|

市場調查報告書

商品編碼

2061510

旅居車市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Motorhome - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

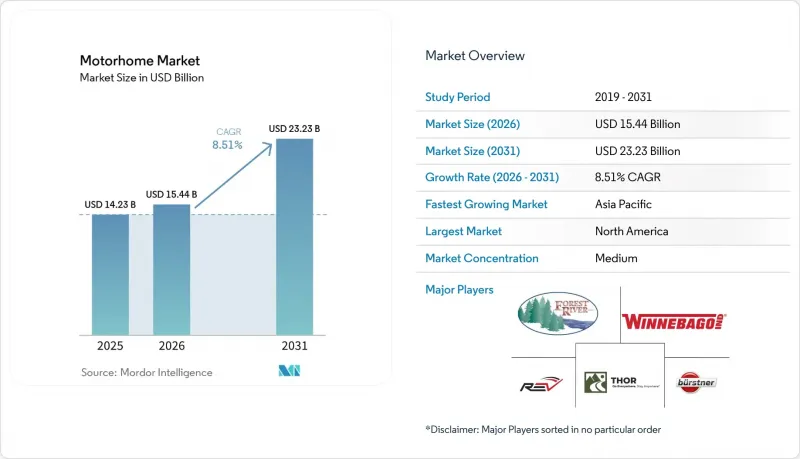

根據 Mordor Intelligence 預測,旅居車市場規模將從 2025 年的 142.3 億美元成長到 2026 年的 154.4 億美元,到 2031 年將達到 232.3 億美元,2026 年至 2031 年的複合年成長率為 8.51%。

本報告按旅居車類型(A級、B級、C級)、最終用戶(個人買家、租賃公司、車隊營運商)、動力系統(柴油、汽油、電動)、價格區間(經濟型、中階、高階)和地區(北美、南美、歐洲、亞太、中東和非洲)進行細分。市場預測以價值(美元)和銷售(輛)兩種形式呈現。

全球旅居車市場趨勢及洞察

以房車為中心的旅遊生態系統的擴展

為了滿足日益成長的房車度假需求,私人業者和公共機構正在升級電力連接、Wi-Fi和污水處理站等設施。在美國露營地協會(Kampgrounds of America),嬰兒潮世代的露營者數量顯著增加,如今已佔據所有遊客的相當大一部分。在德國,隨著熱門地區新露營地的不斷湧現,註冊量也呈現爆炸性成長。在日本,監管政策的調整允許大型旅居車在高速公路上行駛,刺激了豪華房車的進口。設施的改善縮短了繁忙路段沿線露營地的投資回收期,形成良性循環,促進了基礎設施的進一步發展。

遠距辦公和房車生活方式日益普及

數位遊民的數量急劇成長,擁有至少一名全職遠距工作者的房車家庭數量顯著增加。年輕一代的專業人士推動了對符合人體工學的辦公桌、行動電話訊號增強器和高容量鋰離子電池組等功能的需求。星鏈天線和每月套餐也變得司空見慣,即使在偏遠地區也能實現穩定的視訊會議。與大城市相比,這種生活方式的生活成本顯著降低,因此極具經濟吸引力。為了滿足這項需求,原始設備製造商(OEM)正在整合先進的系統、太陽能車頂和滑出式工作站,有效地將房車改造為行動辦公室。

高零售價格和易受利率波動影響的貸款

旅居車貸款通常涉及較長的合約期限和較高的首付,這使得購車者極易受到聯準會利率政策波動的影響。利率上升會顯著增加每月還款額,使對價格敏感的家庭難以負擔這些貸款。優質貸款主要惠及信用評分高的個人,但次級貸款的借款人則面臨更高的年利率(APR),進一步提高了購車門檻。經銷商透過延長高階房車的貸款期限來解決這個問題,但這種策略會增加在貸款到期前換車輛的車主出現負資產的風險。對於入門級C型房車,為了保持價格優勢並符合傳統的房車貸款標準,廠商正在透過移除不必要的功能來股權。

細分市場分析

預計到2025年,C級房車將佔全球房車出貨量的46.26%。這主要歸功於6-8座佈局的流行,這種佈局能夠輕鬆滿足35英尺的停車限制。追求操控性和經濟實惠保險的家庭尤其青睞這一旅居車市場。雖然豪華A級房車的銷售量較低,但隨著富裕的退休人士從拖曳式房車轉向A級房車,預計其年複合成長率將達到9.32%。製造商正透過整合先進系統和太陽能板來提升自身競爭力,使車頂空調能夠脫離電網獨立運行,從而符合更嚴格的發電機法規。同時,緊湊型B級房車適合追求隱密停車和日常實用性的都市區買家,但其高昂的價格阻礙了其市場滲透。

第二排車型的發展也同樣重要。 C級房車製造商現在正將自主研發的創新電池作為標準配置,旨在減輕車重並延長續航里程。同時,B級房車改裝商正在引入升降式車頂和滑出式廚房區域,以在符合停車高度限制的同時保持車內頭部空間。配備智慧家庭系統(可與虛擬助理搭配使用)的高階A級房車,在持續的經濟挑戰下,依然能夠提供居家般的舒適體驗,並維持高階價格。

預計到2025年,個人買家將佔銷售額的60.28%,反映出人們追求個人化和彈性旅行安排的文化趨勢。然而,租賃車輛的成長速度更快,高價值資產的短期租賃正透過數位市場逐漸成為主流,預計到2031年,其複合年成長率將達到9.09%。旅居車租賃市場正經歷顯著成長,這得益於平台提供的責任責任險不斷擴大,讓車主安心無憂,以及高日運轉率提高了車隊的投資收益率(ROI)。

在新註冊的房車中,首次購車者目前佔相當大的比例,與回頭客相比,年輕一代的需求日益明顯。隨著經濟狀況的改善,預計許多對旅居車有興趣的家庭將最終下定決心購買。為了滿足這一需求,汽車製造商(OEM)正在提供諸如即插即用的太陽能系統、影片教學和簡化的管道佈局等功能,以降低用戶的學習難度。車隊營運商也透過利用C級旅居車大宗訂單的批量折扣,以及瞄準企業活動和電影攝製組等市場,來維持穩定的生產水準。

區域分析

北美地區佔2025年銷售額的47.71%,主要原因是庫存調整導致美國批發出貨量減少。然而,在資金籌措穩定和年輕一代首次購屋者數量增加的支撐下,零售需求正在趨於穩定。由於美國擁有大量房車家庭和遍布全國的眾多露營地,美國市場依然強勁。在加拿大,不列顛哥倫比亞省和亞伯達省等地區正在改善配套設施,例如接駁設施和污水處理站,以吸引從都市區搬遷而來的退休人士。

亞太地區正經歷最快的成長,複合年成長率達8.72%。在日本,監管政策的調整允許長軸距房車在高速公路上行駛,包括Annex在內的本土製造商正在擴大生產規模。同時,中國國務院正在重點地區為露營地提供補貼,將房車旅遊打造為重要的休閒產業。在印度,房車市場仍在發展中,但中產階級的壯大和高速公路基礎設施的改善預計將推動未來的需求成長。

歐洲是一個成熟且充滿活力的市場,德國在熱門地區率先開放全年開放的公園。倫敦和巴黎等主要城市引入低排放氣體區,促進了適合城市環境的緊湊型B級廂型車的銷售。義大利和西班牙的沿海旅遊業推動了租賃車輛的成長,而東歐地區新建的製造工廠則推高了運輸成本。

南美洲和中東市場仍處於發展初期。在巴西,進口關稅推高了價格,但當地製造商正在推出價格適中的入門車型。阿拉伯聯合大公國和沙烏地阿拉伯正在投資建造沙漠露營地,以豐富其旅遊產品。土耳其憑藉優惠的稅收政策吸引整車製造商,並致力於成為歐洲的主要出口樞紐。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 市場分析與定義的前提條件

- 分析範圍

第2章 分析方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 擴展以房車為中心的旅遊生態系統

- 遠距辦公與「房車生活」的興起

- 疫情後人們對個人交通工具的偏好

- 擁有高可支配所得的嬰兒潮世代退休人員

- OEM廠商的電動底盤平台實現了成本持平

- 基於訂閱的「房車即服務」經營模式

- 市場限制因素

- 零售價格上漲和對利率敏感的資金籌措

- 已開發地區以外缺乏服務基礎設施

- 電動旅居車。

- 露營地禁止怠速,並實施更嚴格的排放氣體規定。

- 價值鍊和供應鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章:預測市場規模與成長率

- 依旅居車類型

- A級(豪華)

- B級(緊湊型)

- C級(中型)

- 最終用戶

- 個人買家

- 租賃公司

- 車隊營運商

- 透過驅動系統

- 柴油引擎

- 汽油

- 電的

- 按價格範圍

- 經濟

- 中階

- 優質的

- 按地區

- 北美洲

- 美國

- 加拿大

- 其他北美國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太國家

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

- 土耳其

- 其他中東和非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Thor Industries Inc.

- Winnebago Industries Inc.

- Forest River Inc.

- REV Group

- Erwin Hymer Group

- Jayco Inc.

- Tiffin Motorhomes Inc.

- Coachmen RV

- Newmar Corporation

- Leisure Travel Vans

- Dethleffs GmbH

- Hobby-Wohnwagenwerk

- Burstner GmbH & Co. KG

- Trigano SA

- Knaus Tabbert AG

第7章 市場機會與未來展望

According to Mordor Intelligence, the motorhome market size is expected to grow from USD 14.23 billion in 2025 to USD 15.44 billion in 2026 and is forecast to reach USD 23.23 billion by 2031 at an 8.51% CAGR over 2026-2031.

This report is Segmented by Motorhome Class (Class A, Class B, and Class C), End User (Individual Buyers, Rental Companies, and Fleet Operators), Propulsion Type (Diesel, Gasoline, and Electric), Price Range (Economy, Mid-Range, and Premium), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

Global Motorhome Market Trends and Insights

Growing RV-Centric Tourism Ecosystems

Private operators and public agencies are enhancing amenities such as electrical hookups, Wi-Fi, and dump stations to meet the growing demand for RV vacations. Kampgrounds of America has observed a notable increase in baby-boomer campers, with this demographic now representing a significant portion of all guests . Germany has seen a surge in registrations, driven by the continued opening of new parks in popular regions. In Japan, regulatory changes have allowed larger coaches on expressways, facilitating the import of premium RV models. Improved amenities have shortened campground payback periods in high-traffic corridors, creating a cycle that drives further infrastructure development.

Rising Adoption of Remote-Work Van-Life Lifestyles

The number of digital nomads has significantly increased, with a notable rise in RV households featuring at least one full-time remote worker. Younger professionals are driving demand for features such as ergonomic desks, cellular boosters, and large lithium battery banks. Starlink's antenna and monthly plan have become common additions, ensuring reliable video conferencing even in remote locations . With living costs substantially lower than those in major cities, the lifestyle offers a strong financial appeal. In response, OEMs are integrating advanced systems, solar roofs, and slide-out workstations, effectively transforming RVs into mobile offices.

High Retail Prices and Interest-Rate Sensitive Financing

Motorhome loans often come with long-term commitments and significant down payments, leaving buyers exposed to fluctuations in Federal Reserve rate policies. An increase in interest rates can substantially raise monthly payments, making it challenging for price-sensitive households to afford these loans. Prime lending primarily favors individuals with strong credit scores, while subprime borrowers face higher annual percentage rates, further widening the affordability gap. Dealers are addressing this by extending loan terms for luxury coaches, but this strategy increases the risk of negative equity for owners who trade in before the loan term ends. Entry-level Class C units are being simplified by removing non-essential features to maintain affordability and ensure eligibility for conventional RV financing.

Other drivers and restraints analyzed in the detailed report include:

- Post-Pandemic Preference for Private Travel Modes

- OEM Electrified Chassis Platforms Hitting Cost Parity

- Service-Infrastructure Shortages Outside Developed Regions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Class C units commanded a 46.26% share of global deliveries in 2025, underpinned by 6- to 8-berth layouts that easily navigate 35-foot park limits. This slice of the motorhome market is favored by families seeking maneuverability and acceptable insurance premiums. Luxury Class A coaches, while smaller in volume, are projected to grow at a 9.32% CAGR as affluent retirees upgrade from towables. Manufacturers are enhancing differentiation with advanced systems and solar arrays, enabling the off-grid operation of rooftop air conditioners in response to tightening generator regulations. While Compact Class B vans cater to urban buyers seeking stealth parking and daily usability, their high pricing limits broader market penetration.

Developments in the second row are equally significant. Class C builders are now standardizing on innovative house batteries, reducing weight and extending autonomy. Meanwhile, Class B converters introduce pop-top roofs and slide-out galley areas, boosting headroom while staying within parking garage height limits. Luxury Class A models, equipped with smart-home suites that integrate with virtual assistants, not only echo home comfort standards but also maintain their premium pricing amidst ongoing economic challenges.

Retail buyers accounted for 60.28% of the 2025 volume, reflecting cultural preferences for customization and flexible travel schedules. Yet rental fleets are expanding faster, tracking a 9.09% CAGR through 2031 as digital marketplaces mainstream short-term access to high-ticket assets. The motorhome rental market is experiencing significant growth, driven by increased platform-provided liability coverage that reassures owners and high daily utilization rates, which enhance fleet ROI.

First-time buyers now account for a substantial portion of new registrations, with a younger demographic emerging compared to repeat purchasers. A large number of households expressing interest in motorhomes are expected to convert as financial conditions become more favorable. To address this demand, OEMs are offering features such as plug-and-play solar systems, video tutorials, and simplified plumbing layouts to reduce the learning curve. Fleet operators are also leveraging bulk discounts on large orders of Class C motorhomes, targeting corporate events and film crews, thereby maintaining consistent production levels.

Geography Analysis

North America accounted for 47.71% of 2025 revenue from U.S. wholesale shipments, which have declined due to inventory corrections. However, retail demand is stabilizing, supported by steady financing and an increasing number of younger, first-time buyers. With a significant number of RV-owning households and numerous campgrounds nationwide, the U.S. market remains strong. In Canada, regions like British Columbia and Alberta are enhancing amenities such as hookups and dump stations to attract retirees relocating from urban areas.

The Asia-Pacific region is the fastest-growing, with an 8.72% CAGR. Japan's reform allowing longer coaches on expressways has prompted local manufacturers, such as Annex, to increase production. Meanwhile, China's State Council has allocated subsidies to campgrounds in key regions, positioning RV tourism as a significant leisure focus. In India, the market is still developing, but a growing middle class and improved highway infrastructure are expected to drive future demand.

Europe remains a mature yet dynamic market, with Germany leading due to the opening of new year-round parks in popular regions. Low-emission zones in major cities like London and Paris are encouraging buyers to opt for compact Class B vans, which are better suited for urban environments. Coastal tourism is driving rental-fleet growth in Italy and Spain, while Eastern Europe benefits from lower shipping costs enabled by new manufacturing facilities in the region.

South America and the Middle East are still in the early stages of market development. In Brazil, import tariffs continue to drive up prices, but local producers are offering more affordable entry-level models. The United Arab Emirates and Saudi Arabia are investing in desert campgrounds to diversify their tourism offerings. Turkey is attracting OEMs with favorable tax policies, aiming to position itself as a key export hub for Europe.

- Thor Industries Inc.

- Winnebago Industries Inc.

- Forest River Inc.

- REV Group

- Erwin Hymer Group

- Jayco Inc.

- Tiffin Motorhomes Inc.

- Coachmen RV

- Newmar Corporation

- Leisure Travel Vans

- Dethleffs GmbH

- Hobby-Wohnwagenwerk

- Burstner GmbH & Co. KG

- Trigano S.A.

- Knaus Tabbert AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing RV-Centric Tourism Ecosystems

- 4.2.2 Rising Adoption of Remote-Work "Van-Life" Lifestyles

- 4.2.3 Post-Pandemic Preference for Private Travel Modes

- 4.2.4 Baby-Boomer Retirement Cohorts with High Disposable Income

- 4.2.5 OEM Electrified Chassis Platforms Hitting Cost Parity

- 4.2.6 Subscription-Based "RV-as-a-Service" Business Models

- 4.3 Market Restraints

- 4.3.1 High Retail Prices and Interest-Rate Sensitive Financing

- 4.3.2 Service-Infrastructure Shortages Outside Developed Regions

- 4.3.3 Battery-Pack Weight/Energy-Density Trade-Offs in E-Motorhomes

- 4.3.4 Rising Anti-Idling and Emission Regulations at Campsites

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size and Growth Forecasts (Value (USD) Volume (Units))

- 5.1 By Motorhome Class

- 5.1.1 Class A (Luxury)

- 5.1.2 Class B (Compact)

- 5.1.3 Class C (Mid-size)

- 5.2 By End User

- 5.2.1 Individual Buyers

- 5.2.2 Rental Companies

- 5.2.3 Fleet Operators

- 5.3 By Propulsion Type

- 5.3.1 Diesel

- 5.3.2 Gasoline

- 5.3.3 Electric

- 5.4 By Price Range

- 5.4.1 Economy

- 5.4.2 Mid-Range

- 5.4.3 Premium

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 South Africa

- 5.5.5.4 Turkey

- 5.5.5.5 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Thor Industries Inc.

- 6.4.2 Winnebago Industries Inc.

- 6.4.3 Forest River Inc.

- 6.4.4 REV Group

- 6.4.5 Erwin Hymer Group

- 6.4.6 Jayco Inc.

- 6.4.7 Tiffin Motorhomes Inc.

- 6.4.8 Coachmen RV

- 6.4.9 Newmar Corporation

- 6.4.10 Leisure Travel Vans

- 6.4.11 Dethleffs GmbH

- 6.4.12 Hobby-Wohnwagenwerk

- 6.4.13 Burstner GmbH & Co. KG

- 6.4.14 Trigano S.A.

- 6.4.15 Knaus Tabbert AG

7 Market Opportunities and Future Outlook

露營車和旅居車市場-全球市場預測(2026-2032年)

露營車和旅居車市場-全球市場預測(2026-2032年) 露營車和旅居車:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)

露營車和旅居車:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年) 房車和旅居車市場規模、佔有率和成長分析:按產品類型、燃料/驅動系統、最終用途/生命週期階段和地區分類-2026-2033年產業預測

房車和旅居車市場規模、佔有率和成長分析:按產品類型、燃料/驅動系統、最終用途/生命週期階段和地區分類-2026-2033年產業預測 露營車市場機會、成長要素、產業趨勢分析及2026-2035年預測。

露營車市場機會、成長要素、產業趨勢分析及2026-2035年預測。 露營車市場 - 全球產業規模、佔有率、趨勢、機會、預測:按類型、最終用戶、地區和競爭格局分類,2021-2031年

露營車市場 - 全球產業規模、佔有率、趨勢、機會、預測:按類型、最終用戶、地區和競爭格局分類,2021-2031年 房車和旅居車市場規模、佔有率、趨勢和預測:按產品類型、最終用戶和地區分類,2026-2034 年

房車和旅居車市場規模、佔有率、趨勢和預測:按產品類型、最終用戶和地區分類,2026-2034 年 2026年全球旅居車市場報告2026年全球旅居車車市場報告

2026年全球旅居車市場報告2026年全球旅居車車市場報告 露營車和旅居車市場:按產品和地區分類

露營車和旅居車市場:按產品和地區分類 全球旅居車市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球旅居車市場規模、佔有率、趨勢和成長分析報告(2026-2034)