|

市場調查報告書

商品編碼

2044192

印刷設備:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Print Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

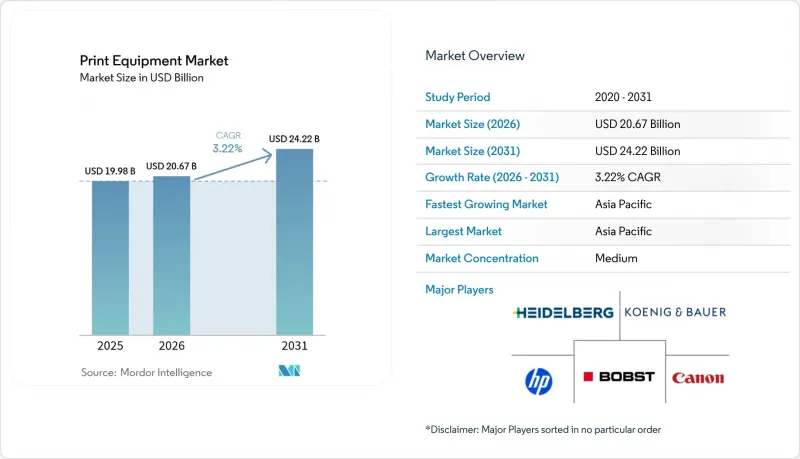

預計印刷設備市場將從 2025 年的 199.8 億美元和 2026 年的 206.7 億美元成長到 2031 年的 242.2 億美元,2026 年至 2031 年的年複合成長率(CAGR)為 3.22%。

隨著印刷企業追求快速切換、最短設定時間和可變數據印刷能力,市場需求正從以膠印為主的生產線轉向數位印刷和混合印刷。歐盟和美國的食品藥品標籤規例推動了對能夠處理序列化和過敏原標籤的印刷機的投資。履約中心正在採用窄幅數位印刷設備,以便在出貨當天印刷包裝盒,而品牌所有者則在擴展其SKU以滿足細分市場的需求。來自以軟體為中心的新興參與企業的競爭壓力正迫使現有印刷機製造商增加雲端連接的工作流程平台和訂閱計劃。這種轉變將增加資金籌措需求,但預計將帶來更穩定的業務收益。

全球印刷設備市場趨勢與洞察

食品和藥品行業數位化標籤的監管利多因素

歐盟和美國的標籤法規強制要求使用數位浮水印、可變過敏原標籤和批間可追溯性,迫使加工商改用噴墨印刷或投資新的數位印刷機。印度將於2025年4月起對出口藥品增加QR碼序列化,進一步加速了這個全球趨勢。由於品牌所有者會根據ISO 12647合規性對供應商進行預篩選,印刷機供應商在每次銷售中都附贈分光光度計和閉合迴路校準服務,以確保通過客戶的審核。數位印刷機還能幫助加工商避免歐盟監管機構可能對貼錯標籤的食品處以的罰款,罰款金額最高可達全球銷售額的4%。這種風險使得模擬切換錯誤變得不可接受。為了因應未來的監管變化,藥品包裝製造商現在指定使用能夠同時支援水性油墨和UV固化油墨的印刷機,以便在PFAS法規更加嚴格時,能夠靈活地調整配方,降低頭痛風險。因此,數位序列化不再只是監管要求,而成為董事會層級資本支出 (CAPEX) 的決定因素。

按需書籍和包裝印刷正在推動資本投資。

自2024年以來,短週期生產的經濟效益發生了翻天覆地的變化。碳粉和噴墨技術消除了製版成本和準備流程中的浪費,使得62%的商業印刷商現在接受500份以下的訂單,較2020年的41%顯著成長。電商平台現在在當地印刷瓦楞紙箱,降低了庫存成本,並實現了當日送達的季節性促銷活動。 Cimpress已投資超過1億美元購買惠普Indigo設備,以實現生產在地化,並將訂單到出貨的週期從72小時縮短至24小時。像Springer Nature這樣的出版商已將其78%的舊書轉向客製印刷,從而無需銷毀未售出的庫存。膠印機製造商正競相在其捲紙印刷生產線上加裝噴墨條,以確保獲得1000至10000份的訂單,在這些訂單中,模擬印刷的速度仍然至關重要。隨著這些混合原型機的可靠性得到驗證,金融機構開始提供包含服務和耗材的特定機器租賃計劃,從而降低了中型印刷公司的進入門檻。

繪圖紙價格波動給利潤率帶來了壓力。

2025年初,斯堪的納維亞半島和巴西的紙漿價格大幅上漲,導致塗佈紙價格上漲18%,給印刷企業的息稅折舊攤銷前利潤(EBITDA)帶來壓力,並延緩了印刷機的升級換代。儘管歐盟循環經濟法規鼓勵使用再生纖維,但紙張品質的波動迫使營運商頻繁調整印刷機,增加了停機時間和油墨堆積。利潤率僅8-12%的加工商難以將這些價格上漲轉嫁給簽訂多年合約的客戶,迫使他們降低新生產線資本支出(CAPEX)的優先順序。一些膠印企業透過期貨合約對沖紙漿價格風險,但2025年對沖費用上漲22%將抵銷其收益。數位設備供應商大力宣傳其產品可減少廢棄物,但高覆蓋率的噴墨列印會消耗大量昂貴的油墨和墨盒,從而抵消了成本節約。因此,投資趨勢呈現兩極化。大型印刷公司透過多年合約確保紙張採購,並引進高速噴墨印表機,而小規模印刷公司則傾向於推遲設備升級,任由現貨市場波動。

細分市場分析

至2025年,數位印刷機將佔印刷設備市場41.32%的佔有率,年均成長率為4.02%。噴墨和碳粉產品線受到加工商的青睞,他們需要可變圖形且無需製版成本,其具成本效益彌補了基礎速度的不足。隨著出版商轉向客製印刷,數位印刷機的市場規模預計將顯著擴大。膠印仍將用於長幅印刷,但其市場佔有率正在逐年下降。柔版印刷機仍然是高不透明度軟性薄膜印刷的必備設備,而凹版印刷則用於超長幅裝飾性印刷。網版印刷仍主要應用於紡織品和電子產品等小眾市場。加工商擴大選擇將噴墨印表機頭與柔版印刷捲筒結合的混合設備,以平衡印刷量和個人需求。

Canon和海德堡計畫於2024年合作開發B2幅面靜電照相引擎,旨在為混合型中等批量生產機型奠定基礎。Ricoh的生產型噴墨技術藍圖則瞄準了渴望擺脫印版需求的標籤加工商。儘管水性噴墨技術的進步提高了墨水在無塗布紙的附著力,但其耐磨性仍落後於溶劑型系統。

預計到2025年,印刷機硬體將佔總產量的37.32%,而印後設備則以3.84%的複合年成長率成為成長最快的細分市場,這主要得益於工廠中模切、折疊和檢測等環節自動化程度的不斷提高。隨著人手不足使得機器人分切和視覺檢測更具吸引力,印後加工生產線上印刷設備的市場佔有率正在擴大。海德堡的「Cartonmaster」系統整合了這些流程,展示了承包單元如何減少占地面積和生產週期。雖然印前系統在雲端工作流程下逐漸商品化,但它們對於色彩管理仍然至關重要。切斷機和貼合機等周邊設備正在推動軟質包裝行業的需求,因為加工商每個班次需要處理多種承印物。

博斯特公司預計其Mastercut模切機的訂單將在2024年成長28%,反映出減少停機時間的迫切需求。單張紙印刷機憑藉其幅面柔軟性仍然主導著商業印刷市場,但由於捲筒紙容量的下降,捲筒紙印刷生產線正在萎縮。以幅面分類,B1和B2幅面滿足中等印量的需求,而B3幅面則迎合快印需求。專有周邊設備套裝會增加換版成本,並且在歐盟和美國都受到反壟斷審查。

區域分析

預計到2025年,亞太地區將佔全球市場的41.43%,並預計在2031年之前以4.12%的年均複合成長率成長。在中國,80億元人民幣(約11億美元)的補貼正在推動中小型城市採用數位印刷機,從而縮短物流距離。印度藥品出口商正在維修生產線以符合歐盟序列化法規,這提振了噴墨印刷的需求。日本大型企業正在採用混合印刷機來實現短週期包裝,但澳洲對新設備的進口關稅阻礙了這一趨勢。在韓國,半導體封裝用網版印刷系統正在蓬勃發展。

到2025年,歐洲和北美合計將佔全球總量的約45%,但成長緩慢。歐盟的可追溯性法規正推動加工商轉向數位化序列化,但這給小規模企業帶來了負擔。在德國,儘管2024年裝機總量下降了4%,但由於企業積極推行減少廢棄物的舉措,數位化設備的訂單卻增加了12%。美國的產業兩極化日益加劇。大型包裝公司正大力投資高速噴墨印刷,而許多商業印刷公司卻難以維持傳統的膠印設備。在加拿大,印刷業正經歷重組,中型印刷公司紛紛破產或合併。

其餘地區包括南美洲、中東和非洲。巴西正在投資食品包裝的柔版印刷,但進口成本波動較大。沙烏地阿拉伯在其「2030願景」框架下,透過為印刷機提供優惠融資來支持國內印刷業。阿拉伯聯合大公國正在推動建立一個面向海灣國家和非洲的自由印刷中心。南非正面臨能源成本上漲的挑戰,但仍選擇性地引進噴墨印表機用於藥品包裝盒;而肯亞則正在擴大其包裝生產線,以滿足當地消費者的需求。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 產業價值鏈分析

- 市場促進因素

- 食品和藥品數位化標籤的監管利多因素

- 對按需圖書和包裝的需求正在推動資本投資。

- 品牌所有者促進 SKU 擴展

- 混合式印刷機的引進將降低總擁有成本。

- 人工智慧驅動的預測性維護可減少印表機停機時間。

- 終端用戶附近分散式微型工廠的興起

- 市場限制因素

- 印刷用紙價格波動劇烈,利潤率帶來了壓力。

- 熟練印刷操作員短缺

- 雲端連接印表機帶來的網路安全風險日益增加。

- PFAS法規限制某些油墨化學品的使用。

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

- 新進入者的威脅

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 競爭公司之間的競爭

第5章 市場規模與成長預測

- 透過技術

- 輪轉印刷膠印

- 柔版印刷

- 凹版印刷

- 網版印刷

- 數位的

- 透過裝置

- 印前系統

- 印刷機(單張紙式、捲筒紙式)

- 書籍裝訂和精加工

- 輔助/線上處理

- 透過使用

- 書籍/出版

- 廣告和廣告牌

- 證券交易

- 包裝

- 其他用途

- 按最終用戶行業分類

- 包裝處理器

- 商業印刷公司

- 內部/公司

- 快速列印影印店

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 歐洲

- 英國

- 德國

- 法國

- 西班牙

- 義大利

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 肯亞

- 其他非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Heidelberger Druckmaschinen AG

- Koenig and Bauer AG

- Bobst Group SA

- HP Inc.

- Canon Inc.

- Seiko Epson Corporation

- Fujifilm Holdings Corporation

- Ricoh Company Ltd.

- Electronics for Imaging, Inc.

- Durst Phototechnik AG

- Mark Andy Inc.

- Nilpeter A/S

- Gallus Ferd. Ruesch AG(Heidelberg)

- OMET Srl

- MPS Systems BV

- Uteco Converting SpA

- Manroland Goss Web Systems GmbH

- Agfa-Gevaert Group NV

- Brother Industries Ltd.

- AB Graphic International Ltd.

第7章 市場機會與未來展望

The Print Equipment Market size is projected to expand from USD 19.98 billion in 2025 and USD 20.67 billion in 2026 to USD 24.22 billion by 2031, registering a CAGR of 3.22% between 2026 to 2031.

Demand is shifting from offset-dominated lines toward digital and hybrid presses as converters chase fast changeovers, minimal makeready, and variable-data features. Food and pharmaceutical labeling rules in the European Union and the United States are pulling capital toward presses that support serialization and allergen declarations. E-commerce fulfillment centers are buying narrow-web digital equipment to print shipping boxes on the day of dispatch, while brand owners widen SKU counts to serve micro-segments. Competitive pressure from software-centric entrants is forcing incumbent press makers to add cloud-connected workflow platforms and subscription plans, a pivot that raises refinancing needs but promises sticky service revenue.

Global Print Equipment Market Trends and Insights

Regulatory Tailwinds For Food And Pharma Digital Labels

EU and U.S. labeling mandates now require digital watermarks, variable allergen labeling, and batch-level traceability, pushing converters toward inkjet retrofits and greenfield digital press purchases. India added QR serialization for export drugs in April 2025, reinforcing this global convergence. Brand owners are prequalifying suppliers based on ISO 12647 compliance, so press vendors bundle spectrophotometers and closed-loop calibration with every sale to pass customer audits. Digital presses also help converters avoid penalties that EU regulators can levy at up to 4% of global turnover for mislabeled food products, a risk that makes analog changeover errors untenable. To hedge against future rule changes, pharmaceutical packagers now specify presses that accept both water-based and UV-curable inks, ensuring headroom for low-migration formulations once PFAS restrictions tighten. The net effect is that digital serialization has become a board-level CAPEX trigger rather than a mere regulatory checkbox.

On-Demand Book And Packaging Runs Driving CAPEX

Short-run economics flipped after 2024, when 62% of commercial printers accepted jobs below 500 units, up from 41% in 2020, thanks to toner and inkjet lines that erase plate cost and makeready waste. E-commerce hubs now print corrugated boxes on-site, reducing inventory costs and enabling same-day seasonal promotions. Cimpress committed more than USD 100 million for HP Indigo units to localize production and cut order-to-ship cycles from 72 to 24 hours. Publishers such as Springer Nature moved 78% of backlist titles to print-on-demand, eliminating the need to pulp unsold stock. Offset press makers are racing to bolt inkjet bars onto web lines so they can chase jobs that fall in the 1,000-10,000 range, where analog speed still matters. As these hybrid prototypes prove reliable, lenders are starting to offer structure-specific leasing packages that bundle service and consumables, lowering the hurdle rate for mid-size shops.

Volatile Graphic-Paper Prices Squeeze Margins

Nordic and Brazilian pulp spikes in early 2025 lifted coated-sheet prices 18%, squeezing printer EBITDA and delaying press upgrades. EU circular-economy rules encourage recycled fiber, but variable sheet quality forces operators to recalibrate presses more often, increasing downtime and ink lay-down. Converters with thin 8-12% margins struggle to pass these hikes through multi-year customer contracts, so CAPEX for new lines slips down the priority list. Some offset printers hedge pulp risk with futures contracts, yet hedging fees rose 22% in 2025, eroding the benefit. Digital vendors pitch reduced waste, but high-coverage inkjet jobs consume expensive ink and drums, muting savings. As a result, investment bifurcates: large groups lock multi-year paper deals and adopt high-speed inkjet, while small shops defer upgrades and ride spot-market volatility.

Other drivers and restraints analyzed in the detailed report include:

- Brand-Owner Push For SKU Proliferation

- Hybrid Press Adoption Cuts Total Cost Of Ownership

- Skilled Press-Operator Shortage

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Digital captured 41.32% of the print equipment market in 2025 and rose at 4.02% annually. Inkjet and toner lines appeal to converters who need variable graphics without plate costs, a value that offsets slower raw speed. The print equipment market size for digital presses is forecast to expand significantly as publishers pivot to print-on-demand. Offset retains long runs, yet its slice narrows each year. Flexographic units stay vital for high-opacity flexible films, while gravure holds ultra-long decorative work. Screen equipment remains a niche for textiles and electronics. Converters increasingly choose hybrid rigs that bolt inkjet bars onto flexo webs, balancing run length and personalization.

Canon and Heidelberg joined forces in 2024 on a B2 electrophotographic engine, aiming to anchor hybrid mid-volume models. Ricoh's production inkjet roadmap targets label converters craving plate elimination. Advances in aqueous inkjet have improved adhesion on uncoated stock, yet rub resistance still trails solvent systems.

Press hardware held 37.32% of 2025 tonnage, but post-press equipment is the fastest-growing segment, with a 3.84% CAGR, as plants automate die-cutting, folding, and inspection. The print equipment market share for finishing lines is growing as labor shortages make robotic blank separation and vision QC more attractive. Heidelberg's Cartonmaster integrates these steps, showing how turnkey cells compress floor space and cycle time. Pre-press systems commoditize under cloud workflows, yet remain essential for color control. Ancillary gear, such as slitters and laminators, sustains demand in flexible packaging, where converters juggle multiple substrates each shift.

Bobst logged a 28% order rise for Mastercut die-cutters in 2024, reflecting the urgency to cut downtime. Sheet-fed presses still dominate commercial work thanks to their format agility, whereas roll-fed lines shrink as magazine volume declines. Format-wise, B1 and B2 classes secure mid-runs, while B3 serves quick printers. Proprietary ancillary bundles raise switching costs and draw antitrust scrutiny in the EU and the United States.

The Print Equipment Market Report is Segmented by Technology (Web-Offset Lithographic, Flexographic, Gravure, Screen Printing, and Digital), Equipment Type (Pre-Press Systems, Press, and More), Application (Books and Publishing, Advertising and Signage, and More), End-User Industry (Packaging Converters, Commercial Printers, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific accounted for 41.43% of global volume in 2025 and is projected to grow at 4.12% through 2031. China's CNY 8 billion (USD 1.1 billion) subsidy funds digital press rollouts in smaller cities, shrinking logistics miles. India's drug exporters are retrofitting lines for EU serialization, boosting inkjet demand. Japan's majors embrace hybrid presses for short-run packaging, while Australia faces import-duty drag on new equipment. South Korea grows in screen systems for semiconductor packaging.

Europe and North America together account for about 45% of the 2025 tons, but growth is slow. EU traceability rules push converters toward digital serialization, straining small operators. Germany saw 4% fewer overall installs in 2024, yet digital orders rose 12% as firms pursued waste-cutting initiatives. The United States splits: large packaging houses pour money into high-speed inkjet, while many commercial shops sweat legacy offset assets. Canada consolidates as mid-sized printers fold or merge.

South America, the Middle East, and Africa hold the rest. Brazil invests in flexo for food packaging but fights import-cost volatility. Saudi Arabia backs local printing under Vision 2030 with soft loans for presses. The United Arab Emirates markets free-zone print hubs to serve Gulf and Africa. South Africa grapples with energy costs but sees selective inkjet buys for pharma cartons, while Kenya scales packaging lines for regional consumer demand.

- Heidelberger Druckmaschinen AG

- Koenig and Bauer AG

- Bobst Group SA

- HP Inc.

- Canon Inc.

- Seiko Epson Corporation

- Fujifilm Holdings Corporation

- Ricoh Company Ltd.

- Electronics for Imaging, Inc.

- Durst Phototechnik AG

- Mark Andy Inc.

- Nilpeter A/S

- Gallus Ferd. Ruesch AG (Heidelberg)

- OMET S.r.l.

- MPS Systems B.V.

- Uteco Converting SpA

- Manroland Goss Web Systems GmbH

- Agfa-Gevaert Group NV

- Brother Industries Ltd.

- AB Graphic International Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Market Drivers

- 4.3.1 Regulatory Tailwinds for Food and Pharma Digital Labels

- 4.3.2 On-Demand Book and Packaging Runs Driving CAPEX

- 4.3.3 Brand-Owner Push for SKU Proliferation

- 4.3.4 Hybrid Press Adoption Cuts Total Cost of Ownership

- 4.3.5 AI-Based Predictive Maintenance Reduces Press Downtime

- 4.3.6 Rise of Decentralised Micro-Factories Near End Users

- 4.4 Market Restraints

- 4.4.1 Volatile Graphic-Paper Prices Squeeze Margins

- 4.4.2 Skilled Press-Operator Shortage

- 4.4.3 Escalating Cyber-Security Risks in Cloud-Connected Presses

- 4.4.4 PFAS Regulations Limiting Certain Ink Chemistries

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Technology

- 5.1.1 Web-offset Lithographic

- 5.1.2 Flexographic

- 5.1.3 Gravure

- 5.1.4 Screen Printing

- 5.1.5 Digital

- 5.2 By Equipment Type

- 5.2.1 Pre-press Systems

- 5.2.2 Press(Sheet-fed, Roll-fed)

- 5.2.3 Post-press and Finishing

- 5.2.4 Ancillary and Inline Converting

- 5.3 By Application

- 5.3.1 Books and Publishing

- 5.3.2 Advertising and Signage

- 5.3.3 Security and Transactional

- 5.3.4 Packaging

- 5.3.5 Other Applications

- 5.4 By End-User Industry

- 5.4.1 Packaging Converters

- 5.4.2 Commercial Printers

- 5.4.3 In-plant/Corporate

- 5.4.4 Quick Print and Copy Shops

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Spain

- 5.5.3.5 Italy

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 Australia

- 5.5.4.5 South Korea

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Kenya

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Heidelberger Druckmaschinen AG

- 6.4.2 Koenig and Bauer AG

- 6.4.3 Bobst Group SA

- 6.4.4 HP Inc.

- 6.4.5 Canon Inc.

- 6.4.6 Seiko Epson Corporation

- 6.4.7 Fujifilm Holdings Corporation

- 6.4.8 Ricoh Company Ltd.

- 6.4.9 Electronics for Imaging, Inc.

- 6.4.10 Durst Phototechnik AG

- 6.4.11 Mark Andy Inc.

- 6.4.12 Nilpeter A/S

- 6.4.13 Gallus Ferd. Ruesch AG (Heidelberg)

- 6.4.14 OMET S.r.l.

- 6.4.15 MPS Systems B.V.

- 6.4.16 Uteco Converting SpA

- 6.4.17 Manroland Goss Web Systems GmbH

- 6.4.18 Agfa-Gevaert Group NV

- 6.4.19 Brother Industries Ltd.

- 6.4.20 AB Graphic International Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

2026-2030年全球印刷設備市場

2026-2030年全球印刷設備市場 瓶子印刷機市場規模、佔有率和成長分析:按印刷技術、自動化程度、適用瓶材、終端用戶產業和地區分類-2026-2033年產業預測

瓶子印刷機市場規模、佔有率和成長分析:按印刷技術、自動化程度、適用瓶材、終端用戶產業和地區分類-2026-2033年產業預測 3D熱壓壓平機市場:依產品類型、操作模式、材料類型、壓制能力、應用和終端用戶產業分類,全球預測,2026-2032年輪轉印刷機市場:材料類型、印刷機類型、速度範圍、應用和最終用途產業分類-全球預測,2026-2032年

3D熱壓壓平機市場:依產品類型、操作模式、材料類型、壓制能力、應用和終端用戶產業分類,全球預測,2026-2032年輪轉印刷機市場:材料類型、印刷機類型、速度範圍、應用和最終用途產業分類-全球預測,2026-2032年 大幅面印表機(LFP):市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)

大幅面印表機(LFP):市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年) 2026年全球印刷檢測設備市場報告PCB SMT設備市場按設備類型、基板類型、吞吐量、產量和最終用途行業分類 - 全球預測(2026-2032年)按類型、連接方式、列印解析度、最終用戶和分銷管道分類的收據印表機市場—2026-2032年全球預測翻新印表機市場:依產品類型、組件、連接方式、功能、最終用戶和通路分類,全球預測,2026-2032年

2026年全球印刷檢測設備市場報告PCB SMT設備市場按設備類型、基板類型、吞吐量、產量和最終用途行業分類 - 全球預測(2026-2032年)按類型、連接方式、列印解析度、最終用戶和分銷管道分類的收據印表機市場—2026-2032年全球預測翻新印表機市場:依產品類型、組件、連接方式、功能、最終用戶和通路分類,全球預測,2026-2032年 印刷設備市場規模、佔有率和成長分析(按產品類型、業務類型、承印物類型、應用、最終用途和地區分類)-2026-2033年產業預測

印刷設備市場規模、佔有率和成長分析(按產品類型、業務類型、承印物類型、應用、最終用途和地區分類)-2026-2033年產業預測