|

市場調查報告書

商品編碼

2061518

醫療產業高級認證:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Advanced Authentication In Healthcare Industry - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

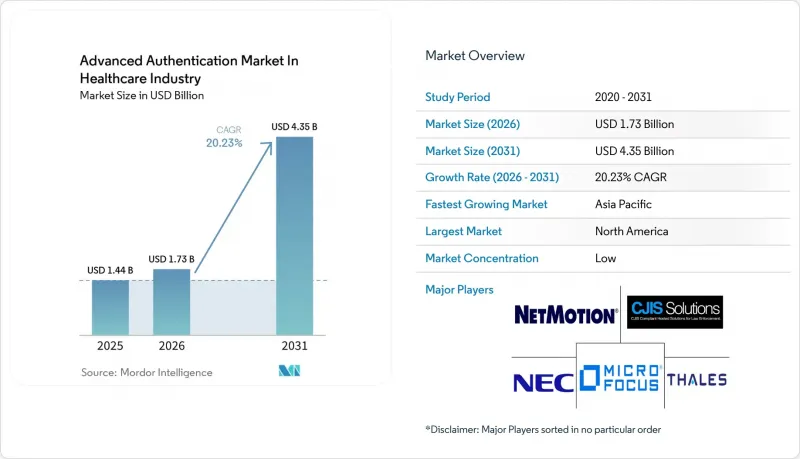

2025 年,高資質醫療產業的市場規模價值為 14.4 億美元,預計到 2031 年將達到 43.5 億美元,而 2026 年為 17.3 億美元,預測期(2026-2031 年)的複合年成長率為 20.23%。

本報告按認證方式(生物識別、智慧卡等)、認證要素(單一因素、多重因素)、組件(解決方案、服務)、部署模式(本地部署、雲端部署)、最終用戶(醫院、診所、醫療保險公司等)和地區進行細分。市場預測以美元計價。

醫療產業高級認證市場的趨勢與發展

醫療保健產業勒索軟體攻擊的增加推高了安全預算。

2024年發生的444起醫療保健網路安全事件中,有238起與勒索軟體相關,佔記錄在案的違規事件總數的69%,凸顯了憑證竊盜威脅的嚴重性。 Change Healthcare因系統故障造成的24億美元損失,揭露了醫療保健網路安全領域身分驗證漏洞造成的巨大經濟損失。平均安全預算已從IT支出的5%增加到12%,在董事會的指南下,消除密碼已成為可衡量的病患安全目標。 FinCEN追蹤到2022年至2024年間發生的389起醫療保健相關事件,共支付了3.054億美元的贖金,這進一步強化了無密碼策略的商業合理性。已實施反釣魚功能的醫療機構特權帳戶外洩事件顯著減少,這表明強大的身份驗證與抵禦勒索軟體攻擊之間存在關聯。

病患資料保護的監管要求

美國食品藥物管理局 (FDA) 第 524B 條款於 2023 年 3 月生效,要求醫療設備製造商在所有上市前申報文件中整合身分驗證功能並公佈軟體材料清單。美國國家標準與技術研究院 (NIST) 於 2025 年 7 月發布的 SP 800-63A-4 更新了生物識別標準,以低於萬分之一的誤報率檢測呈現攻擊。 HIPAA 的執行力度不斷加大,2024 年,一項因門禁控制不力而處以 1.42 億美元罰款的案例被曝光。歐洲的 GDPR 也規定了類似的處罰,罰款最高可達全球營業額的 4%,迫使跨國公司統一其跨洲的身份策略。隨著網路保險續保中強制實施多因素身份驗證,監管和市場力量正朝著相同的身份驗證標準靠攏。

傳統醫院IT系統的實施成本很高

許多醫院運行著超過150個應用程式,這些應用程式都基於過時的作業系統。對每個遺留平台進行客製化整合可能會使專案成本高達數百萬美元,這對利潤率僅為2-3%的醫療機構構成了巨大的挑戰。身份閘道器可以將過時的LDAP和專有登入方式轉換為現代的SAML和OAuth,但這會增加系統的複雜性。資本支出委員會通常優先考慮診斷設備而非隱藏的安全措施,導致升級被推遲到發生安全漏洞或達成法庭和解之後。

細分市場分析

到2025年,生物識別將佔醫療產業高級認證市場銷售額的47.85%,幾乎佔高級認證市場佔有率的一半。這種方法的優點在於,手術團隊即使戴著手套,也能透過指紋或手掌掃描在不到一秒的時間內存取記錄。隨著生物識別有效性標準的日趨成熟,預計到2031年,高級生物識別認證市場將以19.60%的複合年成長率成長。供應商正在將多波長感測器整合到行動推車中,從而在一次操作中同時保護設備和會話安全。成功部署的關鍵在於制定衛生規範,在不影響準確性的前提下對掃描儀進行消毒。

在醫療產業的先進身分驗證市場中,行動智慧身分驗證正經歷最快的成長,預計到2031年將以22.05%的複合年成長率成長。這主要得益於將實體門禁和邏輯登入整合到單一智慧型手機錢包中。醫院可以立即使這些數位徽章失效,從而降低員工離職時的風險。智慧卡由於美國國防部(DHA)的強制要求而繼續存在,但由於讀卡機終端的高昂維修成本,其需求正在趨於平穩。硬體符記用於保護禁止使用行動電話的無菌區域,但隨著FIDO2設備內金鑰的標準化,其市場佔有率正在下降。在SIM卡交換攻擊事件頻傳之後,動態密碼正逐漸淘汰。

在醫療產業的高級身份驗證市場中,多因素身份驗證解決方案預計到2025年將佔據63.10%的市場佔有率,年複合成長率(CAGR)為21.10%,原因是網路保險公司擴大拒絕為未實施此類解決方案的醫療機構提供保險。基於風險的身份驗證引擎現在僅在檢測到異常行為時才會增加身份驗證因素的數量,從而在安全性和臨床醫生便利性之間取得平衡。據報道,2024年底出現的推播通知疲勞攻擊加速了向FIDO2硬體金鑰的轉變,以防止重播攻擊。預計到2031年,醫療產業採用多因素身分驗證相關的高階身分驗證市場規模將達到28.6億美元。

單因素身份驗證仍然保護 36.90% 的終端,其中許多是患者門戶,在這些門戶中,便利性遠大於風險。管治委員會正在根據資料分類等級對應用程式進行分類,為電子處方箋系統實施結合生物識別和令牌的身份驗證機制,同時保留咖啡簡餐店系統所需的使用者名稱和密碼組合。這種分層模型符合 NIST 指南,並避免了可能阻礙實施的統一化阻力。

區域分析

北美地區由於資料外洩成本高昂、監管機構監管嚴格以及IT預算充足,預計將引領市場,到2025年將佔據醫療產業高度認證市場收入的39.95%。美國公民及人權辦公室(OCR)在2024年開出了1.42億美元的罰單,其中68%是由於身分驗證缺陷造成的。 Change Healthcare系統故障引發了整個生態系統的連鎖反應,並將身分管理提上了董事會的議程。加拿大正透過省級電子健康卡走上類似的道路,而墨西哥則處於實施初期,隨著私人醫療機構採用電子健康記錄,墨西哥也逐漸增加身分管理功能。

預計到2031年,亞太地區將以22.60%的複合年成長率成為成長最快的地區。日本正在政府的數位化計畫下推動醫院身分識別管理的現代化,該計畫將臉部辨識整合到電子病歷自助服務終端中。印度正在將Aadhaar的生物識別與Ayushman Bharat數位醫療計畫結合,以建立大規模的新用戶群體,並透過指紋和虹膜掃描進行保護。在中國,部署利用國家醫療雲的智慧醫院必須採用多因素認證管理。澳洲和韓國正在利用其成熟的寬頻環境和高智慧型手機普及率,推動遠距遠端醫療中的行動認證。儘管這一發展勢頭強勁,但各國的資料保護法律差異顯著,因此供應商需要針對醫療產業的各個高級認證市場客製化雲端託管和密鑰儲存模式。

歐洲的情況則介於這兩個極端之間。 GDPR罰款高達全球收入的4%,促使企業儘早遵守相關規定,德國的電子健康卡計畫預設採用X.509證書。英國國民醫療服務體系(NHS)正在其綜合醫療保健系統中實施身分識別,但其複雜性延緩了實施進度。法國、義大利和西班牙正透過國家數位健康基金進行投資,但採購週期仍然很長。在東歐,高階身分驗證市場的普及速度緩慢,過時的基礎設施阻礙了雲端遷移,但歐盟範圍內的標準正在持續推動整合。南美洲、中東和非洲的普及率較低,但新建醫院預計將促進向雲端原生身分管理的快速過渡。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 連網醫療設備的激增正在擴大攻擊面。

- 關於病患資料保護的監管義務

- 向遠端醫療過渡需要安全的身份驗證

- 醫療保健產業勒索軟體攻擊的增加推高了安全預算。

- 將生物識別整合到電子健康記錄系統中

- 醫院IT網路中零信任架構的快速普及

- 市場限制因素

- 實施傳統醫院IT系統成本高昂

- 異質醫療應用之間互通性的挑戰

- 由於工作流程摩擦,臨床工作人員產生抗拒。

- 當地醫療機構寬頻連線受限

- 宏觀經濟因素對市場的影響

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 投資分析

第5章 市場規模與成長預測

- 身份驗證方法

- 生物識別

- 智慧卡

- 行動智慧憑證

- 硬體符記

- 其他身份驗證方法

- 身份驗證方法

- 單一身份驗證方法

- 多因素身份驗證

- 按組件

- 解決方案

- 服務

- 部署模式

- 現場

- 雲

- 最終用戶

- 醫院和診所

- 健康保險提供者

- 製藥和生物技術公司

- 醫療設備製造商

- 其他最終用戶

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲

- 其他亞太國家

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 埃及

- 奈及利亞

- 其他非洲國家

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- NetMotion Software, Inc

(Absolute Software Corporation)

- CJIS Solutions LLC

- Micro Focus International plc

(OpenText UK Holding Limited)

- Auth0 Inc(Okta 的子公司)

- WideBand Corporation

- 富士通有限公司

- 泰雷茲集團(金雅拓集團)

- NEC公司

- 博通(CA Technologies)

- 戴爾科技

- IDEMIA France SAS(Safran Identity and Security)

- HID Global Corporation

- Lumidigm Inc(HID Global)

- PistolStar Inc(SailPoint 的子公司)

- Okta Inc

- Ping Identity Holding Corp

- OneSpan Inc

- Imprivata Inc

- 微軟公司

- RSA Security LLC

- Duo Security Inc(Cisco Systems)

- M2SYS Technology

第7章 市場機會與未來展望

According to Mordor Intelligence, the advanced authentication market size in healthcare industry was valued at USD 1.44 billion in 2025 and estimated to grow from USD 1.73 billion in 2026 to reach USD 4.35 billion by 2031, at a CAGR of 20.23% during the forecast period (2026-2031).

This report is Segmented by Authentication Method (Biometric, Smart Card, and More), Authentication Factor (Single Factor, Multi-Factor), Component (Solutions, Services), Deployment Mode (On-Premises, Cloud), End User (Hospitals and Clinics, Health Insurance Providers, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Insights and Trends of Advanced Authentication Market In Healthcare Industry

Rising Healthcare Ransomware Attacks Driving Security Budgets

Ransomware caused 238 of 444 healthcare cyber events in 2024 and accounted for 69% of compromised records, underscoring the lethality of credential theft pipelines. The USD 2.4 billion fallout from the Change Healthcare outage revealed the monetary weight of weak authentication in the healthcare cybersecurity space. Average security budgets rose from 5% to 12% of IT spending, and board directives now frame password retirement as a measurable patient safety objective. FinCEN tracked USD 305.4 million in ransomware payouts tied to 389 healthcare incidents between 2022 and 2024, which hardened the business case for password-less strategies. Providers that rolled out phishing-resistant factors recorded measurable drops in privileged-account compromise, validating the link between strong identity proofing and ransomware resilience.

Regulatory Mandates for Patient Data Protection

FDA Section 524B, operational since March 2023, requires device manufacturers to embed authentication and publish software bills of materials in every pre-market submission. NIST SP 800-63A-4, issued in July 2025, upgrades biometric standards to include presentation-attack detection at false-match rates below 1 in 10,000. HIPAA enforcement accelerated, with USD 142 million in 2024 penalties tied to access-control lapses. The European GDPR mirrors these fines, with penalties of up to 4% of global revenue, prompting multinationals to unify their identity policies across continents. Cyber-insurance renewals now mandate multi-factor deployment, making regulatory and market forces converge on the same authentication baseline.

High Implementation Costs for Legacy Hospital IT Systems

Many hospitals juggle more than 150 applications that run on unsupported operating systems. Custom integration for each legacy platform pushes project bills into the multi-million-dollar range, a challenge for providers running on 2-3% margins. Identity gateways translate old LDAP or proprietary log-ons into modern SAML or OAuth, but add complexity. Capital committees often choose diagnostic equipment over invisible security, leading to deferred upgrades until after a breach or consent decree.

Other drivers and restraints analyzed in the detailed report include:

- Proliferation of Connected Medical Devices Expanding Attack Surface

- Shift to Remote Telehealth Requiring Secure Identity Verification

- Interoperability Challenges Among Disparate Healthcare Applications

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Biometrics accounted for 47.85% of advanced authentication market in healthcare industry revenue in 2025, giving this segment nearly half of the advanced authentication market share. The modality excels because surgical teams can unlock records with gloved fingerprints or palm-vein scans in under one second. The advanced authentication market size for biometrics is projected to rise at 19.60% CAGR through 2031 as liveness detection standards mature. Vendors embed multispectral sensors into mobile carts, securing both device and session in one gesture. Implementation success hinges on hygiene protocols that disinfect scanners without degrading accuracy.

Mobile smart credentials record the fastest growth, in advanced authentication market in healthcare industry, at a 22.05% CAGR to 2031, driven by the convergence of physical door access and logical log-on inside one smartphone wallet. Hospitals can revoke these digital badges instantly, trimming risk when staff depart. Smart cards persist under Defense Health Agency mandates but face plateauing demand because reader fleets are expensive to maintain. Hardware tokens secure sterile zones where phones are barred; however, market share is eroding as FIDO2 on-device keys become the standard. One-time passwords are falling out of favor after documented SIM-swap exploits.

Multi-factor solutions, in advanced authentication market in healthcare industry, held 63.10% share in 2025 and expand at 21.10% CAGR as cyber-insurance carriers refuse coverage without them. Risk-based engines now elevate factor count only when anomalous behavior is detected, blending security with clinician usability. Push-fatigue attacks documented in late 2024 accelerated migration to FIDO2 hardware keys that block replay. The advanced authentication market in healthcare industry size tied to multi-factor deployments is forecast at USD 2.86 billion by 2031.

Single-factor still protects 36.90% of endpoints, largely patient portals where convenience outweighs risk. Governance committees segment applications by data-classification level, deploying biometric-plus-token gates on e-prescribing while keeping username-password pairs on cafeteria systems. This tiered model aligns with NIST guidance and avoids blanket friction that could undercut adoption.

Geography Analysis

North America dominated with 39.95% of 2025 revenue of advanced authentication market in healthcare industry, helped by high breach costs, aggressive regulators, and strong IT budgets. OCR issued USD 142 million in penalties during 2024, and 68% cited authentication gaps. The Change Healthcare outage demonstrated ecosystem-wide ripple effects, which moved identity to the board agenda. Canada follows similar paths through provincial e-healthcards, while Mexico is earlier in its journey but is adding identity controls as private providers adopt electronic records.

The Asia-Pacific region posts the fastest regional growth at a 22.60% CAGR through 2031. Japan modernizes hospital identity under government digitization schemes that embed face recognition in EHR kiosks. India links Aadhaar biometrics to the Ayushman Bharat Digital Mission, creating a massive new user base secured by fingerprints and iris scans. China mandates multi-factor authentication controls within smart hospital rollouts that utilize national health clouds. Australia and South Korea ride mature broadband and smartphone penetration to push mobile authentication in remote care. Despite momentum, data-protection laws vary widely, so vendors must tailor cloud hosting and key escrow models by advanced authentication market in healthcare industry.

Europe sits between these poles. GDPR fines up to 4% of global turnover motivate early compliance, and Germany's e-healthcard program embeds X.509 certificates by default. The United Kingdom's NHS is rolling identity across integrated care systems, yet complexity slows timelines. France, Italy, and Spain invest through national digital-health funds, but procurement cycles remain lengthy. Advanced authentication market adoption is slower in Eastern Europe, and older infrastructure restrains cloud shifts, yet pan-EU standards exert steady pressure for convergence. South America, the Middle East, and Africa trail in penetration but benefit from new hospital builds that can leapfrog straight to cloud-native identity.

- NetMotion Software, Inc (Absolute Software Corporation)

- CJIS Solutions LLC

- Micro Focus International PLC (OpenText UK Holding Limited)

- Auth0 Inc (an Okta Company)

- WideBand Corporation

- Fujitsu Limited

- Thales Group (Gemalto NV)

- NEC Corporation

- Broadcom Inc (CA Technologies)

- Dell Technologies Inc

- IDEMIA France SAS (Safran Identity and Security)

- HID Global Corporation

- Lumidigm Inc (HID Global)

- PistolStar Inc (SailPoint Company)

- Okta Inc

- Ping Identity Holding Corp

- OneSpan Inc

- Imprivata Inc

- Microsoft Corporation

- RSA Security LLC

- Duo Security Inc (Cisco Systems)

- M2SYS Technology

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Proliferation of Connected Medical Devices Expanding Attack Surface

- 4.2.2 Regulatory Mandates for Patient Data Protection

- 4.2.3 Shift to Remote Telehealth Requiring Secure Identity Verification

- 4.2.4 Rising Healthcare Ransomware Attacks Driving Security Budgets

- 4.2.5 Integration of Biometric Authentication in EHR Systems

- 4.2.6 Rapid Adoption of Zero Trust Architecture in Hospital IT Networks

- 4.3 Market Restraints

- 4.3.1 High Implementation Costs for Legacy Hospital IT Systems

- 4.3.2 Interoperability Challenges Among Disparate Healthcare Applications

- 4.3.3 User Resistance from Clinical Staff Due to Workflow Friction

- 4.3.4 Limited Broadband Connectivity in Rural Healthcare Facilities

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Consumers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitute Products

- 4.8.5 Intensity of Competitive Rivalry

- 4.9 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Authentication Method

- 5.1.1 Biometric

- 5.1.2 Smart Card

- 5.1.3 Mobile Smart Credentials

- 5.1.4 Hardware Token

- 5.1.5 Other Authentication Methods

- 5.2 By Authentication Factor

- 5.2.1 Single Factor

- 5.2.2 Multi-Factor

- 5.3 By Component

- 5.3.1 Solutions

- 5.3.2 Services

- 5.4 By Deployment Mode

- 5.4.1 On-Premises

- 5.4.2 Cloud

- 5.5 By End User

- 5.5.1 Hospitals and Clinics

- 5.5.2 Health Insurance Providers

- 5.5.3 Pharma and Biotech Companies

- 5.5.4 Medical Device Manufacturers

- 5.5.5 Other End Users

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Australia

- 5.6.4.6 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Saudi Arabia

- 5.6.5.1.2 United Arab Emirates

- 5.6.5.1.3 Turkey

- 5.6.5.1.4 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Egypt

- 5.6.5.2.3 Nigeria

- 5.6.5.2.4 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 NetMotion Software, Inc

(Absolute Software Corporation)

- 6.4.2 CJIS Solutions LLC

- 6.4.3 Micro Focus International PLC

(OpenText UK Holding Limited)

- 6.4.4 Auth0 Inc (an Okta Company)

- 6.4.5 WideBand Corporation

- 6.4.6 Fujitsu Limited

- 6.4.7 Thales Group (Gemalto NV)

- 6.4.8 NEC Corporation

- 6.4.9 Broadcom Inc (CA Technologies)

- 6.4.10 Dell Technologies Inc

- 6.4.11 IDEMIA France SAS (Safran Identity and Security)

- 6.4.12 HID Global Corporation

- 6.4.13 Lumidigm Inc (HID Global)

- 6.4.14 PistolStar Inc (SailPoint Company)

- 6.4.15 Okta Inc

- 6.4.16 Ping Identity Holding Corp

- 6.4.17 OneSpan Inc

- 6.4.18 Imprivata Inc

- 6.4.19 Microsoft Corporation

- 6.4.20 RSA Security LLC

- 6.4.21 Duo Security Inc (Cisco Systems)

- 6.4.22 M2SYS Technology

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

FIDO(快速線上識別)市場 - 2026-2032年全球市場預測

FIDO(快速線上識別)市場 - 2026-2032年全球市場預測 進階身分驗證市場報告:按身分驗證方法、部署模型、解決方案、最終用戶產業和地區分類(2026-2034 年)

進階身分驗證市場報告:按身分驗證方法、部署模型、解決方案、最終用戶產業和地區分類(2026-2034 年) 先進公共運輸系統市場:商業機會、成長要素、產業趨勢分析及2026-2035年預測

先進公共運輸系統市場:商業機會、成長要素、產業趨勢分析及2026-2035年預測 2026年全球國防高級認證市場報告高階身分驗證市場:2026-2032 年全球預測,依身分驗證方法、元件、產業、部署類型和企業規模分類2026年金融服務領域高階身分驗證全球市場報告

2026年全球國防高級認證市場報告高階身分驗證市場:2026-2032 年全球預測,依身分驗證方法、元件、產業、部署類型和企業規模分類2026年金融服務領域高階身分驗證全球市場報告 2035 年健康記錄高級生物識別市場分析與預測:按類型、產品類型、服務、技術、組件、應用、部署類型和最終用戶分類FIDO認證市場分析及預測(至2035年):依類型、產品、服務、技術、組件、應用、部署、最終用戶及解決方案分類

2035 年健康記錄高級生物識別市場分析與預測:按類型、產品類型、服務、技術、組件、應用、部署類型和最終用戶分類FIDO認證市場分析及預測(至2035年):依類型、產品、服務、技術、組件、應用、部署、最終用戶及解決方案分類 全球FIDO認證市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球FIDO認證市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 高階身分驗證市場規模、佔有率和成長分析(按身分驗證類型、身分驗證方法、部署類型、組織規模、最終用戶產業和地區分類)—產業預測(2026-2033 年)

高階身分驗證市場規模、佔有率和成長分析(按身分驗證類型、身分驗證方法、部署類型、組織規模、最終用戶產業和地區分類)—產業預測(2026-2033 年)