|

市場調查報告書

商品編碼

2061557

印度汽車用玻璃纖維複合材料:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)India Automotive Glass Fiber Composites - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

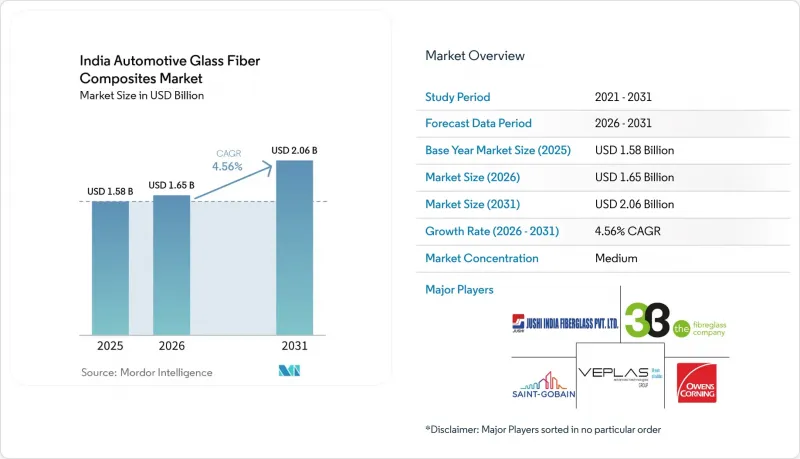

根據 Mordor Intelligence 預測,印度汽車玻璃纖維複合材料市場規模將從 2025 年的 15.8 億美元和 2026 年的 16.5 億美元成長到 2031 年的 20.6 億美元,2026 年至 2031 年的複合年成長率為 4.56%。

本報告按中間材料類型(短纖維熱塑性塑膠 (SFT)、長纖維熱塑性塑膠 (LFT)、連續纖維熱塑性塑膠 (CFT) 及其他中間材料)和應用類型(內飾、外飾、結構組件、動力傳動系統部件及其他應用)進行細分。市場規模和預測以美元計價。

印度汽車玻璃纖維複合材料市場趨勢與洞察

FAME-II獎勵推動電動車產量增加

到2025年,FAME-II補貼計畫將支持161萬輛電動車的銷售,其後續計畫PM E-DRIVE的資金支持將持續到2028年。由於電池式電動車的重量約為內燃機汽車的1.5倍,汽車製造商(OEM)正在採用玻璃纖維電池外殼和底盤護板來抵消增加的重量。塔塔汽車、現代和鈴木都在其下一代平台中使用玻璃纖維零件,這表明複合材料有助於提高續航里程,同時又不影響價格競爭力。一級供應商正在積極回應,在電動車生產基地附近設立短週期成型生產線,以減少物流時間和成本。隨著電氣化在全國範圍內的擴展,輕質複合材料正變得必不可少,而非可有可無。

玻璃纖維和碳纖維的成本績效優勢。

玻璃纖維佔汽車複合材料總量的近92%,因為它在製造過程中能耗僅為原生碳纖維的十分之一,卻能達到350兆帕的抗張強度。由於碳纖維的高成本難以被售價低於1.5萬美元的量產車所接受,玻璃纖維增強塑膠成為車身外板、座椅結構和電池蓋等部件的現實選擇。 Trinseo和CSP公司推出的長纖維玻璃纖維產品,與鋼材相比,可將機殼重量減輕25%以上,這顯示在維持性能標準的同時,還能兼顧成本優勢。隨著日益嚴格的CAFE(企業平均燃油經濟性)法規的實施,玻璃纖維憑藉其強度、價格和永續性的完美平衡,繼續保持領先地位。

熱固性樹脂的回收及使用後所面臨的挑戰

雖然傳統的熱解方法幾乎可以完全去除樹脂,但回收的玻璃纖維強度會降低高達50%,使其只能用作低價值填充材。化學處理方法雖然能保留更多性能,但仍處於中試階段,且成本高。因此,印度82家註冊的汽車拆解廠難以從熱固性廢料中提取價值,這也使得原始設備製造商(OEM)對採用環氧樹脂和聚酯零件猶豫不決。此外,由於缺乏回收纖維的標準化測試和數位化認證,一級供應商對保固責任存在擔憂,這進一步阻礙了熱固性玻璃纖維複合材料的市場滲透。

細分市場分析

2025年,短纖維熱塑性塑膠佔印度汽車玻璃纖維複合材料市場52.38%的佔有率。這反映了射出成型在門板模組、儀錶面板和非載荷外飾複合材料的短週期生產方面的經濟優勢。預計在預測期(2026-2031年)內,長纖維熱塑性塑膠將以5.84%的複合年成長率成長,因為原始設備製造商(OEM)將採用長纖維熱塑性塑膠用於電池外殼、橫樑和底盤護板等需要更高剛度重量比的零件。連續纖維帶目前仍處於小眾市場,但隨著果阿邦一條新的鈽基生產線的運作以及針對氫燃料電池雙極板的研究,其市場發展勢頭強勁。在印度汽車玻璃纖維複合材料市場,隨著一級供應商推進多材料結構的檢驗(這些結構可將零件數量減少高達40%),長纖維(LFT)零件的市場規模預計將穩定成長。雖然短纖維 (SFT) 在產量方面仍將保持優勢,但隨著電動車產量的擴大,長纖維 (LFT) 在結構組件中的佔有率可能會增加。

Lochling 的金屬-塑膠混合橫樑相比鋼材減重 40%,同時整合了安裝點,充分展現了輕質複合材料 (LFT) 如何降低組裝複雜性。朗盛 (LANXESS) 的 Tepex 板材,將連續玻璃纖維層與聚丙烯芯材結合,為 SUV 底盤護板提供卓越的抗碎石衝擊性能。 Martti Suzuki 的輕量化舉措已使其小型車平台減重 80 公斤,表明分階段使用複合材料有助於提高燃油效率 3-4%。隨著本地加工商擴大採用超過 4000 kN 的壓縮和射出成型材料 (LFT) 和混合層壓板將進一步滲透到半結構件領域。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場促進因素

- FAME-II獎勵推動電動車產量增加

- 玻璃纖維與碳纖維成本績效比較

- 擴大國內一級和二級製造商的模塑產能

- PLI-ACC計劃正在促進對高強度熱塑性塑膠的需求。

- 向可回收熱塑性複合材料過渡,為生產者延伸責任制(EPR)做準備

- 市場限制因素

- 熱固性樹脂回收再利用的挑戰

- 粗紗和PA樹脂供不應求。

- 缺乏OEM複合材料設計的技術基礎

- 價值鏈分析

- 波特五力模型

第5章 市場規模與成長預測

- 中間類型

- 短纖維熱塑性塑膠(SFT)

- 長纖維增強熱塑性塑膠(LFT)

- 連續纖維熱塑性樹脂(CFT)

- 其他中間類型

- 按應用程式類型

- 內部的

- 外部的

- 結構組裝

- 動力傳動系統部件

- 其他應用程式類型

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- 3B-the fibreglass company

- Avient

- Hexcel Corporation

- Jushi India Fiberglass Pvt. Ltd.

- Nippon Electric Glass Co., Ltd.

- Owens Corning

- SAERTEX GmbH & Co.KG

- Saint-Gobain India

- Veplas dd

第7章 市場機會與未來展望

According to Mordor Intelligence, the india automotive glass fiber composites market size is projected to expand from USD 1.58 billion in 2025 and USD 1.65 billion in 2026 to USD 2.06 billion by 2031, registering a CAGR of 4.56% between 2026 to 2031.

This report is Segmented by Intermediate Type (Short Fiber Thermoplastic (SFT), Long Fiber Thermoplastic (LFT), Continuous Fiber Thermoplastic (CFT), and Other Intermediate Types), Application Type (Interior, Exterior, Structural Assembly, Power-Train Components, and Other Application Types). The Market Sizes and Forecasts are Provided in Terms of Value (USD).

India Automotive Glass Fiber Composites Market Trends and Insights

Rising EV Production Under FAME-II Incentives

FAME-II subsidies supported 1.61 million electric vehicles through 2025, and the successor PM E-DRIVE program will extend funding to 2028. Battery-electric cars weigh roughly 1.5 times their ICE peers, so OEMs rely on glass-fiber battery enclosures and underbody shields to offset the added mass. Tata Motors, Hyundai, and Suzuki have each adopted glass-fiber parts in next-generation platforms, demonstrating that composites help protect range without eroding price competitiveness. Tier-1 suppliers are responding with rapid-cycle moulding lines near EV hubs, trimming logistics time and cost. As electrification scales nationwide, lightweight composites become integral rather than optional.

Cost-Performance Edge of Glass vs. Carbon Fiber

Glass fiber represents close to 92% of automotive composite volume because it provides 350 MPa tensile strength at one-tenth the embodied energy of virgin carbon fiber. Mass-market vehicles priced below USD 15,000 cannot absorb carbon-fiber premiums, making glass-fiber-reinforced polymers the pragmatic choice for exterior panels, seat structures, and battery covers. Trinseo and CSP have launched long-fiber grades that cut enclosure weight by more than 25% versus steel, proving that performance thresholds can be met at competitive cost. As CAFE limits tighten, the balance of strength, price, and sustainability keeps glass ahead of rival materials.

Recycling and End-of-Life Hurdles for Thermosets

Conventional pyrolysis removes nearly all resin, but cuts recovered glass-fiber strength by up to 50%, confining reuse to low-value fillers. Chemical routes retain more properties but remain pilot-scale and costly. India's 82 Registered Vehicle Scrapping Facilities, therefore, struggle to capture value from thermoset scrap, discouraging OEMs from specifying epoxy or polyester parts. Without standardized testing or digital passports for recovered fiber, tier suppliers fear warranty liabilities, slowing market penetration of thermoset glass-fiber composites.

Other drivers and restraints analyzed in the detailed report include:

- Domestic Tier-1/2 Moulding Capacity Expansion

- PLI-ACC Scheme Boosting High-Strength Thermoplastics

- Intermittent Roving and PA Resin Shortages

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, Short Fiber Thermoplastic accounted for 52.38% of the India Automotive Glass Fiber composites market, reflecting the fast-cycle economics of injection moulding for door modules, instrument panels, and non-load-bearing exterior trims. Long Fiber Thermoplastic is set to grow at 5.84% CAGR during the forecast period (2026-2031) as OEMs adopt it for battery enclosures, cross-car beams, and underbody shields that demand higher stiffness-to-weight ratios. Continuous-fiber tapes remain niche but are gaining momentum through new pultrusion lines in Goa and research partnerships aimed at hydrogen fuel-cell bipolar plates. The India Automotive Glass Fiber Composites market size for LFT components is projected to expand steadily as Tier-1 suppliers validate multi-material architectures with up to 40% part-count reduction. SFT will keep its volume edge, but LFT's share of structural assemblies will climb in tandem with EV production.

Rochling's hybrid metal-plastic cross-car beam cuts weight 40% versus steel while integrating attachment points, showing how LFT reduces assembly complexity. LANXESS Tepex sheets combine continuous glass layers with polypropylene cores to deliver gravel-impact resistance for SUV underbody shields. Maruti Suzuki's lightweight initiative already removed 80 kilograms from a small-car platform, proving that incremental composite substitution contributes 3-4% fuel-economy gains. As local converters scale compression and injection presses beyond 4,000 kN, LFT and hybrid laminates will move deeper into semi-structural domains.

List of Companies Covered in this Report:

- 3B - the fibreglass company

- Avient

- Hexcel Corporation

- Jushi India Fiberglass Pvt. Ltd.

- Nippon Electric Glass Co., Ltd.

- Owens Corning

- SAERTEX GmbH & Co.KG

- Saint-Gobain India

- Veplas d.d.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Drivers

- 4.1.1 Rising EV production under FAME-II incentives

- 4.1.2 Cost-performance edge of glass vs. carbon fibre

- 4.1.3 Domestic Tier-1/2 moulding capacity expansion

- 4.1.4 PLI-ACC scheme spurring demand for high-strength thermoplastics

- 4.1.5 Shift to recyclable thermoplastic composites for EPR readiness

- 4.2 Market Restraints

- 4.2.1 Recycling and end-of-life hurdles for thermosets

- 4.2.2 Intermittent roving and PA resin supply shortages

- 4.2.3 Limited OEM design-for-composite skill base

- 4.3 Value Chain Analysis

- 4.4 Porter's Five Forces

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitutes

- 4.4.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Intermediate Type

- 5.1.1 Short Fiber Thermoplastic (SFT)

- 5.1.2 Long Fiber Thermoplastic (LFT)

- 5.1.3 Continuous Fiber Thermoplastic (CFT)

- 5.1.4 Other Intermediate Types

- 5.2 By Application Type

- 5.2.1 Interior

- 5.2.2 Exterior

- 5.2.3 Structural Assembly

- 5.2.4 Power-train Components

- 5.2.5 Other Application Types

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 3B - the fibreglass company

- 6.4.2 Avient

- 6.4.3 Hexcel Corporation

- 6.4.4 Jushi India Fiberglass Pvt. Ltd.

- 6.4.5 Nippon Electric Glass Co., Ltd.

- 6.4.6 Owens Corning

- 6.4.7 SAERTEX GmbH & Co.KG

- 6.4.8 Saint-Gobain India

- 6.4.9 Veplas d.d.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

中東和非洲汽車用玻璃纖維複合材料:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)

中東和非洲汽車用玻璃纖維複合材料:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年) 汽車玻璃纖維複合材料市場:按樹脂類型、纖維類型、製造流程、應用和車輛類型分類-2026-2032年全球預測

汽車玻璃纖維複合材料市場:按樹脂類型、纖維類型、製造流程、應用和車輛類型分類-2026-2032年全球預測 全球 GFRG(玻璃纖維增強石膏)市場規模研究與預測,按應用、形式、最終用途領域、關鍵特性、纖維類型和區域預測 2025-2035

全球 GFRG(玻璃纖維增強石膏)市場規模研究與預測,按應用、形式、最終用途領域、關鍵特性、纖維類型和區域預測 2025-2035 汽車玻璃纖維複合材料市場,按複合材料類型、按製造程序、按纖維類型、按樹脂類型、按最終用戶、按國家/地區分類 - 2025 年至 2032 年全球行業分析、市場規模、市場佔有率及預測

汽車玻璃纖維複合材料市場,按複合材料類型、按製造程序、按纖維類型、按樹脂類型、按最終用戶、按國家/地區分類 - 2025 年至 2032 年全球行業分析、市場規模、市場佔有率及預測 汽車玻璃纖維複合材料市場-全球產業規模、佔有率、趨勢、機會和預測(按類型、應用、地區和競爭細分,2020-2030 年)

汽車玻璃纖維複合材料市場-全球產業規模、佔有率、趨勢、機會和預測(按類型、應用、地區和競爭細分,2020-2030 年) 汽車玻璃纖維複合材料市場:2024-2031年全球產業分析、規模、佔有率、成長、趨勢、預測

汽車玻璃纖維複合材料市場:2024-2031年全球產業分析、規模、佔有率、成長、趨勢、預測