|

市場調查報告書

商品編碼

2044271

印度工程塑膠:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)India Engineering Plastics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

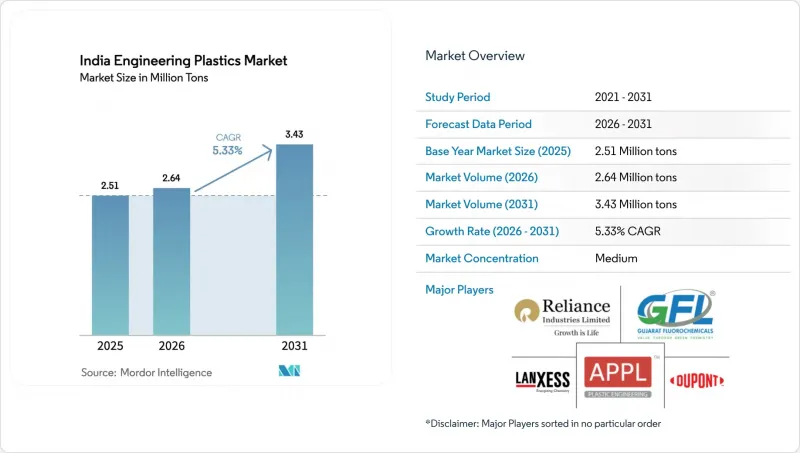

印度工程塑膠市場預計將從 2025 年的 251 萬噸成長到 2026 年的 264 萬噸,然後從 2026 年到 2031 年以 5.33% 的複合年成長率成長,到 2031 年達到 343 萬噸。

飲料、食品和電子商務產業對硬質和軟質包裝材料的需求仍然強勁。然而,在電氣電子設備和出行領域,高階組件的需求正在顯著成長。政府的各項舉措,例如生產連結獎勵計畫(PLI)支出,以及電動車(EV)生產基地的擴張和對再生材料含量的嚴格監管,正在顯著加快樹脂的普及應用週期。過去需要近10年的時間,現在縮短至約5年。這種快速轉變體現在阻燃聚醯胺、聚碳酸酯-ABS共混物和含氟聚合物等級的成長。 2026年至2031年間,國內產能擴張將主要集中在PET、ABS和標準聚醯胺6。然而,印度仍然嚴重依賴進口來滿足其大部分特種聚合物的需求。這種高度依賴性使加工商面臨外匯波動和運輸延誤的風險。

印度工程塑膠市場趨勢與洞察

更輕的汽車和電動車的快速發展

預計2024年至2033年間,印度電動車銷量將大幅成長,這將帶動汽車聚合物需求的激增。汽車製造商正擴大採用玻璃纖維增強聚醯胺66、聚鄰苯二甲醯胺和阻燃聚碳酸酯-ABS等材料來取代傳統的金屬外殼。這種轉變正成為電池外殼、電力電子模組和溫度控管歧管的關鍵選擇,不僅可以減輕車輛重量,還能延長電動車的續航里程。塔塔汽車和馬恆達汽車在新型電動車平台上工程塑膠的使用方面處於領先地位,其使用速度是同類內燃機車型的兩倍。目前,印度國內聚醯胺66的生產面臨產能限制,而價值鏈上的各個參與企業都依賴進口己內醯胺和己二酸等中間體。儘管邦薩裡工程聚合物公司(Bangsari Engineering Polymers)的擴建計畫預計將於2028年完成,但對進口的依賴阻礙了潛在的成本降低。從2027年開始,能源效率局將收緊企業平均燃油經濟性(CAFE)標準。預計此舉將進一步加速車門模組、儀錶群和座椅結構等零件從塑膠轉向金屬的轉變。

政府對特種聚合物的生產關聯獎勵

到2025年12月,生產關聯激勵計畫(PLI)下的支出已達到相當可觀的水平,多個待開發區項目在以電子、電池和特種化學品為重點的產業走廊啟動。富士康、三星和塔塔電子等大型企業已承諾從國內市場採購聚碳酸酯外殼、液晶聚合物連接器和PVDF黏合劑等零件,這標誌著它們顯著減少了對進口的依賴。資金雄厚的「先進化學電池生產關聯激勵計畫」為陰極黏合劑和隔膜塗層等應用領域創造了PVDF和PTFE的巨大年度需求。古吉拉突邦的達赫傑-巴多達拉地區和卡納塔克邦的班加羅爾產業叢集的發展勢頭最為強勁。在這些地區,土地補貼和優惠的電價使樹脂生產商能夠降低營運成本。尤其值得一提的是,自2020-2021年以來行動電話進口量的顯著下降凸顯了在地化措施在一個投資週期內重塑貿易平衡的巨大潛力。

原物料價格波動(對甲苯、苯、氫氟酸)

對二甲苯價格波動劇烈,苯價格在短期內也經歷了大幅波動。這些價格波動擠壓了聚酯和聚醯胺生產商的利潤空間。為了維持價差,信實工業和古吉拉突邦化肥化工公司已將價格調整頻率從季度調整改為月度調整。然而,這項變化加劇了營運資金緊張,並對下游業務產生了負面影響。同時,由於中國推出了新的環保法規,作為聚四氟乙烯(PTFE)和聚偏氟乙烯(PVDF)生產關鍵原料的氫氟酸供應趨緊。因此,古吉拉突邦氟化工公司以高於常規平均價格的溢價簽訂了多年期供應合約。此外,通常不進行避險的中小型混煉企業已將新擠出生產線的投產推遲數月。這種延遲阻礙了用於5G天線和電動汽車電池密封件等新興應用的樹脂產品的商業化。

細分市場分析

2025年,包裝產業在印度工程塑膠市場主導主導地位,市佔率高達57.12%。這一成長趨勢得益於蓬勃發展的國內包裝產業,該產業巧妙地滿足了快速都市化、食品配送服務和有組織零售業的需求。隨著軟性飲料、飲用水和乳製品行業的企業為rPET強制使用做好準備, 寶特瓶的產量穩定成長。軟性多層薄膜如今已成為包裝總噸位中的重要組成部分,它透過結合EVOH和聚醯胺隔離層,延長了休閒食品的保存期限。儘管電子製造業在2025年的產量佔有率較小,但預計在2026年至2031年的預測期內,其複合年成長率將達到8.55%。這一成長預期主要得益於生產關聯激勵(PLI)計劃,該計劃促進了智慧型手機、白色家電和穿戴式裝置的國內組裝。隨著印刷電路基板(PCB)和印刷天線的加入,對耐熱液晶聚合物(LCP)和聚生產連結獎勵計畫(PBT)的需求顯著成長。汽車產業正在加大電動車聚合物的使用,從傳統材料轉向光學級聚碳酸酯,用於電池組、電連接器和外玻璃等零件。建築業也在大量使用CPVC管道、PMMA玻璃和聚碳酸酯屋頂材料,在「智慧城市計畫」和「總理住宅計畫」等舉措的推動下,這些材料的需求量顯著成長。

隨著電子商務趨勢的演變,包裝產業正經歷著向輕量化和可回收方向的顯著轉變。這一趨勢使得單組分乙二醇改質PET和聚烯阻隔薄膜等細分市場備受關注。品牌商對防竄改瓶和雷射雕刻瓶蓋的需求不斷成長,推動了特種聚縮醛和熱可塑性橡膠需求的激增。與蘋果和三星等大型公司密切相關的電子產業正在大幅減少對進口阻燃ABS的依賴。汽車產業對輕量化的重視推動了對玻璃纖維增強PA 66和聚鄰苯二甲醯胺引擎蓋的需求激增。此外,抗衝擊聚碳酸酯正成為摩托車電池外殼的標準材料。建築業的蓬勃發展,尤其是地方政府供水工程,也顯著增加了對CPVC和UPVC管道的需求。在工業機械領域,從軸承到輸送機系統,低摩擦 POM 和芳香聚醯胺增強 PA 6 的應用日益廣泛,以提高耐磨性,儘管高性能等級的產品仍然嚴重依賴進口。

《印度工程塑膠市場報告》按終端用戶產業(汽車、電氣電子、建築、包裝、工業機械、航太及其他終端用戶產業)及樹脂類型(含氟聚合物、液晶聚合物、聚醯胺、聚對聚丁烯對苯二甲酸酯、聚碳酸酯、聚醚醚酮及其他)進行細分。市場預測以噸為單位。

其他好處

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 汽車輕量化趨勢和電動車的日益普及

- 政府對特種聚合物的生產關聯獎勵

- 電子製造業的快速成長

- 飲料瓶必須使用食品級rPET材料。

- 工業纖維和紡織品出口快速成長

- 市場限制因素

- 原物料價格波動(對甲苯、苯、氫氟酸)

- 生產者責任延伸制度(EPR)以及因再生材料含量法規而產生的合規成本。

- 對經認證的回收基礎設施投資不足

- 價值鏈分析

- 監理情勢

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 競爭公司之間的競爭

- 新進入者的威脅

- 進出口趨勢

- 氟聚合物貿易

- 聚醯胺(PA)貿易

- 聚對苯二甲酸乙二酯(PET)貿易

- 聚甲基丙烯酸甲酯(PMMA)貿易

- 聚甲醛(POM)貿易

- 苯乙烯共聚物(ABS 和 SAN)的貿易

- 價格趨勢

- 螢光樹脂

- 聚碳酸酯(PC)

- 聚對苯二甲酸乙二醇酯(PET)

- 聚甲醛(POM)

- 聚甲基丙烯酸甲酯(PMMA)

- 苯乙烯共聚物(ABS 和 SAN)

- 聚醯胺(PA)

- 回收利用概述

- 聚醯胺(PA)回收利用趨勢

- 聚碳酸酯(PC)回收利用趨勢

- 聚對苯二甲酸乙二醇酯(PET)回收趨勢

- 苯乙烯共聚物(ABS和SAN)回收趨勢

- 授權人概覽

- 產品概覽

- 終端用戶產業的趨勢

- 航太(航太零件生產銷售)

- 汽車(汽車產量)

- 建築與施工(新建建築占地面積)

- 電氣和電子設備(電氣和電子設備生產銷售收入)

- 包裝(塑膠包裝)

第5章 市場規模與成長預測

- 按最終用戶行業分類

- 車

- 電氣和電子

- 建築/施工

- 包裝

- 工業機械

- 航太

- 其他

- 依樹脂類型

- 螢光樹脂

- 乙烯-四氟乙烯(ETFE)

- 氟化乙烯丙烯(FEP)

- 聚四氟乙烯(PTFE)

- 聚偏氟乙烯(PVF)

- 聚二氟亞乙烯(PVDF)

- 其他樹脂類型

- 液晶聚合物

- 聚醯胺

- 芳香聚醯胺

- 聚醯胺(PA)6

- 聚醯胺(PA)66

- 聚鄰苯二甲醯胺

- 聚丁烯對苯二甲酸酯

- 聚碳酸酯

- 聚醚醚酮

- 聚對苯二甲酸乙二酯

- 聚醯亞胺

- 聚甲基丙烯酸甲酯

- 聚甲醛

- 苯乙烯共聚物(ABS 和 SAN)

- 螢光樹脂

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- APPL Industries Limited

- Bhansali Engineering Polymers Ltd.

- DuPont

- Gujarat Fluorochemicals Limited(GFL)

- Gujarat State Fertilizers & Chemicals Limited(GSFC)

- INEOS

- IVL Dhunseri Petrochem Industries Private Limited(IDPIPL)

- Kingfa Science & Technology (India) Limited

- LANXESS

- Mitsubishi Chemical Group

- Polyplex Corporation Ltd.

- Reliance Industries Ltd

- Styrenix Performance Materials Limited

- JBF Industries Ltd

- CHIRIPAL POLY FILM

第7章 市場機會與未來展望

第8章:執行長面臨的主要策略挑戰:

The Indian Engineering Plastics Market size is expected to grow from 2.51 million tons in 2025 to 2.64 million tons in 2026 and is forecast to reach 3.43 million tons by 2031 at 5.33% CAGR over 2026-2031.

Demand for rigid and flexible packaging remains robust across the beverage, food, and e-commerce sectors. However, there is a notable pivot towards premium components in the electrical, electronics, and mobility domains. Government initiatives, such as the Production Linked Incentive (PLI) outlays, alongside a growing electric vehicle (EV) production base and stringent recycled content mandates, have drastically accelerated resin-adoption cycles. What previously required nearly a decade has now been reduced to approximately five years. This swift transition is highlighted by the expanding grades in flame-retardant polyamides, polycarbonate-ABS blends, and fluoropolymers. Between 2026 and 2031, domestic capacity expansions have focused on PET, ABS, and standard polyamide 6. However, India continues to depend on imports for a considerable portion of its specialty polymers. This reliance makes converters vulnerable to foreign exchange fluctuations and potential shipping delays.

India Engineering Plastics Market Trends and Insights

Automotive Light-Weighting and Electric-Vehicle Adoption Boom

From 2024 to 2033, India's EV sales are projected to surge, driving up the demand for polymers in vehicles. OEMs are increasingly opting for materials such as glass-fiber-reinforced polyamide 66, polyphthalamide, and flame-retardant polycarbonate-ABS, replacing traditional metal housings. This shift not only reduces curb weight but also enhances the EV driving range, making it a pivotal choice for battery enclosures, power-electronics modules, and thermal-management manifolds. Tata Motors and Mahindra are leading the charge, specifying a higher content of engineering plastics in their new EV platforms, which doubles the content used in comparable internal-combustion models. While domestic production of PA 66 faces capacity constraints, the value-chain players are turning to imports for intermediates such as caprolactam and adipic acid. This reliance on imports tempers potential cost reductions, even with Bhansali Engineering Polymers planning an expansion set to conclude in 2028. Starting in 2027, the Bureau of Energy Efficiency is tightening Corporate Average Fuel Economy (CAFE) norms. This policy is expected to further accelerate the shift from plastic to metal in components such as door modules, instrument clusters, and seat structures.

Government PLI Incentives for Specialty Polymers

By December 2025, disbursements under the PLI scheme reached significant levels, leading to the establishment of multiple greenfield projects in corridors focused on electronics, batteries, and specialty chemicals. Major players such as Foxconn, Samsung, and Tata Electronics are committed to sourcing components, including polycarbonate housings, liquid-crystal-polymer connectors, and PVDF binders, from domestic markets. This marked a significant shift from their earlier reliance on imports. The Advanced Chemistry Cell PLI, with substantial funding, created a considerable demand for PVDF and PTFE annually for applications such as cathode binders and separator coatings. The Dahej-Vadodara belt in Gujarat and the Bengaluru cluster in Karnataka experienced the most momentum. In these regions, land subsidies and favorable power tariffs enabled resin manufacturers to reduce operating costs. Notably, mobile-phone import volumes had significantly declined since FY 2020-21, underscoring the potential of localization efforts to reshape trade balances within a single investment cycle.

Feedstock Price Volatility (PX, Benzene, HF)

Paraxylene prices have exhibited significant fluctuations, and benzene prices have also experienced notable swings in a short timeframe. These price movements have compressed margins for polyester and polyamide producers. In a bid to safeguard their spreads, Reliance Industries and Gujarat State Fertilizers & Chemicals transitioned from quarterly to monthly price adjustments. However, this shift has strained their working capital, adversely affecting downstream operations. Meanwhile, hydrofluoric acid, a critical feedstock for PTFE and PVDF production, has experienced a tightening supply due to new environmental restrictions implemented in China. As a result, Gujarat Fluorochemicals has entered into multi-year supply contracts at a premium over previous averages. Furthermore, smaller compounders, who typically do not hedge, postponed their new extrusion lines by several months. This postponement has hindered the commercialization of resin grades for emerging applications, including 5G antennas and EV battery seals.

Other drivers and restraints analyzed in the detailed report include:

- Surge in Electronics Manufacturing

- Food-Grade rPET Mandate for Beverage Bottles

- Compliance Costs from EPR and Recycled-Content Rules

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, packaging took the lead in India's engineering plastics market, securing a commanding 57.12% share. This upswing was fueled by a dynamic domestic packaging sector, skillfully addressing the needs of swift urbanization, food delivery services, and organized retail. As companies in the soft drink, water, and dairy sectors geared up for the rPET mandate, production of PET bottles saw a consistent rise. Flexible multi-layer films, now a significant segment of total packaging tonnage, are enhanced with EVOH and polyamide barriers to extend the shelf life of snack foods. Although electronics manufacturing represented a smaller slice of the 2025 volume, it is set to expand at an 8.55% CAGR through the 2026-2031 forecast period. This anticipated growth is driven by PLI incentives that bolster the domestic assembly of smartphones, white goods, and wearables. Each addition of a PCB or printed antenna notably heightens the demand for high-temperature LCP and PBT. The automotive sector is ramping up its polymer usage for electric vehicles (EVs), favoring optical-grade polycarbonate for components like battery packs, electrical connectors, and exterior glazing, moving away from traditional materials. The construction sector, leveraging CPVC pipes, PMMA glazing, and polycarbonate roofing, is a major consumer, spurred by initiatives like the Smart Cities Mission and PM Awas Yojana housing projects.

As e-commerce trends evolve, there is a noticeable shift in packaging towards lighter, recyclable formats. This evolution has spotlighted niches for monomaterial glycol-modified PET and polyolefin-based barrier films. Brand owners' push for tamper-evident bottles and laser-engraved closures has spiked the demand for specialty polyacetal and thermoplastic elastomers. The electronics sector, closely tied to major players like Apple and Samsung, has seen a marked decrease in the country's dependence on imported flame-retardant ABS. The automotive industry's drive for lightweight components has led to a surge in demand for glass-fiber-reinforced PA 66 and polyphthalamide engine covers. Additionally, impact-modified polycarbonate is becoming the go-to for two-wheeler battery casings. With a construction boom underway, especially in municipal water projects, there has been a notable uptick in the demand for CPVC and UPVC pipes. Industrial machinery, from bearings to conveyor systems, is increasingly opting for low-friction POM and aramid-reinforced PA 6 to boost wear resistance, though there is still a significant dependence on imports for advanced grades.

The India Engineering Plastics Market Report is Segmented by End-User Industry (Automotive, Electrical and Electronics, Building and Construction, Packaging, Industrial and Machinery, Aerospace, and Other End-User Industries), Resin Type (Fluoropolymers, Liquid Crystal Polymer, Polyamide, Polybutylene Terephthalate, Polycarbonate, Polyether Ether Ketone, and More). Market Forecasts are Provided in Terms of Volume (Tons).

List of Companies Covered in this Report:

- APPL Industries Limited

- Bhansali Engineering Polymers Ltd.

- DuPont

- Gujarat Fluorochemicals Limited (GFL)

- Gujarat State Fertilizers & Chemicals Limited (GSFC)

- INEOS

- IVL Dhunseri Petrochem Industries Private Limited (IDPIPL)

- Kingfa Science & Technology (India) Limited

- LANXESS

- Mitsubishi Chemical Group

- Polyplex Corporation Ltd.

- Reliance Industries Ltd

- Styrenix Performance Materials Limited

- JBF Industries Ltd

- CHIRIPAL POLY FILM

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Automotive Light-weighting and Electric Vehicle Adoption Boom

- 4.2.2 Government PLI Incentives for Specialty Polymers

- 4.2.3 Surge in Electronics Manufacturing

- 4.2.4 Food-grade rPET Mandate for Beverage Bottles

- 4.2.5 Rapid Growth of Technical-textile and Fiber Exports

- 4.3 Market Restraints

- 4.3.1 Feedstock Price Volatility (PX, Benzene, HF)

- 4.3.2 Compliance Costs from EPR and Recycled-content Rules

- 4.3.3 Under-investment in Certified Recycling Infrastructure

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of Substitutes

- 4.6.4 Competitive Rivalry

- 4.6.5 Threat of New Entrants

- 4.7 Import and Export Trends

- 4.7.1 Fluoropolymer Trade

- 4.7.2 Polyamide (PA) Trade

- 4.7.3 Polyethylene Terephthalate (PET) Trade

- 4.7.4 Polymethyl Methacrylate (PMMA) Trade

- 4.7.5 Polyoxymethylene (POM) Trade

- 4.7.6 Styrene Copolymers (ABS and SAN) Trade

- 4.8 Price Trends

- 4.8.1 Fluoropolymer

- 4.8.2 Polycarbonate (PC)

- 4.8.3 Polyethylene Terephthalate (PET)

- 4.8.4 Polyoxymethylene (POM)

- 4.8.5 Polymethyl Methacrylate (PMMA)

- 4.8.6 Styrene Copolymers (ABS and SAN)

- 4.8.7 Polyamide (PA)

- 4.9 Recycling Overview

- 4.9.1 Polyamide (PA) Recycling Trends

- 4.9.2 Polycarbonate (PC) Recycling Trends

- 4.9.3 Polyethylene Terephthalate (PET) Recycling Trends

- 4.9.4 Styrene Copolymers (ABS and SAN) Recycling Trends

- 4.10 Licensors Overview

- 4.11 Production Overview

- 4.12 End-use Sector Trends

- 4.12.1 Aerospace (Aerospace Component Production Revenue)

- 4.12.2 Automotive (Automobile Production)

- 4.12.3 Building and Construction (New Construction Floor Area)

- 4.12.4 Electrical and Electronics (Electrical and Electronics Production Revenue)

- 4.12.5 Packaging (Plastic Packaging Volume)

5 Market Size and Growth Forecasts (Volume)

- 5.1 By End-User Industry

- 5.1.1 Automotive

- 5.1.2 Electrical and Electronics

- 5.1.3 Building and Construction

- 5.1.4 Packaging

- 5.1.5 Industrial and Machinery

- 5.1.6 Aerospace

- 5.1.7 Other End-User Industries

- 5.2 By Resin Type

- 5.2.1 Fluoropolymers

- 5.2.1.1 Ethylenetetrafluoroethylene (ETFE)

- 5.2.1.2 Fluorinated Ethylene-propylene (FEP)

- 5.2.1.3 Polytetrafluoroethylene (PTFE)

- 5.2.1.4 Polyvinylfluoride (PVF)

- 5.2.1.5 Polyvinylidene Fluoride (PVDF)

- 5.2.1.6 Other Sub Resin Types

- 5.2.2 Liquid Crystal Polymer

- 5.2.3 Polyamide

- 5.2.3.1 Aramid

- 5.2.3.2 Polyamide (PA) 6

- 5.2.3.3 Polyamide (PA) 66

- 5.2.3.4 Polyphthalamide

- 5.2.4 Polybutylene Terephthalate

- 5.2.5 Polycarbonate

- 5.2.6 Polyether Ether Ketone

- 5.2.7 Polyethylene Terephthalate

- 5.2.8 Polyimide

- 5.2.9 Polymethyl Methacrylate

- 5.2.10 Polyoxymethylene

- 5.2.11 Styrene Copolymers (ABS and SAN)

- 5.2.1 Fluoropolymers

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 APPL Industries Limited

- 6.4.2 Bhansali Engineering Polymers Ltd.

- 6.4.3 DuPont

- 6.4.4 Gujarat Fluorochemicals Limited (GFL)

- 6.4.5 Gujarat State Fertilizers & Chemicals Limited (GSFC)

- 6.4.6 INEOS

- 6.4.7 IVL Dhunseri Petrochem Industries Private Limited (IDPIPL)

- 6.4.8 Kingfa Science & Technology (India) Limited

- 6.4.9 LANXESS

- 6.4.10 Mitsubishi Chemical Group

- 6.4.11 Polyplex Corporation Ltd.

- 6.4.12 Reliance Industries Ltd

- 6.4.13 Styrenix Performance Materials Limited

- 6.4.14 JBF Industries Ltd

- 6.4.15 CHIRIPAL POLY FILM

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment

8 Key Strategic Questions for CEOs

高性能聚合物(PEEK、PEI)市場預測(2034 年)—按聚合物類型、形態、等級、加工技術、應用、最終用戶和地區分類的全球分析

高性能聚合物(PEEK、PEI)市場預測(2034 年)—按聚合物類型、形態、等級、加工技術、應用、最終用戶和地區分類的全球分析 聚甲醛市場:全球市場預測,2026-2032年

聚甲醛市場:全球市場預測,2026-2032年 2026 年至 2035 年木質素基工程塑膠的市場機會、成長要素、產業趨勢分析與預測。工程塑膠市場:2026-2032年全球市場預測(依產品類型、加工技術、形狀、原料及應用分類)工程塑膠市場預測至2034年-全球分析(按樹脂類型、產品形式、加工技術、性能、應用、終端用戶產業和地區分類)

2026 年至 2035 年木質素基工程塑膠的市場機會、成長要素、產業趨勢分析與預測。工程塑膠市場:2026-2032年全球市場預測(依產品類型、加工技術、形狀、原料及應用分類)工程塑膠市場預測至2034年-全球分析(按樹脂類型、產品形式、加工技術、性能、應用、終端用戶產業和地區分類) 工程塑膠,全球,2025–2032 年

工程塑膠,全球,2025–2032 年 工程塑膠市場報告:按類型、性能參數、應用和地區分類(2026-2034 年)

工程塑膠市場報告:按類型、性能參數、應用和地區分類(2026-2034 年) 工程塑膠市場:按產品類型、應用和地區分類

工程塑膠市場:按產品類型、應用和地區分類 全球高性能塑膠化合物市場-按塑膠類型、添加劑類型、最終用途產業和地區分類-預測(至2030年)先進工程熱塑性塑膠市場預測至2034年-按產品類型、加工技術、應用和地區分類的全球分析

全球高性能塑膠化合物市場-按塑膠類型、添加劑類型、最終用途產業和地區分類-預測(至2030年)先進工程熱塑性塑膠市場預測至2034年-按產品類型、加工技術、應用和地區分類的全球分析