|

市場調查報告書

商品編碼

2062048

物聯網微控制器:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年)IoT Microcontroller - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

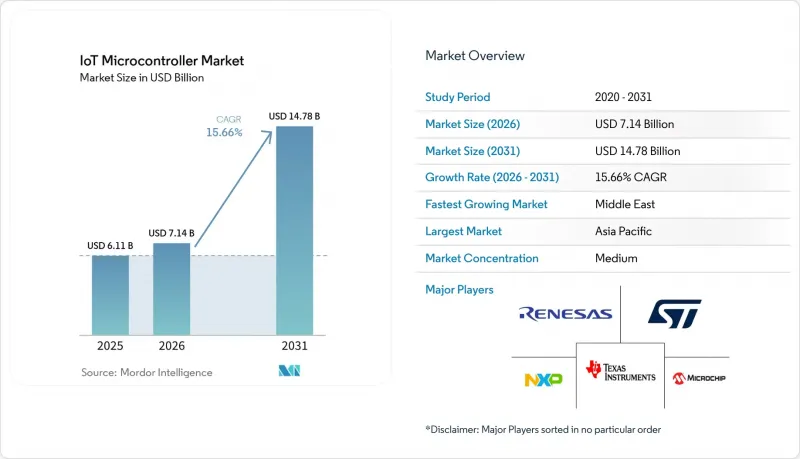

根據 Mordor Intelligence 預測,物聯網微控制器市場規模將從 2025 年的 61.1 億美元成長到 2026 年的 71.4 億美元,到 2031 年達到 147.8 億美元,2026 年至 2031 年的複合年成長率為 15.66%。

本報告按位類型(8 位、16 位及其他)、連接類型(無整合連接、Wi-Fi、藍牙/BLE、Zigbee/Thread 及其他)、指令集架構(ARM、RISC-V、x86 及其他)、應用領域(智慧家庭和穿戴式設備、工業自動化和工業物聯網、汽車和交通運輸及其他)以及地區進行細分。市場預測以美元計價。

全球物聯網微控制器市場趨勢與洞察

互聯工業系統的快速擴張

為了減少意外停機時間,工廠管理者在工廠數位化預算中優先考慮分散式控制和分析。每個機器人單元、輸送機模組和智慧工具都至少包含一個控制器,該控制器結合了感測器融合和確定性網路。預測性維護應用場景需要片上模擬前端,以及充足的振動和熱推斷餘量,且無需雲端延遲。英飛凌將於 2025 年推出的 PSOC Edge E8x 系列晶片正是這一趨勢的體現,它整合了 ARM Cortex-M33 核心和 Ethos-U55 神經網路處理單元,實現了無需雲端延遲的片上異常檢測。此系列新產品整合了硬體信任根 (RoT) 組件,以滿足 IEC 62443 標準的要求,使安全性與材料清單(BOM) 中的訊號完整性同等重要。

邊緣人工智慧設備對「安全設計」MCU的需求日益成長

在延遲不可接受的系統中,例如服務機器人和自主無人機,將推理工作負載從雲端遷移到板載已成為日益成長的趨勢。這種轉變提高了對硬體隔離的要求,以防止模型權重提取、安全啟動和篡改偵測。諸如PSA Certified Level 2之類的認證框架將設計選擇與明確定義的威脅模型相匹配,但這同時也意味著開發週期將延長數月。由於歐盟網路安全法規和類似的美國指令對安全措施不足的連網產品規定了嚴格的責任,品牌方正在接受這一進度壓力。

新ISA中軟體生態系的碎片化

雖然 RISC-V 的開放授權降低了專利費支出,但不受限制的自訂擴充導致了大量缺乏二進位相容性的工具鏈。開發人員通常需要為每種晶片變體維護單獨的程式碼庫,這增加了非重複性工程 (NRE) 預算。整合工作(例如 RVA 配置文件)正在進行中,但合規性是自願的,而且採用情況仍然不均衡。由此產生的不確定性阻礙了汽車和醫療設備設計人員的採用,因為他們必須保證 15 年的軟體支援。

細分市場分析

預計到 2025 年,32 位元微控制器將占到總銷量的 58.39%,凸顯其在運算能力和成本方面的出色平衡。這些量產控制器在智慧閘道器和工廠驅動市場佔據主導地位,可運行即時作業系統以及精簡的機器學習庫。物聯網微控制器市場正持續向整合向量處理單元和片上安全模組的產品轉型,在不影響加密吞吐量的前提下實現確定性控制。將於 2024 年發布的 Raspberry Pi RP2350 採用雙核心配置,可執行 ARM Cortex-M33 或 RISC-V Hazard3 指令,為開發人員提供架構柔軟性,並可實現從 32 位元工作負載到 64 位元工作負載的遷移。

由於高解析度成像和多感測器融合需要更寬的位址空間,對 64 位元控制器的需求正以 16.46% 的複合年成長率成長。機器人模組和高級駕駛輔助系統 (ADAS) 闆卡已使用超過 4GB 的內存,儘管工作電流有所增加,工程師仍被迫採用更寬的數據通路。隨著編譯器支援的成熟,向 64 位元指令集的過渡將從高階設計擴展到主流邊緣分析領域。

預計到2025年,Wi-Fi 設備出貨量將維持37.73%的佔有率。這是因為大多數閘道器都安裝在現有網路基地台覆蓋範圍內的建築物內。智慧家庭中心、零售手持終端機和小型工業終端都受益於Wi-Fi基礎設施的頻寬和廣泛應用。現今,模組支援節能模式,可將平均電流消耗控制在25µA以下,從而延長電池壽命,並使Wi-Fi突破以往藍牙在行動裝置上的限制。

隨著計量表製造商、物流運營商和農業平台尋求在無需自建回程傳輸的情況下實現廣域覆蓋,蜂窩NB-IoT和LTE-M模組正以16.86%的複合年成長率快速成長。 eSIM和全球漫遊協議的興起簡化了庫存管理,使單一零件號碼可涵蓋多個監管區域。在預測期內,預裝認證調變解調器韌體和資料方案管理功能的供應商將在物聯網微控制器市場中佔據優勢,從而縮短車隊營運商的引進週期。

區域分析

到2025年,亞太地區將佔全球銷售額的38.14%。這得歸功於中國深厚的契約製造、日本的精密機器人技術基礎以及印度旨在降低進口依賴的財政激勵措施。中國國內雲端服務供應商擴大推薦使用RISC-V組件來建立邊緣節點,這不僅強化了本地供應鏈,也降低了支付專利費的風險。印度在其生產激勵計畫下投入了1555.4兆印度盧比(約16.48億美元),該計畫已吸引了多家快速測試和整合晶片的企業,從而縮短了從晶圓到成品模組的前置作業時間。

北美受益於汽車電子產品的強勁需求和工業自動化基礎設施的持續升級。 《晶片與科學法案》為物聯網微控制器市場成熟節點提供了數十億美元的津貼,但預計新的晶圓廠要到2020年代末期才能穩定運作。在此期間,原始設備製造商 (OEM) 依靠多元化採購策略和已通過核准的替代品來應對因供應不足造成的供應衝擊。在歐洲,能源價格上漲推高了晶圓製造成本,但該地區對於安全性至關重要的控制器設計仍然至關重要。歐洲供應商的影響力遠超過其出貨量佔有率,因為德國和法國的一級供應商正在推動嚴格的 ISO 26262 認證,這最終將成為全球最佳實踐。

中東地區雖然目前規模較小,但以16.53%的複合年成長率快速擴張,成長率超過其他地區。這主要得益於大型智慧城市專案需要能夠承受沙漠高溫和沙塵侵蝕的感測器網路。南美洲和非洲仍蘊藏著巨大的發展機會。精準灌溉和太陽能微電網監測試驗計畫對遠端蜂窩控制器的需求日益成長,以彌補基礎設施的不足。隨著資料通訊計畫和衛星回程傳輸成本的下降,這些地區將從概念驗證(PoC)階段過渡到大規模部署,從而推動成本績效32位元元件的長期需求。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 互聯工業系統的快速擴張

- 邊緣人工智慧設備對「安全設計」MCU的需求日益成長

- 多重通訊協定無線MCU在智慧家庭生態系統中的普及

- 政府主導的促進國內半導體生產的措施

- 透過採用開放原始碼RISC-V 降低許可成本。

- 將人工智慧加速器整合到 32 位元 MCU 中的工作正在穩步推進。

- 市場限制因素

- 新ISA中軟體生態系的碎片化

- 半導體供應鏈的波動仍在持續。

- 物聯網OEM公司網路安全合規成本不斷增加

- 性能與功耗之間的權衡限制了電池續航時間的提升。

- 宏觀經濟因素對市場的影響

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 位元類

- 8-bit

- 16 位元

- 32 位元

- 64 位元

- 按連線類型

- 無整合連接

- Wi-Fi

- Bluetooth/BLE

- Zigbee/Thread

- 蜂窩NB-IoT/LTE-M

- 多重通訊協定SoC

- 依指令集架構

- ARM

- RISC-V

- x86

- 專有規範/其他指令集架構

- 透過使用

- 智慧家庭和穿戴式裝置

- 工業自動化和工業物聯網

- 汽車和運輸業

- 醫療保健和醫療設備

- 智慧城市基礎設施

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 其他亞太國家

- 中東和非洲

- 中東

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 其他中東國家

- 非洲

- 南非

- 埃及

- 其他非洲國家

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- STMicroelectronics NV

- NXP Semiconductors NV

- Texas Instruments Incorporated

- Microchip Technology Inc.

- Renesas Electronics Corporation

- Infineon Technologies AG

- Silicon Laboratories Inc.

- Nordic Semiconductor ASA

- GigaDevice Semiconductor Inc.

- Espressif Systems(Shanghai)Co., Ltd.

- Holtek Semiconductor Inc.

- Analog Devices, Inc.

- Maxim Integrated Products, Inc.

- Toshiba Electronic Devices and Storage Corporation

- Nuvoton Technology Corporation

- Qualcomm Incorporated

- Intel Corporation

- Advanced Micro Devices, Inc.

- Samsung Electronics Co., Ltd.

- ROHM Co., Ltd.

- Espressif Systems(Shanghai)Co., Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the ioT microcontroller market size is expected to increase from USD 6.11 billion in 2025 to USD 7.14 billion in 2026 and reach USD 14.78 billion by 2031, growing at a CAGR of 15.66% over 2026-2031.

This report is Segmented by Bit Class (8-Bit, 16-Bit, and More), Connectivity Type (No Integrated Connectivity, Wi-Fi, Bluetooth/BLE, Zigbee/Thread, and More), Instruction Set Architecture (ARM, RISC-V, X86, and More), Application (Smart Home and Wearables, Industrial Automation and IIoT, Automotive and Transportation, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global IoT Microcontroller Market Trends and Insights

Rapid Expansion of Connected Industrial Systems

Factory digitization budgets now prioritize distributed control and analytics as plant managers seek to cut unplanned downtime. Every robot cell, conveyor module, and smart tool embeds at least one controller that must combine sensor fusion with deterministic networking. Predictive-maintenance use cases demand on-chip analog front ends plus enough headroom to run vibration and thermal inference without cloud latency. Infineon's PSOC Edge E8x family, launched in 2025, exemplifies this trend by embedding an ARM Cortex-M33 core alongside an Ethos-U55 neural processing unit, enabling on-chip anomaly detection without cloud latency. New product families embed hardware root-of-trust components to meet IEC 62443 mandates, meaning security now rides alongside signal integrity in the bill of materials.

Growing Demand for Secure-by-Design MCUs in Edge AI Devices

Latency-intolerant systems, such as service robots and autonomous drones, are moving inference workloads from the cloud to the board. This change increases the requirements for hardware isolation, secure boot, and tamper detection to prevent the extraction of model weights. Certification frameworks like PSA Certified Level 2 map design choices to clearly defined threat models, but they also extend development schedules by several months. Brands accept the timeline penalty because the EU Cyber Resilience Act and similar U.S. directives impose strict liability for insecure connected products.

Software Ecosystem Fragmentation for New ISAs

RISC-V's open license lowers royalty outlays, but unrestricted custom extensions have created a patchwork of toolchains that lack binary compatibility. Developers often maintain separate code bases for each silicon variant, which inflates non-recurring engineering budgets. Consolidation efforts such as the RVA profiles are underway, yet adherence is optional, and uptake remains uneven. The resulting uncertainty deters automotive and medical designers who must guarantee 15-year software support.

Other drivers and restraints analyzed in the detailed report include:

- Proliferation of Multi-Protocol Wireless MCUs for Smart-Home Ecosystems

- Government-Led Semiconductor Localization Incentives

- Persistent Semiconductor Supply-Chain Volatility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The 32-bit class delivered 58.39% of revenue in 2025, underscoring its balance between compute ceiling and cost. High-volume controllers in this tier dominate smart gateways and factory drives because they run real-time operating systems alongside compact machine-learning libraries. The IoT microcontroller market continues to pivot toward variants with vector math units and on-chip security blocks, enabling deterministic control without compromising encryption throughput. Raspberry Pi's RP2350, launched in 2024, offers a dual-core configuration that can run either ARM Cortex-M33 or RISC-V Hazard3 instructions, providing developers with architectural flexibility and a migration path from 32-bit to 64-bit workloads.

Demand for 64-bit controllers is climbing at a 16.46% CAGR as high-definition imaging and multi-sensor fusion need wider address spaces. Robotics modules and advanced driver-assistance boards already exceed 4 GB of memory, compelling engineers to adopt wider data paths despite higher active current. As compiler support matures, the jump to 64-bit instruction sets will spread beyond premium designs into mainstream edge analytics.

Wi-Fi maintained a 37.73% shipment share in 2025 because most gateways are located inside buildings with existing access-point coverage. Smart-home hubs, retail handhelds, and small industrial terminals benefit from the bandwidth headroom and ubiquity of Wi-Fi infrastructure. Modules now support power-saving modes that lower average draw to below 25 µA, extending battery life and nudging Wi-Fi into portable devices once locked to Bluetooth.

Cellular NB-IoT and LTE-M modules are expanding at a 16.86% CAGR as meter companies, logistics providers, and agricultural platforms pursue wide-area reach without owning a private backhaul. The rise of eSIM and global roaming profiles means a single part number can address many regulatory domains, simplifying inventory. Over the forecast horizon, the IoT microcontroller market will reward suppliers that preload certified modem firmware and data-plan management hooks, shortening deployment cycles for fleet operators.

Geography Analysis

Asia-Pacific captured 38.14% of global revenue in 2025, anchored by China's contract-manufacturing depth, Japan's precision robotics base, and India's fiscal incentives that reduce import reliance. Domestic cloud providers in China increasingly recommend RISC-V parts for edge nodes, reinforcing local supply chains and lowering royalty exit risk. India's disbursement of INR 15,554 crore (approximately USD 1,648 million) under its production incentive plan has already attracted several bump-and-test houses that shorten the time from wafer to finished module.

North America benefits from strong automotive electronics demand and continuing upgrades to industrial automation infrastructure. The CHIPS and Science Act funnels multi-billion-dollar grants to mature nodes serving the IoT microcontroller market, but new fabs will not reach steady state until the back half of the decade. In the interim, original-equipment manufacturers rely on multi-sourcing strategies and approved alternates to manage allocation shocks. Europe faces higher energy prices that raise wafer fabrication overhead, yet the region remains essential for safety-critical controller design. German and French tier-ones drive stringent ISO 26262 documentation that eventually becomes global best practice, giving European suppliers influence that exceeds their shipment share.

The Middle East, though smaller today, is scaling faster than any peer region at 16.53% CAGR because flagship smart-city programs require sensor networks that survive desert heat and sand ingress. South America and Africa remain emerging opportunities. Pilot programs in precision irrigation and solar-microgrid monitoring highlight long-range cellular controllers that bridge infrastructure gaps. As data plans and satellite-backhaul tariffs decline, these regions will shift from proof of concept to scaled deployments, lifting long-tail unit volumes for value-optimized 32-bit parts.

- STMicroelectronics N.V.

- NXP Semiconductors N.V.

- Texas Instruments Incorporated

- Microchip Technology Inc.

- Renesas Electronics Corporation

- Infineon Technologies AG

- Silicon Laboratories Inc.

- Nordic Semiconductor ASA

- GigaDevice Semiconductor Inc.

- Espressif Systems (Shanghai) Co., Ltd.

- Holtek Semiconductor Inc.

- Analog Devices, Inc.

- Maxim Integrated Products, Inc.

- Toshiba Electronic Devices and Storage Corporation

- Nuvoton Technology Corporation

- Qualcomm Incorporated

- Intel Corporation

- Advanced Micro Devices, Inc.

- Samsung Electronics Co., Ltd.

- ROHM Co., Ltd.

- Espressif Systems (Shanghai) Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Expansion of Connected Industrial Systems

- 4.2.2 Growing Demand for Secure-by-Design MCUs in Edge AI Devices

- 4.2.3 Proliferation of Multi-protocol Wireless MCUs for Smart Home Ecosystems

- 4.2.4 Government-Led Semiconductor Localization Incentives

- 4.2.5 Open-Source RISC-V Adoption Reducing Licensing Costs

- 4.2.6 Increasing Integration of AI Accelerators Inside 32-bit MCUs

- 4.3 Market Restraints

- 4.3.1 Software Ecosystem Fragmentation for New ISAs

- 4.3.2 Persistent Semiconductor Supply-Chain Volatility

- 4.3.3 Rising Cyber-Security Compliance Costs for IoT OEMs

- 4.3.4 Performance-Power Trade-offs Limiting Battery Life Gains

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Bit Class

- 5.1.1 8-bit

- 5.1.2 16-bit

- 5.1.3 32-bit

- 5.1.4 64-bit

- 5.2 By Connectivity Type

- 5.2.1 No Integrated Connectivity

- 5.2.2 Wi-Fi

- 5.2.3 Bluetooth / BLE

- 5.2.4 Zigbee / Thread

- 5.2.5 Cellular NB-IoT / LTE-M

- 5.2.6 Multi-protocol SoC

- 5.3 By Instruction Set Architecture

- 5.3.1 ARM

- 5.3.2 RISC-V

- 5.3.3 x86

- 5.3.4 Proprietary / Other Instruction Set Architectures

- 5.4 By Application

- 5.4.1 Smart Home and Wearables

- 5.4.2 Industrial Automation and IIoT

- 5.4.3 Automotive and Transportation

- 5.4.4 Healthcare and Medical Devices

- 5.4.5 Smart City Infrastructure

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 United Arab Emirates

- 5.5.5.1.2 Saudi Arabia

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Egypt

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 STMicroelectronics N.V.

- 6.4.2 NXP Semiconductors N.V.

- 6.4.3 Texas Instruments Incorporated

- 6.4.4 Microchip Technology Inc.

- 6.4.5 Renesas Electronics Corporation

- 6.4.6 Infineon Technologies AG

- 6.4.7 Silicon Laboratories Inc.

- 6.4.8 Nordic Semiconductor ASA

- 6.4.9 GigaDevice Semiconductor Inc.

- 6.4.10 Espressif Systems (Shanghai) Co., Ltd.

- 6.4.11 Holtek Semiconductor Inc.

- 6.4.12 Analog Devices, Inc.

- 6.4.13 Maxim Integrated Products, Inc.

- 6.4.14 Toshiba Electronic Devices and Storage Corporation

- 6.4.15 Nuvoton Technology Corporation

- 6.4.16 Qualcomm Incorporated

- 6.4.17 Intel Corporation

- 6.4.18 Advanced Micro Devices, Inc.

- 6.4.19 Samsung Electronics Co., Ltd.

- 6.4.20 ROHM Co., Ltd.

- 6.4.21 Espressif Systems (Shanghai) Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

物聯網微控制器市場-2026-2032年全球市場預測

物聯網微控制器市場-2026-2032年全球市場預測 微控制器 (MCU) 市場預測至 2034 年—按產品類型、架構、記憶體類型、分銷管道、應用、最終用戶和地區分類的全球分析

微控制器 (MCU) 市場預測至 2034 年—按產品類型、架構、記憶體類型、分銷管道、應用、最終用戶和地區分類的全球分析 2026-2030年全球微控制器(MCU)市場

2026-2030年全球微控制器(MCU)市場 2026年全球金屬氧化物半導體(MOS)微控制器(MCU)市場報告

2026年全球金屬氧化物半導體(MOS)微控制器(MCU)市場報告 航太微控制器市場:市場機會、成長促進因素、產業趨勢分析及未來預測(2026-2035)物聯網微控制器市場預測至2034年:按組件、位元深度、記憶體、應用和地區分類的全球分析

航太微控制器市場:市場機會、成長促進因素、產業趨勢分析及未來預測(2026-2035)物聯網微控制器市場預測至2034年:按組件、位元深度、記憶體、應用和地區分類的全球分析 物聯網微控制器市場報告:按產品、應用和地區分類(2026-2034 年)

物聯網微控制器市場報告:按產品、應用和地區分類(2026-2034 年) 物聯網微控制器市場:按產品類型、應用和地區分類

物聯網微控制器市場:按產品類型、應用和地區分類 物聯網微控制器市場 - 全球產業規模、佔有率、趨勢、機會及預測(按產品、應用、最終用戶、地區和競爭格局分類),2021-2031年物聯網MCU解決方案市場:按處理器類型、供電模式、記憶體容量、工作電壓、通訊協定、應用和最終用戶分類,全球預測,2026-2032年

物聯網微控制器市場 - 全球產業規模、佔有率、趨勢、機會及預測(按產品、應用、最終用戶、地區和競爭格局分類),2021-2031年物聯網MCU解決方案市場:按處理器類型、供電模式、記憶體容量、工作電壓、通訊協定、應用和最終用戶分類,全球預測,2026-2032年