|

市場調查報告書

商品編碼

2044272

日本工程塑膠:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)Japan Engineering Plastics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

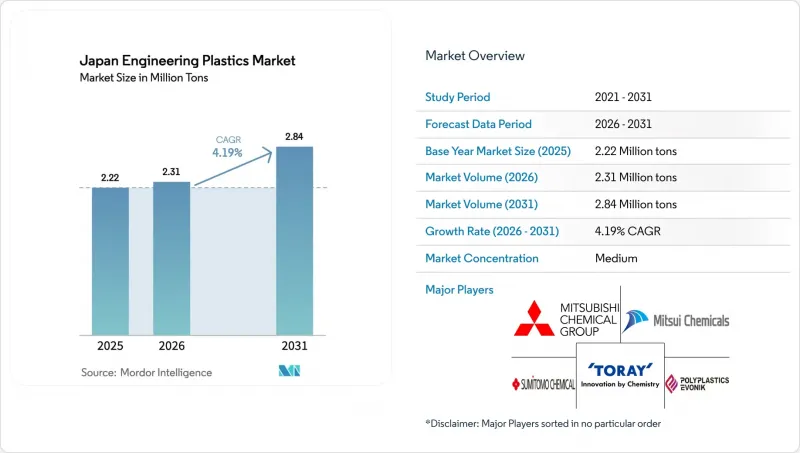

預計到 2025 年,日本工程塑膠市場將達到 222 萬噸,到 2026 年將達到 231 萬噸,到 2031 年將達到 284 萬噸,2026 年至 2031 年的複合年成長率為 4.19%。

隨著國內製造商退出與低價進口產品直接競爭的大規模生產,市場需求正從通用聚烯轉向用於5G基礎設施、醫療植入和氫電解等特種用途的聚烯烴。日本的價值鏈正從中部地區的汽車沖壓廠轉向關東地區的半導體封裝生產線以及東京都會圈生產高附加價值醫療設備的無塵室。投資集中在含氟聚合物、聚醯亞胺薄膜和不含PFAS的摩擦學聚醯胺上,因為這些細分市場不受中國產能過剩的影響,且擁有定價權。同時,通用樹脂製造商和射出成型之間的整合正在擴大高性能樹脂和普通樹脂之間的價格差距,小規模企業被擠出市場。

日本工程塑膠市場趨勢與洞察

5G與先進半導體封裝技術的激增

日本為實現半導體自給自足所做的努力,正促使每年超過1.5萬噸高純度含氟聚合物被重新用於等電漿蝕刻腔和化學品輸送管。 AGC公司位於千葉的工廠斥資350億日元進行擴建,預計將於2025年竣工,旨在透過提高乙烯-四氟乙烯(ETFE)和聚二氟亞乙烯(PVDF)的產能來滿足這一需求。凸版印刷和京瓷正在擴大厚度小於10微米的超薄聚醯亞胺薄膜的生產,這些薄膜用於先進的積體電路基板,這是一個利潤率比汽車樹脂高3到5倍的細分市場。宇部化學工業株式會社計劃在2030年將其聚醯亞胺產能加倍,同時退出其通用尼龍業務。這些發展正推動日本工程塑膠市場向低介電常數、耐熱聚合物轉型,而中國競爭對手目前尚無法以所需的純度水平進行大規模生產。

高齡化社會對醫療設備的需求

日本65歲以上人口占比高達28.6%,醫療設備逐漸成為經濟成長的支柱產業。 2025年,厚生勞動省核准了47種採用符合ISO 10993標準的聚合物製成的新型醫療設備。聚醚醚酮(PEEK)和聚碸因其能夠提供金屬材料無法實現的核磁共振相容和耐化學腐蝕性能,正在脊椎移植和透析膜領域擴大市場佔有率。旭化成計畫在2030年將其PIMEL聚醯亞胺的產能翻番,以滿足微創手術器械的需求。臨床領域的這些創新意味著樹脂的需求不再與GDP掛鉤,而是隨著高利潤率、生物相容性強的外科手術數量的成長而同步成長。

2023-2024年汽車產量下降

2025年11月,日本汽車月產量降至587,348輛,遠低於先前的高峰。此外,根據日本汽車零件工業協會(JAPIA)的記錄,2024年有36家供應商破產。這次經濟衰退對通用聚丙烯(PP)和ABS的打擊最為嚴重,同時也對PA66進氣歧管和PC頭燈透鏡的需求造成了壓力。倖存的模具製造商,例如新成立的GMS集團(由日精塑膠和東洋創新株式會社於2026年4月合併而成),目前佔據了更大的下游加工產能佔有率,從而減緩了新一代樹脂的普及應用。

細分市場分析

到2025年,包裝業將佔日本工程塑膠市場佔有率的28.89%,這主要得益於飲料和食品業對PET、PP和PS的消費量達到64萬噸。電子電氣產業預計在預測期(2026-2031年)內將以6.37%的複合年成長率成長,這主要得益於Rapidus和台積電晶圓廠產能的提升以及國內積體電路產量17%的成長。汽車產業雖然在體積上仍佔據較大佔有率,但其相對權重正在下降。然而,電動車每輛車需要30-40公斤高性能PPS、PPA和PEEK,彌補了與內燃機汽車(15-20公斤)之間的差距,從而支撐了日本工程塑膠在該領域的市場規模。

醫院向一次性醫療設備和機器人平台的轉變,拓展了滲透性的PEEK和耐消毒PSU的醫療應用範圍。建築業對PVC型材和PC玻璃的需求隨著住宅開工量的穩定而趨於平穩,而工業機械行業則因工廠數位化而維持著3-4%的年成長率。航太領域雖然規模較小,但也受益於NEDO(新能源產業技術綜合開發機構)的複合材料計劃,該計劃重點是發展高溫聚醯亞胺和碳纖維增強熱塑性塑膠。

《日本工程塑膠市場報告》依樹脂類型(含氟聚合物、液晶聚合物、聚醯胺、聚丁烯對苯二甲酸酯、聚碳酸酯、聚醚醚酮、聚醯亞胺、聚甲基丙烯酸甲酯等)及終端使用者產業(航太、汽車、建築、電氣電子、工業機械等)進行細分。市場預測以噸為單位。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 5G 和先進封裝技術的蓬勃發展

- 高齡化社會對醫療設備的需求

- 回收和循環經濟的合規要求

- PFAS 的逐步淘汰導致了摩擦學級 PA 的廣泛應用。

- 雲端基礎聚合物 CAE 可提升高周轉率SKU 的產量。

- 市場限制因素

- 2023-2024年汽車產量下降

- 含氟聚合物中 PFAS 法規的不確定性

- 國內射出成型中小企業基礎萎縮

- 價值鏈分析

- 監理情勢

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 競爭公司之間的競爭

- 新進入者的威脅

- 進出口趨勢

- 氟聚合物貿易

- 聚醯胺(PA)貿易

- 聚對苯二甲酸乙二酯(PET)的交易

- 聚甲基丙烯酸甲酯(PMMA)的交易

- 聚甲醛(POM)的交易

- 苯乙烯共聚物(ABS和SAN)的交易

- 價格趨勢

- 螢光樹脂

- 聚碳酸酯(PC)

- 聚對苯二甲酸乙二醇酯(PET)

- 聚甲醛(POM)

- 聚甲基丙烯酸甲酯(PMMA)

- 苯乙烯共聚物(ABS 和 SAN)

- 聚醯胺(PA)

- 回收利用概述

- 聚醯胺(PA)回收利用趨勢

- 聚碳酸酯(PC)回收利用趨勢

- 聚對苯二甲酸乙二醇酯(PET)的回收趨勢

- 苯乙烯共聚物(ABS和SAN)的回收趨勢

- 授權人概況

- 產品概覽

- 終端用戶領域的趨勢

- 航太(來自航太零件生產的銷售額)

- 汽車(汽車產量)

- 建築與施工(新建建築占地面積)

- 電氣和電子設備(電氣和電子設備生產銷售收入)

- 包裝(塑膠包裝量)

第5章 市場規模與成長預測

- 按最終用戶行業分類

- 車

- 電氣和電子

- 建築/施工

- 包裝

- 工業機械

- 航太

- 其他終端用戶產業

- 依樹脂類型

- 螢光樹脂

- 乙烯-四氟乙烯(ETFE)

- 氟化乙烯丙烯(FEP)

- 聚四氟乙烯(PTFE)

- 聚偏氟乙烯(PVF)

- 聚二氟亞乙烯(PVDF)

- 其他類型的樹脂

- 液晶聚合物

- 聚醯胺

- 芳香聚醯胺

- 聚醯胺(PA)6

- 聚醯胺(PA)66

- 聚鄰苯二甲醯胺

- 聚丁烯對苯二甲酸酯

- 聚碳酸酯

- 聚醚醚酮

- 聚對苯二甲酸乙二酯

- 聚醯亞胺

- 聚甲基丙烯酸甲酯

- 聚甲醛

- 苯乙烯共聚物(ABS 和 SAN)

- 螢光樹脂

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- AGC Inc.

- Asahi Kasei

- Daicel Corporation

- Daikin Industries Ltd.

- Idemitsu Kosan Co., Ltd.

- Kaneka Corporation

- Kuraray Co., Ltd.

- Kureha Corporation

- MCT PET Resin Co., Ltd.

- Mitsubishi Chemical Group Corporation

- Mitsui Chemicals, Inc.

- PBI Advanced Materials Co., Ltd.

- Polyplastics-Evonik Corporation

- Sumitomo Chemical Co., Ltd.

- Techno-UMG Co., Ltd.

- Teijin Limited

- TORAY INDUSTRIES INC.

- UBE Corporation

第7章 市場機會與未來展望

第8章:執行長面臨的主要策略挑戰:

The Japan Engineering Plastics Market size is projected to be 2.22 million tons in 2025, 2.31 million tons in 2026, and reach 2.84 million tons by 2031, growing at a CAGR of 4.19% from 2026 to 2031.

Demand is shifting from commodity polyolefins to specialty grades that serve 5G infrastructure, medical implants, and hydrogen-electrolysis equipment as domestic producers retreat from volumes that compete head-on with low-priced imports. Japan's value chain is migrating away from Chubu's automotive stamping plants toward Kanto's semiconductor packaging lines and metropolitan clean rooms that manufacture high-added-value medical devices. Investment is concentrating in fluoropolymers, polyimide films, and PFAS-free tribological polyamides because these niches are insulated from Chinese overcapacity and enjoy pricing power. Meanwhile, consolidation among commodity producers and injection molders is squeezing marginal players, creating wider spreads between high-performance resins and bulk grades.

Japan Engineering Plastics Market Trends and Insights

Surge in 5G and Advanced Semiconductor Packaging

Japan's drive for semiconductor sovereignty is redirecting more than 15,000 tons per year of high-purity fluoropolymers into plasma-etch chambers and chemical-delivery tubing. AGC's JPY 35 billion expansion at Chiba, completed in 2025, increased Ethylenetetrafluoroethylene (ETFE) and Polyvinylidene Fluoride (PVDF) capacity expressly for this demand. TOPPAN and Kyocera have ramped ultra-thin polyimide films below 10 µm for advanced IC substrates, a niche that commands three to five times the margin of automotive resins. UBE is doubling polyimide capacity by 2030 as it exits commodity nylon. These moves tilt the Japan engineering plastics market toward low-dielectric, heat-resistant polymers that Chinese competitors cannot yet mass-produce at required purity levels.

Aging-Society Demand for Medical Devices

Twenty-eight-point-six percent of Japan's population is over 65, transforming medical devices into a structural growth pillar. The Ministry of Health, Labour and Welfare approved 47 new device classifications in 2025 that rely on ISO-10993-compliant polymers. Polyether Ether Ketone (PEEK) and polysulfone are taking share in spinal implants and dialysis membranes because they enable MRI-compatible and chemically robust solutions that metals cannot offer. Asahi Kasei is doubling PIMEL polyimide capacity by 2030 to support minimally invasive surgical tools. Such clinical innovation decouples resin demand from GDP, linking growth instead to procedure adoption curves that favor high-margin biocompatible grades.

Automotive Output Contraction 2023-24

Monthly vehicle output fell to 587,348 units in November 2025, far below historical peaks, and Japan Auto Parts Industries Association (JAPIA) recorded 36 supplier bankruptcies in 2024. The slump hits commodity PP and ABS hardest, but it also crimps demand for PA66 intake manifolds and PC headlamp lenses. Surviving molders such as the newly formed GMS Group (created by the April 2026 Nissei Plastic-TOYO Innobex merger) now control larger shares of downstream conversion capacity, slowing diffusion of next-generation resins.

Other drivers and restraints analyzed in the detailed report include:

- Recycling and Circular-Economy Compliance Mandates

- PFAS Phase-Out Enabling PA Tribological Grades

- PFAS Regulatory Uncertainty for Fluoropolymers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Packaging held 28.89% of Japan Engineering Plastics market share in 2025, driven by beverage and food applications that consumed 640,000 tons of PET, PP, and PS. Electrical and Electronics is forecast to grow at a 6.37% CAGR during the forecast period (2026-2031), propelled by a 17% surge in domestic IC output as Rapidus and TSMC fabs ramp capacity. Automotive remains volume-heavy but is losing relative weight; however, each EV integrates 30-40 kg of high-performance PPS, PPA, and PEEK versus 15-20 kg in internal-combustion cars, cushioning the Japan Engineering Plastics market size for this segment.

Hospitals' shift to single-use devices and robotic platforms is boosting medical applications of radiolucent PEEK and sterilization-resistant PSU. Building and Construction demand for PVC profiles and PC glazing is stabilizing alongside residential starts, while Industrial Machinery is pacing 3-4% annual growth as factories digitize. Aerospace, though small, benefits from NEDO-funded composite programs that favor high-temperature polyimides and carbon-fiber-reinforced thermoplastics.

The Japan Engineering Plastics Market Report is Segmented by Resin Type (Fluoropolymer, Liquid Crystal Polymer, Polyamide, Polybutylene Terephthalate, Polycarbonate, Polyether Ether Ketone, Polyimide, Polymethyl Methacrylate, and More) and End-User Industry (Aerospace, Automotive, Building and Construction, Electrical and Electronics, Industrial and Machinery, and More). The Market Forecasts are Provided in Terms of Volume (Tons).

List of Companies Covered in this Report:

- AGC Inc.

- Asahi Kasei

- Daicel Corporation

- Daikin Industries Ltd.

- Idemitsu Kosan Co., Ltd.

- Kaneka Corporation

- Kuraray Co., Ltd.

- Kureha Corporation

- MCT PET Resin Co., Ltd.

- Mitsubishi Chemical Group Corporation

- Mitsui Chemicals, Inc.

- PBI Advanced Materials Co., Ltd.

- Polyplastics-Evonik Corporation

- Sumitomo Chemical Co., Ltd.

- Techno-UMG Co., Ltd.

- Teijin Limited

- TORAY INDUSTRIES INC.

- UBE Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in 5G and advanced semiconductor packaging

- 4.2.2 Ageing-society demand for medical devices

- 4.2.3 Recycling and circular-economy compliance mandates

- 4.2.4 PFAS phase-out enabling PA tribological grades

- 4.2.5 Cloud-based polymer CAE boosting high-turnover SKUs

- 4.3 Market Restraints

- 4.3.1 Automotive output contraction 2023-24

- 4.3.2 PFAS regulatory uncertainty for fluoropolymers

- 4.3.3 Shrinking domestic injection-molding SME base

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of Substitutes

- 4.6.4 Competitive Rivalry

- 4.6.5 Threat of New Entrants

- 4.7 Import and Export Trends

- 4.7.1 Fluoropolymer Trade

- 4.7.2 Polyamide (PA) Trade

- 4.7.3 Polyethylene Terephthalate (PET) Trade

- 4.7.4 Polymethyl Methacrylate (PMMA) Trade

- 4.7.5 Polyoxymethylene (POM) Trade

- 4.7.6 Styrene Copolymers (ABS and SAN) Trade

- 4.8 Price Trends

- 4.8.1 Fluoropolymer

- 4.8.2 Polycarbonate (PC)

- 4.8.3 Polyethylene Terephthalate (PET)

- 4.8.4 Polyoxymethylene (POM)

- 4.8.5 Polymethyl Methacrylate (PMMA)

- 4.8.6 Styrene Copolymers (ABS and SAN)

- 4.8.7 Polyamide (PA)

- 4.9 Recycling Overview

- 4.9.1 Polyamide (PA) Recycling Trends

- 4.9.2 Polycarbonate (PC) Recycling Trends

- 4.9.3 Polyethylene Terephthalate (PET) Recycling Trends

- 4.9.4 Styrene Copolymers (ABS and SAN) Recycling Trends

- 4.10 Licensors Overview

- 4.11 Production Overview

- 4.12 End-use Sector Trends

- 4.12.1 Aerospace (Aerospace Component Production Revenue)

- 4.12.2 Automotive (Automobile Production)

- 4.12.3 Building and Construction (New Construction Floor Area)

- 4.12.4 Electrical and Electronics (Electrical and Electronics Production Revenue)

- 4.12.5 Packaging (Plastic Packaging Volume)

5 Market Size and Growth Forecasts (Volume)

- 5.1 By End-User Industry

- 5.1.1 Automotive

- 5.1.2 Electrical and Electronics

- 5.1.3 Building and Construction

- 5.1.4 Packaging

- 5.1.5 Industrial and Machinery

- 5.1.6 Aerospace

- 5.1.7 Other End-User Industries

- 5.2 By Resin Type

- 5.2.1 Fluoropolymers

- 5.2.1.1 Ethylenetetrafluoroethylene (ETFE)

- 5.2.1.2 Fluorinated Ethylene-propylene (FEP)

- 5.2.1.3 Polytetrafluoroethylene (PTFE)

- 5.2.1.4 Polyvinylfluoride (PVF)

- 5.2.1.5 Polyvinylidene Fluoride (PVDF)

- 5.2.1.6 Other Sub Resin Types

- 5.2.2 Liquid Crystal Polymer

- 5.2.3 Polyamide

- 5.2.3.1 Aramid

- 5.2.3.2 Polyamide (PA) 6

- 5.2.3.3 Polyamide (PA) 66

- 5.2.3.4 Polyphthalamide

- 5.2.4 Polybutylene Terephthalate

- 5.2.5 Polycarbonate

- 5.2.6 Polyether Ether Ketone

- 5.2.7 Polyethylene Terephthalate

- 5.2.8 Polyimide

- 5.2.9 Polymethyl Methacrylate

- 5.2.10 Polyoxymethylene

- 5.2.11 Styrene Copolymers (ABS and SAN)

- 5.2.1 Fluoropolymers

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 AGC Inc.

- 6.4.2 Asahi Kasei

- 6.4.3 Daicel Corporation

- 6.4.4 Daikin Industries Ltd.

- 6.4.5 Idemitsu Kosan Co., Ltd.

- 6.4.6 Kaneka Corporation

- 6.4.7 Kuraray Co., Ltd.

- 6.4.8 Kureha Corporation

- 6.4.9 MCT PET Resin Co., Ltd.

- 6.4.10 Mitsubishi Chemical Group Corporation

- 6.4.11 Mitsui Chemicals, Inc.

- 6.4.12 PBI Advanced Materials Co., Ltd.

- 6.4.13 Polyplastics-Evonik Corporation

- 6.4.14 Sumitomo Chemical Co., Ltd.

- 6.4.15 Techno-UMG Co., Ltd.

- 6.4.16 Teijin Limited

- 6.4.17 TORAY INDUSTRIES INC.

- 6.4.18 UBE Corporation

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment

8 Key Strategic Questions for CEOs

全球聚甲醛市場

全球聚甲醛市場 工程塑膠,全球,2025–2032 年

工程塑膠,全球,2025–2032 年 工程塑膠市場:按產品類型、加工技術、形狀和應用分類的全球市場預測-2026-2032年聚甲醛市場:2026-2032年全球市場預測(依產品類型、等級、加工技術、應用及通路分類)

工程塑膠市場:按產品類型、加工技術、形狀和應用分類的全球市場預測-2026-2032年聚甲醛市場:2026-2032年全球市場預測(依產品類型、等級、加工技術、應用及通路分類) 工程塑膠市場報告:按類型、性能參數、應用和地區分類(2026-2034 年)

工程塑膠市場報告:按類型、性能參數、應用和地區分類(2026-2034 年) 工程塑膠市場:按產品類型、應用和地區分類

工程塑膠市場:按產品類型、應用和地區分類 全球高性能塑膠化合物市場-按塑膠類型、添加劑類型、最終用途產業和地區分類-預測(至2030年)

全球高性能塑膠化合物市場-按塑膠類型、添加劑類型、最終用途產業和地區分類-預測(至2030年) 先進工程熱塑性塑膠市場預測至2034年-按產品類型、加工技術、應用和地區分類的全球分析

先進工程熱塑性塑膠市場預測至2034年-按產品類型、加工技術、應用和地區分類的全球分析 印度工程塑膠:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)全球聚甲醛樹脂市場規模、佔有率、趨勢和成長分析報告(2026-2034)

印度工程塑膠:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)全球聚甲醛樹脂市場規模、佔有率、趨勢和成長分析報告(2026-2034)