|

市場調查報告書

商品編碼

2044257

印尼密封劑市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Indonesia Sealants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

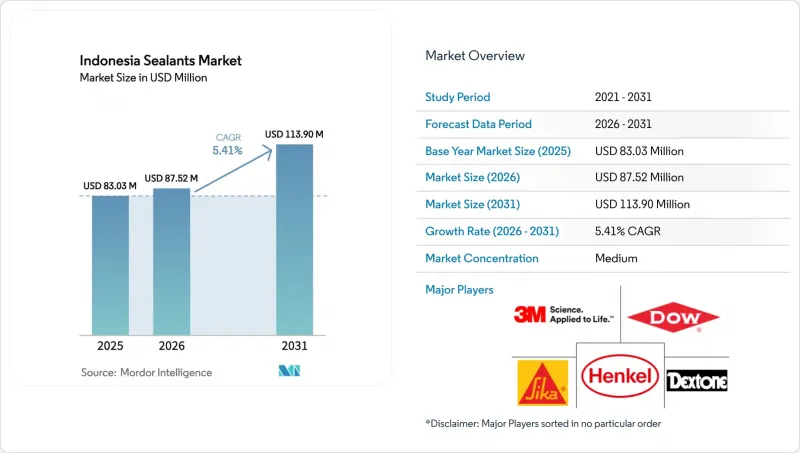

預計印尼密封膠市場規模將從 2025 年的 8,303 萬美元成長到 2026 年的 8,752 萬美元,然後在 2031 年達到 1.139 億美元,2026 年至 2031 年的複合年成長率為 5.41%。

在印度尼西亞,住宅和產業建設的激增,加上西爪哇電動車組裝的投資以及蘇拉威西造船業的復興,正在推動耐候性、結構性和船用級組合藥物的應用。跨國品牌正在擴大本地生產,以滿足熱帶環境下強制性的SNI認證和性能測試要求。同時,計畫於2026年至2031年間生效的低VOC排放法規,也增加了對水性丙烯酸和α-矽烷化學品的需求。此外,儘管來自中國的低成本進口產品給大宗商品價格帶來了壓力,但市場正明顯轉向差異化產品,並輔以技術服務和本地檢驗。

印尼密封膠市場趨勢及洞察

西爪哇一家汽車OEM製造商擴建生產線

比亞迪位於梳邦的電動車工廠預計將於2026年3月即將完工。該廠的年產能目標預計將對矽基導熱材料和聚氨酯基結構密封膠的需求產生影響。 2025年6月,IMAS和廣汽集團在普沃加達開設了一家可擴展工廠,在地採購。這些舉措預計將透過創造對電池外殼墊片、輕量化車身黏合劑和座艙氣密密封膠的穩定需求,推動2026年至2031年的複合年成長率。瓦克在亞太地區擴大特種矽酮產能,確保了印尼OEM廠商的穩定供應。雖然隨著產業從內燃機轉向電池組,某些引擎室應用有所減少,但這種轉變也為高價值的電氣化連接件創造了機會,並提高了印尼密封膠市場的品質標準。

熱帶氣候下的密封條維修

在印度尼西亞,濕度常年維持在70%至90%之間,年降雨量可達6,000毫米,這縮短了密封膠的使用壽命。這種氣候挑戰正穩步提升著玻璃安裝、帷幕牆接縫和衛生級建築等領域的維修需求。近年來,隨著建築業的擴張,開發商們也深刻意識到濕度帶來的挑戰,並致力於尋找應對措施,尤其是在高密度居住專案中。到了2024年,西卡已擴大零售業務,這項策略性舉措符合印尼「DIY密封膠更換」日益成長的趨勢。雖然印尼國家標準局(SNI)規定的熱帶環境耐久性測試需要4至8週才能獲得產品核准,但證明其具有耐水解和抗真菌性能正成為一項重要的品牌優勢。隨著電子商務的快速發展,倉儲需求不斷成長,進一步增加了對能夠承受堆高機荷載的柔軟性地面接縫密封膠的需求。這些密封劑必須能夠承受重型機械的負荷以及該國獨特而顯著的濕度波動。

大量低價中國進口商品湧入

2025年7月,印尼從中國進口的填縫材料和黏合劑數量激增,尤其是黏合劑,價格遠低於本地品牌。這些進口產品,包括甲苯二異氰酸酯和矽酮聚合物,使得中國企業得以大力推行低價銷售,從而擠壓了印尼通用密封膠供應商的利潤空間。同年,漢高公司重組了在東南亞的分銷網路。這清楚地表明,全球企業如何調整市場策略,以在與價格較低的競爭對手抗衡的同時,強化其高階服務形象。儘管印尼政府根據第110/2025號法規引入了碳課稅機制,旨在彌合成本差距並對高排放進口產品徵稅,但短期價格壓力仍然對2026年至2031年預測期內的成長構成一定程度的威脅。

細分市場分析

2025年,矽酮密封膠在印尼密封膠市場佔據了44.22%的主導地位。這主要歸功於其卓越的紫外線穩定性和黏合強度。這些特性對於印尼這個島國特有的潮濕多雨氣候至關重要。同時,預計在2026年至2031年的預測期內,丙烯酸密封膠將以5.83%的複合年成長率(CAGR)實現最高成長。這一趨勢主要受2025年第110號法規的影響,該法規促使承包商在住宅翻新中越來越傾向於選擇性價比高且低揮發性有機化合物(VOC)的解決方案。

利用矽酮的彈性恢復性能和與消毒劑的優異相容性,外牆和衛生潔具的接縫能夠承受日常的乾濕循環,確保10至15年的使用壽命。同時,在印度尼西亞,受政府住宅補貼鼓勵重新粉刷和漏水維修的推動,對丙烯酸屋頂和牆壁填充材的需求正在成長。在汽車產業,聚氨酯在倉庫地面接縫的黏合和固定中發揮著至關重要的作用,其中超過1.5兆帕(MPa)的拉伸黏合強度至關重要。西爪哇快速發展的電動車走廊也使該領域受益。此外,瓦克公司在其亞洲基地開發的混合α-矽烷技術,結合了矽酮的柔軟性和聚氨酯的黏合強度。這些創新提供了無錫替代方案,並滿足了未來的VOC法規要求。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 西爪哇一家汽車OEM製造商擴建生產線

- 熱帶氣候地區對密封條維修工作的需求日益成長

- 推廣廣泛使用環保低VOC矽氧烷(環境與林業部(MoEF)2027年法規草案)

- 蘇拉威西的造船走廊帶動了對船用產品需求的成長。

- 電子商務物流中心需要具有高靈活性的地板接縫

- 市場限制因素

- 來自中國的低成本進口商品大量湧入。

- 航太級密封劑的擴展SNI認證

- Java 以外地區熟練承包商短缺

- 價值鏈分析

- 波特五力模型

- 新進入者的威脅

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 競爭公司之間的競爭

- 分銷通路分析

第5章 市場規模與成長預測

- 依樹脂類型

- 丙烯酸纖維

- 環氧樹脂

- 聚氨酯

- 矽酮

- 其他樹脂

- 按最終用戶行業分類

- 航太

- 車

- 建築/施工

- 衛生保健

- 其他終端用戶產業

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- 3M

- Arkema

- Avery Dennison

- BASF SE

- Carlisle Companies

- DEXTONE INDONESIA

- Dow

- HB Fuller Company

- Henkel AG & Co. KGaA

- Illinois Tool Works

- MAPEI SpA

- Momentive

- Pidilite Industries Ltd

- RPM International Inc.

- Shin-Etsu Chemical Co., Ltd.

- Sika AG

- Soudal Holding NV

- Tremco

- Wacker Chemie AG

第7章 市場機會與未來展望

The Indonesia Sealants Market size is expected to grow from USD 83.03 million in 2025 to USD 87.52 million in 2026 and is forecast to reach USD 113.90 million by 2031 at 5.41% CAGR over 2026-2031. In Indonesia, a surge in residential and industrial construction, coupled with investments in electric vehicle assembly in West Java and a shipbuilding revival in Sulawesi, is driving the adoption of weather-proofing, structural, and marine-grade formulations. Multinational brands are ramping up local production to meet mandatory SNI certification and tropical-performance testing. Meanwhile, a draft regulation on low-VOC emissions set for the 2026-2031 period is pushing demand toward waterborne acrylic and alpha-silane chemistries. Additionally, while low-cost imports from China are putting pressure on commodity prices, there is a noticeable shift toward differentiated products, bolstered by technical services and local validation.

Indonesia Sealants Market Trends and Insights

OEM Automotive Line Expansion in West Java

By March 2026, BYD's electric-vehicle plant in Subang will have neared completion. With a target for annual production capacity, the plant is expected to influence the demand for silicone thermal-interface materials and polyurethane structural sealants. In June 2025, IMAS and GAC Aion inaugurated a scalable facility in Purwakarta, with a notable portion of their components sourced locally. These initiatives are projected to boost the forecast CAGR for the period 2026-2031 by creating a consistent demand for battery-housing gaskets, lightweight body bonding, and cabin air-tightening sealants. Wacker's expansion of specialty silicones capacity in the Asia-Pacific region ensures a steady supply for Indonesian OEM tiers. As the industry transitions from internal combustion engines to battery packs, certain engine-bay applications have diminished. However, this shift has created opportunities for more valuable electrification joints, elevating quality standards in Indonesia's sealants market.

Tropical-Climate Weather-Seal Retrofits

In Indonesia, where humidity levels consistently range from 70% to 90% and annual rainfall can peak at 6,000 mm, sealants experience reduced lifespans. This climatic hurdle has spurred a steady demand for retrofitting in areas such as glazing, facade joints, and sanitary grades. In recent years, as the building sector has expanded, developers, acutely aware of humidity challenges, have emphasized mitigation strategies, particularly in high-occupancy projects. By 2024, Sika had broadened its retail footprint, a strategic move in tune with Indonesia's growing trend of do-it-yourself sealant replacements. Although SNI-mandated tropical durability testing can extend product approval by four to eight weeks, showcasing resilience against hydrolytic and fungal stress is becoming a pivotal branding edge. With the e-commerce boom, there is an escalating demand for warehouses, amplifying the need for flexible, forklift-resistant floor-joint sealants. These sealants must endure the challenges posed by heavy machinery and the country's pronounced moisture fluctuations.

Rising Inflow of Low-Cost Chinese Imports

In July 2025, Indonesia saw a surge in imports of caulking compounds and adhesive preparations from China, with the latter offering substantial discounts over local brands. These imports, including toluene di-isocyanate and silicone polymers, enabled aggressive under-pricing, thereby tightening profit margins for Indonesia's commodity-grade sealant suppliers. In 2025, Henkel restructured its Southeast Asia distributorship, underscoring how global entities recalibrated their market strategies to combat budget-friendly competitors while enhancing their premium service image. Despite the introduction of carbon-levy mechanisms under Regulation 110/2025, aimed at penalizing high-emission imports to bridge the cost gap, the immediate pricing pressures still cast a slight shadow on growth during the forecast period of 2026-2031.

Other drivers and restraints analyzed in the detailed report include:

- Low-VOC Siloxane Reformulation Push

- Sulawesi Shipbuilding Corridor Stimulus

- Certification and Skilled-Labor Gaps

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, silicone secured a commanding 44.22% revenue share in Indonesia's sealants market, primarily due to its exceptional ultraviolet (UV) stability and adhesion. These attributes are critical for the archipelago's humid, high-rainfall climate. Conversely, acrylic grades are projected to register the highest compound annual growth rate (CAGR) of 5.83% during the forecast period of 2026-2031. This trend is attributed to a growing preference among contractors for cost-effective, low-volatile organic compound (VOC) solutions for residential retrofits, a shift catalyzed by Regulation 110/2025.

Silicone's elastic recovery and biocide-friendly formulation ensure that facade and sanitary joints can withstand daily wet-dry cycles, with a lifespan of 10 to 15 years. Simultaneously, the demand for acrylic roof and wall fillers in Indonesia is increasing, driven by government housing subsidies that encourage repainting and leakage repairs. In the automotive sector, polyurethane plays a critical role in bonding and securing joints in warehouse flooring, where tensile adhesion exceeding 1.5 megapascal (MPa) is essential. This segment is also benefiting from the rapidly expanding West Java Electric Vehicle corridor. Furthermore, hybrid alpha-silane technologies, developed at Wacker's Asian facilities, combine the flexibility of silicone with the adhesion strength of polyurethane. These advancements offer tin-free alternatives, aligning with future VOC regulations.

The Indonesia Sealants Market Report is Segmented by Resin (Acrylic, Epoxy, Polyurethane, Silicone, and Other Resins), End-User Industry (Aerospace, Automotive, Building and Construction, Healthcare, and Other End-User Industries), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- 3M

- Arkema

- Avery Dennison

- BASF SE

- Carlisle Companies

- DEXTONE INDONESIA

- Dow

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Illinois Tool Works

- MAPEI S.p.A.

- Momentive

- Pidilite Industries Ltd

- RPM International Inc.

- Shin-Etsu Chemical Co., Ltd.

- Sika AG

- Soudal Holding N.V.

- Tremco

- Wacker Chemie AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 OEM automotive line-expansion in West Java

- 4.2.2 Growing demand for tropical-climate weather-seal retrofits

- 4.2.3 Eco-friendly low-VOC siloxane push (2027 draft MoEF rule)

- 4.2.4 Sulawesi shipbuilding corridor fueling marine-grade uptake

- 4.2.5 E-commerce logistics hubs needing high-movement floor joints

- 4.3 Market Restraints

- 4.3.1 Rising inflow of low-cost PRC imports

- 4.3.2 Prolonged SNI certification for aerospace-grade sealants

- 4.3.3 Skilled applicator shortage outside Java

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

- 4.6 Distribution Channel Analysis

5 Market Size and Growth Forecasts (Value)

- 5.1 By Resin

- 5.1.1 Acrylic

- 5.1.2 Epoxy

- 5.1.3 Polyurethane

- 5.1.4 Silicone

- 5.1.5 Other Resins

- 5.2 By End-User Industry

- 5.2.1 Aerospace

- 5.2.2 Automotive

- 5.2.3 Building and Construction

- 5.2.4 Healthcare

- 5.2.5 Other End-user Industries

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 3M

- 6.4.2 Arkema

- 6.4.3 Avery Dennison

- 6.4.4 BASF SE

- 6.4.5 Carlisle Companies

- 6.4.6 DEXTONE INDONESIA

- 6.4.7 Dow

- 6.4.8 H.B. Fuller Company

- 6.4.9 Henkel AG & Co. KGaA

- 6.4.10 Illinois Tool Works

- 6.4.11 MAPEI S.p.A.

- 6.4.12 Momentive

- 6.4.13 Pidilite Industries Ltd

- 6.4.14 RPM International Inc.

- 6.4.15 Shin-Etsu Chemical Co., Ltd.

- 6.4.16 Sika AG

- 6.4.17 Soudal Holding N.V.

- 6.4.18 Tremco

- 6.4.19 Wacker Chemie AG

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment

建築和施工密封膠市場規模、佔有率和成長分析:按類型、應用、固化類型、最終用戶、分銷管道、功能和地區分類—2026-2033年產業預測

建築和施工密封膠市場規模、佔有率和成長分析:按類型、應用、固化類型、最終用戶、分銷管道、功能和地區分類—2026-2033年產業預測 2026-2034年全球建築和施工密封劑市場規模、佔有率、趨勢和成長分析報告

2026-2034年全球建築和施工密封劑市場規模、佔有率、趨勢和成長分析報告 耐燃料密封劑市場:2026-2032年全球市場預測(依樹脂類型、形態、固化機制、包裝、應用分類)

耐燃料密封劑市場:2026-2032年全球市場預測(依樹脂類型、形態、固化機制、包裝、應用分類) 2026年全球預製建築密封劑市場報告彈性體密封劑市場:按類型、包裝、銷售管道、最終用途和應用分類-2026-2032年全球市場預測發泡密封劑市場:2026-2032年全球市場預測(依產品類型、發泡成分、包裝類型、應用、最終用戶和銷售管道)全球浸漬密封劑市場規模、佔有率、趨勢和成長分析報告(2026-2034年)全球隔熱密封劑市場報告(2026 年)CIPG/FIPG液體墊片市場:按產品類型、包裝、黏度、應用、最終用戶、銷售管道分類 - 全球預測(2026-2032年)聲學密封膠和黏合劑市場:按產品、技術、類型、應用和分銷管道分類,全球預測(2026-2032年)

2026年全球預製建築密封劑市場報告彈性體密封劑市場:按類型、包裝、銷售管道、最終用途和應用分類-2026-2032年全球市場預測發泡密封劑市場:2026-2032年全球市場預測(依產品類型、發泡成分、包裝類型、應用、最終用戶和銷售管道)全球浸漬密封劑市場規模、佔有率、趨勢和成長分析報告(2026-2034年)全球隔熱密封劑市場報告(2026 年)CIPG/FIPG液體墊片市場:按產品類型、包裝、黏度、應用、最終用戶、銷售管道分類 - 全球預測(2026-2032年)聲學密封膠和黏合劑市場:按產品、技術、類型、應用和分銷管道分類,全球預測(2026-2032年)