|

市場調查報告書

商品編碼

2062029

碘化銀:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Silver Iodide - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

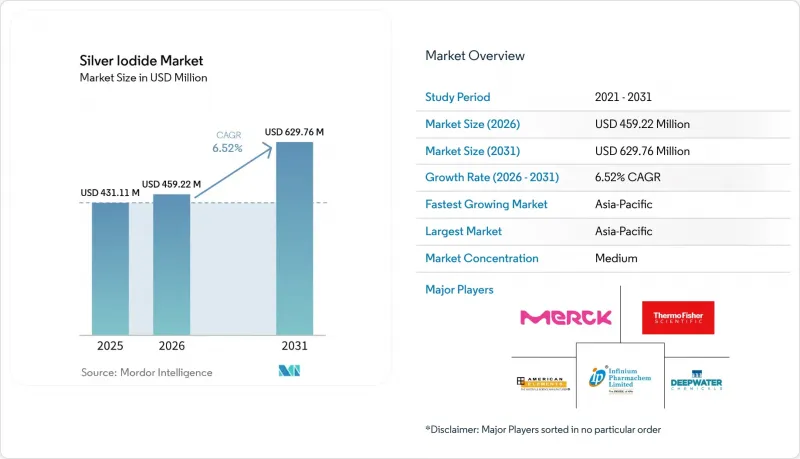

根據 Mordor Intelligence 預測,碘化銀市場規模預計在 2025 年達到 4.3111 億美元,2026 年達到 4.5922 億美元,到 2031 年達到 6.2976 億美元,2026 年至 2031 年的複合年成長率為 6.52%。

本報告按類型(晶體、粉末狀、懸浮液/膠體)、應用(人工降雨、防腐劑/抗菌劑、其他)、終端用戶行業(農業/環境、醫療/製藥、其他)和地區(亞太、北美、歐洲、南美、中東和非洲)進行細分。市場預測以美元計價。

全球碘化銀市場趨勢及洞察

對抗菌和防腐塗層的需求正在飆升。

醫院系統採用碘化銀 (AgI) 基表面薄膜,可釋放離子 6-12 個月,以控制感染成本。與膠體銀相比,這些薄膜具有更長的有效使用壽命。碘化銀塗層符合國際標準化組織 (ISO) 10993 的細胞毒性閾值,並符合歐盟醫療設備法規 (EU MDR)。自美國食品藥物管理局(FDA) 於 2024 年實施更嚴格的無菌指南以來,碘化銀的採購量增加。因此,碘化銀市場需求強勁,尤其是在手術室維修工程中。供應商報告稱,感染率降低了 25-30%,為其溢價提供了合理的依據。

碘化銀感測器在工業IoT的應用拓展

含有碘化銀奈米晶體的石墨烯層能夠以毫秒級的反應時間檢測濃度為0.5 ppm的碘蒸氣,同時與金屬氧化物感測器相比,功耗降低40%。日本和韓國已將鹵素檢測納入其2025年智慧工廠藍圖。風力發電廠營運商正在採用配備此類感測器的電池節點,這推動了海上專案碘化銀市場的成長。臨床機構正在利用碘化銀電極進行非侵入性尿碘檢測,拓展了其在醫療領域的應用。此外,將這些感測器整合到5G閘道器中,也帶動了對膠體前驅物的需求。

環境和倫理方面對人為改變天氣實驗的反對意見。

愛達荷州眾議院第23號法案提案禁止人工降雨,原因是擔心流域內會累積銀殘留物。愛荷華州也正在進行類似的立法討論,非政府組織(NGO)援引預防原則作為依據。由於缺乏明確的責任框架,保險公司延後了相關決定,導致設備訂單停滯。如果此類禁令擴大,北美地區的需求可能會下降15%,這可能會影響到碘化銀市場——其最大的應用領域。人工降雨公司呼籲美國環保署(EPA)制定指導方針,以解決這些問題並恢復市場信心。

細分市場分析

到2025年,結晶型產品將佔銷售額的47.11%,這主要歸功於其4.592埃的晶格常數,該值與六方晶系的晶格常數相近,從而降低了成核勢壘。粉狀產品佔28%,在地面應用領域呈現穩定成長。懸浮液和膠體產品的銷售額成長了7.68%,主要受感測器油墨需求的推動。

晶體供應商正利用閉合迴路系統滿足REACH法規的註冊要求,從而將小規模的競爭對手排除在市場之外。膠體領域的創新者正利用溶液相製程設計奈米薄片,用於旋塗記憶體堆疊。東京化學工業株式會社正在大規模生產濃度為10 g/L的懸浮液用於研發,而默克公司則將碘化銀摻入乙炔碳黑中進行測試,以生產可直接使用的導電漿料。這些發展帶來了多元化的收入來源和更高的平均售價,從而鞏固了碘化銀市場的基礎。

區域分析

預計到2025年,亞太地區將佔全球銷售額的37.15%,並隨著中國部署全球最大的氣象改造網路以及日本擴大物聯網感測器生產規模,該地區的年均成長率將持續到2031年,達到7.76%。印度Infinium Pharmachem公司正在將其年產能提高500噸,加劇了該地區的價格競爭。韓國和台灣正在推進3奈米製程的AgI膜晶片的研究,預計到2028年,這將帶來1億美元的額外需求。目前,東協地區的檢測部署小規模,但隨著霧霾治理資金的增加,其規模可望擴大。

2025年,北美市場活動顯著活躍,這主要得益於美國西部地區為增加積雪覆蓋而採取的撒雪舉措。儘管愛達荷州和愛荷華州的法律阻力依然存在,但醫院和研發機構的採用正在支撐市場穩定。加拿大和墨西哥也零星地進行了一些項目,而美國實驗室則在聯邦政府資助的奈米裝置計畫中,對超高純度碘化銀的需求量主導。

以德國、英國和法國主導的歐洲繼續保持強勁的市場地位。嚴格的REACH註冊體系提高了准入門檻,鞏固了默克集團(Merck KGA-MERCK.COM)等現有參與企業的市場影響力。儘管人工降雨的預算有限,但鈣鈦礦研發和抗菌應用領域的進展正對市場產生正面影響。在北歐國家,碘化銀(AgI)被用於離岸風力發電機葉片塗層,以增強其抗鹽霧性能。

南美洲、中東和非洲地區已取得顯著進展。阿拉伯聯合大公國將於2025年進行多次噴灑作業,據通報降雨量有所改善。沙烏地阿拉伯將於2024年啟動一項全國性計劃,摩洛哥也正在考慮採取類似策略。巴西正在測試地面噴灑設備以保護大豆產量,但資金限制仍然是一大挑戰。南非正在評估碘化銀噴灑方案,以支援其位於開普敦的水庫。這些地區雖然規模較小,但正在推動全球碘化銀市場的成長。

其他好處

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 抗菌和防腐塗料需求激增

- 碘化銀感測器在工業IoT的應用日益廣泛

- 重複使用模擬和即時膠片照片

- 用於神經形態裝置和記憶裝置的客製化AgI奈米顆粒

- 鈣鈦礦和薄膜太陽能電池的突破性整合

- 市場限制因素

- 環境和倫理方面對人為改變天氣實驗的反對意見。

- 生物基冰核蛋白作為替代品的研究進展迅速

- 高純度碘化銀原物料價格波動及避險成本

- 價值鏈分析

- 波特五力模型

第5章 市場規模與成長預測

- 按類型

- 晶體

- 粉末狀

- 懸浮液/膠體

- 透過使用

- 人工降雨

- 防腐劑和抗菌劑

- 攝影與影像

- 電化學和感測器應用

- 測量和軍事用途

- 其他應用(合成、塗層)

- 按最終用戶行業分類

- 農業/環境

- 醫療和製藥

- 國防/航太

- 工業製造

- 其他終端用戶產業(研究等)

- 按地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- ASEAN

- 其他亞太國家

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐國家

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲國家

- 亞太地區

第6章 競爭情勢

- 市場集中度

- Strategic Initiatives

- 市佔率和排名分析

- 公司簡介

- Abcr GmbH

- American Elements

- Aritech Chemazone Pvt. Ltd.

- Ascensus

- Deep Water Chemicals

- ESPI Metals

- Infinium Pharmachem Limited

- Merck KGaA

- Micron Platers

- Nanoshel LLC

- Santa Cruz BIoTechnology Inc.

- Thermo Fisher Scientific Inc.

- Tokyo Chemical Industry (India) Pvt. Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the silver iodide market size is projected to be USD 431.11 million in 2025, USD 459.22 million in 2026, and reach USD 629.76 million by 2031, growing at a CAGR of 6.52% from 2026 to 2031.

This report is Segmented by Type (Crystalline, Powdered, and Suspension/Colloidal), Application (Cloud Seeding, Antiseptic and Antimicrobial Agents, and More), End-User Industry (Agriculture and Environment, Healthcare and Pharmaceuticals, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Silver Iodide Market Trends and Insights

Surging Demand for Antimicrobial and Antiseptic Coatings

Hospital systems are adopting silver iodide (AgI)-based surface films, which release ions for 6-12 months, to manage infection costs. These films have a longer functional lifespan compared to colloidal silver. Silver iodide coatings have met the International Organization for Standardization (ISO) 10993 cytotoxicity thresholds and comply with the European Union Medical Device Regulation (EU MDR). Procurement increased after the United States Food and Drug Administration (US FDA) implemented stricter aseptic guidance in 2024. Consequently, the silver iodide market is experiencing consistent demand, particularly from retrofit programs in operating rooms. Suppliers report a 25-30% reduction in infection rates to support premium pricing.

Expansion of Silver-Iodide-Based Sensors in Industrial IoT

Graphene layers integrated with AgI nanocrystals detect iodine vapor at 0.5 parts per million (ppm) with millisecond response time while consuming 40% less power compared to metal-oxide sensors. Japan and South Korea have included halogen sensing in their 2025 smart-factory roadmaps. Wind-farm operators are adopting battery nodes with these sensors, contributing to the growth of the silver iodide market in offshore projects. Clinical groups are utilizing AgI electrodes for non-invasive urinary iodine tests, expanding the application in the healthcare sector. Furthermore, the integration of these sensors into 5G gateways is driving demand for colloidal precursors.

Environmental and Ethical Opposition to Weather-Modification Trials

Idaho House Bill 23 proposes a ban on cloud seeding, citing concerns about silver residue deposition in watersheds. Similar legislative discussions are ongoing in Iowa, with non-governmental organizations (NGOs) referencing precautionary principles. Insurance providers are delaying decisions due to the absence of clear liability frameworks, resulting in halted equipment orders. If such bans expand, North American demand could decrease by 15%, affecting the silver iodide market, which represents its largest application. Cloud seeding companies are requesting Environmental Protection Agency (EPA) guidelines to address these concerns and restore market confidence.

Other drivers and restraints analyzed in the detailed report include:

- Renewed Use in Analogue and Instant-Film Photography

- Tailored AgI Nanoparticles for Neuromorphic and Memristor Devices

- Rapid Progress of Bio-Based Ice-Nucleating Proteins as Substitutes

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Crystalline grades captured 47.11% revenue in 2025 because their lattice parameter of 4.592 angstroms mirrors that of hexagonal ice and lowers the nucleation barrier. Powdered forms occupied 28% and grew steadily among ground-based seeding cooperatives. Suspension and colloidal variants expanded at 7.68%, catalyzed by sensor ink demand.

Crystalline suppliers leverage closed-loop systems to satisfy REACH dossiers, crowding out smaller rivals. Colloidal innovators tap solution-phase routes to engineer nanoflakes for spin-coated memristor stacks. Tokyo Chemical Industry scales 10 g/L suspensions for research and development, while Merck bundles AgI with test-grade acetylene black to create drop-in conductive pastes. These moves diversify revenue while lifting average selling prices, underpinning the silver iodide market.

Geography Analysis

Asia-Pacific generated 37.15% revenue in 2025 and accelerated at 7.76% through 2031 as China deploys the world's largest weather-modification network, and Japan scales IoT sensor manufacturing. India's Infinium Pharmachem adds 500 tons of annual capacity, sharpening regional price competition. South Korea and Taiwan explore AgI memristors for 3 nm processes, potentially adding USD 100 million incremental demand by 2028. ASEAN pilots, though tiny today, may expand if haze-control mandates gain funding.

In 2025, North America demonstrated significant market activity, driven by western U.S. seeding initiatives that enhanced snowpack levels. While legislative resistance in Idaho and Iowa presents challenges, adoption by hospitals and research and development (R&D) entities supports market stability. Canada and Mexico operate sporadic programs, with U.S. laboratories leading in the consumption of ultra-pure AgI for federally backed nanodevice projects.

Europe, led by Germany, the U.K., and France, maintained a strong presence in the market. The stringent REACH registration increases entry barriers and consolidates influence among established players like Merck KGA-MERCK.COM. Although cloud-seeding budgets are limited, the market benefits from advancements in perovskite R&D and antimicrobial applications. Nordic countries are utilizing AgI for offshore wind blade coatings to enhance resistance to salt fog.

South America and the Middle East & Africa regions exhibited notable developments. The UAE conducted numerous missions in 2025, reporting improved rainfall outcomes. Saudi Arabia initiated a national program in 2024, with Morocco exploring similar strategies. Brazil is testing ground-based generators to protect soybean yields, though financial constraints remain a consideration. South Africa is evaluating AgI seeding to support Cape Town's reservoirs. These regions, despite starting from smaller bases, contribute to the growth of the global silver iodide market.

- Abcr GmbH

- American Elements

- Aritech Chemazone Pvt. Ltd.

- Ascensus

- Deep Water Chemicals

- ESPI Metals

- Infinium Pharmachem Limited

- Merck KGaA

- Micron Platers

- Nanoshel LLC

- Santa Cruz Biotechnology Inc.

- Thermo Fisher Scientific Inc.

- Tokyo Chemical Industry (India) Pvt. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging demand for antimicrobial and antiseptic coatings

- 4.2.2 Expansion of silver-iodide-based sensors in industrial IoT

- 4.2.3 Renewed use in analogue and instant-film photography

- 4.2.4 Tailored AgI nanoparticles for neuromorphic and memristor devices

- 4.2.5 Break-through integration in perovskite and thin-film PV cells

- 4.3 Market Restraints

- 4.3.1 Environmental and ethical opposition to weather-modification trials

- 4.3.2 Rapid progress of bio-based ice-nucleating proteins as substitutes

- 4.3.3 High purity AgI feed-stock price volatility and hedging costs

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Crystalline

- 5.1.2 Powdered

- 5.1.3 Suspension/Colloidal

- 5.2 By Application

- 5.2.1 Cloud Seeding

- 5.2.2 Antiseptic and Antimicrobial Agents

- 5.2.3 Photography and Imaging

- 5.2.4 Electro-chemical and Sensor Applications

- 5.2.5 Research and Military Uses

- 5.2.6 Other Applications (Synthesis, Coatings)

- 5.3 By End-User Industry

- 5.3.1 Agriculture and Environment

- 5.3.2 Healthcare and Pharmaceuticals

- 5.3.3 Defense and Aerospace

- 5.3.4 Industrial Manufacturing

- 5.3.5 Other End-user Industries (Research, etc.)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 Japan

- 5.4.1.3 India

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 NORDIC Countries

- 5.4.3.8 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Initiatives

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 Abcr GmbH

- 6.4.2 American Elements

- 6.4.3 Aritech Chemazone Pvt. Ltd.

- 6.4.4 Ascensus

- 6.4.5 Deep Water Chemicals

- 6.4.6 ESPI Metals

- 6.4.7 Infinium Pharmachem Limited

- 6.4.8 Merck KGaA

- 6.4.9 Micron Platers

- 6.4.10 Nanoshel LLC

- 6.4.11 Santa Cruz Biotechnology Inc.

- 6.4.12 Thermo Fisher Scientific Inc.

- 6.4.13 Tokyo Chemical Industry (India) Pvt. Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

碘化銀市場-2026-2032年全球市場預測

碘化銀市場-2026-2032年全球市場預測 全球鹵化銀市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球鹵化銀市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 2026-2030年全球硝酸銀市場

2026-2030年全球硝酸銀市場 硝酸銀市場:依等級、應用、終端用戶產業、銷售管道和地區分類。膠體銀市場:依粒徑、形態、應用、通路、終端用戶產業及地區分類

硝酸銀市場:依等級、應用、終端用戶產業、銷售管道和地區分類。膠體銀市場:依粒徑、形態、應用、通路、終端用戶產業及地區分類 2026年全球硝酸銀市場報告

2026年全球硝酸銀市場報告 輝石礦市場規模、佔有率和成長分析:按產品類型、形態、應用、終端用戶產業、純度、分銷管道和地區分類-產業預測,2026-2033年汞測試接觸器市場按產品類型、應用、最終用戶、安裝類型和接點材料分類 - 全球預測,2026-2032年

輝石礦市場規模、佔有率和成長分析:按產品類型、形態、應用、終端用戶產業、純度、分銷管道和地區分類-產業預測,2026-2033年汞測試接觸器市場按產品類型、應用、最終用戶、安裝類型和接點材料分類 - 全球預測,2026-2032年 白銀:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)2026年全球銀礦市場報告

白銀:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)2026年全球銀礦市場報告