|

市場調查報告書

商品編碼

2061654

噴霧乾燥設備:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Spray Drying Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

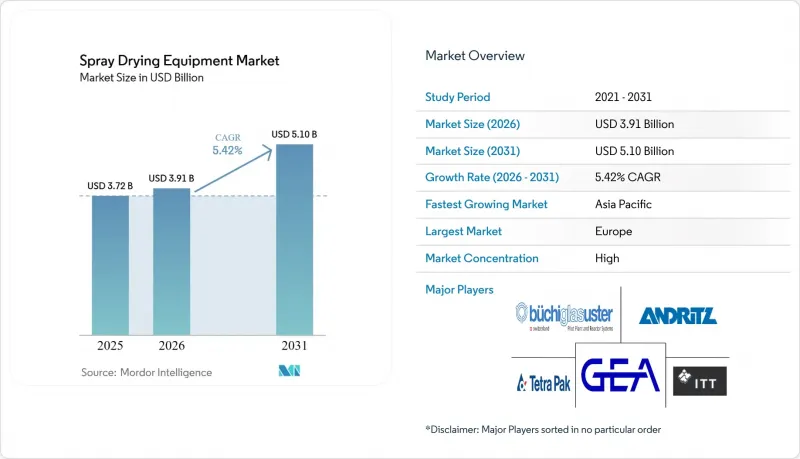

根據 Mordor Intelligence 預測,噴霧乾燥設備市場規模將從 2025 年的 37.2 億美元成長到 2026 年的 39.1 億美元,到 2031 年將達到 51 億美元,2026 年至 2031 年的複合年成長率為 5.42%。

本報告按乾燥階段(單級、兩級、多級)、工藝(旋轉輪式、離心/旋盤式等)、應用領域(乳製品、嬰幼兒配方奶粉、藥品等)和地區(北美、歐洲、亞太、南美、中東和非洲)進行細分。市場預測以美元計價。

全球噴霧乾燥設備市場趨勢及洞察

對加工食品和速食的需求不斷成長

全球消費者對簡便食品的需求不斷成長,這大大改變了噴霧乾燥設備的需求。製造商正大力投資這項技術,其中速溶咖啡和奶粉產品由於消費者的廣泛需求而引領潮流。食品製造商擴大噴霧乾燥技術的應用範圍,不僅是為了延長產品的保存期限,也是為了保留對熱敏性維生素和蛋白質等對維持產品品質至關重要的營養成分。這項技術在生產具有可控粒徑分佈的高流動性粉末方面發揮關鍵作用,這對於確保即溶飲料和即食食品配料的一致性和品質至關重要。此外,消費者對潔淨標示產品的日益偏好也加速了噴霧乾燥技術的普及。此方法能夠生產無添加劑的粉末,滿足消費者對更健康、更天然食品的需求,使其在眾多保鮮技術中脫穎而出。

對高溶解性嬰兒配方奶粉的需求不斷成長

在嬰幼兒配方奶粉的生產過程中,噴霧乾燥技術發揮至關重要的作用,確保奶粉營養全面,並符合世界衛生組織 (WHO) 和美國食品藥物管理局 (FDA) 制定的嚴格安全標準。根據 FDA 的《聯邦法規》第 21 篇第 106 部分 (21 CFR Part 106) 的規定,嬰幼兒配方奶粉的生產必須遵守嚴格的品管措施,包括設備檢驗和熱處理流程。這些措施正日益推動先進噴霧乾燥系統的應用。因此,製造商擴大採用專用噴霧乾燥機。這些先進系統不僅能維持蛋白質的功能性,還能滿足現代嬰幼兒營養配方所需的高溶解度要求。此外,該技術能夠有效包裹 DHA 和益生菌等易分解的營養成分,避免熱解,這一優勢也推動了高階設備的銷售成長。這一趨勢在亞太市場尤為明顯,該地區由於出生率上升和可支配收入增加,嬰幼兒配方奶粉的消費量正在不斷成長。

對經濟高效的乾燥技術的需求日益成長

在經濟壓力下,製造商正在評估與傳統噴霧乾燥系統相比,資本投資和營運成本更低的替代乾燥技術。冷凍乾燥和流體化床乾燥等技術作為有前景的替代方案,特別適用於那些在不顯著影響產品品質的前提下,可以優先考慮能源效率而非加工時間的應用情境。在新興市場,中小製造商正積極採用混合乾燥系統。這些系統將噴霧乾燥與更具成本效益的預濃縮製程相結合,使製造商能夠在保持理想產品品質的同時降低總資本投資。這些財務限制在通用食品應用領域尤為突出,因為利潤率受到巨大壓力,投資新設備的能力受到限制。因此,該領域的製造商正在延長現有設備的運作,並推遲採用先進技術,以有效控制成本。

細分市場分析

到2025年,單級乾燥機將主導噴霧乾燥設備市場,佔51.44%的顯著市場。這些乾燥機因其成本效益高、設計簡單而被廣泛應用,尤其適用於對乾燥要求不高的應用場景。在食品飲料、製藥和化學等行業,單級乾燥機因其能夠高效處理大量原料且操作相對簡單而備受青睞。此外,與多級系統相比,單級乾燥機的維護需求較低,因此對於尋求最佳化營運成本的製造商而言,也是理想之選。

預計到2031年,多級乾燥技術將以6.43%的複合年成長率達到最高成長。這一成長主要得益於市場對能夠確保更高產品品質和能源效率的先進乾燥解決方案的需求不斷成長。多級乾燥機尤其受到那些需要精確控制水分含量和粒徑的行業(例如特殊化學品和高價值食品行業)的青睞。此外,將先進的自動化和控制系統整合到多級乾燥機中,可提高其運作效率,使其成為滿足終端用戶產業不斷變化的需求的關鍵要素。

區域分析

到2025年,歐洲將以32.96%的全球市佔率引領噴霧乾燥設備市場。這得歸功於歐洲成熟的製藥生產基地和嚴格的監管標準,這些都促進了符合FDA標準的先進噴霧乾燥技術的應用。德國在這一區域主導地位中扮演著至關重要的角色,尤其是在乳製品領域。德國生產種類繁多的乳製品,包括脫脂奶粉、全脂奶粉和其他乳製品粉末。根據歐盟統計局(2024年)的數據,德國的乳製品產量約佔歐洲總產量的18.8%,這得益於其強大的生產能力和先進的加工基礎設施。蓬勃發展的乳製品產業是推動全部區域噴霧乾燥設備需求的主要動力。

預計亞太地區將成為成長最快的地區,到2031年複合年成長率將達到6.87%。這一成長主要得益於中國醫藥行業的現代化及其對ICH指南的遵守,加速了全球生產標準的採用。對先進原料藥(API)生產設施的投資顯著提升了對噴霧乾燥設備的需求。同時,印度等國家正在營養補充劑和食品加工領域擴大噴霧乾燥技術的應用,以滿足不斷成長的消費者需求。

北美地區持續保持強勁的市場地位,尤其是在特種化學品和先進食品配料等專業化和高附加價值應用領域。美國仍是主要貢獻者,在吸入劑和緩釋製劑等領域的應用顯著,這得益於其在製藥和食品加工領域持續加大研發投入。包括南美、中東和非洲在內的新興地區也正在加速發展,這主要得益於食品加工業的擴張。在南美,巴西食品飲料產業的成長,特別是乳製品加工業的成長,正在加速噴霧乾燥技術的應用。同樣,在中東和非洲,奶粉和咖啡生產帶來的日益成長的需求,也凸顯了這些市場的新成長機會。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 對加工食品和速食的需求不斷成長

- 對高溶解性嬰兒配方奶粉的需求不斷成長

- 植物來源和替代蛋白質原料的成長

- 奈米噴霧乾燥技術在營養補充品微膠囊化的應用日益廣泛

- 乳製品產業強勁成長

- 多級乾燥機的進展

- 市場限制因素

- 對經濟高效的乾燥技術的需求日益成長

- 嚴格的揮發性有機化合物(VOCs)和粒狀物排放標準

- 乾燥過程中熱敏成分劣化的風險

- 發展中市場操作先進多級乾燥機的技能差距

- 供應鏈分析

- 監理展望

- 波特五力模型

第5章 市場規模與成長預測

- 乾燥階段

- 單級

- 2個階段

- 多階段

- 透過流程

- 旋轉輪(壓力噴嘴)

- 氣動雙組分噴嘴

- 離心分離/旋轉盤

- 流化床噴霧乾燥器

- 閉合迴路(惰性氣體)

- 透過使用

- 乳製品

- 嬰兒配方奶粉

- 機能性食品和植物來源食品

- 製藥

- 營養補充品

- 其他

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 其他北美國家

- 歐洲

- 英國

- 德國

- 西班牙

- 法國

- 義大利

- 荷蘭

- 瑞典

- 波蘭

- 比利時

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 印尼

- 泰國

- 新加坡

- 其他亞太國家

- 南美洲

- 巴西

- 阿根廷

- 智利

- 哥倫比亞

- 秘魯

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 奈及利亞

- 摩洛哥

- 埃及

- 土耳其

- 其他中東和非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市場排名分析

- 公司簡介

- GEA Group AG

- ITT Inc(SPX FLOW)

- Antolab Group Co., Ltd.

- ANDRITZ GROUP

- SiccaDania Group

- The Tetra Laval Group

- Changzhou Jinqiao Spray Drying and Engineering Co., Ltd.

- Pulse Drying Systems

- Buchiglas(Buchi AG)

- Moret Industries

- SSP Pvt Limited

- Yamato Scientific Co Ltd

- G. Larsson Starch Technology AB

- THORNICO A/S

- Col-Int Tech

- AKSH Engineering Systems(P)Limited

- DORST Technologies GmbH & Co. KG

- Sinitech Industries doo

- Mojj Engineering Systems ltd.

- Kerone Engineering Solutions LTD.

第7章 市場機會與未來展望

According to Mordor Intelligence, the spray drying equipment market size is expected to grow from USD 3.72 billion in 2025 to USD 3.91 billion in 2026 and is forecast to reach USD 5.1 billion by 2031 at 5.42% CAGR over 2026-2031.

This report is Segmented by Drying Stage (Single-Stage, Two-Stage and Multi-Stage), Process (Rotary Wheel, Centrifugal/Spin Disc and More), Application (Dairy Products, Infant Formula, Pharmaceuticals and More), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Spray Drying Equipment Market Trends and Insights

Rising demand for processed and instant foods

The global shift toward convenience foods is actively driving a significant transformation in the demand for spray drying equipment. Manufacturers are heavily investing in this technology, with instant coffee and powdered dairy products leading the way due to their widespread consumer demand. Food producers are increasingly adopting spray drying not only to extend the shelf life of their products but also to preserve their nutritional value, particularly for heat-sensitive vitamins and proteins that are essential for maintaining product quality. This technology plays a crucial role in creating free-flowing powders with controlled particle size distribution, which is critical for ensuring consistency and quality in instant beverages and ready-to-eat meal components. Furthermore, the growing preference for clean-label products is accelerating the adoption of spray drying. This method enables the production of additive-free powders, offering a distinct advantage over alternative preservation techniques by meeting consumer demands for healthier and more natural food options.

Mounting demand for high-soluble infant formula powders

Spray drying technology plays a pivotal role in the production of infant formula, ensuring the powders are nutritionally complete and adhere to stringent safety standards set by the WHO and FDA. Under the FDA's 21 CFR Part 106 regulations, infant formula production is subject to rigorous quality control measures . These include validating equipment and thermal processing, both of which increasingly favor advanced spray drying systems. In response, manufacturers are turning to specialized spray dryers. These advanced systems not only uphold protein functionality but also meet the high solubility rates sought after in contemporary infant nutrition formulations. Furthermore, the technology's prowess in encapsulating delicate nutrients, such as DHA and probiotics, without subjecting them to thermal degradation, is propelling a surge in premium equipment sales. This trend is especially pronounced in the Asia-Pacific markets, buoyed by rising birth rates and increasing disposable incomes that bolster formula consumption.

Growing demand for cost effective drying technologies

Economic pressures are driving manufacturers to evaluate alternative drying technologies that offer lower capital and operating costs compared to traditional spray drying systems. Technologies such as freeze-drying and fluidized bed drying are gaining traction as viable alternatives, particularly in applications where manufacturers can prioritize energy efficiency over shorter processing times without significantly compromising product quality. In emerging markets, small and medium-sized manufacturers are actively adopting hybrid drying systems. These systems integrate spray drying with more cost-effective pre-concentration steps, enabling manufacturers to reduce overall equipment investment while still maintaining the desired product quality. The financial constraints are especially pronounced in commodity food applications, where intense margin pressures limit the ability to invest in new equipment. As a result, manufacturers in this segment are extending the operational lifecycles of their existing equipment and delaying the adoption of advanced technologies to manage costs effectively.

Other drivers and restraints analyzed in the detailed report include:

- Growth of plant-based and alternative protein ingredients

- Strong growth in dairy industry

- Stringent Volatile Organic Compound (VOC) and particulate emission norms

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, single-stage dryers dominated the spray drying equipment market, accounting for a significant 51.44% market share. These dryers are widely used due to their cost-effectiveness and simpler design, making them suitable for applications where basic drying requirements are sufficient. Industries such as food and beverages, pharmaceuticals, and chemicals frequently utilize single-stage dryers for their efficiency in handling large volumes of material with relatively low operational complexity. Additionally, their lower maintenance requirements compared to multi-stage systems make them a preferred choice for manufacturers aiming to optimize operational costs.

Multi-stage technology is projected to achieve the fastest growth rate, with a CAGR of 6.43% by 2031. This growth is driven by the increasing demand for advanced drying solutions that ensure higher product quality and energy efficiency. Multi-stage dryers are particularly favored in industries requiring precise control over moisture content and particle size, such as specialty chemicals and high-value food products. Furthermore, the integration of advanced automation and control systems in multi-stage dryers enhances their operational efficiency, making them a critical component in meeting the evolving demands of end-user industries.

Geography Analysis

In 2025, Europe leads the spray drying equipment market with a 32.96% global share, supported by a well-established pharmaceutical manufacturing base and stringent regulatory standards that promote the adoption of advanced, FDA-aligned spray drying technologies. Germany plays a pivotal role in this regional dominance, particularly in the dairy sector. The country produces a wide range of dairy products, including skim milk powders, whole milk powders, and other dairy-based powders. According to Eurostat (2024), Germany accounts for approximately 18.8% of Europe's total dairy output, underscoring its strong production capacity and advanced processing infrastructure. This robust dairy industry significantly drives demand for spray drying equipment across the region.

Asia-Pacific is expected to be the fastest-growing region, registering a CAGR of 6.87% through 2031. Growth is largely fueled by the modernization of China's pharmaceutical industry and its alignment with ICH guidelines, which is accelerating the adoption of global manufacturing standards. Investments in advanced API production facilities are significantly boosting demand for spray drying equipment. At the same time, countries like India are expanding the use of spray drying technologies in nutraceuticals and food processing to meet increasing consumer demand.

North America continues to hold a strong position, particularly in specialized and high-value applications such as specialty chemicals and advanced food ingredients. The United States remains a key contributor, with notable adoption in areas like inhalable drugs and controlled-release formulations, supported by ongoing investments in pharmaceutical and food processing research and development. Emerging regions, including South America and the Middle East and Africa, are also gaining momentum, primarily driven by the expansion of their food processing sectors. In South America, Brazil's growing food and beverage industry, especially in dairy processing, is accelerating the uptake of spray drying technologies. Similarly, the Middle East and Africa are experiencing increased demand due to rising production of powdered milk and coffee, highlighting new growth opportunities in these markets.

- GEA Group AG

- ITT Inc (SPX FLOW)

- Antolab Group Co., Ltd.

- ANDRITZ GROUP

- SiccaDania Group

- The Tetra Laval Group

- Changzhou Jinqiao Spray Drying and Engineering Co., Ltd.

- Pulse Drying Systems

- Buchiglas (Buchi AG)

- Moret Industries

- SSP Pvt Limited

- Yamato Scientific Co Ltd

- G. Larsson Starch Technology AB

- THORNICO A/S

- Col-Int Tech

- AKSH Engineering Systems (P) Limited

- DORST Technologies GmbH & Co. KG

- Sinitech Industries d.o.o.

- Mojj Engineering Systems ltd.

- Kerone Engineering Solutions LTD.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand for processed and instant foods

- 4.2.2 Mounting demand for high-soluble infant-formula powders

- 4.2.3 Growth of Plant-Based and Alternative Protein Ingredients

- 4.2.4 Rise in the adoption of nano-spray drying for nutraceutical micro-encapsulation

- 4.2.5 Strong Growth in the Dairy Industry

- 4.2.6 Advancements in multi-stage dryers

- 4.3 Market Restraints

- 4.3.1 Growing demand for cost-effective drying technologies

- 4.3.2 Stringent Volatile Organic Compound (VOC) and particulate emission norms

- 4.3.3 Risk of degradation in heat-sensitive ingredients during drying

- 4.3.4 Skill-gap in operating advanced multi-stage dryers in developing markets

- 4.4 Supply Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Drying Stage

- 5.1.1 Single-Stage

- 5.1.2 Two-Stage

- 5.1.3 Multi-Stage

- 5.2 By Process

- 5.2.1 Rotary Wheel (Pressure Nozzle)

- 5.2.2 Pneumatic Two-Fluid Nozzle

- 5.2.3 Centrifugal/Spin-Disc

- 5.2.4 Fluidized Spray Dryer

- 5.2.5 Closed-Loop (Inert Gas)

- 5.3 By Application

- 5.3.1 Dairy Products

- 5.3.2 Infant Formula

- 5.3.3 Functional and Plant-based Foods

- 5.3.4 Pharmaceuticals

- 5.3.5 Dietary Supplements

- 5.3.6 Others

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.1.4 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 United Kingdom

- 5.4.2.2 Germany

- 5.4.2.3 Spain

- 5.4.2.4 France

- 5.4.2.5 Italy

- 5.4.2.6 Netherlands

- 5.4.2.7 Sweden

- 5.4.2.8 Poland

- 5.4.2.9 Belgium

- 5.4.2.10 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Indonesia

- 5.4.3.7 Thailand

- 5.4.3.8 Singapore

- 5.4.3.9 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Chile

- 5.4.4.4 Colombia

- 5.4.4.5 Peru

- 5.4.4.6 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 United Arab Emirates

- 5.4.5.4 Nigeria

- 5.4.5.5 Morocco

- 5.4.5.6 Egypt

- 5.4.5.7 Turkey

- 5.4.5.8 Rest of Middle East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Ranking Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials (if available), Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 GEA Group AG

- 6.4.2 ITT Inc (SPX FLOW)

- 6.4.3 Antolab Group Co., Ltd.

- 6.4.4 ANDRITZ GROUP

- 6.4.5 SiccaDania Group

- 6.4.6 The Tetra Laval Group

- 6.4.7 Changzhou Jinqiao Spray Drying and Engineering Co., Ltd.

- 6.4.8 Pulse Drying Systems

- 6.4.9 Buchiglas (Buchi AG)

- 6.4.10 Moret Industries

- 6.4.11 SSP Pvt Limited

- 6.4.12 Yamato Scientific Co Ltd

- 6.4.13 G. Larsson Starch Technology AB

- 6.4.14 THORNICO A/S

- 6.4.15 Col-Int Tech

- 6.4.16 AKSH Engineering Systems (P) Limited

- 6.4.17 DORST Technologies GmbH & Co. KG

- 6.4.18 Sinitech Industries d.o.o.

- 6.4.19 Mojj Engineering Systems ltd.

- 6.4.20 Kerone Engineering Solutions LTD.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

噴霧乾燥機市場規模、佔有率和成長分析:按產品類型、乾燥階段、最終用途產業和地區分類-2026-2033年產業預測

噴霧乾燥機市場規模、佔有率和成長分析:按產品類型、乾燥階段、最終用途產業和地區分類-2026-2033年產業預測 塗料乾燥劑市場:按技術、塗料類型、應用和最終用途產業分類-2026-2032年全球市場預測

塗料乾燥劑市場:按技術、塗料類型、應用和最終用途產業分類-2026-2032年全球市場預測 2026年全球噴霧乾燥設備市場報告

2026年全球噴霧乾燥設備市場報告 全球藥品噴霧乾燥市場:依產品類型、乾燥方法、應用、最終用戶、國家及地區分類-產業分析、市場規模、佔有率及未來預測(2025-2032年)

全球藥品噴霧乾燥市場:依產品類型、乾燥方法、應用、最終用戶、國家及地區分類-產業分析、市場規模、佔有率及未來預測(2025-2032年) 藥物噴霧乾燥:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

藥物噴霧乾燥:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 噴霧乾燥設備市場-全球產業規模、佔有率、趨勢、機會和預測,按類型、按乾燥階段、按流程類型、按應用、按地區和競爭情況細分,2020-2030 年

噴霧乾燥設備市場-全球產業規模、佔有率、趨勢、機會和預測,按類型、按乾燥階段、按流程類型、按應用、按地區和競爭情況細分,2020-2030 年