|

市場調查報告書

商品編碼

2061719

美國職業健康:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)United States Occupational Health - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

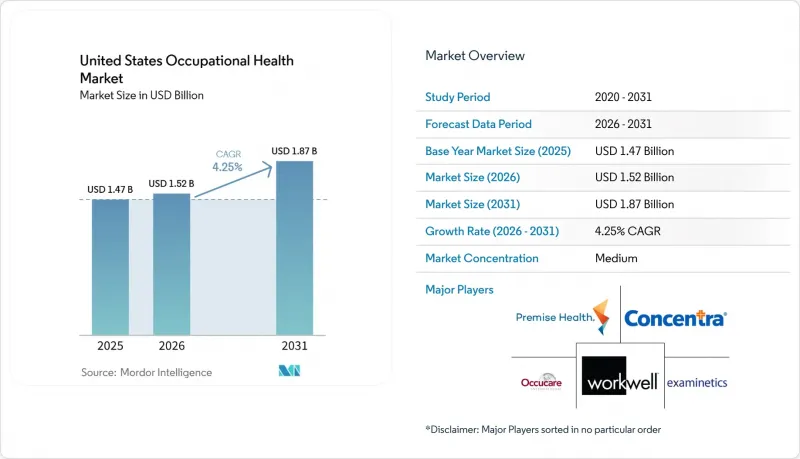

據 Mordor Intelligence 稱,2025 年美國職業健康市場價值 14.7 億美元,預計到 2031 年將從 2026 年的 15.2 億美元成長到 18.7 億美元,預測期(2026-2031 年)的複合年成長率為 4.25%。

本報告按服務類型(入職前和入職後體檢、藥物和酒精檢測等)、健康狀況(工作壓力、呼吸系統疾病等)、服務提供方式(現場診所等)以及最終用戶行業(製造業、建築業和採礦業等)進行分類。市場預測以美元計價。

美國職業健康市場趨勢與洞察

擴大雇主主導的健康福利

企業越來越將健康計畫視為留住人才的手段。 2024年的一項調查發現,實施結合生物特徵檢測、健康指導和心理健康支持資源的健康計畫的公司,其員工自願離職率比未提供此類計畫的競爭對手低12%。醫療服務提供者網路目前提供的套餐服務涵蓋預防性健康檢查、營養諮詢和壓力管理工作坊,旨在成為當地社區的健康合作夥伴,並在低風險地區抵消停滯不前的勞工保險。

遠距/混合辦公的普及推動了對遠距醫療服務的需求。

混合辦公模式正在瓦解傳統的以診所為中心的醫療服務模式。遠距員工可以透過視訊進行工作能力評估、提交在家採集的檢體並進行虛擬聽力測試,從而加快跨州入職流程。 2024年的一項系統性回顧發現,對於非體力勞動型職業,遠距評估與面對面諮商的診斷一致性高達94%。因此,現有診所營運商正在採用遠端醫療平台,以維持其在職業健康市場的佔有率。

註冊工業醫師短缺

全國範圍內,註冊執業醫師不足3000人,這限制了地方診所的服務範圍。醫療服務提供者越來越依賴執業護理師和醫師助理,在職業健康市場服務不足的地區,醫療服務擴張速度正在放緩。

細分市場分析

截至2025年,入職前和入職後健康檢查將維持32.46%的職業健康市場佔有率,但由於重工業自動化導致勞動力減少,其成長速度正在放緩。相較之下,員工支援計畫和心理健康計畫的複合年成長率(CAGR)為7.25%,因為對於許多白領員工而言,與職業倦怠相關的缺勤率超過了工傷賠償。藥物和酒精檢測仍然是合規性的重要支柱,但廉價口腔液檢測套組的出現正在擠壓其利潤空間。復健服務保持穩定,這得益於優先考慮早期療育的保險公司的支持。人體工學諮詢在大規模倉庫中不斷擴展,預防性評估使上肢損傷在兩年內減少了23%。

如今,雇主們更傾向於選擇打包服務而非單獨契約,這迫使服務提供者拓展服務範圍,並與健康服務供應商建立合作關係。預計到2031年,職業健康領域(尤其是心理健康服務)的市場規模將不斷擴大,並在總收入中佔據更大佔有率。遠距諮詢服務透過降低服務成本和提高諮詢使用率,幫助那些先前難以獲得相關服務的小規模雇主也能享受這些服務。這種結構性成長仍然與人們持續認知到社會心理風險是一項核心業務成本密切相關。

至2025年,工作壓力將佔職業健康市場的27.57%,年複合成長率達8.05%。這反映了高離職率以及因焦慮和憂鬱症導致的殘疾成本。肌肉骨骼疾病是第二大類,但由於工廠環境中物料搬運設備的日益普及,其佔有率正在下降。儘管改進的通風系統降低了呼吸系統疾病的發生率,但它們仍然是化工廠面臨的關鍵問題。陽光地帶地區因中暑而前往急診室就診的人數增加了18%,而且根據美國職業安全與健康管理局(OSHA)的新標準,這一趨勢可能會加速。

醫療機構正在擴大其行為醫學服務能力,並投資聘請全職諮詢師。他們現在利用數位化工具及早篩檢與壓力相關的問題,防止其升級為請假申請。同時,診所正在引入人體工學療法和重返職場支持,以應對累積創傷。這些服務轉變正在增強更廣泛的職業健康市場的成長前景。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 擴大公司主導的健康福利

- 遠程辦公和混合辦公的增加正在推動對遠距辦公服務的需求。

- 美國勞動市場日趨緊張,導致招募前篩檢擴大。

- 美國職業安全與健康管理局 (OSHA) 糾正建議的增加,促使各方實施積極主動的合規計畫。

- 利用人工智慧進行風險預測,降低傷害成本。

- 與氣候變遷相關的熱應激預防服務

- 市場限制因素

- 透過重工業自動化減少勞動力

- 降低低風險行業的工傷賠償保險費

- 註冊工業醫師短缺

- 雇主對持續健康監測中的資料隱私問題表示擔憂

- 價值供應鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按服務類型

- 入職前及入職後體檢

- 藥物和酒精檢測

- 免疫接種和旅遊醫學

- 員工支援計劃和心理健康計劃

- 復健及重返職場支援服務

- 人體工學及現場安全服務

- 依健康狀況

- 工作壓力

- 呼吸系統疾病

- 噪音性耳聾

- 化學和振動相關疾病

- 肌肉骨骼疾病

- 其他

- 透過配送方式

- 企業診所

- 異地診所/獨立中心

- 移動式工業衛生單元

- 遠距職業健康平台

- 按最終用戶行業分類

- 製造業

- 建築和採礦

- 醫療和社會福利

- 政府/公共部門

- 運輸/倉儲業

- 資訊科技、金融、專業服務

- 零售和酒店

第6章 競爭情勢

- 市場集中度

- 市佔率分析

- 公司簡介

- AllOne Health Resources

- Axiom Medical

- BioIQ

- Concentra

- Conserve Health

- CorVel Corporation

- Examinetics

- Harness Health Partners

- Intermountain WorkMed

- MediTrax

- Mobile Health

- National Vision Administrators(OccMed division)

- Nova Medical Centers

- OccuSystems

- Praxis Occupational Medicine

- Premise Health

- Total Safety

- US HealthWorks

- WorkCare, Inc.

- Workplace Safety & Prevention Services

- WorkWell Occupational Medicine

第7章 市場機會與未來展望

According to Mordor Intelligence, the united states occupational health market size was valued at USD 1.47 billion in 2025 and is estimated to grow from USD 1.52 billion in 2026 to reach USD 1.87 billion by 2031, at a CAGR of 4.25% during the forecast period (2026-2031).

This report is Segmented by Service Type (Pre-Employment & Post-Offer Exams, Drug & Alcohol Screening, and More), Health Condition (Work-Induced Stress, Respiratory Diseases, and More), Delivery Setting (On-Site Employer Clinics, and More), End-User Industry (Manufacturing, Construction & Mining and More). The Market Forecasts are Provided in Terms of Value (USD).

United States Occupational Health Market Trends and Insights

Expanding Employer-Sponsored Wellness Benefits

Organizations increasingly view wellness programs as retention tools. A 2024 study reported 12% lower voluntary turnover among companies that bundled biometric screenings, health coaching, and mental-health resources versus peers without such offerings.Provider networks now package preventive screenings with nutrition counseling and stress-management workshops, positioning themselves as population-health partners and offsetting flat workers' compensation premiums in low-risk sectors.

Growth of Remote/Hybrid Workforce Demanding Tele-OccMed Services

Hybrid work dismantles the traditional clinic-centric delivery model. Remote employees can complete fitness-for-duty evaluations by video, submit at-home specimens, and undergo virtual audiometry, accelerating onboarding across multiple states. A 2024 systematic review showed 94% diagnostic concordance between tele-evaluations and in-person visits for non-physical roles. Established clinic operators are therefore acquiring telehealth platforms to protect share within the occupational health market.

Shortage of Board-Certified Occupational Physicians

Fewer than 3,000 certified practitioners are active nationwide, limiting service scope in rural clinics. Operators rely more on nurse practitioners and physician assistants, and expansion slows in underserved regions of the occupational health market.

Other drivers and restraints analyzed in the detailed report include:

- Tight U.S. Labor Market Boosting Pre-Employment Screenings

- Rise in OSHA Citations Prompting Proactive Compliance Programs

- Employer Data-Privacy Concerns Over Continuous Health Monitoring

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Pre-Employment & Post-Offer Exams retained a 32.46% occupational health market share in 2025, but growth moderates as automation trims headcount in heavy industry. In contrast, Employee Assistance & Mental-Health Programs grow at a 7.25% CAGR, because burnout-driven absenteeism surpasses injury claims in many white-collar groups. Drug & Alcohol Screening remains a compliance pillar, yet margins tighten with cheaper oral-fluid kits. Rehabilitation services stay stable, aided by insurers that favor early intervention. Ergonomic consulting expands in large warehouses where proactive assessments cut upper-extremity injuries by 23% over two years.

Employers now seek bundled packages instead of individual engagements, forcing providers to diversify offerings or partner with wellness vendors. The occupational health market size for mental-health services is expected to represent an increasing slice of overall revenue by 2031. Tele-based counseling compresses delivery costs and increases session uptake, helping programs reach smaller employers that previously lacked access. Structural growth remains tied to continued recognition of psychosocial hazards as core business costs.

Work-Induced Stress captured 27.57% of the occupational health market size in 2025 and leads growth at 8.05% CAGR, reflecting high turnover and disability costs stemming from anxiety and depression. Musculoskeletal Disorders rank second but their share erodes as lift-assist devices spread on factory floors. Respiratory Disease incidence eases due to improved ventilation systems, yet remains a focus in chemical plants. Heat-stress visits rise 18% in Sun Belt emergency rooms, a trend likely to accelerate under OSHA's new standard.

Providers are expanding behavioral-health capacity and investing in on-staff counselors. Digital tools now triage stress claims before they escalate into leave requests. At the same time, clinics are integrating ergonomic therapy and return-to-work coaching to address cumulative trauma. These service shifts fortify growth prospects inside the broader occupational health market.

List of Companies Covered in this Report:

- AllOne Health Resources

- Axiom Medical

- BioIQ

- Concentra

- Conserve Health

- CorVel Corporation

- Examinetics

- Harness Health Partners

- Intermountain WorkMed

- MediTrax

- Mobile Health

- National Vision Administrators (OccMed division)

- Nova Medical Centers

- OccuSystems

- Praxis Occupational Medicine

- Premise Health

- Total Safety

- U.S. HealthWorks

- WorkCare

- Workplace Safety & Prevention Services

- WorkWell Occupational Medicine

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expanding Employer-Sponsored Wellness Benefits

- 4.2.2 Growth Of Remote / Hybrid Workforce Demanding Tele-Occmed Services

- 4.2.3 Tight U.S. Labor Market Boosting Pre-Employment Screenings

- 4.2.4 Rise In OSHA Citations Prompting Proactive Compliance Programs

- 4.2.5 AI-Enabled Risk-Prediction Reducing Injury Costs

- 4.2.6 Climate-Related Heat-Stress Prevention Services

- 4.3 Market Restraints

- 4.3.1 Automation Reducing Head-Count In Heavy Industry

- 4.3.2 Shrinking Workers? Comp Premiums In Low-Risk Sectors

- 4.3.3 Shortage Of Board-Certified Occupational Physicians

- 4.3.4 Employer Data-Privacy Concerns Over Continuous Health Monitoring

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value in USD)

- 5.1 By Service Type

- 5.1.1 Pre-Employment & Post-Offer Exams

- 5.1.2 Drug & Alcohol Screening

- 5.1.3 Immunizations & Travel Medicine

- 5.1.4 Employee Assistance & Mental-Health Programs

- 5.1.5 Rehabilitation & Return-to-Work Services

- 5.1.6 Ergonomic & On-Site Safety Services

- 5.2 By Health Condition

- 5.2.1 Work-Induced Stress

- 5.2.2 Respiratory Diseases

- 5.2.3 Noise-Induced Hearing Loss

- 5.2.4 Chemical & Vibration-Related Disorders

- 5.2.5 Musculoskeletal Disorders

- 5.2.6 Others

- 5.3 By Delivery Setting

- 5.3.1 On-Site Employer Clinics

- 5.3.2 Off-Site Clinics / Stand-Alone Centers

- 5.3.3 Mobile Occupational Health Units

- 5.3.4 Tele-Occupational Health Platforms

- 5.4 By End-User Industry

- 5.4.1 Manufacturing

- 5.4.2 Construction & Mining

- 5.4.3 Healthcare & Social Assistance

- 5.4.4 Government & Public Sector

- 5.4.5 Transportation & Warehousing

- 5.4.6 IT, Finance & Professional Services

- 5.4.7 Retail & Hospitality

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.3.1 AllOne Health Resources

- 6.3.2 Axiom Medical

- 6.3.3 BioIQ

- 6.3.4 Concentra

- 6.3.5 Conserve Health

- 6.3.6 CorVel Corporation

- 6.3.7 Examinetics

- 6.3.8 Harness Health Partners

- 6.3.9 Intermountain WorkMed

- 6.3.10 MediTrax

- 6.3.11 Mobile Health

- 6.3.12 National Vision Administrators (OccMed division)

- 6.3.13 Nova Medical Centers

- 6.3.14 OccuSystems

- 6.3.15 Praxis Occupational Medicine

- 6.3.16 Premise Health

- 6.3.17 Total Safety

- 6.3.18 U.S. HealthWorks

- 6.3.19 WorkCare, Inc.

- 6.3.20 Workplace Safety & Prevention Services

- 6.3.21 WorkWell Occupational Medicine

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment

環境、健康與安全市場-2026-2032年全球市場預測

環境、健康與安全市場-2026-2032年全球市場預測 感覺統合和職業治療設備市場預測——按設備類型、分銷管道、應用、最終用戶和地區分類的全球分析——2034年

感覺統合和職業治療設備市場預測——按設備類型、分銷管道、應用、最終用戶和地區分類的全球分析——2034年 職業健康市場分析與預測(至2035年):按類型、產品、服務、技術、組件、應用、最終用戶、解決方案和部署方式分類

職業健康市場分析與預測(至2035年):按類型、產品、服務、技術、組件、應用、最終用戶、解決方案和部署方式分類 職業健康市場:按服務類型、施行地點、最終用戶和區域分類職業治療服務市場預測-全球分析(按服務類型、治療類型、交付方式、年齡層、應用、最終用戶和地區分類)——2034年

職業健康市場:按服務類型、施行地點、最終用戶和區域分類職業治療服務市場預測-全球分析(按服務類型、治療類型、交付方式、年齡層、應用、最終用戶和地區分類)——2034年 環境、健康與安全 (EHS) 市場規模、佔有率、趨勢和預測:按組件、部署類型、行業和地區分類,2026-2034 年

環境、健康與安全 (EHS) 市場規模、佔有率、趨勢和預測:按組件、部署類型、行業和地區分類,2026-2034 年 2026年全球環境、健康與安全市場報告2026年全球環境健康與安全(EHS)軟體市場報告環境、健康與安全 (EHS) 市場分析及預測(至 2035 年):按類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶、功能和解決方案分類

2026年全球環境、健康與安全市場報告2026年全球環境健康與安全(EHS)軟體市場報告環境、健康與安全 (EHS) 市場分析及預測(至 2035 年):按類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶、功能和解決方案分類 職業安全與健康(OHS)全球市場規模、佔有率、趨勢和成長分析報告(2026-2034)

職業安全與健康(OHS)全球市場規模、佔有率、趨勢和成長分析報告(2026-2034)