|

市場調查報告書

商品編碼

2044267

歐洲建築塗料市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Europe Architectural Coatings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

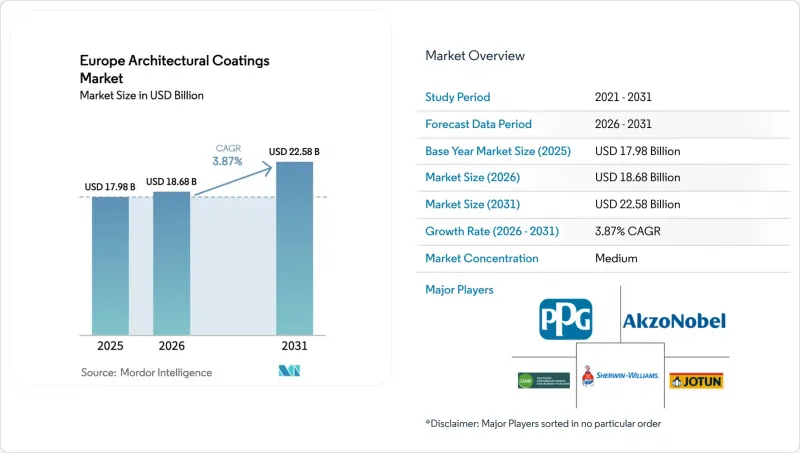

歐洲建築塗料市場預計將從 2025 年的 179.8 億美元成長到 2026 年的 186.8 億美元,到 2031 年達到 225.8 億美元。

預計從 2026 年到 2031 年,年複合成長率將達到 3.87%。

隨著買家積極應對歐盟日益嚴格的揮發性有機化合物(VOC)排放上限規定,以及建築存量平均超過50年,消費者開始謹慎地轉向高價值、低排放配方,這種趨勢正逐漸超越單純的銷售成長。水性塗料的需求已成為主流,專業油漆工更青睞低氣味、易於清潔的產品,而零售商為了規避合規風險,也已停止銷售許多溶劑型產品。供應商也將業務重心轉向維修和維修項目,因為這些項目的利潤比新建項目更為穩定,而新建項目由於高利率,盈利相對較低。主要製造商之間的整合正在加速,以分攤原料價格飆升帶來的成本負擔,投資於環保研發開發平臺,並擴大市場規模。

歐洲建築塗料市場趨勢與洞察

老舊住宅存量維修熱潮興起。

歐洲有超過2.2億套住宅建於1990年之前,其中許多房屋需要進行外牆修繕、防潮處理和內部維修,才能達到現代衛生標準。根據歐盟統計局的數據,預計到2025年,住宅維修支出將達到3,100億歐元,比前一年增加12%。法國、德國、義大利和西班牙的支出佔總支出的60%,其中義大利的支出增加了20%,這主要得益於節能塗料的慷慨稅額扣抵。歐洲議會的目標是到2030年將年度維修率提高一倍,達到2%,這將推動對高耐久性丙烯酸和聚氨酯塗料的需求,這些塗料可以將重新粉刷的周期從7年延長至12年。因此,歐洲建築塗料市場在維持整體強勁成長的同時,正持續向高利潤細分市場轉型。

歐盟的VOC法規正在加速向水性塗料的轉變。

2026年2月,歐盟委員會修訂了歐盟生態標籤法規,降低了揮發性有機化合物(VOC)和半揮發性有機化合物(SVOC)的上限值,並增加了適用性測試,以遏制黏合劑稀釋。零售商迅速停止銷售不符合法規的溶劑型產品線。到2025年底,水性產品佔裝飾塗料銷售量的70%,五年內成長了5個百分點。目前,純丙烯酸乳液在內牆塗料領域佔據主導地位,而苯乙烯-丙烯酸混合物則逐漸轉向價格較低的室外塗料。在2025年的一項試驗測試中,BASF、阿克蘇諾貝爾和阿科瑪證實,生物基樹脂可有效減少塗料40%的碳足跡。這些進展表明,更嚴格的法規不僅會加速水性塗料的普及,還會提高缺乏研發規模的中小型化合物生產商的進入門檻。因此,歐洲建築塗料市場正在向擁有科學永續性記錄的大型成熟公司轉變。

二氧化鈦和石油基原料價格的波動

2025年,二氧化鈦(TiO2)現貨價格在每噸2800歐元至3400歐元之間波動,漲幅高達21%,這擠壓了大眾市場內牆乳化的毛利率。製造商透過添加填料顏料和複合遮光劑來抵消部分價格上漲的影響,但使用這些替代品會帶來耐磨性和高濃度著色時色彩還原度下降的風險。同時,丙烯酸單體的成本與布蘭特原油價格密切相關,在每桶75美元至95美元之間波動。由於歐盟關稅阻礙了廉價的中國二氧化鈦流入該地區,當地塗料生產商面臨與亞洲競爭對手相比,其最低成本持續高企的局面。

細分市場分析

2025年,住宅項目佔銷售額的68.96%,預計到2031年將以4.04%的複合年成長率成長。由於需要維護老舊建築的資產價值,維修工程正逐漸成為主流。目前,國家稅額扣抵允許對節能外牆塗料的成本進行高達30%的報銷。義大利在擴大其環保獎勵計畫後,2025年實現了20%的成長,從而推動了消費支出。消費者越來越傾向於選擇帶有氣喘/過敏友善標籤的低氣味塗料,以及號稱10年無需重新粉刷的耐刮擦內牆乳膠漆。這一趨勢導致每戶用量下降,但平均售價卻上漲。

商業應用領域對建築塗料的需求也在成長。辦公室正在適應混合辦公模式,所需占地面積減少了約15%。同時,飯店、醫療機構和教育機構的維修工程正在加速進行,所有這些場所都需要快乾、不含揮發性有機化合物(VOC)或抗菌塗料,以最大程度地減少對營運的干擾。在這一領域,能夠利用週末進行快速重塗的供應商至關重要,而中型區域品牌正在充分利用這項服務優勢。歐洲整體市場復甦仍不均衡。西班牙酒店業的塗料銷售量實現了兩位數的成長,而德國的辦公室相關交易則因資金籌措而停滯不前。

其他好處

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 老舊住宅存量維修熱潮興起。

- 歐盟的VOC法規正在加速向水性塗料的轉變。

- 新冠疫情後商業設施室內裝潢市場的復甦

- 節能隔熱塗料的需求

- 現場配色服務平台

- 市場限制因素

- 二氧化鈦和石油原料價格波動

- 由於高利率,住宅市場低迷

- 專業油漆工人手不足

- 價值鏈分析

- 監管分析

- 波特五力模型

- 新進入者的威脅

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 競爭公司之間的競爭

第5章 市場規模與成長預測

- 按最終用戶行業分類

- 商業的

- 家用

- 透過技術

- 溶劑型

- 水溶液

- 依樹脂類型

- 丙烯酸纖維

- 阿爾基多

- 環氧樹脂

- 聚酯纖維

- 聚氨酯

- 其他

- 按地區

- 法國

- 德國

- 義大利

- 北歐國家

- 波蘭

- 俄羅斯

- 西班牙

- 英國

- 其他歐洲國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- AkzoNobel NV

- Benjamin Moore & Co.

- Brillux GmbH & Co. KG

- CIN SA

- DAW SE

- Flugger group A/S

- Hempel A/S

- Jotun

- Kansai Paint Co., Ltd.

- KOBER SRL

- Nippon Paint Holdings Co., Ltd.

- POLICOLOR SA

- PPG Industries, Inc.

- The Sherwin-Williams Company

- Sniezka SA

- Sto SE & Co. KGaA

- Teknos Group

- Tikkurila

第7章 市場機會與未來展望

The Europe Architectural Coatings Market size is projected to grow from USD 17.98 billion in 2025 to USD 18.68 billion in 2026, and reach USD 22.58 billion by 2031, growing at a CAGR of 3.87% from 2026 to 2031.

A measured pivot toward high-value, low-emission formulations has started to outweigh pure volume growth, as purchasers respond to tougher European Union VOC ceilings and a building stock whose average age now tops 50 years. Demand for waterborne systems already dominates because professional painters favor low-odor, easy-clean products, and retailers have delisted many solventborne lines to avoid compliance risk. Suppliers are also repositioning toward repair and refurbishment projects that promise steadier margins than new-build work, weakened by high borrowing costs. Consolidation among leading producers is accelerating in order to spread raw-material inflation, fund greener research and development pipelines, and strengthen go-to-market scale.

Europe Architectural Coatings Market Trends and Insights

Aging Housing-Stock Renovation Boom

Europe counts more than 220 million dwellings built before 1990; many now require facade repair, moisture protection, and interior upgrades to meet modern health standards. Eurostat recorded EUR 310 billion spent on housing renovation in 2025, up 12% from the prior year. France, Germany, Italy, and Spain delivered 60% of that spending, with Italy alone surging 20% thanks to generous tax credits for energy-efficient coatings. The European Parliament wants to double annual renovation rates to 2% by 2030, lifting demand for durable acrylic and polyurethane finishes that extend repaint cycles from seven to twelve years. Consequently, the Europe architectural coatings market continues to rotate toward high-margin segments while sustaining steady headline growth.

EU VOC Regulations Accelerating Waterborne Shift

The European Commission updated EU Ecolabel rules in February 2026, lowering both VOC and SVOC caps and adding fitness-for-use tests that discourage binder dilution. Retailers quickly delisted non-compliant solventborne lines; by end-2025 waterborne products already formed 70% of decorative volume, up five points in five years. Pure acrylic emulsions now dominate interior walls, while styrene-acrylic blends migrate to budget exteriors. BASF, AkzoNobel, and Arkema validated bio-attributed resins that cut coating carbon footprints 40% during 2025 pilot runs. These moves confirm that tighter regulation not only accelerates waterborne uptake but also raises entry barriers for smaller formulators lacking research and development scale. As a result, the Europe architectural coatings market is tilting toward larger incumbents with science-based sustainability credentials.

Titanium-Dioxide and Petro-Feedstock Price Volatility

Spot TiO2 hovered between EUR 2,800 and EUR 3,400 per ton in 2025, a 21% swing that squeezed gross margins for mass-market interior emulsions. Producers offset part of the spike with extender pigments and composite opacifiers, yet these substitutions risk reduced scrub resistance or color fidelity at higher tint levels. Simultaneously, acrylic-monomer costs tracked Brent crude, which ranged from USD 75 to USD 95 per barrel. Because EU duties keep cheap Chinese TiO2 out of the bloc, local formulators face a persistently high cost floor relative to Asian rivals.

Other drivers and restraints analyzed in the detailed report include:

- Post-COVID Rebound in Commercial Fit-Outs

- Demand for Energy-Saving Thermal-Insulation Paints

- High Interest Rates Dampening New-Build Housing

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Residential projects generated 68.96% of 2025 revenue and will climb at a 4.04% CAGR through 2031. Renovation dominates because owners must preserve asset value in an aging building stock, and national tax credits now reimburse up to 30% of energy-saving exterior paint costs. Italy led spending with a 20% uptick in 2025 after enhancing its Eco-Bonus scheme. Consumers increasingly specify low-odor paints carrying asthma-allergy labels, and anti-scuff interior emulsions advertised to last a decade between coats. That dynamic lifts average selling prices even as liters per dwelling shrink.

Commercial applications are also witnessing increasing demand for architectural coatings. Offices are adapting to hybrid work, which trims square footage requirements by roughly 15%. Yet hotel, healthcare, and education refurbishments have accelerated, each demanding fast-dry zero-VOC or antimicrobial coatings to minimize disruption. The segment relies on supply partners able to stage rapid weekend repaints, a service advantage mid-tier regional brands exploit. Nonetheless, volume recovery remains uneven across Europe; Spain posts double-digit hospitality gains, whereas Germany's office pipeline stalls under financing constraints.

The Europe Architectural Coatings Market Report is Segmented by End-User Industry (Commercial and Residential), Technology (Solventborne and Waterborne), Resin (Acrylic, Alkyd, Epoxy, Polyester, Polyurethane, and Other Resin Types), and Geography (France, Germany, Italy, Nordic Countries, Poland, Russia, Spain, United Kingdom, and Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- AkzoNobel N.V.

- Benjamin Moore & Co.

- Brillux GmbH & Co. KG

- CIN S.A.

- DAW SE

- Flugger group A/S

- Hempel A/S

- Jotun

- Kansai Paint Co., Ltd.

- KOBER SRL

- Nippon Paint Holdings Co., Ltd.

- POLICOLOR SA

- PPG Industries, Inc.

- The Sherwin-Williams Company

- Sniezka SA

- Sto SE & Co. KGaA

- Teknos Group

- Tikkurila

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Ageing housing-stock renovation boom

- 4.2.2 EU VOC regulations accelerating waterborne shift

- 4.2.3 Post-COVID rebound in commercial fit-outs

- 4.2.4 Demand for energy-saving thermal-insulation paints

- 4.2.5 On-site tint-as-a-service platforms

- 4.3 Market Restraints

- 4.3.1 Titanium-dioxide and petro-feedstock price volatility

- 4.3.2 High interest rates dampening new-build housing

- 4.3.3 Professional painter labour shortages

- 4.4 Value Chain Analysis

- 4.5 Regulatory Analysis

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By End-User Industry

- 5.1.1 Commercial

- 5.1.2 Residential

- 5.2 By Technology

- 5.2.1 Solventborne

- 5.2.2 Waterborne

- 5.3 By Resin

- 5.3.1 Acrylic

- 5.3.2 Alkyd

- 5.3.3 Epoxy

- 5.3.4 Polyester

- 5.3.5 Polyurethane

- 5.3.6 Other Resin Types

- 5.4 By Geography

- 5.4.1 France

- 5.4.2 Germany

- 5.4.3 Italy

- 5.4.4 Nordic Countries

- 5.4.5 Poland

- 5.4.6 Russia

- 5.4.7 Spain

- 5.4.8 United Kingdom

- 5.4.9 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)}

- 6.4.1 AkzoNobel N.V.

- 6.4.2 Benjamin Moore & Co.

- 6.4.3 Brillux GmbH & Co. KG

- 6.4.4 CIN S.A.

- 6.4.5 DAW SE

- 6.4.6 Flugger group A/S

- 6.4.7 Hempel A/S

- 6.4.8 Jotun

- 6.4.9 Kansai Paint Co., Ltd.

- 6.4.10 KOBER SRL

- 6.4.11 Nippon Paint Holdings Co., Ltd.

- 6.4.12 POLICOLOR SA

- 6.4.13 PPG Industries, Inc.

- 6.4.14 The Sherwin-Williams Company

- 6.4.15 Sniezka SA

- 6.4.16 Sto SE & Co. KGaA

- 6.4.17 Teknos Group

- 6.4.18 Tikkurila

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

2026年全球側光式壓克力標示市場報告

2026年全球側光式壓克力標示市場報告 2034年外牆塗料市場預測-按塗料類型、技術、應用、最終用戶和地區分類的全球分析

2034年外牆塗料市場預測-按塗料類型、技術、應用、最終用戶和地區分類的全球分析 住宅建築塗料市場:2026-2032年全球市場預測(按產品類型、配方、飾面類型、應用、最終用戶和分銷管道分類)水性建築塗料市場:依功能、產品類型、應用、通路和最終用途分類-2026-2032年全球市場預測2026年全球壓克力牆面標牌支架市場報告建築塗料市場:2026-2032年全球市場預測(依產品類型、技術、樹脂類型、應用方法、用途及通路分類)建築翻新塗裝市場:依產品類型、應用方法、塗裝技術及最終用戶分類-2026-2032年全球預測

住宅建築塗料市場:2026-2032年全球市場預測(按產品類型、配方、飾面類型、應用、最終用戶和分銷管道分類)水性建築塗料市場:依功能、產品類型、應用、通路和最終用途分類-2026-2032年全球市場預測2026年全球壓克力牆面標牌支架市場報告建築塗料市場:2026-2032年全球市場預測(依產品類型、技術、樹脂類型、應用方法、用途及通路分類)建築翻新塗裝市場:依產品類型、應用方法、塗裝技術及最終用戶分類-2026-2032年全球預測 建築塗料市場分析及預測(至2035年):依類型、產品類型、技術、應用、材質、製程、最終用戶、功能、應用方法及解決方案分類

建築塗料市場分析及預測(至2035年):依類型、產品類型、技術、應用、材質、製程、最終用戶、功能、應用方法及解決方案分類 建築塗料:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

建築塗料:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 全球建築塗料市場:市場規模、佔有率和趨勢分析(按樹脂類型、技術、應用和地區分類),細分市場預測(2026-2033 年)

全球建築塗料市場:市場規模、佔有率和趨勢分析(按樹脂類型、技術、應用和地區分類),細分市場預測(2026-2033 年)