|

市場調查報告書

商品編碼

2062089

印度金屬積層製造:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)India Metal Additive Manufacturing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

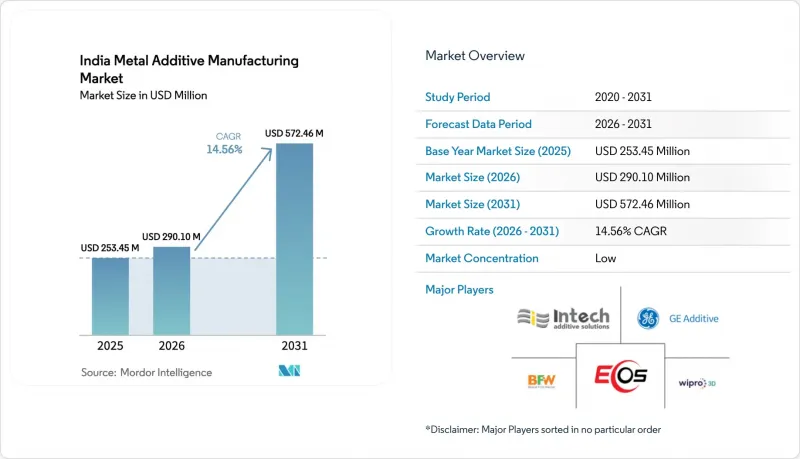

據 Mordor Intelligence 稱,2025 年印度金屬積層製造市場價值為 2.5345 億美元,預計到 2031 年將達到 5.7246 億美元,而 2026 年為 2.901 億美元,在預測期(2026-2031 年)內複合年成長率為 14.56%。

本報告按技術(粉末層熔融、黏著劑噴塗成型等)、材料類型(不銹鋼、鋁等)、終端應用產業(航太與國防、汽車、醫療與牙科、石油天然氣與能源、模具與工業產品、電子與半導體、建築、珠寶與藝術品)以及地區進行細分。市場預測以美元以金額為準。

印度金屬積層製造市場趨勢與洞察

擴大航太和國防領域的國內生產計劃

資本投資的增加和對國內採購的重視正在推動航空航太、陸地和海軍平台推進系統、結構和溫度控管系統對經認證的金屬積層製造零件的需求。下一代飛機引擎專案的公佈擴大了列印噴油嘴、襯套和複雜冷卻通道的應用範圍,這些零件受益於高度可重複的粉末床製程和可靠的後處理。任務計劃和平台升級提高了對經認證的設備、粉末和熱處理流程的要求,這使得紮根於航太叢集的經驗豐富的服務供應商和整合商更具優勢。符合 ISO 和 ASTM 標準的標準化指南正在飛機適航性和海軍船隻分類流程中得到應用,隨著測試數據的積累,這些指南有助於關鍵部件的可靠批量生產。這些變化將採購管道與國內認證能力連結起來,正在擴大印度金屬積層製造市場的機會。

政府的「印度製造」和「自力更生印度」舉措

國家藍圖將積層製造定位為一項尖端技術,認為其將對國內生產毛額(GDP)產生顯著的正面影響。路線圖概述了「即插即用」型工業園區和共用基礎設施的建設,旨在降低資本密集金屬印表機的進入門檻。政策措施強調發展國產設備、在地採購材料以及保障熟練勞動力,使中小企業能夠在無需承擔高昂前期成本的情況下使用先進系統。技術發展委員會提供的競爭性津貼正進一步投入資源,推動國產金屬和陶瓷3D列印技術及其底層子系統在整個價值鏈中的商業化。這些措施將採購重點與產業能力建設相結合,加快符合國家標準的零件、機械和材料的認證週期。因此,印度金屬積層製造市場將擁有更多能夠處理受監管應用和時間緊迫項目的認證供應商。

設備和材料成本極高

對於印度的微型、微企業而言,工業級金屬積層製造系統及其耗材的資本投入仍然很高。由於缺乏共用基礎設施和計量收費模式,這些技術的普及應用受到限制。除了鈦粉價格之外,特種合金的關稅也推高了航太級原料的每公斤成本,使其高於其他地區成熟的供應鏈。雖然上游工程提煉鈦鐵礦製成鈦渣的努力正在加強原料供應鏈,但下游的粉碎能力仍需時間才能達到航太級粉末所需的球形度和氧含量標準。國家規劃的共用前沿技術園區可以減輕負擔,但供應商的地理分散意味著本地服務中心對於物流和支援仍然至關重要。這些成本和供應方面的不利因素正在減緩印度金屬積層製造市場在成本敏感型終端用戶領域的短期滲透。

細分市場分析

截至2025年,粉末床熔融(PBF)技術佔總應用量的45.87%。這反映了飛機製造對渦輪機、噴油器和溫度控管部件的合格要求,即亞50微米解析度和可重複性,並通過無損檢測和結構化後處理檢驗。這種精度,結合成熟的工藝控制和熱等向性靜壓(HIP)工藝,符合航太產業的認證流程,該流程強調複雜幾何形狀部件的微觀結構和機械性能的一致性。黏著劑噴塗成型是成長最快的技術,預計到2031年將以15.78%的複合年成長率成長,這得益於其在模具和中等批量零件方面的經濟性,因為燒結和滲透工藝能夠提供汽車和工業領域買家可接受的性能。直接能量沉積技術適用於維修和再製造應用場景,例如葉尖修復和現場/近場零件加固,從而減少引擎和船舶系統的停機時間。由於技術選擇與認證準備情況相關,因此在認證框架內,PBF 目前是飛機硬體的首選,但隨著資料集的成熟,黏著劑噴塗成型正在成本敏感型應用中擴展。

這些實施模式反映了國家研發重點,例如網格結構、保形冷卻以及最佳化建造參數以提高一次通過率並減少返工。這增強了印度金屬積層製造市場的商業機會,此前模具成本的攤銷會阻礙複雜、中小批量生產的實施。在技術選擇方面,粉末床熔融(PBF)技術在印度金屬積層製造市場中的佔有率受益於符合ISO和ASTM標準的適航性和分類指南。同時,黏著劑噴塗成型認證指南在材料系統和燒結重複性方面也在不斷發展。隨著電子束、電弧和混合平台認證數據的積累,多技術工廠將能夠最佳化工藝,以滿足零件的功能和生命週期要求。這些基於認證的選擇正在重塑印度區域叢集中原始設備製造商(OEM)和服務供應商的打入市場策略。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 政府的「印度製造」和「自力更生印度」舉措

- 擴大航太和國防領域的國內生產計劃

- 印度的太空計畫正在擴展。

- 對個體化醫療植入和義肢的需求日益成長

- 汽車產業向電動車的轉型

- 小批量生產和製造複雜零件具有成本優勢。

- 市場限制因素

- 設備和材料成本極高

- 日本供不應求

- 缺乏標準化和品質認證框架

- 傳統製造業缺乏意識

- 價值供應鏈分析

- 監理情勢

- 技術展望

- 產業吸引力—五力分析

- 新進入者的威脅

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 競爭公司之間的競爭

- 印度各產業和城市規模的部署模式

- 以航太和汽車產業為中心的區域叢集

第5章 市場規模與成長預測

- 透過技術

- 粉末床熔融(PBF)

- 黏著劑噴塗成型

- 定向能量沉積(DED)

- 其他金屬積層製造程序

- 材料類型

- 不銹鋼

- 鋁

- 鈦

- 鈷鉻合金

- 鎳合金

- 貴金屬(如黃金、白銀、鉑金)

- 其他(客製化合金、高溫超合金)

- 產業最終用途

- 航太/國防

- 車

- 醫療和牙科護理

- 石油、天然氣和能源

- 工具/工業產品

- 電子和半導體

- 建造

- 珠寶藝術

- 按地區

- 印度北部(德里、哈里亞納邦、北方邦、旁遮普邦)

- 印度西部(馬哈拉斯特拉邦、古吉拉突邦、果阿邦)

- 南印度(卡納塔克邦、泰米爾納德邦、特倫甘納邦、喀拉拉邦)

- 印度東部和東北部

- 印度中部(中央邦、恰蒂斯加爾邦)

第6章 競爭情勢

- 市場集中度

- 策略舉措和夥伴關係

- 市佔率分析

- 公司簡介

- Wipro 3D

- Intech Additive Solutions

- Bharat Fritz Werner(BFW Additive)

- GE Additive(India)

- EOS India

- 3D Systems India

- SLM Solutions

- Phillips Additive/Phillips Machine Tools

- Objectify Technologies

- 3D Incredible

- Imaginarium Rapid

- Truventor.ai(Supercraft3D)

- BASF Forward AM India

- Indo-MIM

- Agnikul Cosmos

- Godrej Aerospace

- Tata Advanced Systems

- Bharat Forge

- L&T Technology Services

- HP Metal Jet(India)

第7章 市場機會與未來展望

According to Mordor Intelligence, the india metal additive manufacturing market size was valued at USD 253.45 million in 2025 and is estimated to grow from USD 290.10 million in 2026 to reach USD 572.46 million by 2031, at a CAGR of 14.56% during the forecast period (2026-2031).

This report is Segmented by Technology (Powder Bed Fusion, Binder Jetting, More), Material Type (Stainless Steel, Aluminum, More), End-Use Industry (Aerospace and Defense, Automotive, Healthcare and Dental, Oil Gas and Energy, Tooling and Industrial Goods, Electronics and Semiconductors, Construction, Jewellery and Art), and Geography. Market Forecasts are Provided in Terms of Value in USD

India Metal Additive Manufacturing Market Trends and Insights

Growing Aerospace and Defense Indigenization Programs

Higher capital outlays and ringfenced domestic procurement are channeling demand for qualified metal AM components in air, land, and naval platforms across propulsion, structural, and thermal systems. Program announcements for next-generation aero engines elevate the role of printed injectors, liners, and complex cooling channels that benefit from repeatable powder-bed processes and robust post-processing. Mission timelines and platform upgrades tighten requirements for certified machines, powders, and heat treatment routes, which favors experienced service bureaus and integrators embedded in aerospace clusters. Standardization guidance aligned with ISO and ASTM practices is being adopted across airworthiness and naval classification pathways, which supports reliable series production of critical parts as test data matures. These shifts expand the opportunity space for the Indian metal additive manufacturing market by linking procurement pipelines to domestic qualification capacity.

Government's Make in India and Atmanirbhar Bharat Initiatives

The national roadmap places additive manufacturing among frontier technologies with significant GDP upside, outlining plug-and-play industrial parks and shared infrastructure that reduce entry barriers for capital-intensive metal printers. Policy measures emphasize indigenous machine development, localized materials, and a trained workforce so small and mid-sized firms can access advanced systems without prohibitive up-front costs. Competitive grants from the Technology Development Board further direct resources toward commercializing domestic metal and ceramics 3D printing technologies and enabler subsystems across the value chain. These interventions link procurement priorities with industrial capability-building, which accelerates qualification cycles for parts, machines, and materials aligned with national standards. The result for the Indian metal additive manufacturing market is a broader funnel of certified suppliers ready to serve regulated applications and time-bound projects.

Extremely High Equipment and Material Costs

Capital outlays for industrial-grade metal AM systems and their consumables remain high for the country's MSME base, which constrains adoption without access to shared infrastructure or pay-per-use models. Titanium powder pricing, combined with duties on specialty alloys, raises per-kilogram costs for aerospace-grade feedstocks relative to mature supply chains in other regions. Upstream moves to beneficiate ilmenite into titanium slag are building raw material resilience, yet downstream atomization capacity will take time to meet aerospace-grade sphericity and oxygen thresholds for powders. National plans for frontier-technology parks with shared equipment can reduce the burden, though the geographic spread of suppliers means localized service bureaus still matter for logistics and support. These cost and availability headwinds temper near-term penetration of the Indian metal additive manufacturing market in cost-sensitive end uses.

Other drivers and restraints analyzed in the detailed report include:

- Cost Advantages for Low-Volume and Complex Part Production

- Automotive Industry's Shift Toward Electric Vehicles

- Limited Availability of Qualified Metal Powders Domestically

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Powder Bed Fusion accounted for 45.87% of the installed base in 2025, reflecting airworthiness needs for sub-50-micron resolution and repeatability in turbine, injector, and thermal management parts validated through non-destructive evaluation and structured post-processing. This precision, combined with mature process controls and hot isostatic pressing routines, aligns with aerospace qualification flows that emphasize consistent microstructures and mechanical properties across complex geometries. Binder Jetting is the fastest-growing technology at a projected 15.78% CAGR to 2031, sustained by economics in tooling and medium-volume parts where sintering and infiltration deliver acceptable properties for automotive and industrial buyers. Directed Energy Deposition supports repair and remanufacture use cases, including blade-tip restoration and on-site or near-site part reinforcement, which shortens downtime for engines and shipboard systems. Technology selection correlates with certification readiness, so qualification frameworks favor PBF for flight hardware today while Binder Jetting expands in cost-sensitive applications as datasets mature.

Adoption patterns also mirror national R&D priorities for lattice structures, conformal cooling, and build-parameter optimization that raise first-time-right rates and cut rework. This strengthens the opportunity in the Indian metal additive manufacturing market, where tooling amortization would otherwise hinder complex, low- to mid-volume runs. Within technology choices, the Indian metal additive manufacturing market share for PBF benefits from airworthiness and classification guidance aligned with ISO and ASTM, while Binder Jetting's qualification playbook continues to evolve on material systems and sintering repeatability. As certification data accumulates for electron-beam variants, wire-arc routes, and hybrid platforms, multi-technology facilities can tailor processes to part function and lifecycle requirements. These certification-driven choices are reshaping go-to-market strategies for both OEMs and service bureaus in India's regional clusters.

List of Companies Covered in this Report:

- Wipro 3D

- Intech Additive Solutions

- Bharat Fritz Werner (BFW Additive)

- GE Additive (India)

- EOS India

- 3D Systems India

- SLM Solutions

- Phillips Additive/Phillips Machine Tools

- Objectify Technologies

- 3D Incredible

- Imaginarium Rapid

- Truventor.ai (Supercraft3D)

- BASF Forward AM India

- Indo-MIM

- Agnikul Cosmos

- Godrej Aerospace

- Tata Advanced Systems

- Bharat Forge

- L&T Technology Services

- HP Metal Jet (India)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government's Make in India and Atmanirbhar Bharat Initiatives

- 4.2.2 Growing Aerospace and Defense Indigenization Programs

- 4.2.3 Expansion of India's Space Program

- 4.2.4 Rising Demand for Customized Medical Implants and Prosthetics

- 4.2.5 Automotive Industry's Shift Toward Electric Vehicles

- 4.2.6 Cost Advantages for Low-Volume and Complex Part Production

- 4.3 Market Restraints

- 4.3.1 Extremely High Equipment and Material Costs

- 4.3.2 Limited Availability of Qualified Metal Powders Domestically

- 4.3.3 Lack of Standardization and Quality Certification Frameworks

- 4.3.4 Insufficient Awareness Among Traditional Manufacturing Sectors

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Industry Attractiveness - Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Tier-Based Adoption Pattern Across Indian Industry

- 4.9 Regional Concentration Around Aerospace and Automotive Clusters

5 Market Size & Growth Forecasts (Value, In USD Billion)

- 5.1 By Technology

- 5.1.1 Powder Bed Fusion (PBF)

- 5.1.2 Binder Jetting

- 5.1.3 Directed Energy Deposition (DED)

- 5.1.4 Other Metal AM Processes

- 5.2 By Material Type

- 5.2.1 Stainless Steel

- 5.2.2 Aluminum

- 5.2.3 Titanium

- 5.2.4 Cobalt Chrome

- 5.2.5 Nickel Alloys

- 5.2.6 Precious Metals (e.g., gold, silver, platinum)

- 5.2.7 Others (custom alloys, high-temp superalloys)

- 5.3 By End-Use Industry

- 5.3.1 Aerospace & Defence

- 5.3.2 Automotive

- 5.3.3 Healthcare & Dental

- 5.3.4 Oil, Gas & Energy

- 5.3.5 Tooling & Industrial Goods

- 5.3.6 Electronics & Semiconductors

- 5.3.7 Construction

- 5.3.8 Jewellery & Art

- 5.4 By Region

- 5.4.1 North India (Delhi, Haryana, UP, Punjab)

- 5.4.2 West India (Maharashtra, Gujarat, Goa)

- 5.4.3 South India (Karnataka, Tamil Nadu, Telangana, Kerala)

- 5.4.4 East & North-East India

- 5.4.5 Central India (MP, Chhattisgarh)

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves & Partnerships

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Wipro 3D

- 6.4.2 Intech Additive Solutions

- 6.4.3 Bharat Fritz Werner (BFW Additive)

- 6.4.4 GE Additive (India)

- 6.4.5 EOS India

- 6.4.6 3D Systems India

- 6.4.7 SLM Solutions

- 6.4.8 Phillips Additive/Phillips Machine Tools

- 6.4.9 Objectify Technologies

- 6.4.10 3D Incredible

- 6.4.11 Imaginarium Rapid

- 6.4.12 Truventor.ai (Supercraft3D)

- 6.4.13 BASF Forward AM India

- 6.4.14 Indo-MIM

- 6.4.15 Agnikul Cosmos

- 6.4.16 Godrej Aerospace

- 6.4.17 Tata Advanced Systems

- 6.4.18 Bharat Forge

- 6.4.19 L&T Technology Services

- 6.4.20 HP Metal Jet (India)

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

金屬粉末積層製造市場機會、成長促進因素、產業趨勢分析及預測(2026-2035年)

金屬粉末積層製造市場機會、成長促進因素、產業趨勢分析及預測(2026-2035年) 積層製造市場預測至2034年-按產品類型、材料、技術、應用、最終用戶和地區分類的全球分析

積層製造市場預測至2034年-按產品類型、材料、技術、應用、最終用戶和地區分類的全球分析 全球金屬粉末積層製造市場:規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球金屬粉末積層製造市場:規模、佔有率、趨勢和成長分析報告(2026-2034年) 2026-2030年全球金屬積層製造市場

2026-2030年全球金屬積層製造市場 金屬黏結劑噴射 (BJT) 3D 列印機市場:依類型(全自動、半自動)、材料(不銹鋼、鈦、鋁、工具鋼、鎳合金)和應用劃分 - 全球預測至 2036 年

金屬黏結劑噴射 (BJT) 3D 列印機市場:依類型(全自動、半自動)、材料(不銹鋼、鈦、鋁、工具鋼、鎳合金)和應用劃分 - 全球預測至 2036 年 日本金屬積層製造市場規模、佔有率、趨勢及預測(按類型、組件、最終用途產業及地區分類),2026-2034年

日本金屬積層製造市場規模、佔有率、趨勢及預測(按類型、組件、最終用途產業及地區分類),2026-2034年 2026年全球金屬積層製造市場報告積層製造粉末市場預測至2032年:按粉末特性、材料類型、技術、最終用戶和地區分類的全球分析

2026年全球金屬積層製造市場報告積層製造粉末市場預測至2032年:按粉末特性、材料類型、技術、最終用戶和地區分類的全球分析 金屬積層製造設備市場規模、佔有率和趨勢分析報告:按技術、最終用途、應用、地區和細分市場預測(2025-2033 年)金屬黏著劑噴塗成型市場規模、佔有率和趨勢分析報告:按最終用途、地區和細分市場預測(2025-2033 年)

金屬積層製造設備市場規模、佔有率和趨勢分析報告:按技術、最終用途、應用、地區和細分市場預測(2025-2033 年)金屬黏著劑噴塗成型市場規模、佔有率和趨勢分析報告:按最終用途、地區和細分市場預測(2025-2033 年)