|

市場調查報告書

商品編碼

1940738

大幅面印表機(LFP):市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)Large Format Printers (LFP) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

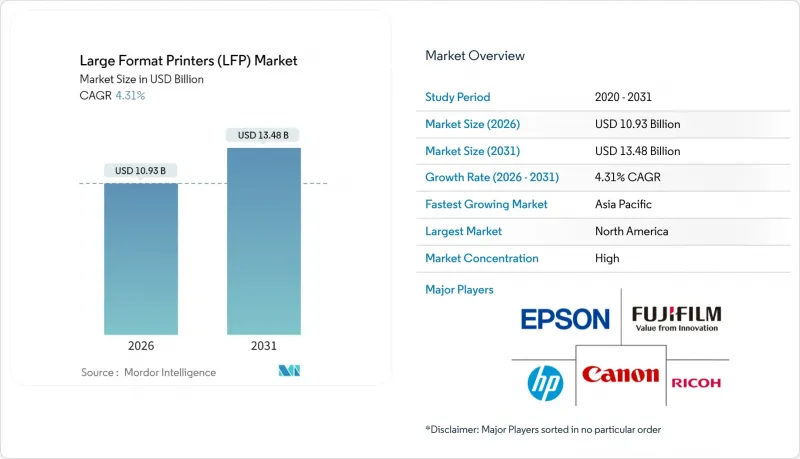

預計到 2026 年,大幅面印表機市場價值將達到 109.3 億美元,高於 2025 年的 104.8 億美元。

預計到 2031 年,該產業規模將達到 134.8 億美元,2026 年至 2031 年的複合年成長率為 4.31%。

這一成長軌跡反映出,印刷業經歷了快速擴張期,但隨著數位化包裝、紡織品個人化和高衝擊力標牌需求的融合,該行業正持續鞏固自身地位。高速紫外線固化系統、永續水性油墨的創新以及人工智慧驅動的工作流程自動化,在延長印表機使用壽命的同時,有效控制了營運成本。儘管北美地區仍保持主導地位,但亞太地區加速的資本投資和不斷壯大的製造業基地預示著未來五年產業格局將會轉變。競爭優勢將取決於整合硬體、軟體和經認證的環保油墨的端到端解決方案,使印刷服務供應商能夠在不犧牲品質的前提下,快速回應小批量、可變資料印刷作業。

全球大幅面印表機(LFP)市場趨勢與洞察

包裝、廣告和紡織品產業快速成長

預計印刷包裝市場將從2024年的5,120億美元成長到2029年的6,950億美元,複合年成長率(CAGR)為6.3%,成為大尺寸印表機市場最具影響力的需求促進因素。同時,隨著時尚品牌擴大採用小批量客製化,預計數位紡織品生產將從2024年的31億美元成長到2030年的79億美元,複合年成長率(CAGR)為14.9%。戶外媒體預算的復甦也推動了對耐用承印物的需求。這些趨勢共同促使供應商開發模組化印表機,使其能夠在單班制生產中處理瓦楞紙板、軟性薄膜和聚酯織物。Canon配備白色墨水的Colorado M系列印表機展現了混合列印功能的價值,實現了從原型製作到批量生產的無縫過渡。

採用紫外線固化和高速噴墨列印技術

由於其即時固化、廣泛的承印物相容性和低排放優點,UV固化設備在北美和歐洲正得到越來越廣泛的應用。Canon的UVgel系統和FUJIFILM的AQUAFUZE系統透過縮短印後加工時間和避免使用揮發性溶劑,提高了工廠的生產效率。Ricoh報告稱,受標牌和圖形需求激增的推動,其2024年第一季工業印刷硬體業務成長了32%。高速噴墨技術兼具接近膠印的列印速度和數位印刷的柔軟性,對於需要快速切換作業的大量商業印刷而言,尤其具有吸引力。因此,傳統的溶劑型設備正穩定地轉向具有自動化色彩管理功能的UV固化和水性技術。

數位電子看板的替代方案

預計2018年至2023年,印刷指示牌市場將以-2.2%的複合年成長率萎縮,規模將達到409億美元。同時,歐洲數字顯示市場正以每年約11%的速度成長。數位戶外廣告(DOOH)已佔戶外廣告(OOH)總收入的37%,在澳洲的滲透率高達76%。廣告商優先考慮即時內容更新和受眾分析,而印刷品無法提供這些功能。因此,在高流量交通樞紐,印刷廣告的投放量正在下降,而紙張和乙烯基材料仍然是成本敏感型或一次性宣傳活動的首選。這種限制正在影響大尺寸印表機市場,但也推動了混合宣傳活動的創新,將靜態背景與動態LED疊加層結合。

細分市場分析

到2025年,印表機將貢獻76.92%的收入,鞏固大幅面印表機市場的基礎。 UV固化引擎、混合式平板/捲筒系統以及能夠一次列印多種承印物的乳膠平台,正推動穩定的硬體需求。Canon、Epson和惠普正在擴展其白色墨水和螢光顏料的選擇範圍,使印表機能夠承接利潤更高的裝飾和包裝業務。持續的更新換代週期,使得大尺寸印表機市場始終處於資本預算的核心地位。

軟體收入雖然規模較小,但正以 5.63% 的複合年成長率成長,這主要得益於人工智慧驅動的作業分組、自動拼版和遠端設備健康監控等技術的普及。惠普 PrintOS、CanonPRISMA 和RicohTotalFlow 套件將獨立印表機轉變為雲端連接的生產節點。這項轉變表明,大尺寸印表機市場與工業 4.0 的理念高度契合,其價值不僅體現在機械輸出上,更體現在數據驅動的效率上。

預計到2025年,噴墨列印仍將佔據大幅面印表機市場47.74%的佔有率,這主要得益於其按需列印技術的多功能性和廣色域。噴墨列印可使用多種水性、乳膠、溶劑型和UV墨水,使用者可根據應用需求選擇最合適的墨水,使其成為標誌和裝飾應用領域的首選技術。

儘管目前規模較小,但隨著新一代靜電照相印刷機尺寸達到B2XL,預計到2031年,碳粉和雷射平台將以5.52%的複合年成長率成長。RicohPro C9500系列在複雜作業中可達到額定速度的97%,使其成為高印量商業印刷的理想選擇,因為在這些領域,運作的穩定性優於卷軸式介質的靈活性。噴墨和碳粉的共存表明,大尺寸印表機市場正在滿足多種作業需求,而非單一的主導技術。

區域分析

預計到2025年,北美將佔全球收入的40.86%,這主要得益於人工智慧工作流程的早期應用以及NESHAP(40 CFR Part 63)下嚴格的環境標準,該標準有利於低排放印表機的發展。對預測性維護的投資已將營運成本降低了10%至35%,從而在列印量下降的情況下保持了穩定的利潤率。華盛頓州等州的PFAS法規正在加速向相容的水性系統的升級,鞏固了支撐大幅面印表機市場的高階細分市場。亞太地區是成長最快的地區,預計到2031年將以5.48%的複合年成長率成長。根據FAPGA的報告,商業印刷市場預計將從2022年的1,846億美元成長到2031年的2,826億美元。

歐洲在永續性趨勢方面持續引領潮流。 2024/825 號指令禁止模糊的環境聲明,並強制規定可回收性閾值,引導買家使用不含 PFAS 的油墨和經 FSC 認證的基材。需要 ESG 報告審核追蹤的品牌所有者正在採用配備在線連續光強度和封閉回路型色彩引擎的印刷機。雖然成熟的需求放緩了整體成長速度,但早期合規投資正在支持服務合約和改造套件的銷售,從而擴大潛在市場規模。

南美洲和中東及非洲地區的貢獻較小,但為能夠提供可承受電壓波動和高溫的堅固耐用設備的供應商提供了機會。沿岸地區的體育場館和旅遊綜合體等大型企劃青睞高階UV混合印表機,而巴西的加工業者則在尋找經濟實惠的溶劑型印表機。隨著資金籌措通路的拓展,這些地區將推動大幅面印表機市場產量的成長。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 包裝、廣告和紡織領域的需求不斷成長

- 採用紫外線固化和高速噴墨列印技術

- ESG主導的向水性油墨轉型

- 中小型印刷廠的AI自動化工作流程

- 社區型「微型工廠」印刷中心的興起

- 用於乳製品替代品的無菌冷填充技術

- 市場限制

- 數位電子看板的替代方案

- 工業磷酸鐵鋰電池的高昂資本與營運成本

- PFAS-free油墨監理方面即將出現的空白

- 輕質玻璃技術降低了重量優勢

- 產業供應鏈分析

- 監管環境

- 技術展望

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 報價

- 印表機

- 軟體

- 服務

- 透過印刷技術

- 噴墨

- 墨粉/雷射

- 按墨水類型

- 水溶液

- 溶劑型及環保溶劑型

- 紫外線固化型

- 乳膠

- 染料昇華

- 按最終用戶行業分類

- 標誌和戶外廣告

- 服裝和紡織品

- 裝飾和室內圖形

- 電腦輔助設計/技術

- 包裝和標籤

- 其他終端用戶產業

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 智利

- 南美洲其他地區

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 馬來西亞

- 亞太其他地區

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東地區

- 非洲

- 南非

- 奈及利亞

- 其他非洲地區

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- HP Inc.

- Canon Inc.

- Seiko Epson Corporation

- Roland DG Corporation

- Mimaki Engineering Co., Ltd.

- Ricoh Company, Ltd.

- Agfa-Gevaert NV

- Durst Group AG

- Electronics For Imaging, Inc.(EFI)

- Konica Minolta, Inc.

- Kyocera Corporation

- Mutoh Holdings Co., Ltd.

- Fujifilm Holdings Corporation

- ColorJet Group

- SwissQprint AG

- JHF Group

- DGI Co., Ltd.

第7章 市場機會與未來展望

Large-format printers market size in 2026 is estimated at USD 10.93 billion, growing from 2025 value of USD 10.48 billion with 2031 projections showing USD 13.48 billion, growing at 4.31% CAGR over 2026-2031.

The growth path reflects a sector that has moved beyond rapid expansion yet continues to gain ground as packaging digitization, textile personalization, and high-impact signage demand converge. Faster UV-curable systems, sustainable water-based ink innovations, and AI-enabled workflow automation are extending printer lifecycles while keeping operating costs in check. Regional leadership remains with North America, but Asia Pacific's accelerating capital investment and expanding manufacturing base signal a shift in power over the next five years. Competitive differentiation hinges on end-to-end solutions that integrate hardware, software, and certified eco-inks, enabling print service providers to respond promptly to short-run, variable-data jobs without compromising quality.

Global Large Format Printers (LFP) Market Trends and Insights

Packaging, advertising and textile boom

Printed packaging is projected to expand from USD 512 billion in 2024 to USD 695 billion by 2029, at a 6.3% CAGR, making packaging the most influential demand driver for the large-format printers market. Simultaneously, digital textile output is projected to rise from USD 3.1 billion in 2024 to USD 7.9 billion in 2030, at a 14.9% CAGR, as fashion brands increasingly adopt short-run customization. Outdoor media budgets are rebounding, which elevates the need for high-durability substrates. Together, these trends push vendors to develop modular printers capable of handling corrugated board, flexible films, and polyester fabric in a single shift. Canon's Colorado M-series with white ink showcases the value of hybrid capability that seamlessly transitions between prototyping and production.

UV-curable and high-speed inkjet adoption

Immediate curing, broad substrate support, and low emissions drive the adoption of UV-curable installations in North America and Europe. Canon UVgel and Fujifilm AQUAFUZE systems reduce finishing times and eliminate volatile solvents, enhancing shop throughput. Ricoh reports that its industrial printing hardware grew 32% in Q1 2024, driven by surging sign-graphics demand. Print speeds that approach offset quality while retaining digital flexibility make high-speed inkjet technology attractive for high-volume commercial work, especially where quick job changeovers are crucial. The outcome is a steady migration away from legacy solvent machines toward UV-curable and aqueous technologies with automated color control.

Digital signage substitution

Printed signage contracted at a -2.2% CAGR between 2018 and 2023 to USD 40.9 billion, while digital displays gained roughly 11% annually in Europe. Digital out-of-home already secures 37% of total OOH revenue and holds 76% penetration in Australia. Advertisers value real-time content updates and audience analytics that print cannot match. As a result, print volumes fall in high-traffic transit hubs, although cost-sensitive or temporary campaigns still favor paper or vinyl. The restraint pulls on the large-format printers market yet sparks innovation in hybrid campaigns that pair static backdrops with active LED overlays.

Other drivers and restraints analyzed in the detailed report include:

- ESG-driven shift to water-based inks

- AI-automated workflow for SMB print shops

- High cap-ex and opex of industrial LFPs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Printers generated 76.92% of revenue in 2025, anchoring the large format printers market. Hardware demand remains stable, thanks to UV-curable engines, hybrid flatbed-roll systems, and latex platforms that handle diverse substrates in a single pass. Canon, Epson, and HP expand their white-ink and neon pigment options, allowing print shops to pursue higher-margin decor and packaging work. Ongoing replacement cycles sustain the large-format printers market size at the core of capital budgets.

Software revenue, though smaller, is rising at a 5.63% CAGR as AI-driven job ganging, automatic imposition, and remote device health monitoring gain traction. HP PrintOS, Canon PRISMA, and Ricoh TotalFlow suites convert stand-alone printers into cloud-linked production nodes. The shift illustrates how the large-format printers market aligns with Industry 4.0, where value resides in data-enabled efficiency as much as in mechanical output.

Inkjet maintained a 47.74% market share of the large-format printers market in 2025, driven by the versatility of drop-on-demand technology and its wide color gamut. Water-based, latex, solvent, and UV variations enable users to tailor fluids to meet end-use requirements, making inkjet the default technology for signage and decor.

Toner and laser platforms, although smaller, are projected to show a 5.52% CAGR through 2031 as next-generation electrophotographic presses reach B2XL sizes. Ricoh's Pro C9500 series achieves a 97% rated speed on complex jobs, making it an attractive option for high-volume commercial runs where uptime consistency outweighs the benefits of roll-to-roll media freedom. The coexistence of inkjet and toner confirms that the large-format printers market serves multiple job profiles rather than a single dominant method.

The Large Format Printers Market Report is Segmented by Offering (Printers, Software, and Services), Printing Technology (Inkjet, and Toner/Laser), Ink Type (Aqueous, Solvent and Eco-Solvent, UV-Curable, Latex, and Dye-Sublimation), End-User Industry (Signage and Outdoor Advertising, Apparel and Textiles, Decor and Interior Graphics, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America accounted for 40.86% of revenue in 2025, driven by the early adoption of AI-enabled workflows and stringent environmental standards under NESHAP 40 CFR Part 63, which rewards low-emission printers. Investments in predictive maintenance deliver 10-35% operating cost reductions, keeping profit margins resilient even as print runs shrink. PFAS limits in states such as Washington accelerate upgrades to compliant water-based systems, solidifying a premium segment that underpins the large-format printers market. The Asia Pacific is the fastest-growing region, with a 5.48% CAGR projected to 2031. FAPGA reports that commercial printing is expected to expand from USD 184.6 billion in 2022 to USD 282.6 billion in 2031.

Europe remains a sustainability trendsetter. Directive 2024/825 bans vague green claims and enforces recyclability thresholds, steering buyers toward PFAS-free inks and FSC-certified substrates. Printers equipped with inline spectrophotometers and closed-loop color engines gain acceptance among brand owners who require audit trails for ESG reporting. While mature demand keeps overall growth modest, early compliance spend supports service contracts and retrofit kits, enriching the total addressable opportunity.

South America, the Middle East, and Africa contribute smaller shares, yet present opportunities for suppliers that can deliver rugged devices tolerant of voltage swings and heat. Mega-projects in the Gulf, such as stadiums and tourism complexes, favor high-end UV hybrids, whereas Brazilian converters seek cost-effective solvent units. As financing options widen, these territories will add incremental tonnage to the large-format printers market.

- HP Inc.

- Canon Inc.

- Seiko Epson Corporation

- Roland DG Corporation

- Mimaki Engineering Co., Ltd.

- Ricoh Company, Ltd.

- Agfa-Gevaert NV

- Durst Group AG

- Electronics For Imaging, Inc. (EFI)

- Konica Minolta, Inc.

- Kyocera Corporation

- Mutoh Holdings Co., Ltd.

- Fujifilm Holdings Corporation

- ColorJet Group

- SwissQprint AG

- JHF Group

- DGI Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Packaging, Advertising and Textile Boom

- 4.2.2 UV-curable and High-speed Inkjet Adoption

- 4.2.3 ESG-Driven Shift to Water-based Inks

- 4.2.4 AI-Automated Workflow for SMB Print Shops

- 4.2.5 Rise of Localised "Micro-Factory" Print Hubs

- 4.2.6 Aseptic cold-fill for dairy-alternatives

- 4.3 Market Restraints

- 4.3.1 Digital Signage Substitution

- 4.3.2 High Cap-Ex and Opex of Industrial LFPs

- 4.3.3 Looming PFAS-Free Ink Compliance Gap

- 4.3.4 Lightweight glass tech eroding weight edge

- 4.4 Industry Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Offering

- 5.1.1 Printers

- 5.1.2 Software

- 5.1.3 Services

- 5.2 By Printing Technology

- 5.2.1 Inkjet

- 5.2.2 Toner / Laser

- 5.3 By Ink Type

- 5.3.1 Aqueous

- 5.3.2 Solvent and Eco-Solvent

- 5.3.3 UV-curable

- 5.3.4 Latex

- 5.3.5 Dye-Sublimation

- 5.4 By End-user Industry

- 5.4.1 Signage and Outdoor Advertising

- 5.4.2 Apparel and Textiles

- 5.4.3 Decor and Interior Graphics

- 5.4.4 CAD and Technical

- 5.4.5 Packaging and Labels

- 5.4.6 Other End-user Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Chile

- 5.5.2.4 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Malaysia

- 5.5.4.7 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 HP Inc.

- 6.4.2 Canon Inc.

- 6.4.3 Seiko Epson Corporation

- 6.4.4 Roland DG Corporation

- 6.4.5 Mimaki Engineering Co., Ltd.

- 6.4.6 Ricoh Company, Ltd.

- 6.4.7 Agfa-Gevaert NV

- 6.4.8 Durst Group AG

- 6.4.9 Electronics For Imaging, Inc. (EFI)

- 6.4.10 Konica Minolta, Inc.

- 6.4.11 Kyocera Corporation

- 6.4.12 Mutoh Holdings Co., Ltd.

- 6.4.13 Fujifilm Holdings Corporation

- 6.4.14 ColorJet Group

- 6.4.15 SwissQprint AG

- 6.4.16 JHF Group

- 6.4.17 DGI Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

2026-2030年全球印刷設備市場

2026-2030年全球印刷設備市場 瓶子印刷機市場規模、佔有率和成長分析:按印刷技術、自動化程度、適用瓶材、終端用戶產業和地區分類-2026-2033年產業預測

瓶子印刷機市場規模、佔有率和成長分析:按印刷技術、自動化程度、適用瓶材、終端用戶產業和地區分類-2026-2033年產業預測 印刷設備:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

印刷設備:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 3D熱壓壓平機市場:依產品類型、操作模式、材料類型、壓制能力、應用和終端用戶產業分類,全球預測,2026-2032年輪轉印刷機市場:材料類型、印刷機類型、速度範圍、應用和最終用途產業分類-全球預測,2026-2032年

3D熱壓壓平機市場:依產品類型、操作模式、材料類型、壓制能力、應用和終端用戶產業分類,全球預測,2026-2032年輪轉印刷機市場:材料類型、印刷機類型、速度範圍、應用和最終用途產業分類-全球預測,2026-2032年 2026年全球印刷檢測設備市場報告PCB SMT設備市場按設備類型、基板類型、吞吐量、產量和最終用途行業分類 - 全球預測(2026-2032年)按類型、連接方式、列印解析度、最終用戶和分銷管道分類的收據印表機市場—2026-2032年全球預測翻新印表機市場:依產品類型、組件、連接方式、功能、最終用戶和通路分類,全球預測,2026-2032年

2026年全球印刷檢測設備市場報告PCB SMT設備市場按設備類型、基板類型、吞吐量、產量和最終用途行業分類 - 全球預測(2026-2032年)按類型、連接方式、列印解析度、最終用戶和分銷管道分類的收據印表機市場—2026-2032年全球預測翻新印表機市場:依產品類型、組件、連接方式、功能、最終用戶和通路分類,全球預測,2026-2032年 印刷設備市場規模、佔有率和成長分析(按產品類型、業務類型、承印物類型、應用、最終用途和地區分類)-2026-2033年產業預測

印刷設備市場規模、佔有率和成長分析(按產品類型、業務類型、承印物類型、應用、最終用途和地區分類)-2026-2033年產業預測