|

市場調查報告書

商品編碼

2062043

藍牙智慧和智慧就緒:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)Bluetooth Smart And Smart Ready - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

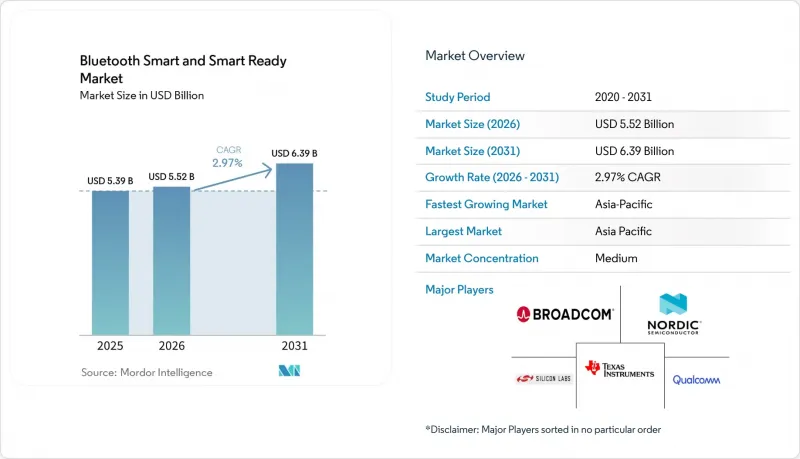

根據 Mordor Intelligence 預測,藍牙智慧和智慧就緒市場將從 2025 年的 53.9 億美元成長到 2026 年的 55.2 億美元,到 2031 年將達到 63.9 億美元,2026 年至 2031 年的複合年成長率為 2.97%。

本報告按產品類型(藍牙智慧型裝置、支援藍牙智慧的裝置)、技術(低功耗藍牙、經典藍牙、藍牙Mesh、藍牙5.0及其他)、應用領域(醫療保健、穿戴式裝置、智慧家庭及其他)、終端用戶產業(消費性電子及其他)和地區進行細分。市場預測以美元計價。

全球藍牙智慧與智慧就緒市場趨勢及洞察

物聯網節點部署數量增加

預計到2025年,藍牙設備的出貨量將達到53億台,到2029年將接近80億台,凸顯了藍牙智慧和智慧就緒市場的巨大規模。目前,支援網狀網路的低功耗藍牙感測器已被應用於工業、農業和建築自動化專案中,用於測量溫度、濕度和人員佔用情況,從而避免使用專用閘道器,並將組件成本降低近30%。在邊緣架構中,該協定備受青睞,因為任何智慧型手機都可以作為現場編程器,從而加快部署和維護速度。這一趨勢直接推動了紐扣電池供電感測器的出貨量,預計到2025年,其出貨量將年增22%。未來十年,隨著低於1微安培的工作電流成為現實,預計這一應用浪潮將進一步加劇,並在對電力消耗敏感的終端設備領域進一步拉大與Zigbee和Z-Wave的差距。

智慧型手機OEM廠商採用LE音訊規範

2025年1月,三星在其Galaxy S25系列中加入了原生低功耗音訊(LE Audio)支持,使用戶能夠透過Auracast廣播功能,將登機口廣播和音樂串流傳輸到相容的耳機和助聽器(samsung.com)。隨後,Google強制要求在Android 16(預覽版於2026年2月發布)中整合LE Audio API,確保未來的裝置能夠提供多串流音訊和低延遲廣播功能。 Auracast發送器已在公共場所運作,例如,2025年3月,芝加哥奧黑爾機場的120個信標投入使用,可將特定位置的音訊直接傳輸到乘客的裝置。這項升級週期要求智慧型手機廠商在過渡期內同時支援經典音訊和LE Audio,這將使檢驗矩陣翻倍,並增加對雙模系統晶片(SoC)的需求。隨著部署基礎轉向LE Audio,單模設計預計將加速發展,進一步推動藍牙智慧(Bluetooth Smart)和智慧就緒(Smart Ready)市場規模的成長。

藍牙經典協定堆疊安全漏洞

美國國家漏洞資料庫 (NVD) 記錄了 2025-2026 年間與 Classic 協定堆疊相關的 17 個嚴重性CVE 漏洞。這些漏洞包括針對 Zephyr、Linux 和 Airoha 晶片的攻擊。這導致 230 萬台設備被召回,降級攻擊仍在智慧家庭門鎖和監護儀中持續發生。儘管許多 OEM 廠商正在向採用安全 AES-128 加密的低功耗藍牙 (BLE) 遷移,但仍有約 32 億台僅支援 Classic 協定堆疊的裝置仍在運作,這為攻擊留下了可乘之機。這種風險會削弱用戶信心,並在部署基礎更新之前阻礙藍牙智慧 (Bluetooth Smart) 和智慧就緒 (Smart Ready) 市場的短期成長。

細分市場分析

預計到2025年,藍牙智慧型裝置將佔藍牙智慧及智慧就緒市場總收入的61.32%,而這一主導地位預計將以3.37%的複合年成長率進一步擴大。它們的優點在於超低功耗,使得血糖值儀、資產標籤和健身追蹤器等設備僅需一枚紐帶電池即可運作數年。預計到2031年,藍牙智慧及智慧就緒市場中智慧型裝置的出貨量成長將佔據市場的大部分佔有率。

雙模智慧就緒設備在汽車資訊娛樂系統和工業閘道器領域仍然至關重要,但它們面臨著結構性挑戰。經典協定堆疊的工作電流約為 30mA,而低功耗藍牙 (Bluetooth Low Energy) 的工作電流低於 5mA;這種差異正促使硬體設計人員轉向單模晶片。組件供應商也正在響應這一轉變,例如 Nordic 的 22nm 製程 nRF54L 透過將 Cortex-M33 處理器與 RISC-V 協處理器結合,將接收電流降低到 3µA 以下。同時,Silicon Labs 的 BG29 將 1MB 快閃記憶體封裝在 2.0mm x 2.5mm 的封裝中,用於助聽器。因此,智慧就緒設備的市場佔有率正在萎縮,但在對向下相容性要求較高的細分市場(例如高階智慧型手機和筆記型電腦),預計其出貨量仍將保持強勁。

預計到2025年,低功耗藍牙(Bluetooth Low Energy)的出貨量將佔46.36%,但藍牙5.1的複合年成長率(CAGR)最高,達到3.97%,主要得益於零售、倉儲和醫院資產管理領域對到達角落(AoA)功能的需求。基於藍牙5.1標籤的智慧藍牙(Bluetooth Smart)和智慧就緒藍牙(Smart Ready)市場規模龐大,憑藉其亞米級的精度優勢,在對成本敏感的場景中有望取代價格更高的超寬頻(UWB)技術。傳統藍牙(Legacy Classic)憑藉其在汽車領域的免持應用,維持了28%的市場佔有率,但隨著低功耗音訊(LE Audio)技術的普及,其成長率放緩至1.2%。

藍牙Mesh的市佔率達到了12%,尤其是在商業照明領域,其市佔率的提升得益於整合Matter韌體。隨著支援週期性廣播和通道探測的新型晶片組的出現(這些功能已在藍牙5.4和6.0中引入),藍牙5.0的重要性有所下降。德州儀器、恩智浦半導體和Silicon Labs都將在2025年1月至2026年4月期間發布支援藍牙6.0的半導體產品,預示著藍牙智慧和智慧就緒市場將迎來快速的轉型,並保持強勁的發展勢頭。

區域分析

亞太地區正引領藍牙智慧和智慧就緒市場的發展,預計到2025年將佔全球銷售額的38.83%,複合年成長率(CAGR)為3.83%。中國已強制要求自2025年1月起銷售的所有智慧家庭設備必須配備低功耗藍牙(BLE),這將刺激美的、海爾等原始設備製造商(OEM)採用該技術。日本主要電子製造商正在將低功耗音訊(LE Audio)技術應用於其2025年的電視機型中,而韓國Galaxy S25系列在2026年第一季售出了4,200萬部。印度於2026年3月公佈的藍牙醫療設備標準提案將簡化核准流程,並擴大連網血糖值監測儀的潛在市場。

北美市場佔28%的佔有率,複合年成長率為2.9%。美國食品藥物管理局(FDA)更嚴格的網路安全指南增加了合規相關支出,但也為醫療覆蓋的遠端患者監護鋪平了道路。儘管美國半導體政策已在國內晶圓廠投資527億美元,但40奈米以下的製程產能要到2028年才能投入運作,這意味著在可預見的未來,大多數藍牙SoC仍將依賴台灣和韓國。加拿大已將其電力限制與美國聯邦通訊委員會(FCC)的規定保持一致,而墨西哥計劃到2025年將有180萬輛汽車配備藍牙數位鑰匙。

歐洲在2025年底的銷售額成長了24%,複合年成長率(CAGR)為2.7%。 2025年8月生效的《無線電設備指令》中的網路安全條款,現已適用於該地區銷售的所有藍牙無線設備,涵蓋從醫療感測器到智慧家庭中心等各類產品。一家德國汽車製造商採用了藍牙6.0頻道探測技術來防止繼電器攻擊,英國國家醫療服務體系(NHS)部署了藍牙連接的監測設備,用於檢測12萬名慢性疾病患者。南美洲和中東及非洲合計佔總合佔有率的10%,複合年成長率為2.4%。巴西國家電信暨電信管理局(Anatel)於2025年4月將其認證標準與ETSI EN 300 328標準接軌。

其他好處

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 物聯網節點部署數量增加

- 智慧型手機OEM廠商採用LE音訊規範

- 推動對連線健診設備的監管

- 對基於位置的零售分析的需求日益成長

- 整合藍牙Mesh與Matter標準

- 無晶圓廠廠商超低功耗SoC藍圖

- 市場限制因素

- 藍牙經典協定堆疊中的安全漏洞

- 40nm 以下節點的晶片級供應受限

- 高密度射頻環境中的協定間干擾

- OEM韌體更新生態系統的細分

- 宏觀經濟因素對市場的影響

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 依產品類型

- 藍牙智慧型裝置

- 支援藍牙智慧的設備

- 按機器人類型

- 工業機器人

- 協作機器人

- 商用服務機器人

- 家用服務機器人

- 人形機器人

- 透過技術

- Bluetooth Low Energy

- Bluetooth Classic

- Bluetooth Mesh

- Bluetooth 5.0

- Bluetooth 5.1

- 透過使用

- 衛生保健

- 穿戴式裝置

- 智慧家庭

- 車

- 工業自動化

- 按最終用戶行業分類

- 家用電器

- 衛生保健

- 車

- 產業

- 零售

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 其他亞太國家

- 中東和非洲

- 中東

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 其他中東國家

- 非洲

- 南非

- 埃及

- 其他非洲地區

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Qualcomm Inc.

- Nordic Semiconductor ASA

- Texas Instruments Incorporated

- Broadcom Inc.

- Silicon Laboratories Inc.

- NXP Semiconductors NV

- STMicroelectronics NV

- Infineon Technologies AG

- Renesas Electronics Corporation

- Microchip Technology Inc.

- Cypress Semiconductor Corporation

- Realtek Semiconductor Corp.

- Murata Manufacturing Co. Ltd.

- Atmosic Technologies Inc.

- Dialog Semiconductor plc

- Espressif Systems(Shanghai)Co. Ltd.

- MediaTek Inc.

- Toshiba Electronic Devices & Storage Corp.

- Panasonic Holdings Corp.

- ON Semiconductor Corp.

第7章 市場機會與未來展望

According to Mordor Intelligence, the bluetooth smart and Smart Ready market size is expected to grow from USD 5.39 billion in 2025 to USD 5.52 billion in 2026 and is forecast to reach USD 6.39 billion by 2031 at a 2.97% CAGR over 2026-2031.

This report is Segmented by Product Type (Bluetooth Smart Devices, and Bluetooth Smart Ready Devices), Technology (Bluetooth Low Energy, Bluetooth Classic, Bluetooth Mesh, Bluetooth 5. 0, and More), Application (Healthcare, Wearable Devices, Smart Home, and More), End-User Industry (Consumer Electronics, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Bluetooth Smart And Smart Ready Market Trends and Insights

Growing Installed Base of IoT Nodes

Shipments of Bluetooth-enabled devices climbed to 5.3 billion units in 2025, and forecasts approach 8 billion by 2029, underscoring the scale that is fueling the Bluetooth Smart and Smart Ready market. Industrial, agricultural, and building-automation projects now specify mesh-enabled Bluetooth Low Energy sensors for temperature, humidity, and occupancy, avoiding proprietary gateways and trimming bill-of-materials cost by nearly 30%. Edge architectures favor the protocol because every smartphone can act as a field programmer, accelerating commissioning and maintenance. The trend directly lifts coin-cell sensor volumes, which grew 22% year over year in 2025. The adoption wave strengthens over the next decade as sub-1-microampere active currents arrive, widening the gap with Zigbee and Z-Wave in power-sensitive endpoints.

Smartphone OEM Adoption of LE Audio Specification

Samsung built native LE Audio support into its Galaxy S25 series in January 2025, enabling Auracast broadcasts that stream gate announcements and music to any compatible earbud or hearing aid (samsung.com). Google followed by embedding mandatory LE Audio APIs in Android 16, previewed in February 2026, ensuring that future handsets expose multi-stream audio and low-latency broadcast functions. Public venues are already installing Auracast transmitters; 120 beacons went live at Chicago's O'Hare airport in March 2025, to pipe localized audio directly to passengers' devices. The upgrade cycle obliges smartphone vendors to support both Classic and LE Audio during transition, doubling validation matrices and driving demand for dual-mode system-on-chips. As the installed base flips toward LE Audio, single-mode designs will accelerate, reinforcing volume growth for the Bluetooth Smart and Smart Ready market.

Security Vulnerabilities in Bluetooth Classic Stack

The National Vulnerability Database logged 17 high-severity CVEs tied to the Classic stack in 2025-2026, including exploits in Zephyr, Linux, and Airoha silicon. Associated recalls spanned 2.3 million vehicles, and downgrade attacks persisted in smart-home locks and medical monitors. Although many OEMs are migrating to Bluetooth Low Energy with AES-128 secure connections, roughly 3.2 billion Classic-only devices remain in service, keeping exploit windows open. The risk erodes confidence and clips near-term expansion for the Bluetooth Smart and Smart Ready market until the installed base is refreshed.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory Push for Connected-Healthcare Devices

- Rising Demand for Location-Based Retail Analytics

- Chip-Level Supply Constraints for Sub-40 nm Nodes

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Bluetooth Smart Devices accounted for 61.32% of 2025 revenue within the Bluetooth Smart and Smart Ready market, a dominance expected to widen under a 3.37% CAGR. Their appeal stems from ultra-low-power profiles that let glucose monitors, asset tags, and fitness trackers operate for years on coin-cell batteries. The Bluetooth Smart and Smart Ready market size for Smart Devices is projected to capture the lion's share of incremental shipments through 2031 as smartphone operating systems phase out Classic profiles.

Dual-mode Smart Ready Devices, while still vital for automotive infotainment and industrial gateways, face structural headwinds. Classic stacks draw roughly 30 mA of active current compared with sub-5 mA for Bluetooth Low Energy, a disparity that pushes hardware designers toward single-mode silicon. Component suppliers signal the shift, Nordic's 22-nanometer nRF54L pairs a Cortex-M33 with a RISC-V coprocessor to cut receive currents below 3 µA, while Silicon Labs' BG29 squeezes 1 MB of Flash into a 2.0 mm X 2.5 mm package for hearing aids. As a result, Smart Ready share recedes, but premium smartphones and laptops will preserve niche volumes where backward compatibility is mandatory.

Bluetooth Low Energy held 46.36% of shipments in 2025, yet Bluetooth 5.1 clocked the fastest CAGR at 3.97% on the strength of angle-of-arrival ranging for retail, warehousing, and hospital asset management. The Bluetooth Smart and Smart Ready market size tied to Bluetooth 5.1 tags benefits from sub-meter accuracy, enabling it to replace costly ultra-wideband in cost-sensitive scenarios. Legacy Classic retained 28% share, buoyed by automotive hands-free profiles, but growth slowed to 1.2% as LE Audio takes hold.

Bluetooth Mesh reached 12% share and improved under converged Matter firmware, especially in commercial lighting. Bluetooth 5.0 slipped in relevance as new chipsets embrace periodic advertising and channel sounding introduced in Bluetooth 5.4 and 6.0. Texas Instruments, NXP, and Silicon Labs all rolled out 6.0-ready silicon between January 2025 and April 2026, signaling a steep migration curve that keeps the Bluetooth Smart and Smart Ready market momentum intact.

Geography Analysis

Asia-Pacific led the Bluetooth Smart and Smart Ready market, accounting for 38.83% of revenue in 2025 and a 3.83% CAGR outlook. China mandated Bluetooth Low Energy in all smart-home appliances sold after January 2025, driving adoption across OEMs such as Midea and Haier. Japanese electronics giants embedded LE Audio in 2025 model-year televisions, while South Korea's Galaxy S25 family moved 42 million units in Q1 2026. India's draft standards for Bluetooth medical devices, released in March 2026, will streamline approvals and widen the addressable base for connected glucose monitors.

North America secured 28% share and a 2.9% CAGR. The FDA's stricter cybersecurity guidance lifted compliance spend but also cleared the path for reimbursable remote patient monitoring. U.S. semiconductor policy channels USD 52.7 billion into domestic fabs, yet sub-40-nanometer capacity will not come online until 2028, keeping most Bluetooth SOCs tied to Taiwan and South Korea in the interim. Canada harmonized power limits with FCC rules, and Mexico's vehicle production line fitted 1.8 million cars with Bluetooth digital keys in 2025.

Europe finished 2025 with 24% revenue and a 2.7% CAGR. The Radio Equipment Directive's August 2025 cyber clause now applies to every Bluetooth radio sold in the bloc, from medical sensors to smart-home hubs. German automakers adopted Bluetooth 6.0 channel sounding to guard against relay attacks, and the NHS piloted Bluetooth-connected monitors for 120,000 chronic-care patients. South America, the Middle East, and Africa combined for 10% share and a 2.4% CAGR, with Brazil's Anatel harmonizing certification to ETSI EN 300 328 in April 2025.

- Qualcomm Inc.

- Nordic Semiconductor ASA

- Texas Instruments Incorporated

- Broadcom Inc.

- Silicon Laboratories Inc.

- NXP Semiconductors N.V.

- STMicroelectronics N.V.

- Infineon Technologies AG

- Renesas Electronics Corporation

- Microchip Technology Inc.

- Cypress Semiconductor Corporation

- Realtek Semiconductor Corp.

- Murata Manufacturing Co. Ltd.

- Atmosic Technologies Inc.

- Dialog Semiconductor plc

- Espressif Systems (Shanghai) Co. Ltd.

- MediaTek Inc.

- Toshiba Electronic Devices & Storage Corp.

- Panasonic Holdings Corp.

- ON Semiconductor Corp.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Installed Base of IoT Nodes

- 4.2.2 Smartphone OEM Adoption of LE Audio Specification

- 4.2.3 Regulatory Push for Connected-Healthcare Devices

- 4.2.4 Rising Demand for Location-Based Retail Analytics

- 4.2.5 Convergence of Bluetooth Mesh With Matter Standard

- 4.2.6 Ultra-Low-Power SoC Road-maps From Fabless Vendors

- 4.3 Market Restraints

- 4.3.1 Security Vulnerabilities in Bluetooth Classic Stack

- 4.3.2 Chip-Level Supply Constraints for Sub-40 nm Nodes

- 4.3.3 Inter-Protocol Interference in Dense RF Environments

- 4.3.4 Fragmented Firmware Update Ecosystem for OEMs

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Bluetooth Smart Devices

- 5.1.2 Bluetooth Smart Ready Devices

- 5.2 By Robot Type

- 5.2.1 Industrial Robots

- 5.2.2 Collaborative Robots

- 5.2.3 Professional Service Robots

- 5.2.4 Domestic Service Robots

- 5.2.5 Humanoid Robots

- 5.3 By Technology

- 5.3.1 Bluetooth Low Energy

- 5.3.2 Bluetooth Classic

- 5.3.3 Bluetooth Mesh

- 5.3.4 Bluetooth 5.0

- 5.3.5 Bluetooth 5.1

- 5.4 By Application

- 5.4.1 Healthcare

- 5.4.2 Wearable Devices

- 5.4.3 Smart Home

- 5.4.4 Automotive

- 5.4.5 Industrial Automation

- 5.5 By End-User Industry

- 5.5.1 Consumer Electronics

- 5.5.2 Healthcare

- 5.5.3 Automotive

- 5.5.4 Industrial

- 5.5.5 Retail

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 United Arab Emirates

- 5.6.5.1.2 Saudi Arabia

- 5.6.5.1.3 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Egypt

- 5.6.5.2.3 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Qualcomm Inc.

- 6.4.2 Nordic Semiconductor ASA

- 6.4.3 Texas Instruments Incorporated

- 6.4.4 Broadcom Inc.

- 6.4.5 Silicon Laboratories Inc.

- 6.4.6 NXP Semiconductors N.V.

- 6.4.7 STMicroelectronics N.V.

- 6.4.8 Infineon Technologies AG

- 6.4.9 Renesas Electronics Corporation

- 6.4.10 Microchip Technology Inc.

- 6.4.11 Cypress Semiconductor Corporation

- 6.4.12 Realtek Semiconductor Corp.

- 6.4.13 Murata Manufacturing Co. Ltd.

- 6.4.14 Atmosic Technologies Inc.

- 6.4.15 Dialog Semiconductor plc

- 6.4.16 Espressif Systems (Shanghai) Co. Ltd.

- 6.4.17 MediaTek Inc.

- 6.4.18 Toshiba Electronic Devices & Storage Corp.

- 6.4.19 Panasonic Holdings Corp.

- 6.4.20 ON Semiconductor Corp.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

藍牙市場趨勢

藍牙市場趨勢 藍牙市場:依技術、範圍和應用分類-2026-2032年全球市場預測

藍牙市場:依技術、範圍和應用分類-2026-2032年全球市場預測 2026年藍牙全球市場報告2026年藍牙智慧半導體全球市場報告藍牙晶片市場:依技術、範圍、組件和應用分類-2026-2032年全球市場預測藍牙智慧及智慧就緒市場:依技術、組件、終端用戶產業及應用分類-2026-2032年全球市場預測藍牙感測器市場按類型、技術、連接範圍、電源、應用、最終用戶和銷售管道,全球預測(2026-2032年)

2026年藍牙全球市場報告2026年藍牙智慧半導體全球市場報告藍牙晶片市場:依技術、範圍、組件和應用分類-2026-2032年全球市場預測藍牙智慧及智慧就緒市場:依技術、組件、終端用戶產業及應用分類-2026-2032年全球市場預測藍牙感測器市場按類型、技術、連接範圍、電源、應用、最終用戶和銷售管道,全球預測(2026-2032年) 藍牙IC市場-全球產業規模、佔有率、趨勢、機會及按類型、應用、地區和競爭格局分類的預測(2021-2031年)藍牙智慧就緒市場-全球產業規模、佔有率、趨勢、機會、預測:按設備、技術、最終用戶、地區和競爭對手分類,2021-2031年

藍牙IC市場-全球產業規模、佔有率、趨勢、機會及按類型、應用、地區和競爭格局分類的預測(2021-2031年)藍牙智慧就緒市場-全球產業規模、佔有率、趨勢、機會、預測:按設備、技術、最終用戶、地區和競爭對手分類,2021-2031年 藍牙模組市場:未來預測(2025-2030)

藍牙模組市場:未來預測(2025-2030)