|

市場調查報告書

商品編碼

2062007

飼料脂肪和蛋白質:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)Feed Fats And Proteins - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

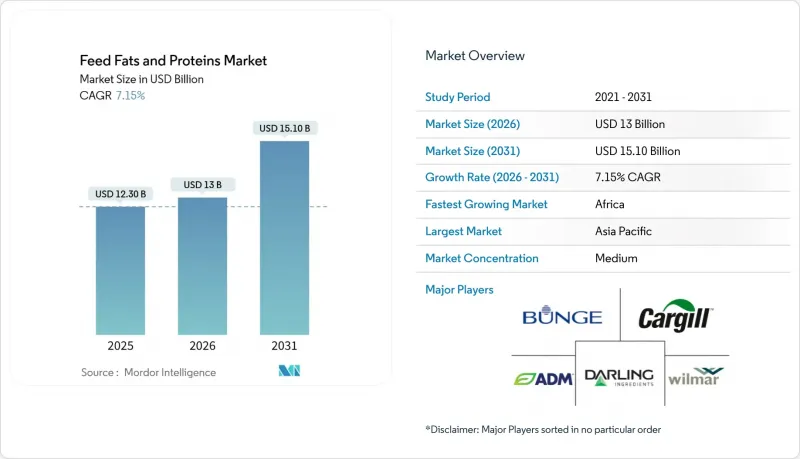

根據 Mordor Intelligence 預測,飼料脂肪和蛋白質的市場規模預計將從 2025 年的 123 億美元成長到 2026 年的 130 億美元,到 2031 年達到 151 億美元。從 2026 年到 2031 年,預計其複合年成長率為 7.15%。

本報告按產品類型(動物脂肪、植物油、混合特種油脂)、形態(乾粉/粉末、液態油脂)、畜牧業(家禽、豬、反芻動物、水產養殖、寵物食品)和地區(北美、南美、歐洲、亞太、中東和非洲)進行細分。市場預測以美元計價。

全球飼料脂肪及蛋白質市場趨勢及洞察

可再生柴油廠產生的過量動物脂肪副產品

來自可再生柴油工廠的剩餘動物脂肪副產品正成為飼料脂肪和蛋白質市場的重要驅動力。隨著可再生柴油產量的增加,動物副產品的供應量也隨之增加,這些副產品如今正被有效地用作飼料配方中經濟高效且營養豐富的成分。這種方法不僅透過最大限度地減少廢棄物來促進永續性,而且還有助於確保飼料原料的穩定供應。美國環保署 (EPA) 制定的 2026-2027 年可再生燃料標準將生質能衍生柴油的產量設定為 36 億加侖,這不僅保證了對原料的需求,也保障了副產品的穩定供應。

一種特殊的脂質混合物,可減少對抗生素的依賴。

全球家禽和生豬養殖戶正逐步淘汰抗生素生長促進劑,功能性脂質正成為可行的替代方案。 ADM 和 Berg+Schmidt GmbH & Co.KG(Stern-Wywiol 集團)共同開發了一種精準配方,將月桂酸與包封的 omega-3 脂肪酸相結合,為整合商提供了一種符合零售商「無抗生素」承諾的優質解決方案。這些特殊脂質混合物不僅有益於動物健康,還能減少對抗生素的依賴,進而促進永續農業實踐,而這正是全球消費者和監管機構日益關注的問題。

消費者對動物性飼料成分的強烈抵制

歐洲寵物食品消費者越來越關注動物性成分的永續性,儘管規模和成本方面仍有挑戰,但各品牌面臨的壓力也越來越大,促使他們嘗試使用藻類和昆蟲油。如果「植物來源」肉類的行銷宣傳進一步升溫,這一趨勢可能會蔓延到整個畜牧業。消費者意識的這種轉變可能會從寵物食品領域擴展到更廣泛的牲畜飼料市場。如果以永續性為導向的行銷在人類食品產業持續發展,動物營養領域也可能出現類似的預期。飼料生產商可能會面臨監管機構更嚴格的審查和配方變更的要求,這可能促使該行業轉向創新且經濟高效的傳統動物性成分替代品。

細分市場分析

到2025年,動物脂肪將成為最大的細分市場,佔飼料脂肪和蛋白質市場佔有率的44.5%,因為動物油脂加工企業向綜合性企業供應經濟實惠的動物和家禽脂肪。這一主導地位主要歸功於動物脂肪作為肉類加工和動物油脂加工行業的副產品而廣泛存在,使其成為飼料配方中經濟高效且永續的選擇。此外,動物脂肪具有高熱值,可提高飼料的能量密度,從而促進牲畜增重並提高飼料轉換率。成熟的供應鏈以及與現有飼料加工系統的兼容性鞏固了其市場地位,尤其是在價格敏感型市場。

混合特種油脂是成長最快的細分市場,預計2026年至2031年間將以9.8%的複合年成長率(CAGR)實現最高成長。這些產品透過將各種脂肪來源(例如植物油和海洋油)與功能性添加劑結合,提供客製化的營養成分。其日益普及的驅動力在於人們越來越重視“精準營養”,即最佳化飼料以滿足特定物種、生長階段和健康狀況的需求。在水產養殖中,混合油脂可以提高omega-3含量,促進魚類健康。在禽類和豬的養殖中,它們有助於提高免疫力,改善腸道環境,並最終提高整體生產力。

區域分析

亞太地區是全球最大的飼料市場,預計2025年將佔飼料脂肪和蛋白質市場34.2%的佔有率。這一主導地位主要得益於該地區規模龐大且快速發展的畜牧業和水產養殖業,尤其是中國、印度、越南和印尼等國家。 2025年,中國設定了2030年將大豆粕含量降至10%的目標,這迫使飼料加工商尋找替代蛋白質來源並提高脂肪含量以維持能量密度,從而推動了家禽脂肪和芥花籽油的進口。人口成長、可支配收入增加以及對動物蛋白質需求的成長是支撐該地區飼料生產的主要促進因素。此外,飼料生產商的強大實力、原料的充足供應以及對商業農業和水產養殖飼料基礎設施的持續投資,進一步鞏固了亞太地區在該市場的主導地位。

非洲是成長最快的地區,預計2026年至2031年間的複合年成長率將達到7.2%,為該地區最高。這一成長主要得益於都市化加快、蛋白質消費量上升以及畜禽養殖業的逐步現代化。各國政府和私人企業都在投資改善飼料品質和供應鏈,以提高農業生產力。儘管與更成熟的地區相比,非洲市場仍處於低度開發狀態,但由於人們對均衡動物營養的認知不斷提高以及商業農業的擴張,預計非洲對飼料脂肪和蛋白質的需求將持續成長。

在南美洲,受油籽加工趨勢和生質燃料政策變化的推動,預計未來幾年將保持穩定成長。在巴西,大豆壓榨的活躍發展正在擴大大豆粕及相關副產品的供應,從而促進飼料生產。在北美,可再生柴油燃料生產的擴張支撐了市場成長,進而產生大量動物脂肪和其他脂類副產品。由於這些副產品經濟實惠且易於獲取,因此擴大被用作飼料飼料。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 市場分析與定義的前提條件

- 分析範圍

第2章 分析方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 可再生柴油廠產生的過量動物脂肪副產品

- 一種特殊的脂質混合物,可減少對抗生素的依賴。

- 東南亞水產飼料生產廠的擴張

- 強制採購不造成森林砍伐的大豆將促進替代油脂的採用。

- 對高能量密度家禽和豬飼料的需求不斷成長。

- 基於區塊鏈的渲染可追溯性和新溢價的創建。

- 市場限制因素

- 動物脂肪和家禽脂肪的價格波動

- 疾病爆發後對加工產品的貿易壁壘

- 消費者對動物性飼料成分的強烈抵制

- 高多元多不飽和脂肪酸(PUFA)含量的液態油在儲存過程中光氧化造成的流失。

- 監理情勢

- 技術展望

- 波特五力分析

第5章:預測市場規模與成長率

- 依產品類型

- 動物脂肪

- 植物油

- 混合特殊脂質

- 按形狀

- 乾粉/粉末

- 液態油

- 畜牧業

- 家禽

- 豬

- 反芻動物

- 水產養殖

- 寵物食品

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 其他北美國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 法國

- 英國

- 西班牙

- 義大利

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 紐西蘭

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Cargill, Incorporated.

- Archer-Daniels-Midland Company

- Darling Ingredients Inc.

- Bunge Global SA

- Wilmar International Limited

- AAK AB

- BASF SE

- Alltech, Inc.

- The Scoular Company

- GrainCorp Limited

- DSM-Firmenich AG

- Evonik Industries AG

- Berg+Schmidt GmbH & Co. KG

- Adisseo SAS

- SARIA SE & Co. KG

第7章 市場機會與未來展望

According to Mordor Intelligence, the feed fats and proteins market size is projected to increase from USD 12.30 billion in 2025 to USD 13.00 billion in 2026 and reach USD 15.10 billion by 2031, growing at a CAGR of 7.15% over 2026-2031.

This report is Segmented by Product Type (Animal Fats, Vegetable Oils, and Blended Specialty Lipids), by Form (Dry Meals and Powders, and Liquid Fats and Oils), by Livestock (Poultry, Swine, Ruminants, Aquaculture, and Pet Food), and by Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Feed Fats And Proteins Market Trends and Insights

Surplus Animal-Fat By-Products from Renewable-Diesel Plants

Surplus animal-fat by-products from renewable diesel plants are becoming a significant driver of the feed fats and proteins market. The rise in renewable diesel production has increased the availability of animal by-products, which are now being effectively used as cost-efficient, nutrient-dense components in animal feed formulations. This approach not only promotes sustainability by minimizing waste but also helps stabilize the supply of feed ingredients. The Environmental Protection Agency's 2026-2027 Renewable Fuel Standard fixed biomass-based diesel at 3.6 billion gal, locking in demand for feedstocks while guaranteeing steady coproduct availability.

Specialty Lipid Blends That Reduce Antibiotic Reliance

Global poultry and swine producers are eliminating antibiotic growth promoters, while functional lipids have emerged as viable substitutes. ADM and Berg+Schmidt GmbH & Co.KG (Stern-Wywiol Gruppe) precision blends that combine lauric acid with encapsulated omega-3s, offering integrators a premium solution that aligns with retailer antibiotic-free pledges. These specialty lipid blends not only support animal health but also contribute to sustainable farming practices by reducing reliance on antibiotics, a demand increasingly sought by consumers and regulatory bodies worldwide.

Consumer Backlash Against Animal-Based Feed Ingredients

A rising cohort of European pet-food buyers questions the sustainability of rendered animal inputs, pressuring brands to trial algal and insect oils even though scale and cost remain constraints. This sentiment could spill into mainstream livestock channels if marketing claims around "plant-based" meat continue to gain traction. This changing consumer sentiment extends beyond the pet-food segment and could influence the broader livestock feed market. If sustainability-focused marketing in the human food industry continues to grow, similar expectations may emerge in animal nutrition. Feed producers may face increased regulatory scrutiny and demands for reformulation, driving the industry toward innovative yet cost-effective alternatives to traditional animal-derived inputs.

Other drivers and restraints analyzed in the detailed report include:

- Aquafeed Milling Expansion in Southeast Asia

- Mandatory Deforestation-Free Soy Sourcing Spurring Alternative Fats

- Photo-Oxidation Losses in High-Polyunsaturated Fatty Acids (PUFA) Liquid Fats During Bulk Storage

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Animal fats led the largest segment, with 44.5% of the feed fats and proteins market share in 2025, as renderers supplied cost-effective tallow and poultry fat to integrators. This dominance is largely due to their widespread availability as by-products of the meat processing and rendering industries, making them a cost-effective and sustainable option for feed formulations. Animal fats also provide a high calorific value, enhancing the energy density of feed and contributing to improved weight gain and feed conversion ratios in livestock. Their established supply chains and compatibility with existing feed processing systems strengthen their position, particularly in price-sensitive markets.

Blended specialty lipids are the fastest-growing segment and will post the highest CAGR of 9.8% through 2026-2031. These products are formulated by combining various fat sources, such as vegetable oils and marine oils, with functional additives to achieve customized nutritional profiles. Their increasing adoption is driven by the emphasis on precision nutrition, which optimizes feed for specific species, growth stages, and health outcomes. In aquaculture, blended lipids enhance omega-3 content and promote fish health, while in poultry and swine, they improve immunity, gut health, and overall productivity.

Geography Analysis

Asia-Pacific is the largest region, with 34.2% of the feed fats and proteins market share in 2025. This dominance is driven by the region's large and rapidly expanding livestock and aquaculture industries, particularly in countries such as China, India, Vietnam, and Indonesia. In 2025, China's aim to cut soybean-meal inclusion to 10% by 2030 forces mills to secure alternative proteins and raise fat levels to maintain energy density, stimulating imports of poultry fat and canola oil. Rising population, increasing disposable incomes, and growing demand for animal protein are key factors supporting feed production in the region. Additionally, the strong presence of feed manufacturers, availability of raw materials, and continued investments in commercial farming and aquafeed infrastructure further reinforce Asia-Pacific's leading position in the market.

Africa is the fastest-growing region, projected to log the highest regional CAGR of 7.2% through 2026-2031. This growth is mainly driven by rising urbanization, increasing protein consumption, and the gradual modernization of livestock and poultry farming practices. Both governments and private entities are investing in improving feed quality and supply chains to boost agricultural productivity. While the market remains less developed than in more established regions, growing awareness of balanced animal nutrition and the expansion of commercial farming are projected to sustain demand for feed fats and proteins in Africa.

South America is projected to experience steady growth in the coming years, driven by evolving oilseed processing dynamics and biofuel policies. In Brazil, robust soybean crushing activity has enhanced the availability of soybean meal and related by-products, bolstering feed production. In North America, market growth is supported by the expansion of renewable diesel production, which produces substantial volumes of animal fat and other lipid coproducts. These by-products are increasingly used in feed applications due to their cost-effectiveness and availability.

- Cargill, Incorporated.

- Archer-Daniels-Midland Company

- Darling Ingredients Inc.

- Bunge Global SA

- Wilmar International Limited

- AAK AB

- BASF SE

- Alltech, Inc.

- The Scoular Company

- GrainCorp Limited

- DSM-Firmenich AG

- Evonik Industries AG

- Berg + Schmidt GmbH & Co. KG

- Adisseo SAS

- SARIA SE & Co. KG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surplus animal-fat by-products from renewable-diesel plants

- 4.2.2 Specialty lipid blends that reduce antibiotic reliance

- 4.2.3 Aquafeed milling expansion in Southeast Asia

- 4.2.4 Mandatory deforestation-free soy sourcing spurring alternative fats

- 4.2.5 Rising demand for energy-dense poultry and swine rations

- 4.2.6 Blockchain-enabled rendering traceability, unlocking new premiums

- 4.3 Market Restraints

- 4.3.1 Price volatility of tallow and poultry fat

- 4.3.2 Trade barriers on rendered products after disease outbreaks

- 4.3.3 Consumer backlash against animal-based feed ingredients

- 4.3.4 Photo-oxidation losses in high-Polyunsaturated Fatty Acids (PUFA) liquid fats during storage

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Animal Fats

- 5.1.2 Vegetable Oils

- 5.1.3 Blended Specialty Lipids

- 5.2 By Form

- 5.2.1 Dry Meals and Powders

- 5.2.2 Liquid Fats and Oils

- 5.3 By Livestock

- 5.3.1 Poultry

- 5.3.2 Swine

- 5.3.3 Ruminants

- 5.3.4 Aquaculture

- 5.3.5 Pet Food

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.1.4 Rest of North America

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 France

- 5.4.3.3 United Kingdom

- 5.4.3.4 Spain

- 5.4.3.5 Italy

- 5.4.3.6 Russia

- 5.4.3.7 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 India

- 5.4.4.3 Japan

- 5.4.4.4 South Korea

- 5.4.4.5 Australia

- 5.4.4.6 New Zealand

- 5.4.4.7 Rest of Asia-Pacific

- 5.4.5 Middle East

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 Rest of Middle East

- 5.4.6 Africa

- 5.4.6.1 South Africa

- 5.4.6.2 Nigeria

- 5.4.6.3 Rest of Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share, Products And Services, And Recent Developments)

- 6.4.1 Cargill, Incorporated.

- 6.4.2 Archer-Daniels-Midland Company

- 6.4.3 Darling Ingredients Inc.

- 6.4.4 Bunge Global SA

- 6.4.5 Wilmar International Limited

- 6.4.6 AAK AB

- 6.4.7 BASF SE

- 6.4.8 Alltech, Inc.

- 6.4.9 The Scoular Company

- 6.4.10 GrainCorp Limited

- 6.4.11 DSM-Firmenich AG

- 6.4.12 Evonik Industries AG

- 6.4.13 Berg + Schmidt GmbH & Co. KG

- 6.4.14 Adisseo SAS

- 6.4.15 SARIA SE & Co. KG

7 Market Opportunities and Future Outlook

飼料油和蛋白質市場:2026-2032年全球市場預測(按產品類型、形態、目標動物、加工技術和應用分類)

飼料油和蛋白質市場:2026-2032年全球市場預測(按產品類型、形態、目標動物、加工技術和應用分類) 肉雞飼料添加劑:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)

肉雞飼料添加劑:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031) 家禽飼料添加劑市場規模、佔有率和成長分析:依產品類型、形態、應用、家禽品種、銷售管道和地區分類-2026年至2033年產業預測

家禽飼料添加劑市場規模、佔有率和成長分析:依產品類型、形態、應用、家禽品種、銷售管道和地區分類-2026年至2033年產業預測 家禽飼料添加劑市場-策略分析與預測(2026-2031)

家禽飼料添加劑市場-策略分析與預測(2026-2031) 2025-2031年全球及中國飼料市場現況及預測

2025-2031年全球及中國飼料市場現況及預測 全球飼料微生物蛋白市場全球家禽飼料原料市場

全球飼料微生物蛋白市場全球家禽飼料原料市場 北美玉米和小麥飼料市場預測至 2030 年 - 區域分析 - 按產品類型和畜牧業(家禽、反芻動物、豬、水產養殖等)

北美玉米和小麥飼料市場預測至 2030 年 - 區域分析 - 按產品類型和畜牧業(家禽、反芻動物、豬、水產養殖等) 歐洲玉米和小麥飼料市場預測至 2030 年 - 區域分析 - 按產品類型和畜牧業(家禽、反芻動物、豬、水產養殖等)

歐洲玉米和小麥飼料市場預測至 2030 年 - 區域分析 - 按產品類型和畜牧業(家禽、反芻動物、豬、水產養殖等) 至 2030 年亞太地區玉米和小麥飼料市場預測 - 區域分析 - 按產品類型和畜牧業(家禽、反芻動物、豬、水產養殖等)

至 2030 年亞太地區玉米和小麥飼料市場預測 - 區域分析 - 按產品類型和畜牧業(家禽、反芻動物、豬、水產養殖等)