|

市場調查報告書

商品編碼

2043832

中東和非洲汽車用玻璃纖維複合材料:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)Africa And Middle-East Automotive Glass Fiber Composites - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

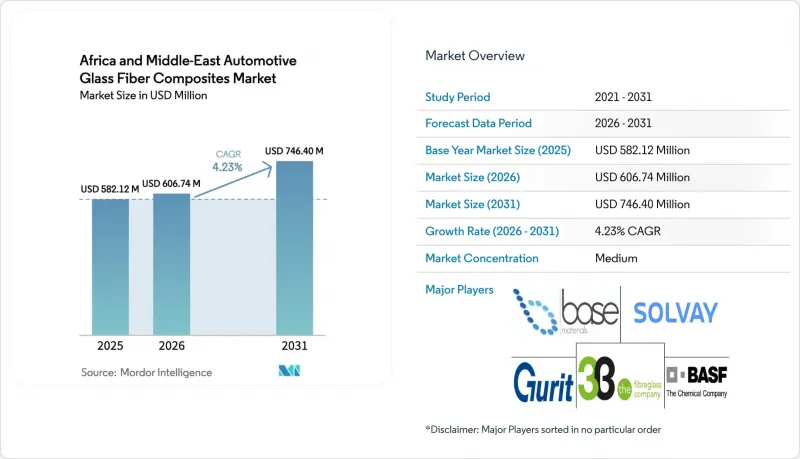

預計到 2025 年,中東和非洲汽車玻璃纖維複合材料市場規模將達到 5.8212 億美元,到 2026 年將達到 6.0674 億美元,到 2031 年將達到 7.464 億美元,2026 年至 2031 年的複合年成長率為 4.23%。

除了海灣國家向下游加工領域轉變的政策外,非洲主要組裝廠強制推行國內採購政策,也推動了投資從基礎碳氫化合物出口轉向高附加價值複合材料模塑。沙烏地阿拉伯於2026年2月透過其公共投資基金向CEER供應商注資9.87億美元,清晰地展現了這一轉變,該項目旨在支持玻璃纖維門模組和電池托盤模具的生產。海灣合作理事會的輕量化法規和阿拉伯聯合大公國的稅收優惠降低了歐洲模塑製造商的進入門檻,但跨越紅海的物流挑戰仍然推高了進口粗紗的成本。非洲的CKD(全組裝組裝)工廠正在從壓製鋼板轉向手工鋪層複合材料,以滿足本地化要求,但南非和埃及熟練技術人員的短缺導致ISO 527拉伸試驗出現品質不合格的情況。

中東和非洲汽車玻璃纖維複合材料市場的趨勢和洞察。

推廣旨在減輕車身重量以提高燃油效率的法規

沙烏地阿拉伯的SASO 2864:2019標準規定,到2028年,車輛的燃油消耗量必須達到5.8公升/百公里,這迫使汽車製造商透過材料替代,將每輛車的重量減輕80-120公斤。與低碳鋼相比,玻璃纖維面板可減輕25-30%的重量,並且在成本上與碳纖維面板相比也具有競爭力。阿拉伯聯合大公國計劃於2026年1月實施歐6B排放標準,並於2030年過渡到歐6D排放標準,這將增加掩埋材料的採用,但由於熱固性玻璃纖維無法重熔,報廢產品的回收仍面臨挑戰,這可能導致2028年後增加垃圾掩埋成本。

向電池驅動動力傳動系統的轉變增加了對電動車機殼用玻璃纖維的需求。

SGL Carbon為BMWiX開發的玻璃纖維電池外殼比鋁製外殼輕15%。 CEER的轎車原型車也採用了類似的方法,使用玻璃纖維下托盤來支撐重達600公斤的電池。樹脂轉注成形(RTM)製程為預算有限的非洲工廠提供了顯著優勢,因為它無需像鋁壓平機那樣進行大規模的資本投資即可製造複雜形狀的零件。埃及的格雷切博士計劃於2026年第四季投資1,620萬美元開設一條注塑成型生產線,用於生產電動車的底盤護板。這表明傳統玻璃加工企業和複合材料零件製造商之間的界限正在變得模糊。

由於紅海運費上漲,玻璃纖維進口價格出現波動

2024年胡塞武裝的攻擊導致28%的亞洲至歐洲貨物經由好望角轉運,運費上漲150%至200%。這使得埃及和肯亞缺乏對沖手段的模具製造商從中國和印度粗紗的成本增加了12%至18%。即使衝突平息後,保險公司仍繼續在保費中加收8%至10%的附加費,預計這種情況將持續到2027年。這將使中東和非洲的汽車玻璃纖維複合材料市場面臨結構性波動。

細分市場分析

至2025年,壓縮成型將佔銷售額的34.28%,並持續維持中東和非洲汽車玻璃纖維複合材料市場的主要生產方式。 Advanced Fibreform公司的12台壓平機每週為豐田和五十鈴皮卡生產3,000多個零件。受電動車電池托盤和底盤護板等複雜、無氣泡層壓板需求的推動,真空灌注成型預計到2031年將以4.47%的複合年成長率成長。 Johns Manville公司正在投資5,500萬美元擴大其位於俄亥俄州的生產線以滿足此需求,產品將供應給海灣合作理事會(GCC)成員國的進口商。

在阿爾及利亞、埃及和肯亞,對於產量低於15,000件的CKD(全散件組裝)產品,手工積層仍被廣泛應用,為滿足在地採購法規提供了一種經濟高效的解決方案。樹脂轉注成形則用於製造一些對纖維結構要求極高的特殊結構件,例如座椅框架。射出成型成型的短纖維複合材料則用於大量生產的內裝支架。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 推廣旨在減輕車身重量以提高燃油效率的法規

- 向電池電動動力傳動系統的轉變增加了對電動車機殼用玻璃纖維的需求。

- 沙烏地阿拉伯和阿拉伯聯合大公國一級供應鏈的在地化獎勵

- 沙漠氣候下對耐腐蝕複合材料的需求增加(車輛和巴士)

- 在整個非洲,CKD/IKD組裝蓬勃發展,採用低資本支出(CAPEX)的手工組裝模製零件。

- 市場限制因素

- 由於紅海運費溢價,玻璃纖維進口價格出現波動

- 該地區二級樹脂混煉生產商數量有限,導致複合材料成本上升。

- 合格複合材料技術人員短缺導致原始設備製造商 (OEM) 的產品出現品質不合格情況。

- 價值鏈分析

- 波特五力模型

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章 市場規模與成長預測

- 依產品類型

- 壓縮成型

- 手工積層

- 樹脂轉注成形

- 真空灌注成型

- 射出成型

- 透過使用

- 外部的

- 結構組裝

- 動力傳動系統部件

- 內部的

- 其他用途

- 按地區

- 南非

- 埃及

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 其他中東和非洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- 3B-the fibreglass company

- Base Materials Ltd.

- BASF

- BorgWarner

- Chongqing Polycomp International Corporation(CPIC)

- Far-UK

- General Motors Company

- Gurit Holding AG

- Hexcel Corporation

- Johns Manville

- LyondellBasell

- Nippon Electric Glass

- Praana Group

- Saint-Gobain Vetrotex

- SGL Carbon

- Solvay

- Taishan Fiberglass

- Teijin Limited

第7章 市場機會與未來展望

The Africa And Middle-East Automotive Glass Fiber Composites Market size is projected to be USD 582.12 million in 2025, USD 606.74 million in 2026, and reach USD 746.40 million by 2031, growing at a CAGR of 4.23% from 2026 to 2031. A shift in policy toward downstream processing in the Gulf, coupled with domestic-content mandates in key African assembly hubs, is driving investment away from basic hydrocarbon exports toward value-added composite molding. Saudi Arabia's allocation of USD 987 million from the Public Investment Fund to CEER suppliers in February 2026 highlights this transition, as the program supports tooling for glass-fiber door modules and battery trays. GCC lightweighting regulations and UAE tax incentives are reducing entry barriers for European molders, although logistical challenges through the Red Sea continue to increase the cost of imported roving. African CKD plants are replacing stamped steel with hand-laid composites to meet localization requirements, despite technician shortages in South Africa and Egypt leading to quality rejections under ISO 527 tensile tests.

Africa And Middle-East Automotive Glass Fiber Composites Market Trends and Insights

Regulatory Push for Fuel-Efficient Lightweighting

Saudi Arabia's SASO 2864:2019 standard lowers fleet consumption to 5.8 L/100 km by 2028, forcing automakers to remove 80-120 kg per vehicle through material substitution. Glass-fiber panels deliver 25-30% weight savings versus mild steel and remain cost-competitive against carbon fiber. The UAE starts EURO 6B in January 2026 and moves to EURO 6D by 2030, increasing pressure on OEMs to amortize lightweight components across GCC runs. While the rules accelerate composite uptake, end-of-life recycling gaps persist because thermoset glass fiber cannot be remelted, raising the prospect of landfill surcharges after 2028.

Shift to Battery-Electric Powertrains Raises Glass-Fiber Demand for EV Enclosures

SGL Carbon's glass-fiber battery enclosure for BMW's iX trims pack weight by 15% compared with aluminum housing. CEER's prototype sedan mirrors this approach with a glass-fiber lower tray that offsets its 600 kg battery. Resin-transfer molding offers complex geometries without the capital intensity of aluminum presses, a key benefit for African plants with tight budgets. Egypt's Dr. Greiche will open a USD 16.2 million infusion line in Q4 2026 to supply EV underbody shields, underscoring the cross-over between traditional glazing firms and composite components.

Volatile Glass-Fiber Import Prices Due to Red Sea Freight Premiums

Houthi attacks in 2024 caused 28% of Asia-to-Europe cargo to be rerouted via the Cape of Good Hope, leading to a 150-200% increase in freight rates. This raised the landed cost of Chinese and Indian rovings by 12-18% for Egyptian and Kenyan molders without hedging tools. Even after the conflict subsides, insurers have added an 8-10% surcharge to premiums, expected to remain through 2027, embedding structural volatility into the Africa and Middle-East automotive glass fiber composites market.

Other drivers and restraints analyzed in the detailed report include:

- Localisation Incentives in Saudi and UAE Tier-1 Supply Chains

- Surge in CKD/IKD Assembly Plants Across Africa Adopting Low-CAPEX Hand Lay-Up Parts

- Shortage of Certified Composite Technicians Causing OEM Quality Rejections

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Compression molding accounted for 34.28% of revenue in 2025, remaining a key production method in the Africa and Middle-East automotive glass fiber composites market. Advanced Fibreform's 12 presses produce over 3,000 parts weekly for Toyota and Isuzu pickups. Vacuum infusion processing is projected to grow at a 4.47% CAGR through 2031, driven by demand for complex, void-free laminates in EV battery trays and underbody shields. Johns Manville's USD 55 million Ohio line expansion aims to meet this demand, with output designated for GCC importers.

Hand lay-up continues to be utilized in CKD operations producing fewer than 15,000 units, offering a cost-effective solution to meet local-content regulations in Algeria, Egypt, and Kenya. Resin-transfer molding is used for niche structural components like seat frames, where fiber architecture is critical. Injection-molded short-fiber compounds are employed for high-volume interior brackets.

The Africa and Middle-East Automotive Glass Fiber Composites Market Report is Segmented by Production Type (Compression Molding, Hand Lay-Up, and More), Application Type (Exterior, Structural Assembly, Powertrain Components, Interior, and Other Application Types), and Geography (South Africa, Egypt, United Arab Emirates, Saudi Arabia, and Rest of Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- 3B - the fibreglass company

- Base Materials Ltd.

- BASF

- BorgWarner

- Chongqing Polycomp International Corporation (CPIC)

- Far-UK

- General Motors Company

- Gurit Holding AG

- Hexcel Corporation

- Johns Manville

- LyondellBasell

- Nippon Electric Glass

- Praana Group

- Saint-Gobain Vetrotex

- SGL Carbon

- Solvay

- Taishan Fiberglass

- Teijin Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Regulatory push for fuel-efficient lightweighting

- 4.2.2 Shift to battery-electric powertrains raises glass-fiber demand for EV enclosures

- 4.2.3 Localisation incentives in Saudi and UAE Tier-1 supply chains

- 4.2.4 Growing demand for corrosion-resistant composites in desert climates (fleets/buses)

- 4.2.5 Surge in CKD/IKD assembly plants across Africa adopting low-CAPEX hand lay-up parts

- 4.3 Market Restraints

- 4.3.1 Volatile glass-fiber import prices due to Red Sea freight premiums

- 4.3.2 Limited regional Tier-2 resin formulators inflating composite costs

- 4.3.3 Shortage of certified composite technicians causing OEM quality rejections

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Consumers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Production Type

- 5.1.1 Compression Molding

- 5.1.2 Hand Lay-up

- 5.1.3 Resin Transfer Molding

- 5.1.4 Vacuum Infusion Processing

- 5.1.5 Injection Molding

- 5.2 By Application Type

- 5.2.1 Exterior

- 5.2.2 Structural Assembly

- 5.2.3 Powertrain Components

- 5.2.4 Interior

- 5.2.5 Other Application Types

- 5.3 By Geography

- 5.3.1 South Africa

- 5.3.2 Egypt

- 5.3.3 United Arab Emirates

- 5.3.4 Saudi Arabia

- 5.3.5 Rest of Middle-East and Africa

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 3B - the fibreglass company

- 6.4.2 Base Materials Ltd.

- 6.4.3 BASF

- 6.4.4 BorgWarner

- 6.4.5 Chongqing Polycomp International Corporation (CPIC)

- 6.4.6 Far-UK

- 6.4.7 General Motors Company

- 6.4.8 Gurit Holding AG

- 6.4.9 Hexcel Corporation

- 6.4.10 Johns Manville

- 6.4.11 LyondellBasell

- 6.4.12 Nippon Electric Glass

- 6.4.13 Praana Group

- 6.4.14 Saint-Gobain Vetrotex

- 6.4.15 SGL Carbon

- 6.4.16 Solvay

- 6.4.17 Taishan Fiberglass

- 6.4.18 Teijin Limited

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

印度汽車用玻璃纖維複合材料:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

印度汽車用玻璃纖維複合材料:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031) 汽車玻璃纖維複合材料市場:按樹脂類型、纖維類型、製造流程、應用和車輛類型分類-2026-2032年全球預測

汽車玻璃纖維複合材料市場:按樹脂類型、纖維類型、製造流程、應用和車輛類型分類-2026-2032年全球預測 全球 GFRG(玻璃纖維增強石膏)市場規模研究與預測,按應用、形式、最終用途領域、關鍵特性、纖維類型和區域預測 2025-2035

全球 GFRG(玻璃纖維增強石膏)市場規模研究與預測,按應用、形式、最終用途領域、關鍵特性、纖維類型和區域預測 2025-2035 汽車玻璃纖維複合材料市場,按複合材料類型、按製造程序、按纖維類型、按樹脂類型、按最終用戶、按國家/地區分類 - 2025 年至 2032 年全球行業分析、市場規模、市場佔有率及預測

汽車玻璃纖維複合材料市場,按複合材料類型、按製造程序、按纖維類型、按樹脂類型、按最終用戶、按國家/地區分類 - 2025 年至 2032 年全球行業分析、市場規模、市場佔有率及預測 汽車玻璃纖維複合材料市場-全球產業規模、佔有率、趨勢、機會和預測(按類型、應用、地區和競爭細分,2020-2030 年)

汽車玻璃纖維複合材料市場-全球產業規模、佔有率、趨勢、機會和預測(按類型、應用、地區和競爭細分,2020-2030 年) 汽車玻璃纖維複合材料市場:2024-2031年全球產業分析、規模、佔有率、成長、趨勢、預測

汽車玻璃纖維複合材料市場:2024-2031年全球產業分析、規模、佔有率、成長、趨勢、預測