|

市場調查報告書

商品編碼

2061812

乳木果油:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Shea Butter - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

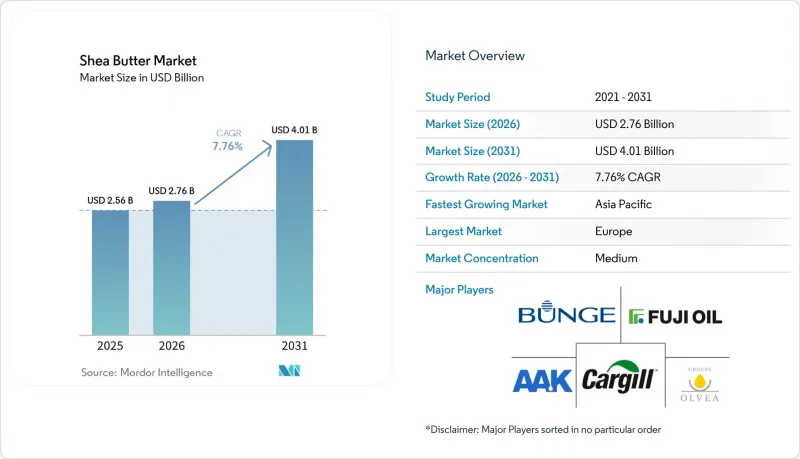

根據 Mordor Intelligence 預測,乳木果油市場規模將從 2025 年的 25.6 億美元和 2026 年的 27.6 億美元成長到 2031 年的 40.1 億美元,2026 年至 2031 年的複合年成長率為 7.76%。

本報告按原料類型(原料/未精製、精製、分餾)、應用領域(個人護理/化妝品、食品/飲料、藥品/營養補充劑、工業)和地區(北美、歐洲、亞太、南美、中東和非洲)進行細分。市場預測以價值(美元)和數量(噸)表示。

全球乳木果油市場趨勢及洞察

消費者對潔淨標示、有機和植物來源的個人護理成分的需求不斷成長。

消費者對潔淨標示、有機和植物來源個人護理成分的需求正在重塑產品開發策略,而乳木果油正逐漸成為護膚和護髮產品配方中的關鍵成分。消費者對透明度和天然成分的日益偏好,促使品牌以乳木果油等加工最少的替代品取代合成化學物質,從而滿足潔淨標示的要求。乳木果植物來源特性也契合了日益壯大的純素和零殘忍美容機芯,使其成為從高級產品到大眾市場等各種產品線的通用成分。根據美國國家衛生基金會 (NSF) 2024 年的數據,74% 的消費者優先考慮個人保健產品中的有機成分,這凸顯了消費者偏好對採購和配方決策的重大影響。為了因應這一趨勢,製造商越來越重視可追溯性和符合道德規範的採購,尤其是在乳木果油生產集中的西非供應鏈。 AAK AB 和 Ghana Nuts Company Limited 等供應商正在透過在其產品線中添加經認證的有機和公平貿易乳木果油來響應不斷變化的市場需求。此外,清潔美容趨勢、永續發展需求和監管壓力共同推動了多功能天然成分的普及,其中乳木果油的保濕和修復皮膚屏障功效更增添了其價值。獨立品牌和D2C(直接面對消費者)品牌透過強調「潔淨標示」的競爭優勢,進一步擴大了市場需求,鞏固了乳木果油在全球個人護理市場的地位。

GRAS/FDA 批准支持在美國和歐盟擴大食品應用。

美國和歐盟近期推出的法規核准措施,透過解決長期存在的監管難題,顯著推動了乳木果油在食品生產中的應用。美國食品藥物管理局(FDA)已將乳木果油酸(GRN 850,2020)和乳木果硬脂酸(GRN 1116,2024)認定為“公認安全(GRAS)”,允許將其添加到烘焙點心、糖果甜點塗層和乳製品替代品等產品中,最低添加量為總脂肪含量的10%。這項進展與食品業尋求經濟高效且功能等效的可可脂替代品的需求相契合,尤其是在可可價格波動和供應受限的情況下。同樣,歐洲食品安全局 (EFSA) 根據 (EC) No. 258/97 號法規於 2024 年進行的重新評估,再次確認了乳木果油的安全性,並將其適用範圍擴大到嬰兒配方奶粉和醫用營養食品等高度監管的類別。這些進展增強了製造商的信心,並刺激了對偏好和機能性食品等乳木果基配方研發的投資。邦吉洛德斯克羅克蘭 (Bunge Loders Croklaan) 等供應商已擴大其乳木果原料組合,以滿足不斷成長的需求。同時,美國和歐盟之間的監管協調正在促進跨境貿易,並為跨國製造商統一標準。加強可追溯性和品質保證要求進一步推動了標準化和規範化供應鏈的形成,使乳木果油成為食品行業中用途廣泛且受監管的成分。

乳木果供應量的波動受氣候和季節的影響。

由於乳木果供應量波動,乳木果油市場面臨嚴峻挑戰。乳木果的產量受氣候和季節因素影響顯著。乳木果的生產主要依賴西非的野生乳木果樹,人工栽培的機會有限。不規律的降雨模式、漫長的旱季以及季節性的收穫週期直接影響乳木果的產量,導致原料供應和價格波動。政策動盪進一步加劇了這些問題。例如,奈及利亞將原定於2026年2月宣布的一年出口禁令延長至2027年2月。據非洲貿易商會稱,這將導致每年約35萬至50萬噸乳木果的損失,約佔全球產量的40%。供應減少迫使國際買家在加納、布吉納法索和象牙海岸共和國等國尋找替代貨源。然而,由於2024年至2025年的出口限制,這些國家本來就面臨供應緊張的局面,這進一步加劇了採購的難度。依賴穩定供應鏈的大規模食品和個人保健產品製造商正面臨原料成本波動和供應鏈不確定性加劇的困境。為了應對這些挑戰,企業正在尋求籌資策略多元化,並建立跨區域的夥伴關係,但這些轉型涉及複雜的物流環節和耗時成本。像IOI Loders Croklaan這樣的B2B企業正在拓展其多區域採購網路以降低區域風險,但它們對氣候敏感且地理位置集中的生產模式的依賴,仍然限制了這些策略的有效性,並影響著長期定價和庫存規劃。

細分市場分析

到2025年,未經精煉的乳木果油將佔據最大的市場佔有率,銷售額佔比高達58.13%。其主導地位源自於其傳統的、手工使用方式,這種方式在高階天然和有機化妝品領域仍然佔據重要地位。未經精煉的乳木果油不皂化物含量高達17%,而精煉產品的不皂化物含量僅為3-5%,這支持了其生物活性和加工過程極少的說法,從而吸引了追求天然和有機配方的消費者。另一方面,精煉乳木果油繼續供應給中端化妝品和個人護理品牌,這些品牌更注重標準化的顏色、香料和脂肪酸組成,同時降低成本。這一細分市場尤其受益於亞太市場需求的成長,該地區對符合基本安全性和有效性標準的具成本效益配方需求旺盛。

分餾乳木果油衍生物,如硬脂酸和油酸,正成為成長最快的細分市場,預計2026年至2031年將以8.44%的複合年成長率成長。由於這些衍生物具有精確的熔融特性、更高的穩定性和配方一致性,因此能夠滿足食品和化妝品領域不斷變化的應用需求,工業買家正在加速轉向使用這些衍生物。監管方面的進展,例如AAK AB公司於2024年獲得GRAS認證(GRN 1116),以及產品創新,例如邦吉有限公司的“Coberine 206”(可延長巧克力的保存期限),進一步加速了這一轉變。這些進展正在將分餾乳木果油衍生物確立為工業應用中高度擴充性和高性能的解決方案,同時支援不同終端用途類別的定向產品開發。

區域分析

歐洲在全球乳木果油市場佔最大佔有率,預計到2025年將佔全球需求的33.91%。這一主導地位源自於其嚴格的法規結構,該框架優先考慮可追溯性和永續性。例如,歐盟將於2024年12月生效的森林砍伐法規和政策,以及《企業永續性實質審查指令》,均要求進口商確保其供應鏈的完全透明,包括地塊層級的可追溯性以及對非森林砍伐來源的檢驗。這些措施與消費者對符合道德規範和環保理念的產品日益成長的需求相契合,尤其是在高階個人護理和化妝品領域。德國、法國和英國是主要的進口國,這主要歸功於歐萊雅、拜爾斯道夫和嬌韻詩等跨國化妝品公司,這些公司依賴經過認證的乳木果油來開發高品質的產品。此外,義大利和西班牙正崛起為乳木果油食品應用領域的主要參與者,它們利用監管部門的批准,將乳木果硬脂添加到符合潔淨標示標準的糖果甜點和烘焙產品中。另一方面,由於俄羅斯消費者對乳木果油的認知度較低,以及高階天然個人保健產品的滲透率不高,因此俄羅斯對乳木果油的需求較為有限。

亞太地區是成長最快的市場,預計2026年至2031年將以7.76%的複合年成長率成長。這一成長主要得益於可支配收入的增加以及消費者對清潔美容和功能性成分的需求不斷成長。在中國和印度,植物來源和天然個人保健產品正經歷強勁成長,這得益於監管方面的進步,例如2021年中國批准了含乳木果油的可可脂替代品,從而拓展了其在食品領域的應用。特種油領域的創新也促進了產品的普及,例如邦吉有限公司推出了「Coberine 206」等產品,以解決巧克力在溫暖氣候條件下穩定性不足的問題。日本和韓國正在成為膳食補充劑應用的新興利基市場,尤其是支持關節健康的乳木果油不皂化物補充劑。在澳大利亞,消費者對潔淨標示和符合道德規範的化妝品的需求正在推動市場成長,零售商強調公平貿易和永續發展認證,以吸引具有環保意識的消費者。

北美是一個重要的市場,這得益於其有利的法規環境以及消費者對潔淨標示和植物來源產品的強烈偏好。美國食品藥物管理局 (食品藥物管理局) 對乳木果油和硬脂酸的 GRAS(公認安全)認證,使其應用範圍擴展至糖果甜點、烘焙和乳製品替代品領域。從區域來看,美國是消費的主要驅動力,各大品牌越來越注重可追溯性和符合道德規範的採購,並與 AAK AB 的“Kolo Nafaso”項目等系統化供應鏈合作。加拿大和墨西哥雖然市場規模較小,但在天然化妝品和注重永續性的產品線方面也呈現穩定成長。在南美洲,巴西和阿根廷正逐步接受高階個人保健產品,但進口成本和品牌知名度低等挑戰依然存在。在中東和非洲,南非和阿拉伯聯合大公國等市場是精製乳木果油的主要進口國,其產品用於食品和化妝品。加納、布吉納法索、奈及利亞、馬利共和國和象牙海岸共和國等生產國越來越注重高附加價值加工,並得到出口限制和旨在加強當地產業參與的發展融資舉措的支持。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場動態

- 市場概覽

- 市場促進因素

- 消費者對潔淨標示、有機和植物來源的個人護理成分的需求不斷成長。

- 拓展其在食品配方中作為功能性脂質和可可脂替代品的應用。

- GRAS 和 FDA 的批准支持該產品在美國和歐盟的食品應用範圍擴大。

- 消費者對療效和營養益處的認知不斷提高

- 人們越來越偏好永續來源和公平貿易的原料。

- 加工技術的進步提高了產量和品質穩定性

- 市場限制因素

- 受氣候和季節因素影響,乳木果供應量出現波動。

- 未精煉供應鏈中的品質差異和欺騙風險

- 工業和B2B買家對價格高度敏感

- 與其它天然油脂的競爭非常激烈。

- 供應鏈分析

- 監理情勢

- 波特五力分析

第5章 市場規模與成長預測

- 依成分類型

- 生的,未精煉的

- 純化

- 分餾(硬脂酸、油酸)

- 透過使用

- 個人護理和化妝品

- 食品/飲料

- 藥品和營養保健品

- 工業用途(生物潤滑劑、蠟燭等)

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 其他北美國家

- 歐洲

- 德國

- 英國

- 義大利

- 法國

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 其他亞太國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 南非

- 阿拉伯聯合大公國

- 其他中東和非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市場排名分析

- 公司簡介

- AAK AB

- Bunge Global SA

- Cargill, Incorporated

- Olvea Group

- Savannah Fruits Company

- BASF SE

- Ghana Nuts Company Ltd.

- Fuji Oil Holdings

- Gombella Integrated Services

- Manorama Industries Ltd.

- All Organic Treasures GmbH

- Shea Radiance LLC

- SOPHIM

- Suru Chemicals & Pharmaceuticals Pvt. Ltd.

- Croda International Plc

- Natural Sourcing, LLC

- Bulk Apothecary

- Right Shea

- Hallstar(Biochemica)

- Clariant AG

- DDW The Color House(GNT Group)

- Synthite Industries Pvt. Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the shea butter market size is projected to expand from USD 2.56 billion in 2025 and USD 2.76 billion in 2026 to USD 4.01 billion by 2031, registering a 7.76% CAGR between 2026 and 2031.

This report is Segmented by Ingredient Type (Raw/Unrefined, Refined, Fractionated), Application (Personal-Care and Cosmetics, Food and Beverage, Pharmaceuticals and Nutraceuticals, Industrial), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Tons).

Global Shea Butter Market Trends and Insights

Rising demand for clean-label, organic, and plant-based personal care ingredients

Consumer demand for clean-label, organic, and plant-based personal care ingredients is reshaping product development strategies, with shea butter emerging as a key component in skincare and haircare formulations. The growing preference for transparency and naturally derived ingredients is driving brands to replace synthetic chemicals with minimally processed alternatives like shea butter, which aligns with clean-label expectations. Its plant-based origin also supports the expanding vegan and cruelty-free beauty movement, making it a versatile ingredient across premium and mass-market product lines. Data from the National Sanitation Foundation in 2024 indicates that 74% of consumers prioritize organic ingredients in personal care products, underscoring the impact of consumer preferences on procurement and formulation decisions . This trend has led manufacturers to emphasize traceability and ethical sourcing, particularly from West African supply chains, where shea butter production is concentrated. Suppliers such as AAK AB and Ghana Nuts Company Limited are responding by enhancing their portfolios with certified organic and fair-trade shea butter to meet evolving market demands. Additionally, the convergence of clean beauty trends, sustainability requirements, and regulatory pressures is driving the adoption of multifunctional natural ingredients, with shea butter's moisturizing and skin barrier-repair properties offering added value. Indie and direct-to-consumer brands are further amplifying demand by leveraging clean-label claims as a competitive advantage, solidifying shea butter's role in the global personal care market.

GRAS/FDA approvals supporting broader food applications in the United States and European Union

Recent regulatory approvals in the United States and European Union are significantly influencing the adoption of shea butter in food manufacturing by addressing long-standing regulatory challenges. The U.S. FDA's Generally Recognized as Safe (GRAS) determinations for shea olein (GRN 850, 2020) and shea stearin (GRN 1116, 2024) have enabled their inclusion in products such as baked goods, confectionery coatings, and dairy alternatives, with usage levels permitted up to a minimum 10% of total fat content . This development aligns with the food industry's pursuit of cost-efficient and functionally comparable alternatives to cocoa butter, particularly in response to volatile cocoa prices and supply constraints. Similarly, the European Food Safety Authority's 2024 re-evaluation under Regulation (EC) No 258/97 has reaffirmed the safety of shea butter and extended its application to high-regulation categories, including infant formula and medical nutrition. These advancements are fostering confidence among manufacturers and driving investments in research and development for shea-based formulations across indulgent and functional food categories. Suppliers such as Bunge Loders Croklaan expanded their shea ingredient portfolios to meet growing demand, while regulatory alignment between the U.S. and EU is facilitating smoother cross-border trade and harmonizing standards for multinational producers. Enhanced traceability and quality assurance requirements are further encouraging standardized and compliant supply chains, positioning shea butter as a versatile and regulation-backed ingredient in the food industry.

Volatility in shea nut supply due to climatic and seasonal dependencies

The shea butter market faces significant challenges due to the volatility in shea nut supply, which is heavily influenced by climatic and seasonal factors. Production depends largely on wild-grown shea trees in West Africa, with limited potential for controlled cultivation. Irregular rainfall patterns, prolonged dry periods, and seasonal harvesting cycles directly impact nut yields, causing fluctuations in raw material availability and pricing. Policy disruptions further compound these issues, as demonstrated by Nigeria's extension of its one-year export ban through February 2027, announced in February 2026, which removed an estimated 350,000-500,000 tonnes of annual nut supply, nearly 40% of global output, as per the African Trade Chamber. This supply contraction has forced international buyers to seek alternative sources in countries like Ghana, Burkina Faso, and Cote d'Ivoire, where prior export restrictions in 2024-2025 had already tightened supply, creating additional procurement challenges. Manufacturers reliant on consistent volumes for large-scale food and personal care production are grappling with increased input cost volatility and supply chain uncertainty. Companies are diversifying sourcing strategies and forming origin-specific partnerships to address these challenges, though such transitions involve logistical complexities and time. B2B players like IOI Loders Croklaan are expanding multi-origin sourcing networks to mitigate regional risks, but the reliance on climate-sensitive and geographically concentrated production continues to limit the effectiveness of these strategies, impacting long-term pricing and inventory planning.

Other drivers and restraints analyzed in the detailed report include:

- Growing consumer awareness of therapeutic and nutritional benefits

- Increasing preference for sustainably sourced and fair-trade ingredients

- Quality inconsistency and adulteration risks in unrefined supply chains

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Raw/unrefined shea butter accounted for the largest share of the market in 2025, contributing 58.13% of revenue. Its dominance is attributed to its traditional and artisanal usage base, which remains significant in premium natural and organic cosmetics. The high unsaponifiable content of raw shea butter, up to 17% compared to 3-5% in refined variants, supports claims of bioactivity and minimal processing, appealing to consumers seeking natural and organic formulations. At the same time, refined shea butter continues to serve mid-tier cosmetic and personal care brands that prioritize standardized color, odor, and fatty acid composition at a lower cost. This segment is particularly benefiting from rising demand in Asia-Pacific markets, where cost-effective formulations that meet baseline safety and efficacy standards are in high demand.

Fractionated shea butter derivatives, such as stearin and olein, are emerging as the fastest-growing segment, projected to expand at a CAGR of 8.44% from 2026 to 2031. Industrial buyers are increasingly shifting toward these derivatives due to their precise melting profiles, improved stability, and formulation consistency, which align with evolving application needs in food and cosmetics. Regulatory developments, such as AAK AB's GRAS approval (GRN 1116) for shea stearin in 2024, and product innovations like Bunge Limited's Coberine 206, which extends chocolate shelf life, are further accelerating this transition. These advancements position fractionated shea derivatives as scalable, high-performance solutions for industrial applications, while enabling targeted product development across diverse end-use categories.

Geography Analysis

Europe holds the largest share of the global shea butter market, accounting for 33.91% of demand in 2025. This dominance is attributed to stringent regulatory frameworks that prioritize traceability and sustainability. Policies such as the EU Deforestation Regulation and the Corporate Sustainability Due Diligence Directive, effective December 2024, mandate importers to ensure full supply chain transparency, including plot-level traceability and verification of deforestation-free sourcing. These measures align with growing consumer demand for ethical and environmentally responsible products, particularly in premium personal care and cosmetics. Germany, France, and the United Kingdom lead imports, driven by multinational cosmetic companies like L'Oreal, Beiersdorf, and Clarins, which rely on certified shea butter for high-quality formulations. Additionally, Italy and Spain are emerging as key players in shea-based food applications, leveraging regulatory approvals to incorporate shea stearin into confectionery and bakery products that meet clean-label standards. Conversely, Russia shows modest demand due to limited consumer awareness and lower penetration of premium natural personal care products.

The Asia-Pacific region is the fastest-growing market, projected to expand at a CAGR of 7.76% from 2026 to 2031. This growth is fueled by rising disposable incomes and increasing adoption of clean beauty and functional ingredients. China and India are experiencing robust growth in plant-based and natural personal care products, supported by regulatory developments such as China's 2021 approval of cocoa butter equivalents containing shea, which has broadened food applications. Innovation in specialty fats is also driving adoption, with companies like Bunge Limited introducing products such as Coberine 206 to address challenges in chocolate stability under warm climatic conditions. Japan and South Korea are emerging as niche markets for nutraceutical applications, particularly shea unsaponifiable supplements for joint health. In Australia, demand is driven by clean-label and ethically sourced cosmetics, with retailers emphasizing fair-trade and sustainability certifications that resonate with environmentally conscious consumers.

North America represents a significant market, supported by favorable regulatory frameworks and strong consumer preference for clean-label and plant-based products. The U.S. Food and Drug Administration's GRAS approvals for shea olein and stearin have expanded their use across confectionery, bakery, and dairy-alternative segments. The United States leads regional consumption, with brands increasingly focusing on traceability and ethical sourcing, often collaborating with structured supply chains such as AAK AB's Kolo Nafaso program. Canada and Mexico, while smaller markets, are witnessing steady growth in natural cosmetics and sustainability-driven product lines. In South America, Brazil and Argentina are gradually adopting premium personal care products, though challenges such as import costs and limited awareness persist. In the Middle East and Africa, markets like South Africa and the United Arab Emirates are key importers of refined shea for food and cosmetics. Producing nations, including Ghana, Burkina Faso, Nigeria, Mali, and Cote d'Ivoire, are increasingly focusing on value-added processing, supported by export restrictions and development finance initiatives aimed at strengthening local industry participation.

- AAK AB

- Bunge Global SA

- Cargill, Incorporated

- Olvea Group

- Savannah Fruits Company

- BASF SE

- Ghana Nuts Company Ltd.

- Fuji Oil Holdings

- Gombella Integrated Services

- Manorama Industries Ltd.

- All Organic Treasures GmbH

- Shea Radiance LLC

- SOPHIM

- Suru Chemicals & Pharmaceuticals Pvt. Ltd.

- Croda International Plc

- Natural Sourcing, LLC

- Bulk Apothecary

- Right Shea

- Hallstar (Biochemica)

- Clariant AG

- DDW The Color House (GNT Group)

- Synthite Industries Pvt. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand for clean-label, organic, and plant-based personal care ingredients

- 4.2.2 Expanding application as a functional lipid and cocoa butter alternative in food formulations

- 4.2.3 GRAS/FDA approvals supporting broader food applications in the United States and European Union

- 4.2.4 Growing consumer awareness of therapeutic and nutritional benefits

- 4.2.5 Increasing preference for sustainably sourced and fair-trade ingredients

- 4.2.6 Advancements in processing technologies improving yield and quality consistency

- 4.3 Market Restraints

- 4.3.1 Volatility in shea nut supply due to climatic and seasonal dependencies

- 4.3.2 Quality inconsistency and adulteration risks in unrefined supply chains

- 4.3.3 High price sensitivity among industrial and B2B buyers

- 4.3.4 Intense competition from alternative natural butters and oils

- 4.4 Supply Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 By Ingredient Type

- 5.1.1 Raw/Unrefined

- 5.1.2 Refined

- 5.1.3 Fractionated (stearin, olein)

- 5.2 By Application

- 5.2.1 Personal-Care and Cosmetics

- 5.2.2 Food and Beverage

- 5.2.3 Pharmaceuticals and Nutraceuticals

- 5.2.4 Industrial (bio-lubes, candles, etc.)

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.1.4 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 Italy

- 5.3.2.4 France

- 5.3.2.5 Spain

- 5.3.2.6 Russia

- 5.3.2.7 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 Australia

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 South Africa

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 AAK AB

- 6.4.2 Bunge Global SA

- 6.4.3 Cargill, Incorporated

- 6.4.4 Olvea Group

- 6.4.5 Savannah Fruits Company

- 6.4.6 BASF SE

- 6.4.7 Ghana Nuts Company Ltd.

- 6.4.8 Fuji Oil Holdings

- 6.4.9 Gombella Integrated Services

- 6.4.10 Manorama Industries Ltd.

- 6.4.11 All Organic Treasures GmbH

- 6.4.12 Shea Radiance LLC

- 6.4.13 SOPHIM

- 6.4.14 Suru Chemicals & Pharmaceuticals Pvt. Ltd.

- 6.4.15 Croda International Plc

- 6.4.16 Natural Sourcing, LLC

- 6.4.17 Bulk Apothecary

- 6.4.18 Right Shea

- 6.4.19 Hallstar (Biochemica)

- 6.4.20 Clariant AG

- 6.4.21 DDW The Color House (GNT Group)

- 6.4.22 Synthite Industries Pvt. Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

西非乳木果油:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)

西非乳木果油:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年) 分餾乳木果油市場:按形態、加工方法、包裝、應用、終端用戶產業和分銷管道分類-2026-2032年全球市場預測乳木果油市場:按類型、形態、原料、等級、應用和分銷管道分類-2026-2032年全球市場預測

分餾乳木果油市場:按形態、加工方法、包裝、應用、終端用戶產業和分銷管道分類-2026-2032年全球市場預測乳木果油市場:按類型、形態、原料、等級、應用和分銷管道分類-2026-2032年全球市場預測 乳木果油市場-全球產業規模、佔有率、趨勢、機會與預測:按產品、應用、銷售管道、地區和競爭格局分類,2021-2031年

乳木果油市場-全球產業規模、佔有率、趨勢、機會與預測:按產品、應用、銷售管道、地區和競爭格局分類,2021-2031年 乳木果油市場規模、佔有率和成長分析:按產品類型、類別、應用、分銷管道、最終用戶和地區分類-2026-2033年產業預測

乳木果油市場規模、佔有率和成長分析:按產品類型、類別、應用、分銷管道、最終用戶和地區分類-2026-2033年產業預測 2026年全球乳木果油市場報告化妝品級乳木果油市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、性質、最終用途、地區和競爭格局分類,2021-2031年

2026年全球乳木果油市場報告化妝品級乳木果油市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、性質、最終用途、地區和競爭格局分類,2021-2031年 全球乳木果油市場:產業分析、規模、佔有率、成長、趨勢與預測(2025-2032)

全球乳木果油市場:產業分析、規模、佔有率、成長、趨勢與預測(2025-2032) 乳木果油市場分析及預測(至2034年):類型、產品、應用、最終用戶、形式、製程、技術、成分、功能

乳木果油市場分析及預測(至2034年):類型、產品、應用、最終用戶、形式、製程、技術、成分、功能 2025-2029 年全球乳木果油市場

2025-2029 年全球乳木果油市場