strategic capital alignment with this trend. Zn-Al-Mg chemistries offer edge-corrosion resistance crucial for laser-welded battery packs, positioning coated AHSS as a bridge between legacy auto steel and next-generation mobility.

Energy-Efficient Building Envelope Adoption of Pre-Painted Coil

Cooling-load regulations spur use of pre-painted coil achieving solar reflectance above 0.7 and thermal emittance beyond 0.8. Asian Development Bank field work shows cool roofs can cut cooling energy 15-20% in tropical settings. PVDF-based coatings such as Kynar 500 provide 30-year warranties that improve lifecycle economics while helping builders meet LEED and EU Ecodesign thresholds.

Zinc and Aluminum Price Volatility

Spot zinc closed 2024 at RMB 25,900 per ton, up 19.8% year-on-year, before easing to RMB 23,370 in Q1 2025 amid mine disruptions and demand swings. Aluminum shows similar gyrations, complicating procurement for Zn-Al-Mg and aluminized lines. Margin compression is most severe where passing costs downstream meets contract lags.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Rollout of Zn-Al-Mg Alloy Coating Lines in Asia

- Tax-Driven Appliance Replacement Programs (EU and US)

- Aluminum-Composite Facade Substitution

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hot-dipped material held 63.10% of coated steel market share in 2025, equating to roughly 199 million tons. Its 3.89% CAGR through 2031 anchors the coated steel market size for traditional construction, appliance, and storage uses. Electro-galvanized and aluminized alternatives grow faster in high-precision or high-temperature niches, but capacity build-outs center on hot-dip lines due to capital efficiency.

The coated steel industry is pivoting toward Zn-Al-Mg alloys classified in the "Others" bucket, where AM/NS India's Magnelis offers 3-5 times galvanized corrosion life. Producers integrate laser-welding-friendly chemistries for auto body-in-white, suggesting hot-dipped volume will gradually cede mix share to next-generation coatings rather than suffer absolute decline.

The Coated Steel Market Report is Segmented by Product Type (Hot-Dipped, Galvannealed, Electro-Galvanized, Aluminized, and Others), Application (Construction and Building Components, Automotive Components, Appliances, Pipe and Tubular, and Other Applications), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Volume (Tons).

Geography Analysis

Asia-Pacific commanded 61.10% of coated steel market share in 2025-just over 193 million tons-and is projected at a 4.47% CAGR to 2031. China leads with integrated mills upgrading downstream lines, while India, South Korea, and Japan export specialty products. ASEAN nations expand capacity for solar, logistics, and housing projects, enhancing regional coated steel market resilience.

North America ranks second. U.S. anti-dumping tariffs covering corrosion-resistant sheet from 10 countries have narrowed import options, encouraging investments such as Nucor's USD 425 million South Carolina galvanizing line and Hyundai Steel's USD 5.8 billion Louisiana integrated plant. Mexico's 8 million-ton capacity additions over 2025-2026 reinforce near-shoring, keeping the coated steel market in the hemisphere balanced.

Europe confronts energy-cost spikes and CBAM compliance. Producers showcase Environmental Product Declarations to secure architectural premiums and mitigate carbon levies. Germany, France, Italy, and the United Kingdom remain anchor consumers, while Nordic mills focus on renewables and marine segments. Regulatory certainty on circularity and scrap use will shape Europe's coated steel market competitiveness.

- AM/NS INDIA

- ArcelorMittal

- China Baowu Steel Group Corp., Ltd

- CUMIC STEEL LIMITED

- JFE Steel Corporation

- Jindal Steel

- JSW

- KOBE STEEL, LTD.

- MMK (PJSC)

- Nippon Steel Coated Sheet Corporation

- NLMK

- NS BlueScope

- Nucor Corporation

- POSCO Coated Steel(Thailand) Co.,Ltd.

- Salzgitter Flachstahl GmbH

- SSAB AB

- Tata Steel

- thyssenkrupp Steel

- United States Steel Corporation

- voestalpine Stahl GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging Demand for AHSS-Based Coated Steels in EV Lightweighting

- 4.2.2 Energy-Efficient Building Envelope Adoption of Pre-Painted Coil

- 4.2.3 Rapid Rollout of Zn-Al-Mg Alloy Coating Lines In Asia

- 4.2.4 Tax-Driven Appliance Replacement Programs (EU And US)

- 4.2.5 Certified Low-Carbon (EPD/CBAM-Ready) Coated Steels

- 4.3 Market Restraints

- 4.3.1 Zinc And Aluminium Price Volatility

- 4.3.2 Aluminium-Composite Facade Substitution

- 4.3.3 AD/CVD Trade Actions on Coated Sheet

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitute Products

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Product Type

- 5.1.1 Hot-dipped

- 5.1.2 Galvannealed

- 5.1.3 Electro-galvanized

- 5.1.4 Aluminized

- 5.1.5 Others Product Types

- 5.2 By Application

- 5.2.1 Construction and Building Components

- 5.2.2 Automotive Components

- 5.2.3 Appliances

- 5.2.4 Pipe and Tubular

- 5.2.5 Other Applications

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Russia

- 5.3.3.6 NORDIC Countries

- 5.3.3.7 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 AM/NS INDIA

- 6.4.2 ArcelorMittal

- 6.4.3 China Baowu Steel Group Corp., Ltd

- 6.4.4 CUMIC STEEL LIMITED

- 6.4.5 JFE Steel Corporation

- 6.4.6 Jindal Steel

- 6.4.7 JSW

- 6.4.8 KOBE STEEL, LTD.

- 6.4.9 MMK (PJSC)

- 6.4.10 Nippon Steel Coated Sheet Corporation

- 6.4.11 NLMK

- 6.4.12 NS BlueScope

- 6.4.13 Nucor Corporation

- 6.4.14 POSCO Coated Steel(Thailand) Co.,Ltd.

- 6.4.15 Salzgitter Flachstahl GmbH

- 6.4.16 SSAB AB

- 6.4.17 Tata Steel

- 6.4.18 thyssenkrupp Steel

- 6.4.19 United States Steel Corporation

- 6.4.20 voestalpine Stahl GmbH

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

2026-2030年全球塗層鋼市場

2026-2030年全球塗層鋼市場 耐候鋼:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

耐候鋼:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 塗層鋼市場:2026-2032年全球市場預測(按塗層類型、塗層技術、基材等級、銷售管道、應用和最終用途行業分類)耐候鋼市場:依產品類型、技術、應用及通路分類-2026-2032年全球市場預測

塗層鋼市場:2026-2032年全球市場預測(按塗層類型、塗層技術、基材等級、銷售管道、應用和最終用途行業分類)耐候鋼市場:依產品類型、技術、應用及通路分類-2026-2032年全球市場預測 全球塗層鋼板市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球塗層鋼板市場規模、佔有率、趨勢和成長分析報告(2026-2034) 2026年全球耐候鋼市場報告鉻碳化物堆焊板市場按產品類型、塗層厚度、終端用戶產業、應用和銷售管道,全球預測(2026-2032年)

2026年全球耐候鋼市場報告鉻碳化物堆焊板市場按產品類型、塗層厚度、終端用戶產業、應用和銷售管道,全球預測(2026-2032年) 耐候鋼市場規模、佔有率及成長分析(按類型、形式、供應、最終用途產業及地區分類)-2026-2033年產業預測

耐候鋼市場規模、佔有率及成長分析(按類型、形式、供應、最終用途產業及地區分類)-2026-2033年產業預測 全球耐候鋼市場按類型、最終用途產業、材料類型和地區分類

全球耐候鋼市場按類型、最終用途產業、材料類型和地區分類 塗層鋼市場規模、佔有率、趨勢分析報告:按產品、最終用途、地區、細分市場預測,2025-2030 年

塗層鋼市場規模、佔有率、趨勢分析報告:按產品、最終用途、地區、細分市場預測,2025-2030 年