|

市場調查報告書

商品編碼

2061667

複合添加劑:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)Formulation Additive - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

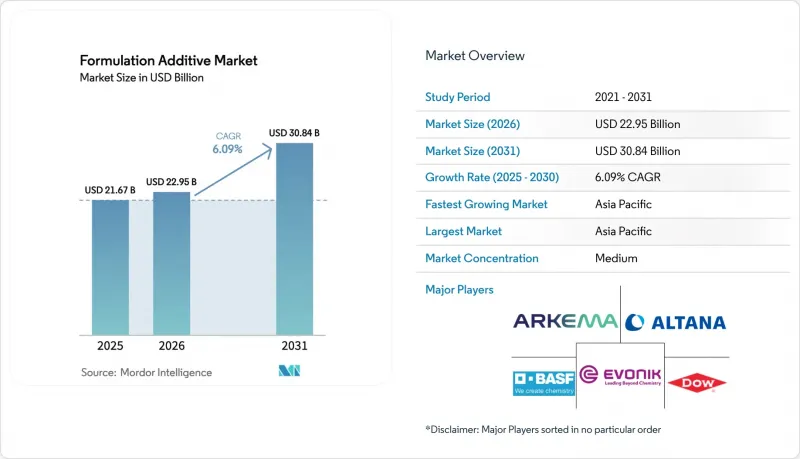

根據 Mordor Intelligence 預測,複合添加劑市場規模將從 2025 年的 216.7 億美元和 2026 年的 229.5 億美元成長到 2031 年的 308.4 億美元,2026 年至 2031 年的年複合成長率(CAGR)為 6.09%。

本報告按添加劑類型(消泡劑、流變改性劑)、終端用戶產業(建築、交通運輸、汽車、石油天然氣等)、配方技術(水性系統、溶劑型體係等)和地區(亞太地區、北美地區、歐洲地區、南美地區、中東和非洲地區)進行細分。市場預測以美元計價。

全球複合添加劑市場趨勢及洞察

基於永續性的低VOC水性塗料過渡

自2020年以來,水性塗料市場迅速成長,如今已佔據全球建築塗料市場的重要佔有率。這項轉變恰逢歐盟和加州等機構實施了更嚴格的VOC(揮發性有機化合物)排放法規。為因應這些變化,領先的製造商正從傳統的乙二醇醚類塗料轉向生物基無芯塗料,同時締合型增稠劑的應用也在不斷增加。這些增稠劑無需使用有機溶劑即可保持塗料黏度,與溶劑型塗料相比,顯著降低了生產階段的排放。BASF推出了流變改性劑,其性能可媲美醇酸樹脂的抗流掛特性,使設計師能夠在保持高品質施工的同時,獲得LEED v4.1認證積分。同時,採用無VOC著色劑的塗料平台,例如本傑明莫耳公司的「Gennex」系列,正在降低顏料的需求,從而顯著降低原料成本。此外,在美國和歐洲,公共部門採購中出現了一個明顯的趨勢,即優先考慮有第三方環境聲明支持的產品,這加速了基礎設施項目的變革。

新興國家基礎建設支出增加

印度計劃在其「國家化學品政策」的指導下,2030年大幅提升國內化學品產量。該保單為在12個指定投資區投資的外國投資者提供極具吸引力的10年免稅優惠。同時,在印度尼西亞,努桑塔拉(Nusantara)首都計畫正在樹立標桿,強制要求所有政府建築使用低揮發性有機化合物(VOC)塗料,從而提升了對水性分散劑和消泡劑的需求。沙烏地阿拉伯公共投資基金(PIF)正在NEOM工業區進行大規模投資,該工業區配備了乙烯裂解裝置,以支持下游添加劑製造工廠。這項策略措施可望降低當地混料企業的物流成本。在越南,近期對《建築法》的修訂強制要求對高層建築專案進行VOC檢測,預計到2028年,受監管添加劑市場將盈利發展。 2024年,主要多邊金融機構投入巨資,以加強東南亞的基礎建設,特別注重綠建築協議,並強調對水性和紫外線固化解決方案的偏好。

嚴格的 REACH 和 TSCA 重新註冊費用

2025年,歐洲化學品管理局(ECHA)在其候選清單中新增了八種物質。除強制性基因毒性測試外,製造商在準備大規模生產物質的註冊文件方面面臨巨大的成本。在美國,美國環保署(EPA)要求製造商每四年報告數千種化學品的暴露數據,違規者將面臨巨額罰款。贏創公司在其內部模型(該模型考慮了未來的許可費用)預測其部分錶面活性劑產品淨現值為負值後,停止了這些產品的銷售。中型企業,尤其是那些產品線規模低於一定標準的企業,則承受過重的合規成本負擔。

細分市場分析

到2025年,分散劑將佔銷售額的33.71%,凸顯了其在穩定各種系統(包括水性、溶劑型和紫外光固化系統)中的顏料和填料方面發揮的關鍵作用。BASF的DISPERBYK-2150採用聚氨酯骨架,可減少二氧化鈦的需求,進而降低塗料批次的成本。

預計在2026年至2031年的預測期內,流變改性劑將以6.61%的複合年成長率成長,這主要得益於對具有剪切稀釋性能的3D列印砂漿和具有防流掛性能的垂直表面塗層的需求。隨著即使在熱帶地區也能承受黏度漂移的共軛增稠劑的出現,複合添加劑市場的應用範圍正從溫帶地區擴展到其他地區。消泡劑佔據了相當大的市場。贏創的無矽產品不僅符合歐盟生態標章標準,也解決了緞面塗料長期存在的凹洞問題。界面活性劑基潤濕劑符合電子產業嚴格的離子污染標準,而偶聯劑、黏合促進劑和紫外線穩定劑的組合產品則在專業細分市場中做出了重要貢獻。

區域分析

預計到2025年,亞太地區將佔全球銷售額的42.23%,並在2026年至2031年的預測期內以6.99%的複合年成長率成長。印度雄心勃勃的化工產業發展藍圖以及中國在江蘇和山東兩省特種化學品產業園區的戰略投資是推動這一成長的主要動力。沙烏地基礎工業公司(SABIC)在福建的合資企業(目前使用EVA原料生產黏合劑添加劑)的投資,正在提振區域生產商在複合添加劑市場擴大市場佔有率的努力。此外,日本的補貼計畫也正在加強半導體級分散劑的國內生產。

北美地區預計將在2025年佔據較大的市場佔有率,這得益於《通貨膨脹控制法案》(IRA)推動的電氣化進程以及陶氏化學在德克薩斯州擴大生物乙烯生產。這項擴張在供應流變改性劑所需的低碳丙烯酸酯單體方面發揮著至關重要的作用。墨西哥的近岸外包熱潮創造了大量工廠就業機會,並推動了對三防膠和導熱界面材料的需求激增。這些材料高度依賴表面活性劑和偶聯劑的包裝。該地區豐富的頁岩氣資源支撐著特種添加劑的生產,而歐洲則不具備此優勢,只好依賴進口且原物料價格波動較大。

在歐洲,市場動態正受到歐盟綠色交易「面向55歲族群」目標的驅動。這些目標促使複合材料製造商轉向水性固化和紫外光固化系統等永續解決方案。德國正利用脫碳補助津貼支持電氣化裂解裝置和生物基先導計畫,為綠色標籤添加劑市場鋪平道路。在南美洲,巴西建設業的復甦和阿根廷鋰產業的崛起正在重振市場,這兩個國家都對耐腐蝕儲層塗層表現出濃厚的興趣。同時,在中東和非洲,儘管低成本的乙烷原料正在被利用,但分散的監管阻礙了特種等級產品的推廣應用。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 基於永續性的低VOC水性塗料過渡

- 新興國家基礎建設投資的擴張

- 高性能輕質複合材料的快速成長

- 電動車領域對溫度控管液和添加劑的需求

- 原始設備製造商推廣與感測器相容的超低介電常數添加劑

- 市場限制因素

- 石化原料價格波動

- 嚴格的 REACH 和 TSCA 重新註冊費用

- 加大力度禁止使用不含 PFAS 的規格。

- 價值鏈分析

- 波特五力模型

第5章 市場規模與成長預測

- 按添加劑類型

- 消泡劑

- 流變改性劑

- 分散劑

- 產業最終用途

- 建造

- 運輸

- 車

- 石油和天然氣

- 食品/飲料

- 電子設備

- 其他終端用戶產業

- 透過配方技術

- 水基系統

- 溶劑型體系

- 粉末塗裝

- UV/EB固化系統

- 按地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 其他亞太國家

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲國家

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- Altana(BYK)

- Arkema

- Arxada

- BASF

- Cabot Corporation

- Clariant

- Dow

- Eastman Chemical Company

- Evonik Industries AG

- Honeywell International Inc.

- Huntsman International LLC

- LANXESS

- Lubrizol

- Momentive

- Munzing Chemie GmbH

- Wacker Chemie AG

第7章 市場機會與未來展望

According to Mordor Intelligence, the formulation additive market size is projected to expand from USD 21.67 billion in 2025 and USD 22.95 billion in 2026 to USD 30.84 billion by 2031, registering a CAGR of 6.09% between 2026 to 2031.

This report is Segmented by Additive Type (Defoamers, Rheology Modifiers, and More), End-Use Industry (Construction, Transportation, Automotive, Oil and Gas, and More), Formulation Technology (Water-Borne Systems, Solvent-Borne Systems, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Formulation Additive Market Trends and Insights

Sustainability-Driven Switch to Low-VOC Water-Borne Coatings

Since 2020, water-borne coatings have surged to dominate a significant share of the global architectural paint volume. This evolution aligns with the heightened VOC limit regulations imposed by authorities in the European Union and California. In light of these changes, major manufacturers are transitioning from the use of traditional glycol ethers to bio-based coalescents and are increasingly adopting associative thickeners. These thickeners, which uphold viscosity without organic solvents, have led to a notable decrease in cradle-to-gate emissions when compared with solvent-borne alternatives. BASF has introduced rheology modifiers that replicate the anti-sag characteristics of alkyds, allowing specifiers to secure LEED v4.1 credits while maintaining high application quality. Meanwhile, platforms such as Benjamin Moore's Gennex, which feature zero-VOC colorants, are reducing pigment demand, resulting in tangible raw-material cost reductions. Furthermore, in both the United States and Europe, there is a discernible trend in public-sector procurement favoring products backed by third-party environmental declarations, accelerating changes in infrastructure projects.

Expansion of Infrastructure Spending in Emerging Economies

India, under its National Chemicals Policy, is targeting a substantial boost in domestic chemical production by 2030. The policy offers foreign investors an enticing decade-long tax holiday across 12 chosen investment zones. Meanwhile, in Indonesia, the Nusantara capital project is setting a benchmark. It requires all government buildings to use low-VOC coatings, thereby increasing the demand for water-borne dispersing agents and defoamers. Saudi Arabia's Public Investment Fund is making a major investment in the NEOM industrial zone, featuring an ethylene cracker that will cater to downstream additive units. This strategic move is expected to cut logistics costs for local formulators. In Vietnam, a recent amendment to the Construction Law mandates VOC testing for skyscraper projects, paving the way for a profitable market for compliant additives by 2028. In 2024, major multilateral lenders committed significant funds to enhance Southeast Asian infrastructure, with a notable emphasis on green-building agreements, highlighting a preference for water-borne and UV-curable solutions.

Stringent REACH and TSCA Re-Registration Costs

In 2025, the European Chemicals Agency added eight substances to its Candidate List. Manufacturers face high costs for high-volume substance dossiers, excluding the essential genotoxicity testing. In the United States, the EPA requires manufacturers to report exposure data for thousands of chemicals every four years, imposing substantial fines for non-compliance. Evonik discontinued several surfactant SKUs after internal models projected a negative net present value, taking future authorization fees into account. Mid-sized firms, particularly those with product line portfolios below a certain threshold, are disproportionately burdened by these compliance costs.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Growth of High-Performance Lightweight Composites

- E-Mobility Demand for Thermal-Management Fluids and Additives

- Rising PFAS-Free Specification Bans

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, dispersing agents accounted for 33.71% of the revenue, highlighting their pivotal role in stabilizing pigments and fillers across various systems, including water-borne, solvent-borne, and UV. BASF's DISPERBYK-2150, leveraging a polyurethane backbone, curtailed the demand for TiO2, leading to cost efficiencies in paint batches.

Rheology modifiers are projected to grow at a 6.61% CAGR during the forecast period of 2026-2031, driven by the demand for shear-thinning 3D-print mortars and anti-sag vertical coatings. Associative thickeners, now adept at resisting viscosity drift even in tropical conditions, have broadened the formulation additive market's reach beyond temperate zones. Defoamers have secured a significant market share; Evonik's silicone-free introduction not only meets EU Ecolabel standards but also addresses crater-formation issues that previously challenged satin finishes. Surfactant-based wetting agents met the stringent ionic contamination standards of electronics, while a combination of coupling agents, adhesion promoters, and UV stabilizers made notable contributions to specialized niches.

Geography Analysis

In 2025, the Asia-Pacific region accounted for 42.23% of the global revenue and is projected to grow at a 6.99% CAGR during the forecast period of 2026-2031. India's ambitious chemical roadmap and China's strategic investments in specialty parks in Jiangsu and Shandong are the primary drivers of this growth. Regional producers are poised to increase their stake in the formulation additive market, bolstered by SABIC's investment in a Fujian complex, now utilizing EVA feedstock for adhesive additives. Furthermore, Japan's subsidy initiative is enhancing domestic production of semiconductor-grade dispersants.

North America, with a significant market share in 2025, is reaping benefits from IRA-driven electrification and Dow's bio-ethylene expansion in Texas. This expansion plays a crucial role in supplying low-carbon acrylate monomers, vital for rheology modifiers. The nearshoring boom in Mexico has spurred the creation of numerous factory jobs, escalating the demand for conformal coatings and thermal interface materials. These materials heavily depend on surfactant and coupling-agent packages. The region's specialty additives production enjoys a cushion from abundant shale gas, a privilege not extended to Europe, which grapples with import reliance and feedstock volatility.

Europe is steering its market dynamics in line with the EU Green Deal's Fit for 55 targets. These targets are steering formulators towards sustainable choices like water-borne and UV systems. Germany is advancing with decarbonization grants, backing electrified crackers and bio-based pilots, paving the way for a market for green-label additives. South America is buoyed by Brazil's construction resurgence and Argentina's rising lithium sector, both showing interest in corrosion-resistant pond coatings. Meanwhile, the Middle-East and Africa are leveraging low-cost ethane feedstock, though they grapple with fragmented regulations that slow the adoption of specialty grades.

- Altana (BYK)

- Arkema

- Arxada

- BASF

- Cabot Corporation

- Clariant

- Dow

- Eastman Chemical Company

- Evonik Industries AG

- Honeywell International Inc.

- Huntsman International LLC

- LANXESS

- Lubrizol

- Momentive

- Munzing Chemie GmbH

- Wacker Chemie AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Sustainability-driven switch to low-VOC water-borne coatings

- 4.2.2 Expansion of infrastructure spending in emerging economies

- 4.2.3 Rapid growth of high-performance lightweight composites

- 4.2.4 E-mobility demand for thermal-management fluids and additives

- 4.2.5 OEM push for sensor-friendly ultra-low-dielectric additives

- 4.3 Market Restraints

- 4.3.1 Volatile petrochemical feedstock pricing

- 4.3.2 Stringent REACH and TSCA re-registration costs

- 4.3.3 Rising PFAS-free specification bans

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitute Products

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Additive Type

- 5.1.1 Defoamers

- 5.1.2 Rheology Modifiers

- 5.1.3 Dispersing Agents

- 5.2 By End-use Industry

- 5.2.1 Construction

- 5.2.2 Transportation

- 5.2.3 Automotive

- 5.2.4 Oil and Gas

- 5.2.5 Food and Beverage

- 5.2.6 Electronics

- 5.2.7 Other End-user Industries

- 5.3 By Formulation Technology

- 5.3.1 Water-borne Systems

- 5.3.2 Solvent-borne Systems

- 5.3.3 Powder Coatings

- 5.3.4 UV/EB-curable Systems

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 Japan

- 5.4.1.3 India

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Altana (BYK)

- 6.4.2 Arkema

- 6.4.3 Arxada

- 6.4.4 BASF

- 6.4.5 Cabot Corporation

- 6.4.6 Clariant

- 6.4.7 Dow

- 6.4.8 Eastman Chemical Company

- 6.4.9 Evonik Industries AG

- 6.4.10 Honeywell International Inc.

- 6.4.11 Huntsman International LLC

- 6.4.12 LANXESS

- 6.4.13 Lubrizol

- 6.4.14 Momentive

- 6.4.15 Munzing Chemie GmbH

- 6.4.16 Wacker Chemie AG

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

- 7.2 Advanced Computational Modeling and In-silico Simulations

建築用卡波姆市場規模、佔有率和成長分析:依產品等級、功能、配方類型、應用、最終用途產業、分銷管道和地區分類-2026-2033年產業預測

建築用卡波姆市場規模、佔有率和成長分析:依產品等級、功能、配方類型、應用、最終用途產業、分銷管道和地區分類-2026-2033年產業預測 陶瓷添加劑市場:按材料、形態、陶瓷類型和應用分類-2026-2032年全球市場預測聚對苯二甲酸乙二醇酯添加劑市場:按類型、形態、應用和最終用途產業分類-2026-2032年全球市場預測

陶瓷添加劑市場:按材料、形態、陶瓷類型和應用分類-2026-2032年全球市場預測聚對苯二甲酸乙二醇酯添加劑市場:按類型、形態、應用和最終用途產業分類-2026-2032年全球市場預測 2026年全球機能飲料添加劑市場報告鹽添加劑市場:按類型、形態、等級、應用和分銷管道分類-2026-2032年全球市場預測環己烷甲胺市場:依等級、應用和分銷管道分類-2026-2032年全球市場預測複合添加劑市場:按類型、功能、形態、應用、最終用途產業和分銷管道分類-2026-2032年全球市場預測熱固性導電添加劑市場:依填料類型、樹脂類型、導電等級、最終用途產業和應用分類-2026-2032年全球預測熱塑性導電添加劑市場:依填料類型、形態、製造流程和應用分類-全球預測,2026-2032年

2026年全球機能飲料添加劑市場報告鹽添加劑市場:按類型、形態、等級、應用和分銷管道分類-2026-2032年全球市場預測環己烷甲胺市場:依等級、應用和分銷管道分類-2026-2032年全球市場預測複合添加劑市場:按類型、功能、形態、應用、最終用途產業和分銷管道分類-2026-2032年全球市場預測熱固性導電添加劑市場:依填料類型、樹脂類型、導電等級、最終用途產業和應用分類-2026-2032年全球預測熱塑性導電添加劑市場:依填料類型、形態、製造流程和應用分類-全球預測,2026-2032年 全球綠色燃料添加劑市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球綠色燃料添加劑市場規模、佔有率、趨勢和成長分析報告(2026-2034年)