|

市場調查報告書

商品編碼

2061539

聚合物電解質膜燃料電池(PEMFC):市場佔有率分析、產業趨勢和統計數據以及成長預測(2026-2031)Polymer Electrolyte Membrane Fuel Cells (PEMFC) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

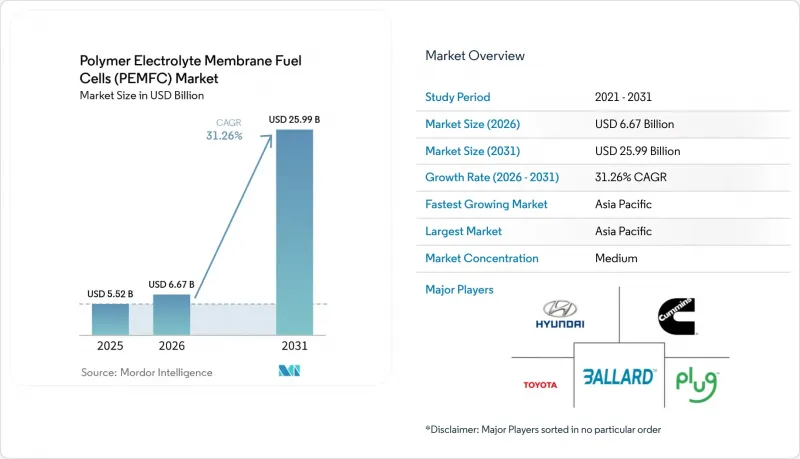

根據 Mordor Intelligence 估計,2026 年聚合物電解質膜燃料電池 (PEMFC) 市場規模為 66.7 億美元,預計到 2031 年將達到 259.9 億美元,在預測期(2026-2031 年)內複合年成長率為 31.26%。

本報告按類型(低溫和高溫)、冷卻方式(空冷和液冷)、功率輸出(10-100kW、100kW 以上及其他)、組件(膜電極組件、催化劑及其他)、應用(交通運輸及其他)、終端用戶行業(交通運輸、公共產業及其他)和地區(歐洲、亞太地區及其他)進行分類。

全球聚合物電解質膜燃料電池(PEMFC)市場趨勢與洞察

政府零排放法規和補貼

目前,相關法規強制要求逐步淘汰港口、物流走廊和市政車隊中的柴油車輛。加州將於2024年生效的法規要求所有新型短程運輸卡車必須實現零排放,而歐盟修訂後的重型車輛二氧化碳排放標準旨在到2040年減排90%,這將加速燃料電池和電池在長途運輸領域的應用。中國已將新能源汽車補貼延長至2025年,撥款37億元人民幣用於商用燃料電池電動車,並在省級層級提供類似支援。韓國的藍圖計劃在2030年資助85萬輛燃料電池電動車和1,200座加氫站的建設。這些協調一致的政策確保了市場需求的確定性,從而為大規模燃料電池堆生產和供應網路的私人投資提供了基礎。

由於超級工廠規模化生產,PEM堆疊成本迅速下降。

Plug Power位於羅徹斯特的1GW超級工廠計劃於2025年底運作,該公司透過將MEA塗層、板材壓制和最終檢驗流程整合到同一地點,降低了35%的成本。現代汽車廣州工廠的目標是透過自動化單元佈局,到2027年將電堆成本降至每千瓦50美元,而博世則利用汽車行業的公差,將缺陷率控制在2%以下。美國能源局(DOE)的藍圖也支持這項進展,該路線圖預測到2024年電堆成本將達到每千瓦60美元,比原計畫提前一年實現。成本的降低將開拓一些利基市場,例如對價格敏感的物料輸送和通訊備份領域,這些領域先前一直由柴油引擎主導。

鉑族金屬的高成本風險

預計到2025年,鉑金價格平均將達到每盎司1,050美元,將使80kW汽車電堆的催化劑成本上升至約1,000美元。回收有助於降低成本。豐田的閉合迴路計畫可從廢棄模組中回收95%的鉑金,每年減少12,000盎司的新增需求。然而,據巴拉德公司稱,除非將成本轉嫁給消費者,否則鉑金價格每上漲10%,毛利率將下降2.5個百分點。鐵基、氮基和碳基催化劑的研究佔鉑金相關研究活動的60%,但由於這些催化劑耐久性不足,預計它們至少在預測期中期之前仍將對鉑金價格產生影響。

細分市場分析

儘管低溫裝置在2025年佔銷售額的73.5%,但預計到2031年,高溫堆的年成長率將達到35.8%。工業運營商優先選擇120°C至180°C的運作溫度,因為可以將廢熱回收利用到製程負荷中,從而降低工廠預算(輔助設備)支出25%。 Serenergy公司於2025年在丹麥一處多用戶住宅安裝的一套5kW系統,透過將廢熱導向散熱器,實現了90%的整體效率。由於低溫設計具有快速冷啟動和4kW/L的功率密度,因此仍然是車輛的標準配備。然而,隨著磷酸Polybenzimidazole膜的使用壽命達到10,000小時,且密度差異不斷縮小,在純氫稀缺的地區,高溫設計的應用可能會擴大。

預計到2025年,水冷式電池堆的出貨量將佔總出貨量的70.1%,並將以32.5%的複合年成長率持續成長,在輸出功率超過30kW時,水冷式電池堆至關重要。透過使用去離子水或乙二醇循環系統將電池溫度維持在65°C至75°C的最佳範圍內,即使因散熱器導致重量增加15%,也能達到4kW/L的功率密度。 Horizon於2025年推出的混合冷卻系統,透過在空氣冷卻和液體冷卻之間切換,可將寄生功耗降低8%。船舶應用凸顯了液體冷卻的重要性。 Waltzila公司的1.2MW船舶模組可將600kW的熱量散發到海水中,僅靠空氣冷卻是無法實現的。同時,在通訊和堆高機等應用中,由於這些應用更注重簡易性而非峰值輸出,因此風冷式電池組仍發揮重要作用。

區域分析

2025年,亞太地區將佔據聚合物電解質膜燃料電池(PEMFC)市場47.6%的佔有率,預計到2031年,年均成長率將達到33.1%。在中國,已建成428座加氫站,廣東、山東和河北三省對卡車購置成本提供40%的補助。日本已將「EneFarm」補貼計畫延長至2027年,目標是2030年為530萬戶家庭安裝加氫設備。韓國已資助生產85萬輛燃料電池電動車(FCEV)並建造1,200座加氫站,而印度的「國家氫能計畫」規定,到2027年,煉油廠生產的氫氣中必須有10%為綠色氫氣。澳洲則專注於氨出口,除採礦機械外,國內對氫的應用有限。

預計2027年,歐洲核心氫能基礎設施管線網路將改造28,000公里,與卡車運輸相比,氫氣運輸成本將降低30%。德國已撥款90億歐元用於獎勵電解和重型卡車的建設;法國的目標是到2030年實現6.5吉瓦的電解產能;英國則專注於HyNet計畫。北歐水電正在支持低碳氫的出口合約。根據RED III指令,政策協調要求到2030年,42%的工業氫必須來自可再生,這將鞏固未來的需求。

北美正受惠於一項價值80億美元的聯邦樞紐計畫。墨西哥灣沿岸地區樞紐的目標是為煉油廠生產1.2吉瓦的藍氫,而加州的燃油排放法規正在提振卡車運輸的需求。加拿大貝康庫爾工廠計畫向歐洲出口8.8萬噸綠氫。墨西哥、南美洲和中東地區仍在發展中,目前的部署嚴重偏向氨出口,而非國內燃料電池的使用。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 政府強制推行零排放政策和提供補貼

- 由於超級工廠規模的生產,PEM電堆的美元/千瓦成本迅速下降。

- 亞洲、歐盟和美國氫燃料加註基礎設施的擴張

- 汽車製造商2025年及以後的燃料電池電動車生產計畫

- 將廢棄的二手用PEM模組重新用於貨櫃式發電機

- PFAS 含量為零的薄膜技術進步催生了新的供應商。

- 市場限制因素

- 鉑族金屬的高成本風險

- 早期採用區域以外的氫氣供應有限。

- 銥和鉑金供應即將短缺

- 100千瓦以上固定式固態氧化物燃料電池(SOFC)計畫的競爭格局

- 供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

第5章 市場規模與成長預測

- 按類型

- 低溫PEMFC

- 高溫PEMFC

- 透過冷卻法

- 空冷式

- 水冷

- 依輸出類型

- 小於1千瓦

- 1~10 kW

- 10~100 kW

- 超過100千瓦

- 按組件

- 燃料電池堆

- 膜電極組件

- 雙極板

- 氣體擴散層

- 催化劑

- 工廠周邊設備

- 透過使用

- 運輸

- 固定式電源

- 可攜式/備用電源

- 按最終用戶行業分類

- 運輸

- 公用事業

- 商業和工業用途

- 其他(國防、住宅)

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 英國

- 德國

- 法國

- 西班牙

- 北歐國家

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 馬來西亞

- 泰國

- 印尼

- 越南

- 澳洲

- 其他亞太國家

- 南美洲

- 巴西

- 阿根廷

- 哥倫比亞

- 其他南美國家

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢(併購、聯盟、購電協議)

- 市場佔有率分析(主要公司的市場排名和佔有率)

- 公司簡介

- Ballard Power Systems

- Plug Power Inc.

- Cummins Inc.

- Toyota Motor Corporation

- Hyundai Motor Company

- Toshiba Corporation

- ITM Power PLC

- PowerCell Sweden AB

- Intelligent Energy Limited

- Doosan Fuel Cell Co., Ltd.

- Bloom Energy Corporation

- FuelCell Energy Inc.

- Panasonic Corporation

- Ceres Power Holdings plc

- Nedstack Fuel Cell Technology BV

- ElringKlinger AG

- Symbio SAS

- Robert Bosch GmbH

- Horizon Fuel Cell Technologies

- SFC Energy AG

第7章 市場機會與未來展望

According to Mordor Intelligence, the polymer electrolyte membrane fuel cells (PEMFC) market size is estimated at USD 6.67 billion in 2026, and is expected to reach USD 25.99 billion by 2031, at a CAGR of 31.26% during the forecast period (2026-2031).

This report is Segmented by Type (Low-Temperature and High-Temperature), Cooling Method (Air-Cooled and Liquid-Cooled), Power Output (10 To 100 KW, Above 100 KW, and More), Component (Membrane Electrode Assembly, Catalysts, and More), Application (Transportation, and More), End-User Industry (Transportation, Utilities, and More), and Geography (Europe, Asia-Pacific, and More).

Global Polymer Electrolyte Membrane Fuel Cells (PEMFC) Market Trends and Insights

Government Zero-Emission Mandates & Subsidies

Mandates now oblige fleet owners to phase out diesel across ports, logistics corridors, and municipal fleets. California's rule, effective 2024, compels all new drayage trucks to be zero-emission, while the EU's revised heavy-duty CO2 standards target a 90% cut by 2040, spurring fuel cell or battery adoption for long-haul. China extended its New Energy Vehicle subsidy through 2025, earmarking CNY 3.7 billion for commercial FCEVs and matching support at provincial levels. South Korea's roadmap funds 850,000 FCEVs and 1,200 hydrogen stations by 2030. These synchronized policies underpin offtake security that justifies private investment in large-scale stack production and dispensing networks.

Rapid Decline in PEM Stack Cost Due to Gigafactory Scale

Rochester's 1 GW gigafactory, commissioned by Plug Power in late 2025, demonstrated a 35% cost drop by unifying MEA coating, plate stamping, and end-of-line testing under one roof. Hyundai's Guangzhou plant already targets USD 50 per kW stacks by 2027 through automated cell placement, while Bosch leverages automotive tolerances to drive scrap below 2%. U.S. DOE roadmaps confirm traction, reporting 2024 stack costs at USD 60 per kW, one year ahead of plan. Such economies open price-sensitive niches like material handling and telecom backup that previously favored diesel engines.

High Platinum-Group Metal Cost Exposure

Platinum averaged USD 1,050 per troy oz in 2025, inflating catalyst bills to roughly USD 1,000 for an 80 kW automotive stack. Recycling helps: Toyota's closed-loop program recovers 95% of platinum from retired modules, trimming virgin demand by 12,000 oz annually. Yet Ballard reports every 10% uptick in platinum price erodes gross margin by 2.5 points unless passed to customers. Research into iron-nitrogen-carbon catalysts hits 60% of platinum activity but falls short of durable service life, meaning exposure persists at least through mid-forecast.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Hydrogen Refueling Infrastructure

- Automaker FCEV Production Commitments Beyond 2025

- Looming Iridium & Platinum Supply Bottlenecks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

High-temperature stacks will grow at 35.8% through 2031, even though low-temperature units owned 73.5% of 2025 sales. Industrial operators value 120 °C-180 °C operation because the waste heat can be recuperated for process loads, cutting balance-of-plant spending by 25%. Serenergy's 5 kW installs in Danish apartment blocks in 2025 delivered 90% combined efficiency by channeling exhaust heat into radiators. Low-temperature designs remain standard for vehicles owing to quick cold starts and 4 kW L-1 power density. However, phosphoric-acid-doped polybenzimidazole membranes now show 10,000-hour durability, shrinking the density gap and suggesting high-temperature adoption may broaden where refined hydrogen is scarce.

Liquid-cooled stacks covered 70.1% of 2025 volume and will expand at a 32.5% CAGR, essential once outputs exceed 30 kW. Deionized water or glycol circuits keep cells within the 65 °C-75 °C sweet spot, allowing 4 kW L-1 density even if radiators add 15% weight. Horizon's hybrid cooling launched in 2025 toggles between air and liquid, trimming parasitic draw by 8%. Maritime uses underline liquid's relevance: Wartsila's 1.2 MW ship module dissipates 600 kW of heat to seawater, an impossible feat with air-only cooling. Air-cooled units stay relevant for telecom and forklifts where simplicity overrides peak power.

Geography Analysis

Asia-Pacific commanded 47.6% of the polymer electrolyte membrane fuel cell (PEMFC) market share in 2025 and should grow at 33.1% through 2031. China deployed 428 hydrogen stations, with Guangdong, Shandong, and Hebei subsidizing 40% of truck purchase costs. Japan extended its Ene-Farm rebate to 2027 and targets 5.3 million home installs by 2030. South Korea funds 850,000 FCEVs and 1,200 stations, while India's National Hydrogen Mission mandates 10% refinery hydrogen be green by 2027. Australia concentrates on export ammonia, with limited domestic uptake outside mining equipment.

Europe's hydrogen backbone will repurpose 28,000 km of pipelines by 2027, lowering delivered hydrogen 30% below trucking costs. Germany assigned EUR 9 billion to electrolyzers and heavy-duty truck incentives, France targets 6.5 GW electrolysis by 2030, and the U.K. clusters on HyNet. Nordic hydropower underwrites low-carbon hydrogen export deals. Policy alignment under RED III mandates 42% renewable hydrogen in industry by 2030, anchoring future demand.

North America benefits from the USD 8 billion federal hub program. The Gulf Coast hub aims at 1.2 GW of blue hydrogen for refineries, whereas California drayage rules push trucking demand. Canada's Becancour plant will export 88,000 t of green hydrogen to Europe. Mexico, South America, and the Middle East remain nascent, skewing current deployments toward export ammonia rather than domestic fuel cells.

- Ballard Power Systems

- Plug Power Inc.

- Cummins Inc.

- Toyota Motor Corporation

- Hyundai Motor Company

- Toshiba Corporation

- ITM Power PLC

- PowerCell Sweden AB

- Intelligent Energy Limited

- Doosan Fuel Cell Co., Ltd.

- Bloom Energy Corporation

- FuelCell Energy Inc.

- Panasonic Corporation

- Ceres Power Holdings plc

- Nedstack Fuel Cell Technology BV

- ElringKlinger AG

- Symbio SAS

- Robert Bosch GmbH

- Horizon Fuel Cell Technologies

- SFC Energy AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government zero-emission mandates & subsidies

- 4.2.2 Rapid decline in PEM stack $/kW due to gigafactory-scale production

- 4.2.3 Expansion of hydrogen refueling infrastructure in Asia, EU & US

- 4.2.4 Automaker FCEV production commitments beyond 2025

- 4.2.5 Second-life automotive PEM modules repurposed for containerised gensets

- 4.2.6 PFAS-free membrane breakthroughs enabling new suppliers

- 4.3 Market Restraints

- 4.3.1 High platinum-group metal cost exposure

- 4.3.2 Limited hydrogen distribution outside early-adopter regions

- 4.3.3 Looming iridium & platinum supply bottlenecks

- 4.3.4 SOFC competition for >=100 kW stationary projects

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Type

- 5.1.1 Low-Temperature PEMFC

- 5.1.2 High-Temperature PEMFC

- 5.2 By Cooling Method

- 5.2.1 Air-Cooled

- 5.2.2 Liquid-Cooled

- 5.3 By Power Output

- 5.3.1 Below 1 kW

- 5.3.2 1 to 10 kW

- 5.3.3 10 to 100 kW

- 5.3.4 Above 100 kW

- 5.4 By Component

- 5.4.1 Fuel Cell Stack

- 5.4.2 Membrane Electrode Assembly

- 5.4.3 Bipolar Plates

- 5.4.4 Gas Diffusion Layers

- 5.4.5 Catalysts

- 5.4.6 Balance-of-Plant Components

- 5.5 By Application

- 5.5.1 Transportation

- 5.5.2 Stationary Power

- 5.5.3 Portable/Backup Power

- 5.6 By End-User Industry

- 5.6.1 Transportation

- 5.6.2 Utilities

- 5.6.3 Commercial and Industrial

- 5.6.4 Others (Defense, Residential)

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 Europe

- 5.7.2.1 United Kingdom

- 5.7.2.2 Germany

- 5.7.2.3 France

- 5.7.2.4 Spain

- 5.7.2.5 Nordic Countries

- 5.7.2.6 Russia

- 5.7.2.7 Rest of Europe

- 5.7.3 Asia-Pacific

- 5.7.3.1 China

- 5.7.3.2 India

- 5.7.3.3 Japan

- 5.7.3.4 South Korea

- 5.7.3.5 Malaysia

- 5.7.3.6 Thailand

- 5.7.3.7 Indonesia

- 5.7.3.8 Vietnam

- 5.7.3.9 Australia

- 5.7.3.10 Rest of Asia-Pacific

- 5.7.4 South America

- 5.7.4.1 Brazil

- 5.7.4.2 Argentina

- 5.7.4.3 Colombia

- 5.7.4.4 Rest of South America

- 5.7.5 Middle East and Africa

- 5.7.5.1 United Arab Emirates

- 5.7.5.2 Saudi Arabia

- 5.7.5.3 South Africa

- 5.7.5.4 Rest of Middle East and Africa

- 5.7.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Ballard Power Systems

- 6.4.2 Plug Power Inc.

- 6.4.3 Cummins Inc.

- 6.4.4 Toyota Motor Corporation

- 6.4.5 Hyundai Motor Company

- 6.4.6 Toshiba Corporation

- 6.4.7 ITM Power PLC

- 6.4.8 PowerCell Sweden AB

- 6.4.9 Intelligent Energy Limited

- 6.4.10 Doosan Fuel Cell Co., Ltd.

- 6.4.11 Bloom Energy Corporation

- 6.4.12 FuelCell Energy Inc.

- 6.4.13 Panasonic Corporation

- 6.4.14 Ceres Power Holdings plc

- 6.4.15 Nedstack Fuel Cell Technology BV

- 6.4.16 ElringKlinger AG

- 6.4.17 Symbio SAS

- 6.4.18 Robert Bosch GmbH

- 6.4.19 Horizon Fuel Cell Technologies

- 6.4.20 SFC Energy AG

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment

質子交換膜燃料電池市場:全球市場預測,2026-2032年

質子交換膜燃料電池市場:全球市場預測,2026-2032年 2026-2034年燃料電池和電解槽用烴類膜全球市場規模、佔有率、趨勢和成長分析報告

2026-2034年燃料電池和電解槽用烴類膜全球市場規模、佔有率、趨勢和成長分析報告 固體電解質燃料電池市場預測—按組件、產量、應用、最終用戶和地區分類的全球分析—2034年質子交換膜燃料電池全球市場規模、佔有率、趨勢和成長分析報告(2026-2034)

固體電解質燃料電池市場預測—按組件、產量、應用、最終用戶和地區分類的全球分析—2034年質子交換膜燃料電池全球市場規模、佔有率、趨勢和成長分析報告(2026-2034) 聚合物電解質膜燃料電池市場-全球產業規模、佔有率、趨勢、機會及預測(按最終用途、應用、地區和競爭格局分類,2021-2031年)硫化聚丙烯腈正極材料市場(按電池類型、電池形式、容量等級、純度等級、製造流程、應用、最終用途和銷售管道)—全球預測(2026-2032 年)質子交換膜燃料電池市場-全球產業規模、佔有率、趨勢、機會及預測(按類型、材料、應用、地區和競爭格局分類,2021-2031年預測)

聚合物電解質膜燃料電池市場-全球產業規模、佔有率、趨勢、機會及預測(按最終用途、應用、地區和競爭格局分類,2021-2031年)硫化聚丙烯腈正極材料市場(按電池類型、電池形式、容量等級、純度等級、製造流程、應用、最終用途和銷售管道)—全球預測(2026-2032 年)質子交換膜燃料電池市場-全球產業規模、佔有率、趨勢、機會及預測(按類型、材料、應用、地區和競爭格局分類,2021-2031年預測) 質子交換膜燃料電池市場規模、佔有率及成長分析(按類型、材料、應用和地區分類)-2026-2033年產業預測

質子交換膜燃料電池市場規模、佔有率及成長分析(按類型、材料、應用和地區分類)-2026-2033年產業預測 質子交換膜(PEM)市場規模、佔有率和成長分析(按類型、材料、應用和地區分類)-2026-2033年產業預測

質子交換膜(PEM)市場規模、佔有率和成長分析(按類型、材料、應用和地區分類)-2026-2033年產業預測 PEM燃料電池市場機會、成長要素、產業趨勢分析及2026年至2035年預測

PEM燃料電池市場機會、成長要素、產業趨勢分析及2026年至2035年預測